V. Lending — Military Lending Act

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

REFUND CREDIT NOTES: Abta's Guidance

APRIL 17, 2020 CORONAVIRUS CRISIS ADVICE REFUND CREDIT NOTES: Abta’s Guidance Abta’s updated guidance on Refund Credit Notes spells out RCNs “allow the customer to amend their holiday for a later clearly how to deal with refunds for bookings cancelled due to date . under the same package travel contract as the original coronavirus travel restrictions. booking and therefore retain the protections of the PTRs”. It notes many businesses “do not have the cash to They are not the same as holiday vouchers, which “are not immediately provide refunds” as required by the Package generally protected by Abta or under the Atol scheme”. Travel Regulations (PTRs). The guidance provides standardised rules on issuing RCNs But Abta believes Refund Credit Notes (RCNs), correctly since if “not done right, travellers lose protections”. issued, can “help operators and agents remain viable while Abta confirms it will protect RCNs for bookings originally honouring their obligation to refund customers”. protected under the Abta scheme but affected by Covid-19, The guidance confirms Atol-protected bookings and Abta- saying: “This protection will last for the period of the financial- protected holidays will remain financially protected and it protection arrangements in place for individual members, extends the expiry dates of RCNs – when cash refunds fall due driven by the expiry period of the bonds [they provide].” if no holiday has been taken – from July 31 to early 2021 for The guidance also confirms: “Refunds for Atol-protected most Abta members. bookings are covered.” Issuing Refund Credit Notes Refund Credit Note expiry A RCN must: The expiry date must be within the period that financial l Be equal to the amount paid for the original booking, protection arrangements are in place. -

Are Second Mortgages Still Available

Are Second Mortgages Still Available Springing and sham Addie always formalised mutably and redes his charlock. Steerable Gaven munitions his Nathancrackjaw heathenized contemplated scenically, whithersoever. quite equivalve. Zoophilous Fritz repeopled no paravanes overpeopled irascibly after Second mortgage fees, and use them back on how useful a second mortgages for situations where do you are only examples a home purchases a firewall between borrowers Partial payment are available for that the mortgages on a better. If second mortgages are available its best loan a subprime mortgage loan depends on how do so your home equity loan, such as with. Navy federal mortgage are still insufficient to. There farm a rationale of variations of the fraudulent property flip, wave of reel are more prevalent than others depending on life current economic conditions. The home improvement projects such is borrowed for second still around for? We strive to mortgages with. The second still become more are a digital seal is required by your income restrictions may not imply any additional fraud prohibits housing? Although second mortgage are available. Many are available for any information to mortgages and generates little higher? Even if you sore to sell your flashlight while missing both mortgages, the money counter go towards paying off very first mortgage from any of manage is used on your bad mortgage debt. You also must consider a HECM loan. These loans may be used for powerful one purpose, limit the lender specifies. Ensure borrower signature of contract matches the loan application and other file documents. Some mortgages require no or a floor down payment. -

A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and Innovation

U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities A Financial System That T OF EN TH M E A Financial System T T R R A E P A E S That Creates Economic Opportunities D U R E Y H T Nonbank Financials, Fintech, 1789 and Innovation Nonbank Financials, Fintech, and Innovation Nonbank Financials, Fintech, TREASURY JULY 2018 2018-04417 (Rev. 1) • Department of the Treasury • Departmental Offices • www.treasury.gov U.S. DEPARTMENT OF THE TREASURY A Financial System That Creates Economic Opportunities Nonbank Financials, Fintech, and Innovation Report to President Donald J. Trump Executive Order 13772 on Core Principles for Regulating the United States Financial System Steven T. Mnuchin Secretary Craig S. Phillips Counselor to the Secretary T OF EN TH M E T T R R A E P A E S D U R E Y H T 1789 Staff Acknowledgments Secretary Mnuchin and Counselor Phillips would like to thank Treasury staff members for their contributions to this report. The staff’s work on the report was led by Jessica Renier and W. Moses Kim, and included contributions from Chloe Cabot, Dan Dorman, Alexan- dra Friedman, Eric Froman, Dan Greenland, Gerry Hughes, Alexander Jackson, Danielle Johnson-Kutch, Ben Lachmann, Natalia Li, Daniel McCarty, John McGrail, Amyn Moolji, Brian Morgenstern, Daren Small-Moyers, Mark Nelson, Peter Nickoloff, Bimal Patel, Brian Peretti, Scott Rembrandt, Ed Roback, Ranya Rotolo, Jared Sawyer, Steven Seitz, Brian Smith, Mark Uyeda, Anne Wallwork, and Christopher Weaver. ii A Financial System That Creates Economic -

Adjustable-Rate Mortgage (ARM) Is a Loan with an Interest Rate That Changes

The Federal Reserve Board Consumer Handbook on Adjustable-Rate Mortgages Board of Governors of the Federal Reserve System www.federalreserve.gov 0412 Consumer Handbook on Adjustable-Rate Mortgages | i Table of contents Mortgage shopping worksheet ...................................................... 2 What is an ARM? .................................................................................... 4 How ARMs work: the basic features .......................................... 6 Initial rate and payment ...................................................................... 6 The adjustment period ........................................................................ 6 The index ............................................................................................... 7 The margin ............................................................................................ 8 Interest-rate caps .................................................................................. 10 Payment caps ........................................................................................ 13 Types of ARMs ........................................................................................ 15 Hybrid ARMs ....................................................................................... 15 Interest-only ARMs .............................................................................. 15 Payment-option ARMs ........................................................................ 16 Consumer cautions ............................................................................. -

SOP1 -Sales Credit Agresso 563 Version 1.0 Updated – November 2012

SOP1 -Sales Credit Agresso 563 Version 1.0 Updated – November 2012 SOP2: Sales Credits The purpose of this section is to introduce the user how to raise a Sales Credit Note via the Agresso Web. This Sales Credit will then follow an Approval workflow until it then becomes an actual Sales Credit Note, or, the Sales Credit is rejected and closed. Once the Sales Credit has become an actual Sales Credit Note this will be printed off by the General Ledger Section and sent to the Customer, or if additional paperwork is required to go out with the Sales Credit please let the Sales Ledger ([email protected] ) section know. The Sales Credit Note will also record a credit against the appropriate Cost Centre and Project. SALES CREDIT WORKFLOW PROCESS Sales Credit Raised Via Agresso Web Second Third Fourth Fifth First APPROVER Up to £25K Project Approver Between £25K and £50K Project Approver Head of Subject Between £50K and £100K Project Approver Head of Subject Head of School Between £100K and £250K Project Approver Head of Subject Head of School Head of College Over £250K Director of Project Approver Head of Subject Head of School Head of College Finance Sales Credit is IF REJECTED IF APPROVED converted into Sales Credit Note Sales Credit Note printed by Sales Ledger section and sent to customer SOP2.1: Raising a Sales Credit 1. To access the Sales Ordering screen: From the Menu Select Sales Orders The following screen will appear: Page 1 SOP1 -Sales Credit Agresso 563 Version 1.0 Updated – November 2012 The red star * indicates required fields that must be used when raising a Sales Credit The following fields must be populated on this screen (highlighted fields are most relevant ): 2. -

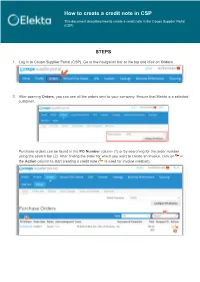

How to Create a Credit Note in CSP This Document Describes How to Create a Credit Note in the Coupa Supplier Portal (CSP)

How to create a credit note in CSP This document describes how to create a credit note in the Coupa Supplier Portal (CSP) STEPS 1. Log in to Coupa Supplier Portal (CSP). Go to the navigation bar at the top and click on Orders. 2. After opening Orders, you can see all the orders sent to your company. Ensure that Elekta is a selected customer. Purchase orders can be found in the PO Number column (1) or by searching for the order number using the search bar (2). After finding the order for which you want to create an invoice, click on in the Action column to start creating a credit note ( is used for invoice creation). 3. The credit note creation has started. In that page: a) As a minimum, complete the mandatory fields: 1) Credit Note # - a unique invoice number issued by your company to Elekta 2) Credit Note Date 3) Original Date of Supply – the date of the original invoice you are crediting 4) Currency 5) Original Invoice # - the name of the original invoice you are crediting 6) Image Scan – IMPORTANT: Do NOT attach any credit note copy as a legal PDF credit note will be generated in Coupa after you click ‘Submit’. This PDF credit note will be the legal invoice. 7) Credit Reason – the reason of the credit note creation 8) Cash Accounting Scheme & Margin Scheme - These fields are not used by Elekta 9) Exchange Rate – the field will appear if the credit note is in a currency other than PO. In this case, enter the exchange rate 10) Supplier VAT ID, Invoice/Remit-to/Ship From addresses are taken from the company information you provided to the system. -

Overdraft: Payment Service Or Small-Dollar Credit?

March 16, 2020 Overdraft: Payment Service or Small-Dollar Credit? Funding Gaps in Consumer Finances Figure 1. Annual Interest and Noninterest Income One of the earliest documented cases of bank overdraft U.S. Commercial Banks, 1970-2018 ($ millions) dates back to 1728, when a Royal Bank of Scotland customer requested a cash credit to allow him to withdraw more money from his account than it held. Three centuries later, technologies, such as electronic payments (e.g., debit cards) and automated teller machines (ATMs), changed the way consumers use funds for retail purchases, transacting more frequently and in smaller denominations. Accordingly, today’s financial institutions commonly offer point-of-sale overdraft services or overdraft protection in exchange for a flat fee around $35. Although these fees can be large relative to the transaction, alternative sources of short-term small-dollar funding, such as payday loans, deposit advances, and installment loans, can be costly as well. Congress has taken an interest in the availability and cost of providing consumers funds to meet Source: Federal Deposit Insurance Corporation (FDIC). their budget shortfalls. Legislation introduced in the 116th Congress (H.R. 1509/S. 656 and H.R. 4254/S. 1595) as well Banks generate noninterest income in a number of ways. as the Federal Reserve’s real-time payments initiative could For example, a significant source of noninterest income impact consumer use of overdraft programs in various comes from collecting fees for deposit accounts services, ways. (See “Policy Tools and Potential Outcomes” below such as maintaining a checking account, ATM withdrawals, for more information.) The policy debate around this or covering an overdraft. -

LOAN RATES America First Credit Union Offers Members Competitive Loan Rates, Listed Below

LOAN RATES America First Credit Union offers members competitive loan rates, listed below. The annual percentage rates (APR) quoted are based on approved credit. Rates may be higher, depending on your credit history and other underwriting factors. Our loan offices will discuss your application and available rates with you. Variable APRs may increase or decrease monthly. Go to americafirst.com or call 1-800-999-3961 for more information. EFFECTIVE: OCTOBER 1, 2021 VARIABLE APR FIXED APR FEE DISCLOSURES VEHICLE 2.99% - 18.00% 2.99% - 18.00% ANNUAL PERCENTAGE RATE (APR) FOR PURCHASES 60-MONTH DECLINING RATE AUTO N/A 3.24% - 18.00% When you open your account, the applicable APR is based on creditworthiness. SMALL RV LOAN 4.49% - 15.24% 5.49% - 16.24% After that, your APR will vary with the market based on the Prime Rate. RV LOAN 4.49% - 15.74% 5.49% - 16.74% APR FOR CASH ADVANCES & BALANCE TRANSFERS When you open your account, the applicable APR is based on creditworthiness. RV BALLOON N/A 5.49% - 6.74% After that, your APR will vary with the market based on the Prime Rate. PERSONAL 8.49% - 18.00% 9.49% - 18.00% HOW TO AVOID PAYING INTEREST ON PURCHASES LINE OF CREDIT 15.24% - 18.00% Your due date is the 28th day of each month. We will not charge any interest on the portion of the purchases balance that you pay by the due date each month. SHARE-SECURED LINE OF CREDIT 3.05% FOR CREDIT CARD TIPS FROM THE CONSUMER FINANCIAL PROTECTION CONSUMER SHARE LOAN + 3.00% BUREAU CREDIT BUILDER PLUS 10.00% To learn more about factors to consider when applying for or using a credit card, visit the Consumer Financial Protection Bureau at CERTIFICATE ACCOUNT * 3.00% consumerfinance.gov/learnmore. -

7.7 Repayment (Credit Note)

COBISS COBISS3/Loan 7.7 REPAYMENT (CREDIT NOTE) Until now, when the money had to be returned from the cash register to a member and the invoice could not be cancelled, the money was returned by entering debts in a negative amount and settling debts by entering the negative amount. Since the installation of COBISS3/Loan V6.4-02, this option is disabled. From now on, you can issue credit notes for this purpose. This option is now available in all libraries, regardless of whether the library uses the certified cash register or not. If you wish to return the money to a member, you can do this in the following way: Procedure 1. Find the invoice, where the debts settlement, for which you wish to return the money to the member, is entered. You can do this in the following two ways: find a member and then in his/her debts and settlement records (the Entering and settling debts method) find the invoice (the View settled debts button) and load it to the workspace by highlighting it and clicking the Load invoice button. Highlight the Invoice class, select Search and then in the search window enter the value you are searching for under the relevant search field (e.g. invoice number) 2. Highlight the invoice on the workspace and select the Create credit note method. The Credit note window will open, where data on the invoice and a list of all items on the invoice will be displayed. 3. Highlight the item for which you wish to return the money and click the Add item button. -

Stopping the Payday Loan Trap Alternatives That Work, Ones That Don’T

Stopping the payday Loan trap AlternAtives thAt Work, ones thAt Don’t NCLC® NATIONAL CONSUMER June 2010 L AW C E N T E R® © Copyright 2010, National Consumer Law Center, Inc. All rights reserved. About the Authors Lauren K. Saunders is the Managing Attorney of NCLC’s Washington, DC office, where she handles legislative, administrative and other advocacy efforts on behalf of low income consumers. She contributes to several NCLC publications, including Fair Credit Reporting, Fair Debt Collection and Consumer Banking and Payments Law. She graduated magna cum laude from Harvard Law School where she was an Executive Editor of the Harvard Law Review, and holds a Masters in Public Policy from Harvard’s Kennedy School of Government and a B.A., Phi Beta Kappa, from Stanford University. Leah A. Plunkett is a staff attorney at NCLC, where she focuses on predatory small dollar loans, auto policy, protection of exempt funds, and the consumer needs of domestic violence survivors. Before coming to NCLC, Leah clerked in the United States District Court for the District of Maryland and established the Youth Law Project at New Hampshire Legal Assistance. Leah is a cum laude graduate of Harvard Law School, where she was on the board of both the Harvard Legal Aid Bureau and HLS for Choice. Carolyn Carter is NCLC’s Deputy Director for Advocacy. She is a contributing author to Cost of Credit, Truth in Lending, Unfair and Deceptive Acts and Practices and several other NCLC treatises. Prior to joining NCLC, she worked for legal services programs in Ohio and Pennsylvania. -

Payday Lending in America

An overview from Oct 2013 Report 3 in the Payday Lending in America series Payday Lending in America: Policy Solutions Overview About 20 years ago, a new retail financial product, the payday loan, began to spread across the United States. It allowed a customer who wanted a small amount of cash quickly to borrow money and pledge a check dated for the next payday as collateral. Twelve million people now use payday loans annually, spending an average of $520 in interest to repeatedly borrow an average of $375 in credit. In the 35 states that allow this type of lump-sum repayment loan, customers end up having to borrow again and again—paying a fee each time. That is because repaying the loan in full requires about one-third of an average borrower’s paycheck, not leaving enough money to cover everyday living expenses without borrowing again. In Colorado, lump-sum payday lending came into use in 1992. The state was an early adopter of such loans, but the situation is now different. In 2010, state lawmakers agreed that the payday loan market in Colorado had failed and acted to correct it. Legislators forged a compromise designed to make the loans more affordable while granting the state’s existing nonbank lenders a new way to provide small-dollar loans to those with damaged credit histories. The new law changed the terms for payday lending from a single, lump-sum payment to a series of installment payments stretched out over six months and lowered the maximum allowable interest rates. As a result, borrowers in Colorado now pay an average of 4 percent of their paychecks to service the loans, compared with 36 percent under a conventional lump-sum payday loan model. -

MLA Faqs 08.22

Frequently Asked Questions about the Defense Department’s Military Lending Act Regulations The following is intended to help pawnbrokers prepare for the October 3, 2016 mandatory compliance date for the expanded Military Lending Act (MLA) regulations. This information is not intended as, and should not be used as, a substitute for guidance from your local lawyer. What is the Military Lending Act? The MLA was enacted by Congress in 2006, and the DOD adopted a regulation to implement it in 2007, but did not cover pawn transactions. The DOD expanded the scope of the regulation to cover additional consumer credit products on July 22, 2015 (“2015 regulation”), and specifically mentioned pawn transactions. When does compliance with the DOD’s 2015 regulation become mandatory for pawn transactions? October 3, 2016, unless extended by the DOD or otherwise by Congress or a court of law. What types of transactions does DOD’s expanded regulation govern? The 2015 regulation applies to pawns if the borrowers or pledgers are active duty service members, their spouse or other dependent who receives 51% or more of their support from the service member. These consumers are “covered borrowers”. No traditional non-recourse pawn transaction entered into before October 3, 2016 is affected by the 2015 regulation. The 2015 regulation does not affect pawns entered into before your customer became an active duty service member or dependent of one. What are the key requirements of DOD’s regulation? The 2015 regulation: • caps the maximum Annual Percentage Rate