Hamburg Commercial Bank AG

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2020 Sample Delegate List

2020 Sample Delegate List Join 600+ institutional and private investors alongside fund managers, developers, telecoms, energy companies and the world's governments for four days of unrivalled networking opportunities and cutting-edge content. Here is a sample of some of the biggest names in the industry who you could meet in March: • Arendt & Medernach • Ancala Partners • 3i Group • APFC • 4IP Group • APG Asset Management • A.P. Moller Capital • Apollo Global Management • Aarden • Aquila Capital Management • Abu Dhabi Investment Authority • Arcus Infrastructure Partners • ABVCAP • Ardian • Access Capital Partners • Arjun Infrastructure • Achmea Investment Management • Arpinge • Actis • ASFO • Africa Investor • Ashurst • Africa50 • Asian Infrastructure Investment Bank • Al Saheal Property Development & • Asper Investment Management Management • Astarte Capital Partners • Alberta Teachers' Retirement Fund • Asterion Industrial Partners • Alberta Teachers' Retirement Fund Board • Astrid Advisors • Allen & Overy • ATLAS Infrastructure • Allianz Capital Partners • ATP • Altamar Capital Partners • AXA Real Estate Investment Managers • AMF Pension • Axium Infrastructure • AMP Capital • Bain & Company • Analysys Mason • Barmenia For more information, visit the website here. Last updated 21/01/2020 • Basalt Infrastructure Partners • Cooperatie • Bases Conversion and Development • Copenhagen Infrastructure Partners Authority (BCDA) • Covalis Capital • BayWa r.e. renewable energy • CPPIB • bfinance • CPV-CAP Pensionskasse Coop • Bimcor • Credit -

Participant List

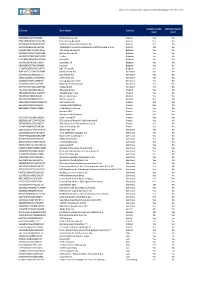

Participant list GC SecLend Select Select Participant Country City Repo Market HQLAx Pooling CCP Invest Finance Aareal Bank AG D Wiesbaden x x ABANCA Corporaction Bancaria S.A E Betanzos x ABN AMRO Bank N.V. NL Amsterdam x x ABN AMRO Clearing Bank N.V. NL Amsterdam x x x Airbus Group SE NL Leiden x x Allgemeine Sparkasse Oberösterreich Bank AG A Linz x x ASR Levensverzekering N.V. NL Utrecht x x ASR Schadeverzekering N.V. NL Utrecht x x Augsburger Aktienbank AG D Augsburg x x B. Metzler seel. Sohn & Co. KGaA D Frankfurt x x Baader Bank AG D Unterschleissheim x x Banco Bilbao Vizcaya Argentaria, S.A. E Madrid x x Banco Cooperativo Español, S.A. E Madrid x x Banco de Investimento Global, S.A. PT Lisbon x x Banco de Sabadell S.A. E Alicante x x Banco Santander S.A. E Madrid x x Bank für Sozialwirtschaft AG D Cologne x x Bank für Tirol und Vorarlberg AG A Innsbruck x x Bankhaus Lampe KG D Dusseldorf x x Bankia S.A. E Madrid x x Banque Centrale du Luxembourg L Luxembourg x x Banque Lombard Odier & Cie SA CH Geneva x x Banque Pictet & Cie AG CH Geneva x x Banque Internationale à Luxembourg L Luxembourg x x x Bantleon Bank AG CH Zug x Barclays Bank PLC GB London x x Barclays Bank Ireland Plc IRL Dublin x x BAWAG P.S.K. A Vienna x x Bayerische Landesbank D Munich x x Belfius Bank B Brussels x x Berlin Hyp AG D Berlin x x BGL BNP Paribas L Luxembourg x x BKS Bank AG A Klagenfurt x x BNP Paribas Fortis SA/NV B Brussels x x BNP Paribas S.A. -

Exchange Council Election Eurex Deutschland Preliminary Voter List – As of 16 August 2019

Exchange Council Election Eurex Deutschland Preliminary Voter List – as of 16 August 2019 Voter group 1a cooperative credit institutions Company State DZ BANK AG Deutsche Zentral-Genossenschaftsbank Germany Page - 1 - Exchange Council Election Eurex Deutschland Preliminary Voter List – as of 16 August 2019 Voter group 1b credit institutions under public law Company State Bayerische Landesbank Germany DekaBank Deutsche Girozentrale Germany Hamburger Sparkasse AG Germany Kreissparkasse Köln Germany Landesbank Hessen-Thüringen Girozentrale Germany Landesbank Saar Germany Norddeutsche Landesbank - Girozentrale Germany NRW.BANK Germany Sparkasse Pforzheim Calw Germany Page - 2 - Exchange Council Election Eurex Deutschland Preliminary Voter List – as of 16 August 2019 Voter group 1c other credit institutions Company State ABN AMRO Bank N.V. Netherlands ABN AMRO Clearing Bank N.V. Netherlands B. Metzler seel. Sohn & Co. KGaA Germany Baader Bank Aktiengesellschaft Germany Banca Akros S.p.A. Italy Banca IMI S.p.A Italy Banca Sella Holding S.p.A. Italy Banca Simetica S.p.A. Italy Banco Bilbao Vizcaya Argentaria S.A. Spain Banco Comercial Português S.A. Portugal Banco Santander S.A. Spain Bank J. Safra Sarasin AG Switzerland Bank Julius Bär & Co. AG Switzerland Bank Vontobel AG Switzerland Bankhaus Lampe KG Germany Bankia S.A. Spain Bankinter Spain Banque de Luxembourg Luxemburg Banque Lombard Odier & Cie SA Switzerland Banque Pictet & Cie SA Switzerland Barclays Bank Ireland Plc Ireland Barclays Bank PLC United Kingdom Basler Kantonalbank Switzerland Berner Kantonalbank AG Switzerland Bethmann Bank AG Germany BNP Paribas United Kingdom BNP Paribas (Suisse) SA Switzerland BNP Paribas Fortis SA/NV Belgium BNP Paribas S.A. Niederlassung Deutschland Germany BNP Paribas Securities Services S.C.A. -

Interim Report As at 30 June 2020 Hamburg Commercial Bank

Interim Report as at 30 June 2020 Hamburg Commercial Bank Group overview INCOME STATEMENT (€ million ) BALANCE SHEET (€ billion) Net income before restructuring and Reported equity privatisation January - June 2020 30.06.2020 (cf. January - June 2019: 104) (cf. 31.12.2019: 4.4) ↘ 76 → 4.4 Net income before taxes Total assets 30.06.2020 (cf. January - June 2019: 96) (cf. 31.12.2019: 47.7) ↘ 71 ↘ 41.8 Group net result Business volume 30.06.2020 (cf. January - June 2019: 5) (cf. 31.12.2019: 55.6) ↘ 4 ↘ 48.0 CAPITAL RATIO & RWA (%)1) EMPLOYEES (computed on full-time equivalent basis) CET1 ratio 30.06.2020 (cf. 31.12.2019: 18.5) Total 30.06.2020 (cf. 31.12.2019: 1,482) ↗ 21.7 ↘ 1,215 Total capital ratio 30.06.2020 Germany 30.06.2020 (cf. 31.12.2019: 23.5) (cf. 31.12.2019: 1,421) ↗ 27.0 ↘ 1,180 Risk weighted assets (RWA) 30.06.2020 Abroad 30.06.2020 (€ billion) (cf. 31.12.2019: 21.0) (cf. 31.12.2019: 61) ↘ 19.0 ↘ 35 Due to rounding, numbers presented throughout this report may not add up to the totals disclosed and percentages may not precisely reflect the absolute figures. 1) Not in-period: regulatory disclosure pursuant to the CRR Content Interim Management Interim group financial Report statements 2 Economic report 46 Group statement of income 2 Underlying economic and industry conditions 7 Business development 47 Group statement of comprehensive income 9 Earings, net assets and financial position 17 Segment results 48 Group statement of financial position 19 Employees of Hamburg Commercial Bank 50 Group statement of changes in equity 21 -

2019-03-28 Investor Presentation

Investor Presentation IFRS Group Result as at 31 December 2018 28 March 2019 Hamburg Commercial Bank – What we are … … now a private commercial bank. True to Hanseatic tradition, we make clear promises and keep them: For us it’s only one • Reliable direction: • Client-centric Clearly ahead. We act towards the future. • Sincere Business Clients Real Estate Project Finance – Renewable Energy and Infrastructure Shipping Capital Markets & Products Investor Presentation - IFRS Group Result 2018 2 28 March 2019 Agenda 1. Closing – Privatisation process 2. Transformation process 3. Financial key figures for 2018 4. Outlook 2019 5. Appendix Investor Presentation - IFRS Group Result 2018 3 28 March 2019 Highlights 2018 EU-COM approved state aid-free privatisation of the bank Management Board – continuity and proven track record with additional expertise of the new board member for markets Transition of protection scheme from public sector to private banks envisaged Comprehensive relief from legacy burdens – dissolution of Non-Core Bank and early termination of guarantee Moody’s and S&P acknowledge improved financial profile of Hamburg Commercial Bank Transformation of business strategy to achieve objectives in 2022 Start with very solid financial profile: strong CET1 and comfortable liquidity ratios, as well as healthy portfolio New shareholders – strong expertise and high level of commitment Investor Presentation - IFRS Group Result 2018 4 28 March 2019 New shareholders with strong expertise, proven track record and reliable commitment New shareholder structure Several funds initiated by One fund advised by One fund initiated by Centaurus BAWAG P.S.K. Cerberus Capital Management, L.P. J.C. Flowers & GoldenTree Asset Capital LP Co. -

Greek Shipping Portfolios

Key Developments and Growth in Greek Ship-Finance June 2020 By Ted Petropoulos, Head, Petrofin Research ©. Petrofin Research© presents, for the 19th year running, an overview and an in-depth analysis of the bank loan portfolios to Greek shipping, as of 31st December 2019. Petrofin wish to thank all participating banks for their steadfast support, without which this research would not have been possible. The portfolios show both the shipping loans outstanding, as well as loans committed but undrawn. The committed but undrawn loans may be viewed as an indication of each bank’s ship lending momentum and / or the extent of its involvement in newbuilding finance. Contents 1. Main Findings p. 2 2. Petrofin Index Of Greek Shipfinance p. 3 3. Total Greek Shipfinance Portfolio As Of End 2019 p. 4 4. Research And Analysis A. The Greek shipfinance market as of end 2019 p. 6 B. Analysis of the 3 Bank Groups p. 14 C. Newbuilding finance research p. 27 D. The Greek Shipping Syndications market p. 28 5. Highlights Of This Year’s Research p. 29 6. The Outlook For 2020 And Beyond p. 30 1 Petrofin Research© - www.petrofin.gr June 2020 1. Main findings Highlight points of this year’s results for Greek ship finance are as follows: Bank shipfinance for Greek shipping has slowed down its decline further to -0.13% compared to -1.52% during 2018 from -5.62% in 2017 and -8.77% during 2016. The Petrofin Index for Greek Shipfinance, which commenced at 100 in 2001 and peaked at 443 in 2008, fell from 322 to 321. -

Patrick Cichy

Patrick Cichy Partner Corporate and M&A excellent content, strong client focus Client, JUVE Handbook 2018/2019 Primary practice Corporate and M&A 29/09/2021 Patrick Cichy | Freshfields Bruckhaus Deringer About Patrick Cichy <p><strong>Patrick is a partner in our global transaction practice. </strong></p> <p>Since joining the firm, he has worked across many industries with a particular focus on financial institutions.</p> <p>Patrick is often recommended for financial institutions and corporate/M&A advice and has built long-term relationships with clients for whom he has acted.</p> <p>He is very comfortable with complex, high-profile transactions. His MBA enables him to focus on and add value to the commercial aspects of each deal, while his nine-month secondment to Deutsche Bank’s M&A department in New York and his long-term advice in particular for Hamburg Commercial Bank mean Patrick understands the workings of large financial institutions. He also has good knowledge of the renewable energy and infrastructure/transport sectors.</p> <p>Patrick is our lead country partner for the Nordics, the author of various publications and a regular speaker at conferences.</p> <p>A native German speaker, Patrick also speaks English and French.</p> Recent work <ul> <li>Advising Hamburg Commercial Bank (ex HSH Nordbank) since 2009 on several large projects, including its restructuring, EU subsidy proceedings, recovery and resolution planning, AQR/stress test, sale of a €5bn non-performing shipping portfolio to a state-owned -

NORD/LB Covered Bond Special

1 / Covered Bond & SSA View 16. März 2021 Transparency requirements §28 PfandBG Q4/2020 Markets Strategy & Floor Research 16 March 2021 Marketing communication (see disclaimer on the last pages) 2 / Transparency requirements §28 PfandBG 16 March 2021 Agenda Authors: Dr. Frederik Kunze // Henning Walten, CIIA Market overview 4 Mortgage covered bonds 9 Aareal Bank 10 Bausparkasse Mainz 11 Bausparkasse Schwäbisch Hall 12 Bayerische Landesbank 13 Berlin Hyp 14 Commerzbank 15 DekaBank 16 Deutsche Apotheker- und Ärztebank 17 Deutsche Bank 18 Deutsche Hypothekenbank 19 Deutsche Kreditbank 20 Deutsche Pfandbriefbank 21 DSK Hyp 22 DZ HYP 23 Hamburg Commercial Bank 24 Hamburger Sparkasse 25 ING-DiBa 26 Kreissparkasse Köln 27 Landesbank Baden-Württemberg 28 Landesbank Berlin 29 Landesbank Hessen-Thüringen 30 M.M.Warburg & CO Hypothekenbank 31 Münchener Hypothekenbank 32 Natixis Pfandbriefbank 33 Norddeutsche Landesbank 34 PSD Bank Nürnberg 35 PSD Bank Rhein-Ruhr 36 SaarLB 37 Santander Consumer Bank 38 Sparkasse Hannover 39 Sparkasse KölnBonn 40 Stadtsparkasse Düsseldorf 41 UniCredit Bank 42 Wüstenrot Bausparkasse 43 3 / Transparency requirements §28 PfandBG 16 March 2021 Public sector covered bonds 44 Aareal Bank 45 Bayerische Landesbank 46 Berlin Hyp 47 Commerzbank 48 DekaBank 49 Deutsche Bank 50 Deutsche Hypothekenbank 51 Deutsche Kreditbank 52 Deutsche Pfandbriefbank 53 DSK Hyp 54 DZ HYP 55 Hamburg Commercial Bank 56 Kreissparkasse Köln 57 Landesbank Baden-Württemberg 58 Landesbank Berlin 59 Landesbank Hessen-Thüringen 60 LIGA Bank 61 M.M. Warburg -

Rating Report Sparkassen-Finanzgruppe

Rating Report Sparkassen-Finanzgruppe DBRS Morningstar Ratings 20 May 2020 Debt Rating Rating Action Trend Long-Term Issuer Rating A Confirmed Positive Contents Short-Term Issuer Rating R-1 (low) Confirmed Positive 2 Franchise Strength Long-Term Senior Debt A Confirmed Positive 8 Earnings Power 12 Risk Profile Short-Term Debt R-1 (low) Confirmed Positive 15 Funding and Liquidity Senior Non-Preferred Debt A (low) Confirmed Positive 17 Capitalisation 21 Annex: Institutional Protection Scheme 23 Company Financials Rating Drivers Rating Considerations 25 Ratings Factors with Positive Rating Implications Franchise Strength (Very Strong/Strong) 25 Related Research • A manageable impact of the COVID-19 outbreak on • The Sparkassen-Finanzgruppe’s (SFG) aggregated balance SFG’s earnings and asset quality metrics and the sheet of close to EUR 2.2 trillion makes the Group of vital German economy overall would likely lead to an up- importance for the German economy, offering a full set of grade of the ratings. financial services to their customers with considerable Sonja Förster • In addition, the successful creation of a central insti- market share in their respective markets. Vice President - Global FIG +49 69 8088 3510 tution, which could drive further efficiency gains and Earnings Power (Good) improve corporate governance could lead to a rating [email protected] • Despite a possible temporary spike in loan demand and an upgrade. improvement in margins due to lower competition we ex- Elisabeth Rudman pect a significant negative impact over the medium term Managing Director - Head of European FIG - from the current Corona pandemic due to lower economic Global FIG activity and mounting loan losses as well as the continua- +44 20 7855 6655 tion of the low rate environment for a longer period. -

Various German Banks Downgraded on Persistent Profitability Challenges and Slow Digitalization Progress

Various German Banks Downgraded On Persistent Profitability Challenges And Slow Digitalization Progress June 24, 2021 - We anticipate that German banks' asset quality and capitalization will likely remain robust, PRIMARY CREDIT ANALYST supported by the German economy's resilience amid the COVID-19 pandemic. Harm Semder Frankfurt - Nevertheless, we believe the pandemic has exacerbated challenges facing the German banking + 49 693 399 9158 sector, and that German banks are now less competitive relative to global peers' due to slow harm.semder progress improving revenue diversification, cost structures, and digitalization. @spglobal.com - As a result, we have downgraded a number of Germany-based, non-government-related banks SECONDARY CONTACTS where our ratings did not already reflect these challenges. Benjamin Heinrich, CFA, FRM Frankfurt FRANKFURT (S&P Global Ratings) June 24, 2021--S&P Global Ratings today said that it has + 49 693 399 9167 lowered by one notch the long-term issuer credit ratings on the following Germany-based banks: benjamin.heinrich @spglobal.com - The Cooperative Banking Sector Germany and its related core members; Giles Edwards - DekaBank Deutsche Girozentrale; London + 44 20 7176 7014 - Core members of S-Finanzgruppe Hessen-Thueringen including Landesbank giles.edwards Hessen-Thueringen Girozentrale (Helaba) and local savings banks; @spglobal.com Markus W Schmaus - Deutsche Pfandbriefbank AG (pbb); and Frankfurt - Volkswagen Bank GmbH. + 49 693 399 9155 markus.schmaus @spglobal.com In addition, we affirmed our ratings on Commerzbank AG and UniCredit Bank AG with negative outlooks. We also revised the outlook on Hamburg Commercial Bank AG to developing from Heiko Verhaag, CFA, FRM Frankfurt negative, and affirmed the ratings. -

EBA List of Institutions for the Purpose of Supervisory Benchmarking (2021

EBA list of institutions for supervisory benchmarking as of 31 Dec 2020 Submits Credit Submits Market LEI Code Bank Name Country Risk? Risk? 529900S9YO2JHTIIDG38 BAWAG Group AG Austria Yes No PQOH26KWDF7CG10L6792 Erste Group Bank AG Austria Yes Yes 9ZHRYM6F437SQJ6OUG95 Raiffeisen Bank International AG Austria Yes Yes 529900IQMS1E10HN8V33 Volkskredit Verwaltungsgenossenschaft reg.Gen.m.b.H. Austria Yes No LSGM84136ACA92XCN876 AXA Bank Europe SA Belgium Yes No A5GWLFH3KM7YV2SFQL84 Belfius Banque SA Belgium Yes Yes 549300DYPOFMXOR7XM56 Crelan Belgium Yes No D3K6HXMBBB6SK9OXH394 Dexia NV Belgium No Yes 549300CBNW05DILT6870 Euroclear SA Belgium Yes No 5493008QOCP58OLEN998 Investar Belgium Yes No 213800X3Q9LSAKRUWY91 KBC Group NV Belgium Yes Yes MAES062Z21O4RZ2U7M96 Danske Bank A/S Denmark Yes Yes 529900PR2ELW8QI1B775 DLR Kredit A/S Denmark Yes No 3M5E1GQGKL17HI6CPN30 Jyske Bank A/S Denmark Yes No 213800UYAHIRLZ4NSN67 Lån og Spar Bank A/S Denmark Yes No LIU16F6VZJSD6UKHD557 Nykredit Realkredit A/S Denmark Yes Yes GP5DT10VX1QRQUKVBK64 Sydbank A/S Denmark Yes No 743700GC62JLHFBUND16 Aktia Bank Abp Finland Yes No 7437006WYM821IJ3MN73 Ålandsbanken Abp Finland Yes No 529900ODI3047E2LIV03 Nordea Bank Abp Finland Yes Yes 7437003B5WFBOIEFY714 OP Osuuskunta Finland Yes No R0MUWSFPU8MPRO8K5P83 BNP Paribas SA France Yes Yes 969500GVS02SJYG9S632 CARREFOUR BANQUE France Yes No 9695000CG7B84NLR5984 Crédit Mutuel Group France Yes No Groupe BPCE France Yes Yes Groupe Credit Agricole France Yes Yes F0HUI1NY1AZMJMD8LP67 HSBC France (*) France Yes Yes 96950001WI712W7PQG45 -

As of 10/31/2020

Annual Report | October 31, 2020 Vanguard Total International Bond Index Fund See the inside front cover for important information about access to your fund’s annual and semiannual shareholder reports. Important information about access to shareholder reports Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of your fund’s annual and semiannual shareholder reports will no longer be sent to you by mail, unless you specifically request them. Instead, you will be notified by mail each time a report is posted on the website and will be provided with a link to access the report. If you have already elected to receive shareholder reports electronically, you will not be affected by this change and do not need to take any action. You may elect to receive shareholder reports and other communications from the fund electronically by contacting your financial intermediary (such as a broker-dealer or bank) or, if you invest directly with the fund, by calling Vanguard at one of the phone numbers on the back cover of this report or by logging on to vanguard.com. You may elect to receive paper copies of all future shareholder reports free of charge. If you invest through a financial intermediary, you can contact the intermediary to request that you continue to receive paper copies. If you invest directly with the fund, you can call Vanguard at one of the phone numbers on the back cover of this report or log on to vanguard.com. Your election to receive paper copies will apply to all the funds you hold through an intermediary or directly with Vanguard.