Sample Debt Validation Letter (Send Via Certified Mail, Return Receipt Requested)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

UNITED STATES DISTRICT COURT NORTHERN DISTRICT of GEORGIA ATLANTA DIVISION in Re

Case 1:17-md-02800-TWT Document 739 Filed 07/22/19 Page 1 of 7 UNITED STATES DISTRICT COURT NORTHERN DISTRICT OF GEORGIA ATLANTA DIVISION MDL Docket No. 2800 In re: Equifax Inc. Customer No. 1:17-md-2800-TWT Data Security Breach Litigation CONSUMER ACTIONS Chief Judge Thomas W. Thrash, Jr. PLAINTIFFS’ MOTION TO DIRECT NOTICE OF PROPOSED SETTLEMENT TO THE CLASS Plaintiffs move for entry of an order directing notice of the proposed class action settlement the parties to this action have reached and scheduling a hearing to approve final approval of the settlement. Plaintiffs are simultaneously filing a supporting memorandum of law and its accompanying exhibits, which include the Settlement Agreement. For the reasons set forth in that memorandum, Plaintiffs respectfully request grant the Court enter the proposed order that is attached as an exhibit to this motion. The proposed order has been approved by both Plaintiffs and Defendants. For ease of reference, the capitalized terms in this motion and the accompanying memorandum have the meaning set forth in the Settlement Agreement. Case 1:17-md-02800-TWT Document 739 Filed 07/22/19 Page 2 of 7 Respectfully submitted this 22nd day of July, 2019. /s/ Kenneth S. Canfield Kenneth S. Canfield Ga Bar No. 107744 DOFFERMYRE SHIELDS CANFIELD & KNOWLES, LLC 1355 Peachtree Street, N.E. Suite 1725 Atlanta, Georgia 30309 Tel. 404.881.8900 [email protected] /s/ Amy E. Keller Amy E. Keller DICELLO LEVITT GUTZLER LLC Ten North Dearborn Street Eleventh Floor Chicago, Illinois 60602 Tel. 312.214.7900 [email protected] /s/ Norman E. -

GEORGIA – COSTA RICA Economic Development Connection

GEORGIA – COSTA RICA Economic Development Connection Government & Commerce The University System of Georgia offers at least 35 study abroad programs to Costa Rica Atlanta is home to the Consulate General of the including programs in art, culture, education, Republic of Costa Rica. Ms. Joanne Leigh Noriega medicine, ecology, biology and creative writing. serves as Consul General. The Consulate serves According to the 2012 U.S. Census Bureau, there the states of Alabama, Georgia, Kentucky, North are more than 3,100 residents in Georgia with Carolina, South Carolina and Tennessee. Costa Rican heritage. The Georgia Institute of Technology created the Costa Rica Trade, Innovation and Productivity Trade Relationship (TIP) Center through a partnership among Georgia Tech, the Foreign Trade Corporation of EXPORTS: In 2013, Georgia exports to Costa Rica Costa Rica and the Chamber of Industries in Costa totaled $150 million a .93% increase from 2012. th Rica. The center focuses on utilizing research, Costa Rica is currently the 50 largest export innovation and education to increase trade across market for Georgia. borders and make existing trade more productive Top exports from Georgia to Costa Rica include to benefit the Costa Rican economy and scientific kraft paper, automatic data processing machines, community. The focus is currently on digital refrigerators and freezers, electric water heaters, services and food products. civilian aircraft, engines and parts and wood The University of Georgia has a 160 acre satellite pulp. campus in San Luis de Monteverde, Costa Rica, Georgia leads the nation in the export of the where it offers classes in a variety of fields ranging following goods to Costa Rica: paper and from ecology to business. -

Corporate Bonds and Debentures

Corporate Bonds and Debentures FCS Vinita Nair Vinod Kothari Company Kolkata: New Delhi: Mumbai: 1006-1009, Krishna A-467, First Floor, 403-406, Shreyas Chambers 224 AJC Bose Road Defence Colony, 175, D N Road, Fort Kolkata – 700 017 New Delhi-110024 Mumbai Phone: 033 2281 3742/7715 Phone: 011 41315340 Phone: 022 2261 4021/ 6237 0959 Email: [email protected] Email: [email protected] Email: [email protected] Website: www.vinodkothari.com 1 Copyright & Disclaimer . This presentation is only for academic purposes; this is not intended to be a professional advice or opinion. Anyone relying on this does so at one’s own discretion. Please do consult your professional consultant for any matter covered by this presentation. The contents of the presentation are intended solely for the use of the client to whom the same is marked by us. No circulation, publication, or unauthorised use of the presentation in any form is allowed, except with our prior written permission. No part of this presentation is intended to be solicitation of professional assignment. 2 About Us Vinod Kothari and Company, company secretaries, is a firm with over 30 years of vintage Based out of Kolkata, New Delhi & Mumbai We are a team of qualified company secretaries, chartered accountants, lawyers and managers. Our Organization’s Credo: Focus on capabilities; opportunities follow 3 Law & Practice relating to Corporate Bonds & Debentures 4 The book can be ordered by clicking here Outline . Introduction to Debentures . State of Indian Bond Market . Comparison of debentures with other forms of borrowings/securities . Types of Debentures . Modes of Issuance & Regulatory Framework . -

Interest-Rate-Growth Differentials and Government Debt Dynamics

From: OECD Journal: Economic Studies Access the journal at: http://dx.doi.org/10.1787/19952856 Interest-rate-growth differentials and government debt dynamics David Turner, Francesca Spinelli Please cite this article as: Turner, David and Francesca Spinelli (2012), “Interest-rate-growth differentials and government debt dynamics”, OECD Journal: Economic Studies, Vol. 2012/1. http://dx.doi.org/10.1787/eco_studies-2012-5k912k0zkhf8 This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. OECD Journal: Economic Studies Volume 2012 © OECD 2013 Interest-rate-growth differentials and government debt dynamics by David Turner and Francesca Spinelli* The differential between the interest rate paid to service government debt and the growth rate of the economy is a key concept in assessing fiscal sustainability. Among OECD economies, this differential was unusually low for much of the last decade compared with the 1980s and the first half of the 1990s. This article investigates the reasons behind this profile using panel estimation on selected OECD economies as means of providing some guidance as to its future development. The results suggest that the fall is partly explained by lower inflation volatility associated with the adoption of monetary policy regimes credibly targeting low inflation, which might be expected to continue. However, the low differential is also partly explained by factors which are likely to be reversed in the future, including very low policy rates, the “global savings glut” and the effect which the European Monetary Union had in reducing long-term interest differentials in the pre-crisis period. -

Onboard Analysis Workbook 2019.Xlsx

sort ranking Revenues legal name 1 The Home Depot, Inc. F500 & Top 50 108203 2 United Parcel Service, Inc. F500 & Top 50 71861 3 Delta Air Lines, Inc. F500 & Top 50 44438 4 The Coca-Cola Company F500 & Top 50 31856 5 The Southern Company F500 & Top 50 23495 6 Aflac Incorporated F500 & Top 50 21758 7 Genuine Parts Company F500 & Top 50 18735 8 WestRock Company F500 & Top 50 16285.1 9 SunTrust Banks, Inc. F500 & Top 50 10431 10 Pultegroup, Inc. F500 & Top 50 10188.331 11 Mohawk Industries, Inc. F500 & Top 50 9983.6 12 AGCO Corporation 1 F500 & Top 50 9352 3 Veritiv Corporation F500 & Top 50 8696.2 14 Asbury Automotive Group, Inc. F500 & Top 50 6874.4 15 NCR Corporation F500 & Top 50 6405 16 Intercontinental Exchange, Inc. F500 & Top 50 6276 17 HD Supply Holdings, Inc. F500 & Top 50 6047 18 Graphic Packaging Holding Com F500 & Top 50 6023 19 Invesco Ltd. Top 50 5314.1 20 Total System Services, Inc. Top 50 4028 21 Flowers Foods, Inc. Top 50 3951.852 22 Aaron's, Inc. Top 50 3828.9 23 Acuity Brands, Inc. Top 50 3680.1 24 Carter's, Inc. Top 50 3462.3 25 Equifax Inc. Top 50 3412.1 26 Global Payments Inc. Top 50 3366.366 27 GMS Inc. Top 50 3116 28 BlueLinx Holdings Inc. Top 50 2862.85 29 FleetCor Technologies, Inc. Top 50 2433.492 30 SiteOne Landscape Supply, Inc. Top 50 2112.3 31 Beazer Homes USA, Inc. Top 50 2107 32 Primerica, Inc. -

Nber Working Papers Series

NBER WORKING PAPERS SERIES WAS THERE A BUBBLE IN THE 1929 STOCK MARKET? Peter Rappoport Eugene N. White Working Paper No. 3612 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 February 1991 We have benefitted from comments made on earlier drafts of this paper by seminar participants at the NEER Summer Institute and Rutgers University. We are particularly indebted to Charles Calomiris, Barry Eicherigreen, Gikas Hardouvelis and Frederic Mishkiri for their suggestions. This paper is part of NBER's research program in Financial Markets and Monetary Economics. Any opinions expressed are those of the authors and not those of the National Bureau of Economic Research. NBER Working Paper #3612 February 1991 WAS THERE A BUBBLE IN THE 1929 STOCK MARKET? ABSTRACT Standard tests find that no bubbles are present in the stock price data for the last one hundred years. In contrast., historical accounts, focusing on briefer periods, point to the stock market of 1928-1929 as a classic example of a bubble. While previous studies have restricted their attention to the joint behavior of stock prices and dividends over the course of a century, this paper uses the behavior of the premia demanded on loans collateralized by the purchase of stocks to evaluate the claim that the boom and crash of 1929 represented a bubble. We develop a model that permits us to extract an estimate of the path of the bubble and its probability of bursting in any period and demonstrate that the premium behaves as would be expected in the presence of a bubble in stock prices. -

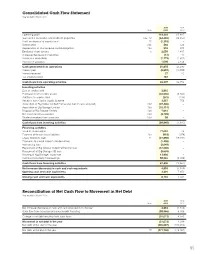

Reconciliation of Net Cash Flow to Movement in Net Debt Year Ended 31 March 2015

Consolidated Cash Flow Statement Year ended 31 March 2015 2015 2014 Note £000 £000 Operating profit 114,203 67,887 Gain on the revaluation of investment properties 13a, 14 (64,465) (28,350) Profit on disposal of surplus land 15 (1,318) – Depreciation 13b 566 526 Depreciation of finance lease capital obligations 13a 918 974 Employee share options 6 2,059 1,437 (Increase)/decrease in inventories (14) 10 Increase in receivables (1,172) (1,652) Increase in payables 1,098 2,458 Cash generated from operations 51,875 43,290 Interest paid (9,692) (10,558) Interest received 27 20 Tax credit received 187 – Cash flows from operating activities 42,397 32,752 Investing activities Sale of surplus land 2,815 – Purchase of non-current assets (42,555) (8,460) Additions to surplus land (231) (136) Receipts from Capital Goods Scheme 3,557 756 Acquisition of Big Yellow Limited Partnership (net of cash acquired) 13d (37,406) – Acquisition of Big Storage Limited 13a (15,114) – Disposal of Big Storage Limited 13a 7,614 – Net investment in associates 13d (3,709) – Dividend received from associate 13d 89 – Cash flows from investing activities (84,940) (7,840) Financing activities Issue of share capital 77,094 42 Payment of finance lease liabilities 13a (918) (974) Equity dividends paid 11 (27,890) (19,591) Payments to cancel interest rate derivatives (1,408) – Refinancing fees (2,649) – Repayment of Big Yellow Limited Partnership loan (57,000) – Repayment of Big Storage AIB loan (9,659) – Drawing of Big Storage Lloyds loan 13,900 – Increase/(reduction) in borrowings -

Equifax: Anatomy of a Security Breach Ashton Glenn Georgia Southern University

Georgia Southern University Digital Commons@Georgia Southern University Honors Program Theses 2018 Equifax: Anatomy of a Security Breach Ashton Glenn Georgia Southern University Follow this and additional works at: https://digitalcommons.georgiasouthern.edu/honors-theses Part of the Accounting Commons Recommended Citation Glenn, Ashton, "Equifax: Anatomy of a Security Breach" (2018). University Honors Program Theses. 378. https://digitalcommons.georgiasouthern.edu/honors-theses/378 This thesis (open access) is brought to you for free and open access by Digital Commons@Georgia Southern. It has been accepted for inclusion in University Honors Program Theses by an authorized administrator of Digital Commons@Georgia Southern. For more information, please contact [email protected]. Equifax: Anatomy of a Security Breach An Honors Thesis submitted in partial fulfillment of the requirements for Honors in the College of Business Administration, School of Accountancy. By Ashton Glenn Under the mentorship of Dr. Thomas Buckhoff ABSTRACT The infamous 2017 Equifax breach not only compromised millions of citizens’ data, but the breach also left Equifax vulnerable to lawsuits that claim the company acted negligently. This thesis analyzes the events and facts behind the incident to determine the probable outcome of the main case against Equifax. A claim of a breach can come from either Equifax’s data protection or breach response. This thesis concludes the results of the case depends on the final court to determine if Equifax acted negligently with its data protection. If the case ends in the Eleventh District Court of Appeals, the court will probably decide Equifax was negligent. If the case ends in the Supreme Court, the Court will probably decide Equifax was not negligent. -

February 9, 2020 Falling Real Interest Rates, Rising Debt: a Free Lunch?

February 9, 2020 Falling Real Interest Rates, Rising Debt: A Free Lunch? By Kenneth Rogoff, Harvard University1 1 An earlier version of this paper was presented at the American Economic Association January 3 2020 meeting in San Diego in a session entitled “The United States Economy: Growth, Stagnation or New Financial Crisis?” chaired by Dominick Salvatore. The author is grateful to Molly and Dominic Ferrante Fund at Harvard University for research support. 1 With real interest rates hovering near multi-decade lows, and even below today’s slow growth rates, has higher government debt become a proverbial free lunch in many advanced countries?2 It is certainly true that low borrowing rates help justify greater government spending on high social return investment and education projects, and should make governments more relaxed about countercyclical fiscal policy, the “free lunch” perspective is an illusion that ignores most governments’ massive off-balance-sheet obligations, as well the possibility that borrowing rates could rise in a future economic crisis, even if they fell in the last one. As Lawrence Kotlikoff (2019) has long emphasized (see also Auerbach, Gokhale and Kotlikoff, 1992) 3 standard measures of government in debt have in some sense become an accounting fiction in the modern post World War II welfare state. Every advanced economy government today spends more on publicly provided old age support and pensions alone than on interest payment, and would still be doing so even if real interest rates on government debt were two percent higher. And that does not take account of other social insurance programs, most notably old-age medical care. -

Debt Collection Guide Update

Debt Collection Guide Update This Update includes new information you should know when dealing with debt collectors. 1. In New York, a debt collector cannot collect or attempt to collect on a payday loan. Payday loans are illegal in New York. A payday loan is a high-interest loan borrowed against your next paycheck. To apply for a payday loan, you need to have a checking account and proof of income. In New York State, most payday loans are handled by phone or online. If a collection agency tries to collect on a payday loan, visit nyc.gov/dca or contact 311 to file a complaint with DCA. 2. Beware of debt collection companies or companies working with debt collection companies that offer you a credit card if you repay, in part or in full, an old debt that may have expired. Companies may use terms like “Fresh Start Program” or “Balance Transfer Program” to describe offers to transfer your old debt to a new credit card account after you make a certain number of payments. If you accept the credit card offer and start making pay- ments, the debt collection agency’s time limit (statute of limitations) for suing you to collect this debt will restart. The company offering the credit card may not tell you that this is a consequence of getting the credit card. See the section What Should You Do When a Debt Collection Agency Contacts You? for information about statute of limitations. 3. It is illegal for a debt collection agency to use “caller ID spoofing.” Some debt collection agencies are using spoofed (or faked) phone numbers to disguise their identities on caller ID. -

2016 Donors & Supporters

2016 DONORS Miracle Maker ($500,000+) Dream Maker ($10,000+) The Arthur M. Blank Family Foundation Allison-Smith Company, LLC Office of Juvenile Justice and Anonymous Deliquency Prevention The Atlanta Foundation The Marcus Foundation, Inc. Atlantic Trust Private Wealth United Way of Greater Atlanta, Inc. Management Berry Plastics Corporation Marvel Maker ($50,000+) Builders 2020 The AEC Trust Chick-fil-A Foundation Altria Deloitte Big Brothers Big Sisters of America Diversey Care CHEP Douglas J. Hertz Family Foundation, Teresa and Alexander Cummings Inc. Georgia Power Company Fannie Mae IBERIABANK Frances Wood Wilson Foundation, Inc. The Rich Foundation, Inc. Gary W. Rollins Foundation Georgia State University Friendship Maker ($25,000+) The Gillin Family Brand Mortgage Global Concessions, Inc. The CIGNA Foundation GOJO Industries Cobb County Board of Commissioners Heritage Bag Company The Coca-Cola Company The Home Depot Foundation Cox Enterprises, Inc. International Paper Equifax, Inc. Kimberly-Clark Corporation EY Leapley Construction GE Energy Services/ GE Energy Kelly L. Loeffler & Jeff Sprecher Georgia-Pacific Corporation Los Angeles Dodgers KPMG, LLP Masters Capital Management, LLC Publix Super Markets Charities, Inc. McKinsey & Company Salesforce Newell Rubbermaid Sealed Air Company Nordstrom Scott Hudgens Family Foundation, Inc. John Pensec The Sara Giles Moore Foundation PRGX USA Inc. The UPS Foundation Pricewaterhouse Coopers, LLP WestRock Pulte Group, Inc. The Sartain Lanier Family Foundation 1 2016 DONORS SCA Wells Fargo Southwire Company Lauren White UPM Scott Yancey Veritiv Corporation Verso Corporation Match Maker ($1,000+) The Weather Channel A2b Fulfillment Wells Fargo Foundation John Adams Alpha Phi Alpha Magic Maker ($5,000+) America's Charities Arby's Foundation, Inc. -

A Roadmap to the Preparation of the Statement of Cash Flows

A Roadmap to the Preparation of the Statement of Cash Flows May 2020 The FASB Accounting Standards Codification® material is copyrighted by the Financial Accounting Foundation, 401 Merritt 7, PO Box 5116, Norwalk, CT 06856-5116, and is reproduced with permission. This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte shall not be responsible for any loss sustained by any person who relies on this publication. The services described herein are illustrative in nature and are intended to demonstrate our experience and capabilities in these areas; however, due to independence restrictions that may apply to audit clients (including affiliates) of Deloitte & Touche LLP, we may be unable to provide certain services based on individual facts and circumstances. As used in this document, “Deloitte” means Deloitte & Touche LLP, Deloitte Consulting LLP, Deloitte Tax LLP, and Deloitte Financial Advisory Services LLP, which are separate subsidiaries of Deloitte LLP. Please see www.deloitte.com/us/about for a detailed description of our legal structure. Copyright © 2020 Deloitte Development LLC. All rights reserved. Publications in Deloitte’s Roadmap Series Business Combinations Business Combinations — SEC Reporting Considerations Carve-Out Transactions Comparing IFRS Standards and U.S.