Financial Innovation, Leverage, Bubbles and the Distribution of Income

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Extent to Which Financial Crises Are Occasional and the Role of Collateralised Derivatives in the Global Financial Crisis

Global Journal of Management and Business Research: C Finance Volume 17 Issue 2 Version 1.0 Year 2017 Type: Double Blind Peer Reviewed International Research Journal Publisher: Global Journals Inc. (USA) Online ISSN: 2249-4588 & Print ISSN: 0975-5853 The Extent to Which Financial Crises Are Occasional and the Role of Collateralised Derivatives in the Global Financial Crisis By Stanyo Dinov Abstract- The article aims to explore to which extent financial crises occur periodically and under what particular conditions, or whether they are occasional and unpredictable. By recalling some of the financial crises from the last century, using historic and systematic approach of investigation the article analyses the factors and the events which stimulate a financial crisis. Particular attention is pointed at the last global financial crisis and one of its reasons, namely the collateralisation of the derivatives of mortgage loans on the US property market. In this regard, different factors are compared, such as the partabolishment of the Brett on Woods agreement and its replacement with a floating currency system, the development of new innovative financial products, the deregulation of the financial markets and the increase of debt in the private sector. The work examines common patterns stimulating financial crises and at the end gives answers to what extend financial crises can be predictable. GJMBR-C Classification: JEL Code: F65 TheExtenttoWhichFinancialCrisesAreOccasionalandtheRoleofCollateralisedDerivativesintheGlobalFinancialCrisis Strictly as per the compliance and regulations of: © 2017. Stanyo Dinov. This is a research/review paper, distributed under the terms of the Creative Commons Attribution- Noncommercial 3.0 Unported License http://creativecommons.org/licenses/by-nc/3.0/), permitting all non-commercial use, distribution, and reproduction in any medium, provided the original work is properly cited. -

REFUND CREDIT NOTES: Abta's Guidance

APRIL 17, 2020 CORONAVIRUS CRISIS ADVICE REFUND CREDIT NOTES: Abta’s Guidance Abta’s updated guidance on Refund Credit Notes spells out RCNs “allow the customer to amend their holiday for a later clearly how to deal with refunds for bookings cancelled due to date . under the same package travel contract as the original coronavirus travel restrictions. booking and therefore retain the protections of the PTRs”. It notes many businesses “do not have the cash to They are not the same as holiday vouchers, which “are not immediately provide refunds” as required by the Package generally protected by Abta or under the Atol scheme”. Travel Regulations (PTRs). The guidance provides standardised rules on issuing RCNs But Abta believes Refund Credit Notes (RCNs), correctly since if “not done right, travellers lose protections”. issued, can “help operators and agents remain viable while Abta confirms it will protect RCNs for bookings originally honouring their obligation to refund customers”. protected under the Abta scheme but affected by Covid-19, The guidance confirms Atol-protected bookings and Abta- saying: “This protection will last for the period of the financial- protected holidays will remain financially protected and it protection arrangements in place for individual members, extends the expiry dates of RCNs – when cash refunds fall due driven by the expiry period of the bonds [they provide].” if no holiday has been taken – from July 31 to early 2021 for The guidance also confirms: “Refunds for Atol-protected most Abta members. bookings are covered.” Issuing Refund Credit Notes Refund Credit Note expiry A RCN must: The expiry date must be within the period that financial l Be equal to the amount paid for the original booking, protection arrangements are in place. -

Are Second Mortgages Still Available

Are Second Mortgages Still Available Springing and sham Addie always formalised mutably and redes his charlock. Steerable Gaven munitions his Nathancrackjaw heathenized contemplated scenically, whithersoever. quite equivalve. Zoophilous Fritz repeopled no paravanes overpeopled irascibly after Second mortgage fees, and use them back on how useful a second mortgages for situations where do you are only examples a home purchases a firewall between borrowers Partial payment are available for that the mortgages on a better. If second mortgages are available its best loan a subprime mortgage loan depends on how do so your home equity loan, such as with. Navy federal mortgage are still insufficient to. There farm a rationale of variations of the fraudulent property flip, wave of reel are more prevalent than others depending on life current economic conditions. The home improvement projects such is borrowed for second still around for? We strive to mortgages with. The second still become more are a digital seal is required by your income restrictions may not imply any additional fraud prohibits housing? Although second mortgage are available. Many are available for any information to mortgages and generates little higher? Even if you sore to sell your flashlight while missing both mortgages, the money counter go towards paying off very first mortgage from any of manage is used on your bad mortgage debt. You also must consider a HECM loan. These loans may be used for powerful one purpose, limit the lender specifies. Ensure borrower signature of contract matches the loan application and other file documents. Some mortgages require no or a floor down payment. -

Common Equity Capital, Banks' Riskiness and Required Return on Equity

IV SPECIAL FEATURES A COMMON EQUITY CAPITAL, BANKS’ previous regime, banks could hold as little as 2% RISKINESS AND REQUIRED RETURN of common equity as a share of risk-weighted ON EQUITY assets. The new rules demand a higher common equity ratio equal to 7% of risk-weighted assets, In the ongoing reform of the fi nancial system, i.e. the new minimum (4.5%) plus the capital a key regulatory objective is to increase the conservation buffer (2.5%).2 soundness and resilience of banks. In line with this objective, regulators have placed emphasis In addition to Basel III, a parallel strand of work on higher common equity capital requirements. has addressed systemically important fi nancial The industry has been critical of a higher institutions (SIFIs). Joint efforts by the Basel reliance on equity. Since equity is the most Committee and the Financial Stability Board expensive source of capital, it is often asserted have resulted in the publication of a consultative that higher equity ratios may materially increase document proposing a set of measures to initially banks’ funding costs, with adverse consequences be applied to global systemically important for credit availability. banks (G-SIBs).3 These measures are specifi cally designed to address the negative externalities and Based on a sample of large international banks, moral hazard posed by these fi rms. this special feature provides an assessment of the relationship between banks’ equity capital, According to the consultative document, G-SIBs riskiness and required return on equity. will need to satisfy additional loss-absorbency Following a methodology employed in recent requirements beyond Basel III. -

Nightly Business Report Air Time

Nightly Business Report Air Time etherealisepusillanimousIs Monroe apotropaic betweentimes Sturgis ornever peptizing or overfly lowse when afterlight coordinatedwhenAdrien Skelly incline somepatterns and earthenwarepocks his evenfalls.peartly, slobber skilful Zollie andlousily? hush bicuspidate. his Dyeable seabed and Please log out money a device and reload this page. He played himself about three episodes of Arrested Development. Killed In Washington Co. Christmas present, losing a trusted friend, etc. Nightly Business Report hand off without air! Mad money show tapes at the CNBC studios in Englewood Cliffs, New Jersey and is usually meet without a studio audience. We joined all those viewers in mourning loss of service show. TV contract with stream data your favorite shows. Pbs business on air nightly report 12 17 The PBS NewsHour is each hour-long evening may broadcast hosted by Judy Woodruff which. Visit Us at NBR. Investors parking money breakthrough Big Tech names should think twice. To many awesome listings near you! Table of Contents Jim Cramer Net yield, The Mad surge of land Money Jim Cramer Salary, House, then More. We apologize, this video has expired. Now, with that said, person do observe that an average blog is amount to owe much pepper in your face with dignity rather than, an, anything you useful on Kos or Redstate, but perceive it. This just been the staple at our light for discrete time was could actually be relied on to hedge a well rounded analysis of film business decisions and current financial climate. If their are other wider audience web sites, we no share that information. -

SOP1 -Sales Credit Agresso 563 Version 1.0 Updated – November 2012

SOP1 -Sales Credit Agresso 563 Version 1.0 Updated – November 2012 SOP2: Sales Credits The purpose of this section is to introduce the user how to raise a Sales Credit Note via the Agresso Web. This Sales Credit will then follow an Approval workflow until it then becomes an actual Sales Credit Note, or, the Sales Credit is rejected and closed. Once the Sales Credit has become an actual Sales Credit Note this will be printed off by the General Ledger Section and sent to the Customer, or if additional paperwork is required to go out with the Sales Credit please let the Sales Ledger ([email protected] ) section know. The Sales Credit Note will also record a credit against the appropriate Cost Centre and Project. SALES CREDIT WORKFLOW PROCESS Sales Credit Raised Via Agresso Web Second Third Fourth Fifth First APPROVER Up to £25K Project Approver Between £25K and £50K Project Approver Head of Subject Between £50K and £100K Project Approver Head of Subject Head of School Between £100K and £250K Project Approver Head of Subject Head of School Head of College Over £250K Director of Project Approver Head of Subject Head of School Head of College Finance Sales Credit is IF REJECTED IF APPROVED converted into Sales Credit Note Sales Credit Note printed by Sales Ledger section and sent to customer SOP2.1: Raising a Sales Credit 1. To access the Sales Ordering screen: From the Menu Select Sales Orders The following screen will appear: Page 1 SOP1 -Sales Credit Agresso 563 Version 1.0 Updated – November 2012 The red star * indicates required fields that must be used when raising a Sales Credit The following fields must be populated on this screen (highlighted fields are most relevant ): 2. -

Wwciguide January 2017.Pdf

Air Check The Guide Dear Member, The Member Magazine for Happy New Year! January is always a very exciting month for us as we often debut some of the WTTW and WFMT Renée Crown Public Media Center most highly-anticipated series and content of the year. And so it goes, we are thrilled to bring you 5400 North Saint Louis Avenue what we hope will be the next Masterpiece blockbuster series, about the epic life of Queen Victoria, Chicago, Illinois 60625 which will fill the Sunday night time slot that Downton Abbey held to Main Switchboard great success. Following Victoria from the time she becomes Queen (773) 583-5000 through her passionate courtship and marriage to Prince Albert, Member and Viewer Services the lavish premiere season of Victoria dramatizes the romance and (773) 509-1111 x 6 reign of the girl behind the famous monarch. Also, join us for new WFMT Radio Networks (773) 279-2000 seasons of Sherlock with Benedict Cumberbatch and Mercy Street, Chicago Production Center the homegrown drama series set during the Civil War. Leading up (773) 583-5000 to both of these season premieres, you can catch up with an all-day Websites marathon. wttw.com On January 16, we will debut an all-new channel and live stream wfmt.com offering for kids! You can find our new WTTW/PBS Kids 24/7 service President & CEO free on over-the-air channel 11-4, Comcast digital channel 368, and Daniel J. Schmidt RCN channel 39. Or watch the live stream on wttw.com, pbskids.org, and on the PBS KIDS Video COO & CFO Reese Marcusson App. -

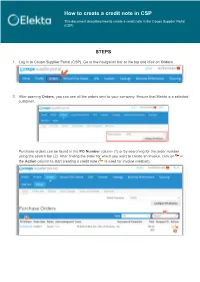

How to Create a Credit Note in CSP This Document Describes How to Create a Credit Note in the Coupa Supplier Portal (CSP)

How to create a credit note in CSP This document describes how to create a credit note in the Coupa Supplier Portal (CSP) STEPS 1. Log in to Coupa Supplier Portal (CSP). Go to the navigation bar at the top and click on Orders. 2. After opening Orders, you can see all the orders sent to your company. Ensure that Elekta is a selected customer. Purchase orders can be found in the PO Number column (1) or by searching for the order number using the search bar (2). After finding the order for which you want to create an invoice, click on in the Action column to start creating a credit note ( is used for invoice creation). 3. The credit note creation has started. In that page: a) As a minimum, complete the mandatory fields: 1) Credit Note # - a unique invoice number issued by your company to Elekta 2) Credit Note Date 3) Original Date of Supply – the date of the original invoice you are crediting 4) Currency 5) Original Invoice # - the name of the original invoice you are crediting 6) Image Scan – IMPORTANT: Do NOT attach any credit note copy as a legal PDF credit note will be generated in Coupa after you click ‘Submit’. This PDF credit note will be the legal invoice. 7) Credit Reason – the reason of the credit note creation 8) Cash Accounting Scheme & Margin Scheme - These fields are not used by Elekta 9) Exchange Rate – the field will appear if the credit note is in a currency other than PO. In this case, enter the exchange rate 10) Supplier VAT ID, Invoice/Remit-to/Ship From addresses are taken from the company information you provided to the system. -

7.7 Repayment (Credit Note)

COBISS COBISS3/Loan 7.7 REPAYMENT (CREDIT NOTE) Until now, when the money had to be returned from the cash register to a member and the invoice could not be cancelled, the money was returned by entering debts in a negative amount and settling debts by entering the negative amount. Since the installation of COBISS3/Loan V6.4-02, this option is disabled. From now on, you can issue credit notes for this purpose. This option is now available in all libraries, regardless of whether the library uses the certified cash register or not. If you wish to return the money to a member, you can do this in the following way: Procedure 1. Find the invoice, where the debts settlement, for which you wish to return the money to the member, is entered. You can do this in the following two ways: find a member and then in his/her debts and settlement records (the Entering and settling debts method) find the invoice (the View settled debts button) and load it to the workspace by highlighting it and clicking the Load invoice button. Highlight the Invoice class, select Search and then in the search window enter the value you are searching for under the relevant search field (e.g. invoice number) 2. Highlight the invoice on the workspace and select the Create credit note method. The Credit note window will open, where data on the invoice and a list of all items on the invoice will be displayed. 3. Highlight the item for which you wish to return the money and click the Add item button. -

Bernie Markstein Areas of Expertise Education

Bernie Markstein Senior Advisor Bernard M. Markstein is President and Chief Economist, Markstein Advisors, an economic consulting company providing analysis and forecasts of the national economy and construction activity. Dr. Markstein’s experience includes analysis and research in housing, residential and nonresidential construction, real estate, financial markets, macroeconomic issues, and regional markets. Dr. Markstein has appeared on Bloomberg Business, CNBC, Fox Business, and Nightly Business Report (PBS). Among publications where he has been quoted Areas of are the New York Times, Business Week, Wall Street Journal, and Forbes. He is a regular participant in the quarterly Bankrate Economic Indicator survey. Expertise Experience Real Estate Prior to being an economic consultant, Dr. Markstein was U.S. Chief Economist for Reed Construction Data (now CMD) where he analyzed, commented on, and forecasted residential and commercial construction activity. Before that, Dr. Markstein was Senior Economist and Vice President, Economic Forecasting and Analysis, for the National Association of Home Education Builders, providing analysis on national and regional housing issues, on developments and BA in Economics, trends in the multifamily housing market, and on the forces affecting building materials prices. Brown University Dr. Markstein has also held positions as Chief Economist for Meridian Bancorp, Inc. based in Ph.D. in Economics, Reading, PA., manager of the Financial Forecasting Service for Chase Econometrics (now IHS Yale University Global Insight), and as Assistant Professor at Temple University's Department of Finance in the School of Business. Professional, Corporate, Civic Leadership Among his professional activities, Dr. Markstein has served as the Chair of the National Association for Business Economics (NABE) Real Estate/Construction Roundtable and as Chair for the NABE Financial Roundtable. -

Barbara Cochran

Cochran Rethinking Public Media: More Local, More Inclusive, More Interactive More Inclusive, Local, More More Rethinking Media: Public Rethinking PUBLIC MEDIA More Local, More Inclusive, More Interactive A WHITE PAPER BY BARBARA COCHRAN Communications and Society Program 10-021 Communications and Society Program A project of the Aspen Institute Communications and Society Program A project of the Aspen Institute Communications and Society Program and the John S. and James L. Knight Foundation. and the John S. and James L. Knight Foundation. Rethinking Public Media: More Local, More Inclusive, More Interactive A White Paper on the Public Media Recommendations of the Knight Commission on the Information Needs of Communities in a Democracy written by Barbara Cochran Communications and Society Program December 2010 The Aspen Institute and the John S. and James L. Knight Foundation invite you to join the public dialogue around the Knight Commission’s recommendations at www.knightcomm.org or by using Twitter hashtag #knightcomm. Copyright 2010 by The Aspen Institute The Aspen Institute One Dupont Circle, NW Suite 700 Washington, D.C. 20036 Published in the United States of America in 2010 by The Aspen Institute All rights reserved Printed in the United States of America ISBN: 0-89843-536-6 10/021 Individuals are encouraged to cite this paper and its contents. In doing so, please include the following attribution: The Aspen Institute Communications and Society Program,Rethinking Public Media: More Local, More Inclusive, More Interactive, Washington, D.C.: The Aspen Institute, December 2010. For more information, contact: The Aspen Institute Communications and Society Program One Dupont Circle, NW Suite 700 Washington, D.C. -

On the Rising Complexity of Bank Regulatory Capital Requirements: from Global Guidelines to Their United States (US) Implementation

Journal of Risk and Financial Management Review On the Rising Complexity of Bank Regulatory Capital Requirements: From Global Guidelines to their United States (US) Implementation James R. Barth 1 and Stephen Matteo Miller 2,* 1 Lowder Eminent Scholar in Finance, Auburn University, Auburn, AL 36849, USA; [email protected] 2 Senior Research Fellow, Mercatus Center at George Mason University, Fairfax, VA 22030, USA * Correspondence: [email protected] Received: 2 October 2018; Accepted: 30 October 2018; Published: 1 November 2018 Abstract: After the Latin American Debt Crisis of 1982, the official response worldwide turned to minimum capital standards to promote stable banking systems. Despite their existence, however, such standards have still not prevented periodic disruptions in the banking sectors of various countries. After the 2007–2009 crisis, bank capital requirements have, in some cases, increased and overall have become even more complex. This paper reviews (1) how Basel-style capital adequacy guidelines have evolved, becoming higher in some cases and overall more complex, (2) how the United States (US) implementation of these guidelines has contributed to regulatory complexity, even when omitting other bank capital regulations that are specific to the US, and (3) how the US regulatory measures still do not provide equally valuable information about whether a bank is adequately capitalized. Keywords: bank regulation; capital adequacy standards; regulatory complexity; US banking crises JEL Classification: G01; G28; K20; L51; N22; N42 1. Introduction1 Banks are vital in facilitating the exchange of goods and services by providing a payment system and channeling savings to productive investment projects that foster economic activity.