Dēmos Fact Sheet the COLOR of DEBT: Credit Card Debt by Race and Ethnicity

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and Innovation

U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities A Financial System That T OF EN TH M E A Financial System T T R R A E P A E S That Creates Economic Opportunities D U R E Y H T Nonbank Financials, Fintech, 1789 and Innovation Nonbank Financials, Fintech, and Innovation Nonbank Financials, Fintech, TREASURY JULY 2018 2018-04417 (Rev. 1) • Department of the Treasury • Departmental Offices • www.treasury.gov U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and Innovation Report to President Donald J. Trump Executive Order 13772 on Core Principles for Regulating the United States Financial System Steven T. Mnuchin Secretary Craig S. Phillips Counselor to the Secretary T OF EN TH M E T T R R A E P A E S D U R E Y H T 1789 Staff Acknowledgments Secretary Mnuchin and Counselor Phillips would like to thank Treasury staff members for their contributions to this report. The staff’s work on the report was led by Jessica Renier and W. Moses Kim, and included contributions from Chloe Cabot, Dan Dorman, Alexan- dra Friedman, Eric Froman, Dan Greenland, Gerry Hughes, Alexander Jackson, Danielle Johnson-Kutch, Ben Lachmann, Natalia Li, Daniel McCarty, John McGrail, Amyn Moolji, Brian Morgenstern, Daren Small-Moyers, Mark Nelson, Peter Nickoloff, Bimal Patel, Brian Peretti, Scott Rembrandt, Ed Roback, Ranya Rotolo, Jared Sawyer, Steven Seitz, Brian Smith, Mark Uyeda, Anne Wallwork, and Christopher Weaver. ii A Financial System That Creates Economic -

Adjustable-Rate Mortgage (ARM) Is a Loan with an Interest Rate That Changes

The Federal Reserve Board Consumer Handbook on Adjustable-Rate Mortgages Board of Governors of the Federal Reserve System www.federalreserve.gov 0412 Consumer Handbook on Adjustable-Rate Mortgages | i Table of contents Mortgage shopping worksheet ...................................................... 2 What is an ARM? .................................................................................... 4 How ARMs work: the basic features .......................................... 6 Initial rate and payment ...................................................................... 6 The adjustment period ........................................................................ 6 The index ............................................................................................... 7 The margin ............................................................................................ 8 Interest-rate caps .................................................................................. 10 Payment caps ........................................................................................ 13 Types of ARMs ........................................................................................ 15 Hybrid ARMs ....................................................................................... 15 Interest-only ARMs .............................................................................. 15 Payment-option ARMs ........................................................................ 16 Consumer cautions ............................................................................. -

Corporate Bonds and Debentures

Corporate Bonds and Debentures FCS Vinita Nair Vinod Kothari Company Kolkata: New Delhi: Mumbai: 1006-1009, Krishna A-467, First Floor, 403-406, Shreyas Chambers 224 AJC Bose Road Defence Colony, 175, D N Road, Fort Kolkata – 700 017 New Delhi-110024 Mumbai Phone: 033 2281 3742/7715 Phone: 011 41315340 Phone: 022 2261 4021/ 6237 0959 Email: [email protected] Email: [email protected] Email: [email protected] Website: www.vinodkothari.com 1 Copyright & Disclaimer . This presentation is only for academic purposes; this is not intended to be a professional advice or opinion. Anyone relying on this does so at one’s own discretion. Please do consult your professional consultant for any matter covered by this presentation. The contents of the presentation are intended solely for the use of the client to whom the same is marked by us. No circulation, publication, or unauthorised use of the presentation in any form is allowed, except with our prior written permission. No part of this presentation is intended to be solicitation of professional assignment. 2 About Us Vinod Kothari and Company, company secretaries, is a firm with over 30 years of vintage Based out of Kolkata, New Delhi & Mumbai We are a team of qualified company secretaries, chartered accountants, lawyers and managers. Our Organization’s Credo: Focus on capabilities; opportunities follow 3 Law & Practice relating to Corporate Bonds & Debentures 4 The book can be ordered by clicking here Outline . Introduction to Debentures . State of Indian Bond Market . Comparison of debentures with other forms of borrowings/securities . Types of Debentures . Modes of Issuance & Regulatory Framework . -

Interest-Rate-Growth Differentials and Government Debt Dynamics

From: OECD Journal: Economic Studies Access the journal at: http://dx.doi.org/10.1787/19952856 Interest-rate-growth differentials and government debt dynamics David Turner, Francesca Spinelli Please cite this article as: Turner, David and Francesca Spinelli (2012), “Interest-rate-growth differentials and government debt dynamics”, OECD Journal: Economic Studies, Vol. 2012/1. http://dx.doi.org/10.1787/eco_studies-2012-5k912k0zkhf8 This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. OECD Journal: Economic Studies Volume 2012 © OECD 2013 Interest-rate-growth differentials and government debt dynamics by David Turner and Francesca Spinelli* The differential between the interest rate paid to service government debt and the growth rate of the economy is a key concept in assessing fiscal sustainability. Among OECD economies, this differential was unusually low for much of the last decade compared with the 1980s and the first half of the 1990s. This article investigates the reasons behind this profile using panel estimation on selected OECD economies as means of providing some guidance as to its future development. The results suggest that the fall is partly explained by lower inflation volatility associated with the adoption of monetary policy regimes credibly targeting low inflation, which might be expected to continue. However, the low differential is also partly explained by factors which are likely to be reversed in the future, including very low policy rates, the “global savings glut” and the effect which the European Monetary Union had in reducing long-term interest differentials in the pre-crisis period. -

Sample Debt Validation Letter (Send Via Certified Mail, Return Receipt Requested)

Sample Debt Validation Letter (Send via certified mail, return receipt requested) Date: Your Name Your Address Your City, State, Zip Collection Agency Name Collection Agency Address Collection Agency City, State, Zip RE: Account # (Fill in Account Number) To Whom It May Concern: Be advised this is not a refusal to pay, but a notice that your claim is disputed and validation is requested. Under the Fair Debt collection Practices Act (FDCPA), I have the right to request validation of the debt you say I owe you. I am requesting proof that I am indeed the party you are asking to pay this debt, and there is some contractual obligation that is binding on me to pay this debt. This is NOT a request for “verification” or proof of my mailing address, but a request for VALIDATION made pursuant to 15 USC 1692g Sec. 809 (b) of the FDCPA. I respectfully request that your offices provide me with competent evidence that I have any legal obligation to pay you. At this time I will also inform you that if your offices have or continue to report invalidated information to any of the three major credit bureaus (Equifax, Experian, Trans Union), this action might constitute fraud under both federal and state laws. Due to this fact, if any negative mark is found or continues to report on any of my credit reports by your company or the company you represent, I will not hesitate in bringing legal action against you and your client for the following: Violation of the Fair Debt Collection Practices Act and Defamation of Character. -

Overdraft: Payment Service Or Small-Dollar Credit?

March 16, 2020 Overdraft: Payment Service or Small-Dollar Credit? Funding Gaps in Consumer Finances Figure 1. Annual Interest and Noninterest Income One of the earliest documented cases of bank overdraft U.S. Commercial Banks, 1970-2018 ($ millions) dates back to 1728, when a Royal Bank of Scotland customer requested a cash credit to allow him to withdraw more money from his account than it held. Three centuries later, technologies, such as electronic payments (e.g., debit cards) and automated teller machines (ATMs), changed the way consumers use funds for retail purchases, transacting more frequently and in smaller denominations. Accordingly, today’s financial institutions commonly offer point-of-sale overdraft services or overdraft protection in exchange for a flat fee around $35. Although these fees can be large relative to the transaction, alternative sources of short-term small-dollar funding, such as payday loans, deposit advances, and installment loans, can be costly as well. Congress has taken an interest in the availability and cost of providing consumers funds to meet Source: Federal Deposit Insurance Corporation (FDIC). their budget shortfalls. Legislation introduced in the 116th Congress (H.R. 1509/S. 656 and H.R. 4254/S. 1595) as well Banks generate noninterest income in a number of ways. as the Federal Reserve’s real-time payments initiative could For example, a significant source of noninterest income impact consumer use of overdraft programs in various comes from collecting fees for deposit accounts services, ways. (See “Policy Tools and Potential Outcomes” below such as maintaining a checking account, ATM withdrawals, for more information.) The policy debate around this or covering an overdraft. -

LOAN RATES America First Credit Union Offers Members Competitive Loan Rates, Listed Below

LOAN RATES America First Credit Union offers members competitive loan rates, listed below. The annual percentage rates (APR) quoted are based on approved credit. Rates may be higher, depending on your credit history and other underwriting factors. Our loan offices will discuss your application and available rates with you. Variable APRs may increase or decrease monthly. Go to americafirst.com or call 1-800-999-3961 for more information. EFFECTIVE: OCTOBER 1, 2021 VARIABLE APR FIXED APR FEE DISCLOSURES VEHICLE 2.99% - 18.00% 2.99% - 18.00% ANNUAL PERCENTAGE RATE (APR) FOR PURCHASES 60-MONTH DECLINING RATE AUTO N/A 3.24% - 18.00% When you open your account, the applicable APR is based on creditworthiness. SMALL RV LOAN 4.49% - 15.24% 5.49% - 16.24% After that, your APR will vary with the market based on the Prime Rate. RV LOAN 4.49% - 15.74% 5.49% - 16.74% APR FOR CASH ADVANCES & BALANCE TRANSFERS When you open your account, the applicable APR is based on creditworthiness. RV BALLOON N/A 5.49% - 6.74% After that, your APR will vary with the market based on the Prime Rate. PERSONAL 8.49% - 18.00% 9.49% - 18.00% HOW TO AVOID PAYING INTEREST ON PURCHASES LINE OF CREDIT 15.24% - 18.00% Your due date is the 28th day of each month. We will not charge any interest on the portion of the purchases balance that you pay by the due date each month. SHARE-SECURED LINE OF CREDIT 3.05% FOR CREDIT CARD TIPS FROM THE CONSUMER FINANCIAL PROTECTION CONSUMER SHARE LOAN + 3.00% BUREAU CREDIT BUILDER PLUS 10.00% To learn more about factors to consider when applying for or using a credit card, visit the Consumer Financial Protection Bureau at CERTIFICATE ACCOUNT * 3.00% consumerfinance.gov/learnmore. -

Stopping the Payday Loan Trap Alternatives That Work, Ones That Don’T

Stopping the payday Loan trap AlternAtives thAt Work, ones thAt Don’t NCLC® NATIONAL CONSUMER June 2010 L AW C E N T E R® © Copyright 2010, National Consumer Law Center, Inc. All rights reserved. About the Authors Lauren K. Saunders is the Managing Attorney of NCLC’s Washington, DC office, where she handles legislative, administrative and other advocacy efforts on behalf of low income consumers. She contributes to several NCLC publications, including Fair Credit Reporting, Fair Debt Collection and Consumer Banking and Payments Law. She graduated magna cum laude from Harvard Law School where she was an Executive Editor of the Harvard Law Review, and holds a Masters in Public Policy from Harvard’s Kennedy School of Government and a B.A., Phi Beta Kappa, from Stanford University. Leah A. Plunkett is a staff attorney at NCLC, where she focuses on predatory small dollar loans, auto policy, protection of exempt funds, and the consumer needs of domestic violence survivors. Before coming to NCLC, Leah clerked in the United States District Court for the District of Maryland and established the Youth Law Project at New Hampshire Legal Assistance. Leah is a cum laude graduate of Harvard Law School, where she was on the board of both the Harvard Legal Aid Bureau and HLS for Choice. Carolyn Carter is NCLC’s Deputy Director for Advocacy. She is a contributing author to Cost of Credit, Truth in Lending, Unfair and Deceptive Acts and Practices and several other NCLC treatises. Prior to joining NCLC, she worked for legal services programs in Ohio and Pennsylvania. -

Payday Lending in America

An overview from Oct 2013 Report 3 in the Payday Lending in America series Payday Lending in America: Policy Solutions Overview About 20 years ago, a new retail financial product, the payday loan, began to spread across the United States. It allowed a customer who wanted a small amount of cash quickly to borrow money and pledge a check dated for the next payday as collateral. Twelve million people now use payday loans annually, spending an average of $520 in interest to repeatedly borrow an average of $375 in credit. In the 35 states that allow this type of lump-sum repayment loan, customers end up having to borrow again and again—paying a fee each time. That is because repaying the loan in full requires about one-third of an average borrower’s paycheck, not leaving enough money to cover everyday living expenses without borrowing again. In Colorado, lump-sum payday lending came into use in 1992. The state was an early adopter of such loans, but the situation is now different. In 2010, state lawmakers agreed that the payday loan market in Colorado had failed and acted to correct it. Legislators forged a compromise designed to make the loans more affordable while granting the state’s existing nonbank lenders a new way to provide small-dollar loans to those with damaged credit histories. The new law changed the terms for payday lending from a single, lump-sum payment to a series of installment payments stretched out over six months and lowered the maximum allowable interest rates. As a result, borrowers in Colorado now pay an average of 4 percent of their paychecks to service the loans, compared with 36 percent under a conventional lump-sum payday loan model. -

MLA Faqs 08.22

Frequently Asked Questions about the Defense Department’s Military Lending Act Regulations The following is intended to help pawnbrokers prepare for the October 3, 2016 mandatory compliance date for the expanded Military Lending Act (MLA) regulations. This information is not intended as, and should not be used as, a substitute for guidance from your local lawyer. What is the Military Lending Act? The MLA was enacted by Congress in 2006, and the DOD adopted a regulation to implement it in 2007, but did not cover pawn transactions. The DOD expanded the scope of the regulation to cover additional consumer credit products on July 22, 2015 (“2015 regulation”), and specifically mentioned pawn transactions. When does compliance with the DOD’s 2015 regulation become mandatory for pawn transactions? October 3, 2016, unless extended by the DOD or otherwise by Congress or a court of law. What types of transactions does DOD’s expanded regulation govern? The 2015 regulation applies to pawns if the borrowers or pledgers are active duty service members, their spouse or other dependent who receives 51% or more of their support from the service member. These consumers are “covered borrowers”. No traditional non-recourse pawn transaction entered into before October 3, 2016 is affected by the 2015 regulation. The 2015 regulation does not affect pawns entered into before your customer became an active duty service member or dependent of one. What are the key requirements of DOD’s regulation? The 2015 regulation: • caps the maximum Annual Percentage Rate -

Nber Working Papers Series

NBER WORKING PAPERS SERIES WAS THERE A BUBBLE IN THE 1929 STOCK MARKET? Peter Rappoport Eugene N. White Working Paper No. 3612 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 February 1991 We have benefitted from comments made on earlier drafts of this paper by seminar participants at the NEER Summer Institute and Rutgers University. We are particularly indebted to Charles Calomiris, Barry Eicherigreen, Gikas Hardouvelis and Frederic Mishkiri for their suggestions. This paper is part of NBER's research program in Financial Markets and Monetary Economics. Any opinions expressed are those of the authors and not those of the National Bureau of Economic Research. NBER Working Paper #3612 February 1991 WAS THERE A BUBBLE IN THE 1929 STOCK MARKET? ABSTRACT Standard tests find that no bubbles are present in the stock price data for the last one hundred years. In contrast., historical accounts, focusing on briefer periods, point to the stock market of 1928-1929 as a classic example of a bubble. While previous studies have restricted their attention to the joint behavior of stock prices and dividends over the course of a century, this paper uses the behavior of the premia demanded on loans collateralized by the purchase of stocks to evaluate the claim that the boom and crash of 1929 represented a bubble. We develop a model that permits us to extract an estimate of the path of the bubble and its probability of bursting in any period and demonstrate that the premium behaves as would be expected in the presence of a bubble in stock prices. -

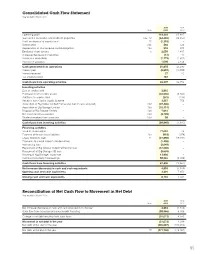

Reconciliation of Net Cash Flow to Movement in Net Debt Year Ended 31 March 2015

Consolidated Cash Flow Statement Year ended 31 March 2015 2015 2014 Note £000 £000 Operating profit 114,203 67,887 Gain on the revaluation of investment properties 13a, 14 (64,465) (28,350) Profit on disposal of surplus land 15 (1,318) – Depreciation 13b 566 526 Depreciation of finance lease capital obligations 13a 918 974 Employee share options 6 2,059 1,437 (Increase)/decrease in inventories (14) 10 Increase in receivables (1,172) (1,652) Increase in payables 1,098 2,458 Cash generated from operations 51,875 43,290 Interest paid (9,692) (10,558) Interest received 27 20 Tax credit received 187 – Cash flows from operating activities 42,397 32,752 Investing activities Sale of surplus land 2,815 – Purchase of non-current assets (42,555) (8,460) Additions to surplus land (231) (136) Receipts from Capital Goods Scheme 3,557 756 Acquisition of Big Yellow Limited Partnership (net of cash acquired) 13d (37,406) – Acquisition of Big Storage Limited 13a (15,114) – Disposal of Big Storage Limited 13a 7,614 – Net investment in associates 13d (3,709) – Dividend received from associate 13d 89 – Cash flows from investing activities (84,940) (7,840) Financing activities Issue of share capital 77,094 42 Payment of finance lease liabilities 13a (918) (974) Equity dividends paid 11 (27,890) (19,591) Payments to cancel interest rate derivatives (1,408) – Refinancing fees (2,649) – Repayment of Big Yellow Limited Partnership loan (57,000) – Repayment of Big Storage AIB loan (9,659) – Drawing of Big Storage Lloyds loan 13,900 – Increase/(reduction) in borrowings