Pakistan's Automotive Industry: 3 N

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Contacts in Japan Contacts in Asia

TheDirectoryof JapaneseAuto Manufacturers′ WbrldwidePurchaslng ● Contacts ● トOriginalEqulpment ● トOriginalEqulpment Service トAccessories トMaterials +RmR JA払NAuTOMOBILEMANUFACTURERSAssocIATION′INC. DAIHATSU CONTACTS IN JAPAN CONTACTS IN ASIA OE, Service, Accessories and Material OE Parts for Asian Plants: P.T. Astra Daihatsu Motor Daihatsu Motor Co., Ltd. JL. Gaya Motor 3/5, Sunter II, Jakarta 14350, urchasing Div. PO Box 1166 Jakarta 14011, Indonesia 1-1, Daihatsu-cho, Ikeda-shi, Phone: 62-21-651-0300 Osaka, 563-0044 Japan Fax: 62-21-651-0834 Phone: 072-754-3331 Fax: 072-751-7666 Perodua Manufacturing Sdn. Bhd. Lot 1896, Sungai Choh, Mukim Serendah, Locked Bag No.226, 48009 Rawang, Selangor Darul Ehsan, Malaysia Phone: 60-3-6092-8888 Fax: 60-3-6090-2167 1 HINO CONTACTS IN JAPAN CONTACTS IN ASIA OE, Service, Aceessories and Materials OE, Service Parts and Accessories Hino Motors, Ltd. For Indonesia Plant: Purchasing Planning Div. P.T. Hino Motors Manufacturing Indonesia 1-1, Hinodai 3-chome, Hino-shi, Kawasan Industri Kota Bukit Indah Blok D1 No.1 Tokyo 191-8660 Japan Purwakarta 41181, Phone: 042-586-5474/5481 Jawa Barat, Indonesia Fax: 042-586-5477 Phone: 0264-351-911 Fax: 0264-351-755 CONTACTS IN NORTH AMERICA For Malaysia Plant: Hino Motors (Malaysia) Sdn. Bhd. OE, Service Parts and Accessories Lot P.T. 24, Jalan 223, For America Plant: Section 51A 46100, Petaling Jaya, Hino Motors Manufacturing U.S.A., Inc. Selangor, Malaysia 290 S. Milliken Avenue Phone: 03-757-3517 Ontario, California 91761 Fax: 03-757-2235 Phone: 909-974-4850 Fax: 909-937-3480 For Thailand Plant: Hino Motors Manufacturing (Thailand)Ltd. -

Table of Contents

TABLE OF CONTENTS Acknowledgements Dedication Executive Summary ----------------------------------------- 01 Chapter 1 (Introduction) ---------------------------------------- 03 Chapter 2 (Industry Overview) --------------------------------------- 08 Chapter 3 (Company Analysis) ---------------------------------------- 15 Existing Product line ---------------------------------------- 16 External Environment ---------------------------------------- 21 Internal Environment ---------------------------------------- 51 SWOT Analysis ---------------------------------------- 67 Growth-share matrix ---------------------------------------- 75 PEST Analysis ---------------------------------------- 78 Customer Environment ---------------------------------------- 81 Marketing Strategies ---------------------------------------- 91 Marketing Mix --------------------------------------- 94 Chapter 4 (Competitor Analysis) ---------------------------------------- 101 SWOT ---------------------------------------- 102 Marketing control ---------------------------------------- 108 Target Market ---------------------------------------- 110 Marketing Mix ---------------------------------------- 112 Chapter 5 (Scenarios) ---------------------------------------- 115 Scenario 1 ---------------------------------------- 116 Scenario 2 ---------------------------------------- 118 Chapter 6 (Recommendations) ---------------------------------------- 119 Appendices ----------------------------------------- 122 ACKNOWLEDGEMENTS We feel blessed by the grace of God for -

Master List of DTP Participants

Institute of Business Administration, Karachi Center for Executive Education Directors' Training Program Certification Year - No Program Name Designation Organization No. Certitied CCL Pharmaceuticals 215 IBA/DTP - 0213 2019 Dr. Shahzad Khan Chief Operating Officer CCL Pharmaceuticals Pvt Ltd Pvt Ltd 216 IBA/DTP - 0214 2019 IBA-Karachi Faisal Jalal IBA Faculty IBA-Karachi 217 IBA/DTP - 0215 2019 Self Lubna Pathan Director own Business 218 IBA/DTP - 0216 2019 Indus Clean Energy Masood Hasan Khan Head of Commercial Indus Clean Energy 219 IBA/DTP - 0217 2019 Avanceon Limited Naveed Ali Baig Director Avanceon Limited Senior Executive Vice President - 220 IBA/DTP - 0218 2019 Premier Insurance Nina Afridi Premier Insurance Head of HR & Administration 221 IBA/DTP - 0219 2019 Hinopak Motors Ltd. Yoshihiko Nanami President & CEO Hinopak Motors Ltd. 222 IBA/DTP - 0220 2019 Hinopak Motors Ltd. Shigeru Tsuchiya Executive Vice President Hinopak Motors Ltd. Vice President & Director 223 IBA/DTP - 0221 2019 Hinopak Motors Ltd. Takehito Sasaki Hinopak Motors Ltd. Production Vice President & Chief Financial 224 IBA/DTP - 0222 2019 Hinopak Motors Ltd. Fahim Aijaz Sabzwari Hinopak Motors Ltd. Officer 225 IBA/DTP - 0223 2019 Hinopak Motors Ltd. Naushad Riaz Vice President Hinopak Motors Ltd. 226 IBA/DTP - 0224 2019 Hinopak Motors Ltd. Syed Samad Siraj Deputy General Manager Hinopak Motors Ltd. 227 IBA/DTP - 0225 2019 Hinopak Motors Ltd. Muhammad Zahid Hasan Deputy General Manager Hinopak Motors Ltd. 228 IBA/DTP - 0226 2019 Hinopak Motors Ltd. Ahsan Waseem Akhtar Senior Manager HR, Admin & HSE Hinopak Motors Ltd. 229 IBA/DTP - 0227 2019 Hinopak Motors Ltd. Abdul Basit Departmental Head Finance Hinopak Motors Ltd. -

Jeenay Ke Rang

Jeenay ke rang Annual Report 2015 CONTENTS Company Information 03 Company Profile 05 The Mission 07 A Commitment to Excellence 09 Customer Service 09 People 10 Health, Safety & Environment 11 Berger Business Lines 13 Quality in Diversity 14 Decorative Paints 15 Automotive Paints 17 Powder Coatings 19 General Industrial Finishes 21 Protective Coatings 23 Vehicle Refinishes 23 Road Safety 24 Govt. & Marine 27 Construction Chemicals 27 Adhesives 28 Printing Inks 29 Marketing Activities 30 Corporate Activities 36 Financial Highlights 40 Directors’ Report 41 Pattern of Shareholding 45 Statement of Compliance 47 Review Report to the Members 49 Financial Statements Auditors’ Report to the Members 50 Balance Sheet 51 Profit and Loss Account 52 Statement of Comprehensive Income 53 Cash Flow Statement 54 Statement of Changes in Equity 55 Notes to the Financial Statement 56 Notice of Annual General Meeting 106 Consolidated Financial Statements Directors’ Report 110 Auditors’ Report to the Members 111 Consolidated Balance Sheet 112 Consolidated Profit and Loss Account 113 Consolidated Statement of Comprehensive Income 114 Consolidated Cash Flow Statement 115 Consolidated Statement of Changes in Equity 116 Notes to the Consolidated Financial Statement 117 Form of Proxy 01 02 Company Information Board of Directors Bankers Mr. Maqbool H. H. Rahimtoola - Chairman Al-Barka Bank Limited Dr. Mahmood Ahmad - Chief Executive Bank Al-Habib Limited Mr. Hamid Masood Sohail Faysal Bank Limited Mr. Muhammad Naseem Habib Bank Limited Mr. Ilyas Sharif Habib Metropolitan Bank Limited Mr. Shahzad M. Husain JS Bank Limited Mr. Zafar A. Osmani MCB Bank Limited Summit Bank Limited Audit Committee United Bank Limited Mr. -

World Bank Document

INTRODUCTION ______________________________________________________________________ The International Finance Corporation (IFC), part of the World Bank Group, is in the business of reducing Public Disclosure Authorized poverty and encouraging economic development in poorer countries through the private sector. IFC carries out this mandate primarily by investing in a wide variety of private projects in developing countries, always investing with other sponsors and financial institutions. These projects are selected first and foremost for their ability to contribute to economic growth and development. Obviously, to contribute effectively to development in the long run, IFC’s private sector projects must also be financially successful. Companies that are not financially viable clearly cannot contribute to development. IFC and its partners are, therefore, profit-seeking and take on the same risks as any private sector investor. Thus all IFC projects are screened not only for their likely contributions to development but also for the likelihood of their financial success. This screening, as it happens, is not simple. Projects have complicated effects on an economy and, more generally, on society as a whole. Usually, for example, projects directly create productive employment and better jobs in the business being financed. But employment effects are spread much more widely, as Public Disclosure Authorized increased business goes to suppliers or retailers and as new business is created elsewhere in the economy by employees spending their wages and salaries. There are many such effects, each difficult, if not impossible, to isolate from the investment. Because of these difficulties, most of these effects are not normally included in project analysis or decisionmaking but are nonetheless important in a development context. -

Poland Regional Cities-Comfort-Vehicle-List

Make Model Year Oldsmobile 19 Oldsmobile Alero Oldsmobile Aurora Oldsmobile Bravada Oldsmobile Cutlass Supreme Oldsmobile Intrigue Oldsmobile Silhouette Dodge Attitude Dodge Avenger 2013 Dodge Caliber Dodge Caravan 2015 Dodge Challenger Dodge Charger 2013 Dodge Dakota Dodge Dart 2015 Dodge Durango 2013 Dodge Grand Caravan 2015 Dodge Intrepid Dodge JCUV Dodge Journey 2013 Dodge Magnum 2013 Dodge Neon 2015 Dodge Nitro 2013 Dodge Ram 1500 Dodge Ram 2500 Dodge Ram 3500 Dodge Ram 4500 Dodge Ram 700 Dodge Ram Van 2015 Dodge Sprinter Dodge Stratus 2015 Dodge Stretch Limo Dodge Viper Dodge Vision Dodge i10 Land Rover Defender 2013 Land Rover Discovery 2013 Land Rover Freelander 2013 Land Rover Freelander 2 Land Rover LR2 Land Rover LR3 Land Rover LR4 Land Rover Range Rover 2013 Land Rover Range Rover Evoque 2013 Land Rover Range Rover Sport 2013 Land Rover Range Rover Velar 2013 Land Rover Range Rover Vogue 2013 Chevrolet Agile Chevrolet Astra 2015 Chevrolet Astro Chevrolet Avalanche 2013 Chevrolet Aveo Chevrolet Aveo5 Chevrolet Beat Chevrolet Blazer Chevrolet Bolt Chevrolet CMV Chevrolet Camaro Chevrolet Caprice Chevrolet Captiva 2013 Chevrolet Cavalier Chevrolet Celta Chevrolet Chevy Chevrolet City Express Chevrolet Classic Chevrolet Cobalt 2015 Chevrolet Colorado Chevrolet Corsa Chevrolet Corsa Sedan Chevrolet Corsa Wagon Chevrolet Corvette Chevrolet Corvette ZR1 Chevrolet Cruze 2015 Chevrolet Cruze Sport6 Chevrolet Dmax Chevrolet Enjoy Chevrolet Epica 2013 Chevrolet Equinox 2013 Chevrolet Esteem Chevrolet Evanda 2013 Chevrolet Exclusive Chevrolet -

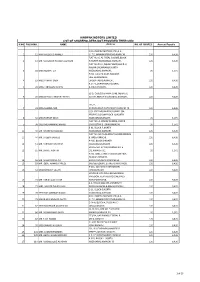

Hinopak Motors Limited List of Shareholders Not Provided Their Cnic S.No Folio No

HINOPAK MOTORS LIMITED LIST OF SHAREHOLDERS NOT PROVIDED THEIR CNIC S.NO FOLIO NO. NAME Address NO. OF SHARES Amount Payable C/O HINOPAK MOTORS LTD.,D-2, 1 12 MIR MAQSOOD AHMED S.I.T.E.,MANGHOPIR ROAD,KARACHI., 120 6,426 FLAT NO. 6, AL-FAZAL SQUARE,BLOCK- 2 13 MR. MANZOOR HUSSAIN QURESHI H,NORTH NAZIMABAD,KARACHI., 120 6,426 FLAT NO.19-O, IQBAL PLAZA,BLOCK-O, NAGAN CHOWRANGI,NORTH 3 18 MISS NUSRAT ZIA NAZIMABAD,KARACHI., 20 1,071 H.NO. E-13/40,NEAR RAILWAY LINE,GHARIBABAD, 4 19 MISS FARHAT SABA LIAQUATABAD,KARACHI., 120 6,426 R.177-1,SHARIFABADFEDERAL 5 24 MISS TABASSUM NISHAT B.AREA,KARACHI., 120 6,426 52-D, Q-BLOCK,PAHAR GANJ, NEAR LAL 6 28 MISS SHAKILA ANWAR FATIMA KOTTHI,NORTH NAZIMABAD,KARACHI., 120 6,426 171/2, 7 31 MISS SAMINA NAZ AURANGABAD,NAZIMABAD,KARACHI-18. 120 6,426 C/O. SYED MUJAHID HUSSAINP-394, PEOPLES COLONYBLOCK-N, NORTH 8 32 MISS FARHAT ABIDI NAZIMABADKARACHI, 20 1,071 FLAT NO. A-3FARAZ AVENUE, BLOCK- 9 38 SYED MOHAMMAD HAMID 20GULISTAN-E-JOHARKARACHI, 20 1,071 B-91, BLOCK-P,NORTH 10 40 MR. KHURSHID MAJEED NAZIMABAD,KARACHI. 120 6,426 FLAT NO. M-45,AL-AZAM SQUARE,FEDRAL 11 44 MR. SALEEM JAWEED B. AREA,KARACHI., 120 6,426 A-485, BLOCK-DNORTH 12 51 MR. FARRUKH GHAFFAR NAZIMABADKARACHI. 120 6,426 HOUSE NO. D/401,KORANGI NO. 5 13 55 MR. SHAKIL AKHTAR 1/2,KARACHI-31. 20 1,071 H.NO. 3281, STREET NO.10,NEW FIDA HUSSAIN SHAIKHA 14 56 MR. -

Mv680491 Arizona Department of Transportation Mv579d Motor Vehicle Division 1801 West Jefferson Phoenix, Arizona 85001 May 2011

MV680491 ARIZONA DEPARTMENT OF TRANSPORTATION MV579D MOTOR VEHICLE DIVISION 1801 WEST JEFFERSON PHOENIX, ARIZONA 85001 MAY 2011 2011 LICENSED AUTOMOTIVE RECYCLER -- AR BROKER -- B DISTRIBUTOR -- DS MOBILE HOME DEALER FOR PLATES ONLY -- M MANUFACTURER -- MF NEW MOTOR VEHICLE DEALER -- N TITLE SERVICE COMPANY -- TS USED MOTOR VEHICLE DEALER -- U WHOLESALE AUCTION DEALER -- WA WHOLESALE MOTOR VEHICLE DEALER -- WD - 1- LICENSE DEALERSHIP NAME AND ADDRESS PHONE NO EXP DATE PRODUCTS AUTHORIZED TO SELL _______ ___________________________ ________ __________ ___________________________ ------ AR ------ L00000021 A A A 20TH STREET AUTO WRECKING INC 6022582020 12/31/2011 (AR112) 3244 S 40TH ST PHOENIX AZ 850401623 L00000057 A A NATIONAL TOWING AUTO PARTS 6022725331 12/31/2011 (AR165) 3410 W WASHINGTON ST PHOENIX AZ 850094705 P O BOX 42321 PHOENIX AZ 85080 L00000175 A AND S AUTO WRECKING 6022439119 12/31/2011 (AR458) 2449 W BROADWAY RD PHOENIX AZ 850412003 L00000125 A C S AUTO WRECKING ** DBA: MUNCHINO INVESTMENT INC L00000302 A TO Z AUTO RECYCLER 6022721680 12/31/2011 (AR595) 2724 W BUCKEYE RD PHOENIX AZ 850095742 L00010226 A-Z QUALITY AUTO AND TRUCK PARTS LLC 6022684558 03/31/2012 2149 W BROADWAY RD # 2 PHOENIX AZ 850412107 L00010579 A-1 TRUCK AND VAN WRECKING 4809830511 12/31/2011 1708 S TOMAHAWK RD APACHE JUNCTION AZ 851197780 7325 E NOPAL AVE MESA AZ 85209 L00008372 AA AUTO PARTS ** DBA: G S FUTURES LLC - 2- LICENSE DEALERSHIP NAME AND ADDRESS PHONE NO EXP DATE PRODUCTS AUTHORIZED TO SELL _______ ___________________________ ________ __________ -

History of Pakistan's Automobile Industry

History of Pakistan’s Automobile Industry Following international trends, the automobile industry in Pakistan showed substantial growth in the years under review. The growth was aided by favorable government policies during this period and levy of lower import duties on raw material inputs and on intermediate products. A significant rise in demand for automobiles, propelled at least partly by easy availability of auto leases and loans from banks and leasing companies at low financial cost, was instrumental in the fast growth of the sector. The expansion in the sector, besides boosting the country‟s industrial output, also provided significant direct and indirect employment opportunities. In the past years, there has been a high growth of more than 40 percent per year in the automobile market. The growth declined somewhat in 2008 and 2009 due mainly to a dip in demand because of rising prices and lease financing becoming expensive for the consumers. Pakistan Car Industry The first automobile plant was set up in May 1949 by General Motor & Sales Co. It was set up on an experimental basis, however grew into an assembly plant. Seeing such progress, three major auto manufacturers from the US collaborated with Pakistani business men to set up; Ali Automobiles to manufacture Ford Products in 1955, Haroon Industries to assemble Chrysler Dodge cars in 1956, Khandawalla Industries to assemble American Motor Products in 1962, and Mack Trucks Plant in 1963. However towards the end of the seventies all automobile assembly in Pakistan stopped, until 1983 when Pak Suzuki started manufacturing their vehicles in Pakistan. Further Toyota Indus Motors was set up in 1990, followed by Honda. -

Topline Market Review P

Pakistan Weekly January 12, 2018 REP‐057 Topline Market Review Gains erode as profit taking ensues KSE‐100 Index +1.0 % WoW; Weekly net FIPI US$26mn Topline Research Best Local Brokerage House [email protected] Brokers Poll 2011-14, 2016-17 Tel: +9221‐35303330, Ext: 133 Topline Securities, Pakistan www.jamapunji.pk Best Local Brokerage House 2015-16 Index gains 1% in outgoing week as profit taking ensues Market Weekly Data KSE Volume & Value KSE‐100 Index 42,933.72 (Shares mn) Volume Value (US$mn) 330 150 1‐Week Change (%) 1.0% 260 Market Cap (Rs tn) 8.9 106 190 1‐Week Change (%) 0.2% 63 Market Cap (US$ bn) 80.6 120 1‐Week Change (%) 0.2% 50 20 18 18 18 18 18 ‐ ‐ 1‐Week Avg. Daily Vol (shares mn) 276.4 ‐ ‐ ‐ n n n n n aa aa aa aa aa J J J J J ‐ ‐ 1‐Week Avg. Daily Value (Rs bn) 12.2 ‐ ‐ ‐ 9 8 1‐Week Avg. Daily Value (US$ mn) 110.2 10 11 12 Source: PSX Source: PSX Outgoing week saw the culmination of the Santa Clause rally which commenced on December 20, 2017 and peaked on Jan 10, 2018 with a net gain of 14%. Since then index has had red two sessions correcting 2%/697pts, which has trimmed weekly gains to 1%/410pts with the index closing the week at 42,934pts level. Going forward, equities maybe further pressured as agitation movement by opposition parties begin on Jan 17 to protest against the Model Town. PtiitiParticipation idimproved siifitlignificantlyasprofitswerebkdbooked, average volumes idincreased 30% WWWoW whilevalue rose 44%. -

PACRA Assigns Initial Ratings to Ghandhara Nissan Limited

T P C R A L NL FY - 2020 - 332 Mr. Ahmed Kuli Khan Khattak Confidential CEO Dec 13, 2019 Ghandhara Nissan Limited Karachi G N L R | U Dear Sir This is with reference to Ratings of Ghandhara Nissan Limited . PACRA has updated its opinions, following are the respective details. Opinion Action Rating Outlook Opinion Type Long Term Short Term Current Previous Current Previous Ghandhara Nissan Limited Maintain A A A1 A1 Stable Entity Yours truly (Muhammad Jhangeer Hanif) Unit Head | Ratings The Pakistan Credit Rating Agency Limited [PACRA] TEL: 92(42)3586 9504 Awami Complex FB-1, Usman Block, New Garden Town Fax: 92(42)3583 0425 Lahore - 54600, Pakistan www.pacra.com The Pakistan Credit Rating Agency Limited Rating Report Report Contents 1. Rating Analysis Ghandhara Nissan Limited 2. Financial Information 3. Rating Scale 4. Regulatory and Supplementary Disclosure Rating History Dissemination Date Long Term Rating Short Term Rating Outlook Action Rating Watch 13-Dec-2019 A A1 Stable Maintain - 13-Jun-2019 A A1 Stable Maintain - 12-Dec-2018 A A1 Stable Maintain - 30-Jun-2018 A A1 Stable Maintain - 29-Dec-2017 A A1 Stable Initial - Rating Rationale and Key Rating Drivers Ghandhara Nissan Limited (GNL) operates in the truck segment of the automobile sector. Presently, the company deals in Chinese and European brands. Company's performance was diluted owing to discontinuation of UD Trucks, which they managed to beef up with other alternative products. Ghandhara Nissan has solidified its position in the market through the launch of JAC X-200 and Renault Trucks, recently. -

Board of Directors

8 Board of Directors Mr. Yusuf H. Shirazi Chairman Mr. Shirazi is a Law graduate (LLB) with BA (Hons) and JD (Diploma in Journalism) from Punjab University and AMP Harvard. He served in the financial services of the Central Superior Services of Pakistan for eight years. He is the author of five books including ‘Aid or Trade’ adjudged by the Writers Guild as the best book of the year and continues to be a columnist, particularly on economy. Mr. Shirazi is the Chairman of Atlas Group, which among others, has joint ventures with Honda, GS Yuasa, MAN and Total. He has been the President Karachi Chamber of Commerce and Industries for two terms. He has been the founder member of Karachi Stock Exchange, Lahore Stock Exchange and International Chamber of Commerce and Industry. He has been on the Board of Harvard Business School Alumni Association and is the Founder President of Harvard Club of Pakistan and Harvard Business School Club of Pakistan. He has been a visiting Faculty Member at National Defense College, Navy War College and Pakistan Administrative Staff College. He has been on the Board of Governors of LUMS, GIK and FC College. Previously he also served, among others on the Board of Fauji Foundation Institute of Management and Computer Sciences (FFIMCS) and Institute of Space Technology - Space & Upper Atmosphere Research Commission (SUPARCO). Mr.Takeharu Aoki President & CEO Mr. Aoki is President & Chief Executive Officer (CEO) of Honda Atlas Cars (Pakistan) Ltd. He has been associated with Honda Motor Company Limited, Japan for last 22 years and has rich experience of Sales & Marketing.