2019-03-28 Investor Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Datenschutzhinweise

Datenschutzhinweise Unser Umgang mit Ihren Daten und Ihre Rechte – Informationen nach Art. 13, 14 und 21 der Datenschutz-Grundverordnung (DS-GVO) – Stand der Informationen: 30.03.2020 Sehr geehrte Kundin, sehr geehrter Kunde, Ihr Vertrauen hat für uns eine hohe Bedeutung. Aus diesem Grund respektieren und schützen wir Ihre Privatsphäre. Wir gehen mit den Daten von Kunden, Interessenten, Mitarbeitern, Bewerbern und Geschäftspartnern sorgsam um und schützen diese vor Missbrauch. Im Folgenden informieren wir Sie über die Verarbeitung Ihrer personenbezogenen Daten durch die Investitionsbank Sachsen-Anhalt – Anstalt der Norddeutschen Landesbank – Girozentrale – (nachfolgend IB genannt) und die Ihnen nach den datenschutzrechtlichen Regelungen zustehenden Ansprüche und Rechte. Welche Daten im Einzelnen verarbeitet und in welcher Weise genutzt werden, richtet sich maßgeblich nach den jeweils von Ihnen beantragten Förderungen bzw. mit Ihnen geschlossenen Verträgen oder vereinbarten Dienstleistungen. 1. Wer ist für die Datenverarbeitung verantwortlich und an wen kann ich mich wenden? Verantwortliche Stelle ist: Investitionsbank Sachsen-Anhalt Anstalt der Norddeutschen Landesbank - Girozentrale Domplatz 12 39104 Magdeburg Telefon: 0391 / 589 - 17 45 Fax: 0391 / 589 - 17 54 E-Mail-Adresse: [email protected] Unseren betrieblichen Datenschutzbeauftragten erreichen Sie unter: Investitionsbank Sachsen-Anhalt Anstalt der Norddeutschen Landesbank - Girozentrale Datenschutzbeauftragter Domplatz 12 39104 Magdeburg Telefon: 0391 / 589 - 8373 E-Mail-Adresse: [email protected] Investitionsbank Sachsen-Anhalt Telefon 03 91 / 5 89 – 17 45 Norddeutsche Landesbank Handelsregister Anstalt der Norddeutschen Landesbank Telefax 03 91 / 5 89 – 17 54 Girozentrale AG Hannover HRA 26247 Girozentrale E-Mail [email protected] Sitz: Hannover, Braunschweig AG Braunschweig HRA 10261 Domplatz 12 39104 Magdeburg www.ib-sachsen-anhalt.de Magdeburg AG Stendal HRA 22150 Postfach 3840 39013 Magdeburg 2. -

2020 Sample Delegate List

2020 Sample Delegate List Join 600+ institutional and private investors alongside fund managers, developers, telecoms, energy companies and the world's governments for four days of unrivalled networking opportunities and cutting-edge content. Here is a sample of some of the biggest names in the industry who you could meet in March: • Arendt & Medernach • Ancala Partners • 3i Group • APFC • 4IP Group • APG Asset Management • A.P. Moller Capital • Apollo Global Management • Aarden • Aquila Capital Management • Abu Dhabi Investment Authority • Arcus Infrastructure Partners • ABVCAP • Ardian • Access Capital Partners • Arjun Infrastructure • Achmea Investment Management • Arpinge • Actis • ASFO • Africa Investor • Ashurst • Africa50 • Asian Infrastructure Investment Bank • Al Saheal Property Development & • Asper Investment Management Management • Astarte Capital Partners • Alberta Teachers' Retirement Fund • Asterion Industrial Partners • Alberta Teachers' Retirement Fund Board • Astrid Advisors • Allen & Overy • ATLAS Infrastructure • Allianz Capital Partners • ATP • Altamar Capital Partners • AXA Real Estate Investment Managers • AMF Pension • Axium Infrastructure • AMP Capital • Bain & Company • Analysys Mason • Barmenia For more information, visit the website here. Last updated 21/01/2020 • Basalt Infrastructure Partners • Cooperatie • Bases Conversion and Development • Copenhagen Infrastructure Partners Authority (BCDA) • Covalis Capital • BayWa r.e. renewable energy • CPPIB • bfinance • CPV-CAP Pensionskasse Coop • Bimcor • Credit -

NORD/LB Group Annual Report 2009

Die norddeutsche Art. Stability – the best link to the future Annual Report 2009 NORD/LB Annual Report 2009 Erweiterter Konzernvorstand (extended Group Managing Board) left to right: Dr. Johannes-Jörg Riegler, Harry Rosenbaum, Dr. Jürgen Allerkamp, Dr. Gunter Dunkel, Christoph Schulz, Dr. Stephan-Andreas Kaulvers, Dr. Hinrich Holm, Eckhard Forst These are our figures 1 Jan.–31 Dec. 1 Jan.–31 Dec. Change 2009 2008 (in %) In € million Net interest income 1,366 1,462 – 7 Loan loss provisions – 1,042 – 266 > 100 Net commission income 177 180 – 2 ProÞ t/loss from Þ nancial instruments at fair value through proÞ t or loss including hedge accounting 589 – 308 > 100 Other operating proÞ t/loss 144 96 50 Administrative expenses 986 898 10 ProÞ t/loss from Þ nancial assets – 140 – 250 44 ProÞ t/loss from investments accounted – 200 6 > 100 for using the equity method Earnings before taxes – 92 22 > 100 Income taxes 49 – 129 > 100 Consolidated proÞ t – 141 151 > 100 Key Þ gures in % Cost-Income-Ratio (CIR) 47.5 62.5 Return on Equity (RoE) – 2.7 – 31 Dec. 31 Dec. Change 2009 2008 (in %) Balance Þ gures in € million Total assets 238,688 244,329 – 2 Customer deposits 61,306 61,998 – 1 Customer loans 112,083 112,172 – Equity 5,842 5,695 3 Regulatory key Þ gures (acc. to BIZ) Core capital in € million 8,051 7,235 11 Regulatory equity in € million 8,976 8,999 – Risk-weighted assets in € million 92,575 89,825 3 BIZ total capital ratio in % 9.7 10.0 BIZ core capital ratio in % 8.7 8.1 NORD/LB ratings (long-term / short-term / individual) Moody’s Aa2 / P-1 / C – Standard & Poor’s A– / A-2 / – Fitch Ratings A / F1 / C / D Our holdings Our subsidiaries and holding companies are an important element of our corporate strategy. -

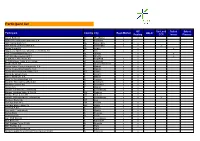

Participant List

Participant list GC SecLend Select Select Participant Country City Repo Market HQLAx Pooling CCP Invest Finance Aareal Bank AG D Wiesbaden x x ABANCA Corporaction Bancaria S.A E Betanzos x ABN AMRO Bank N.V. NL Amsterdam x x ABN AMRO Clearing Bank N.V. NL Amsterdam x x x Airbus Group SE NL Leiden x x Allgemeine Sparkasse Oberösterreich Bank AG A Linz x x ASR Levensverzekering N.V. NL Utrecht x x ASR Schadeverzekering N.V. NL Utrecht x x Augsburger Aktienbank AG D Augsburg x x B. Metzler seel. Sohn & Co. KGaA D Frankfurt x x Baader Bank AG D Unterschleissheim x x Banco Bilbao Vizcaya Argentaria, S.A. E Madrid x x Banco Cooperativo Español, S.A. E Madrid x x Banco de Investimento Global, S.A. PT Lisbon x x Banco de Sabadell S.A. E Alicante x x Banco Santander S.A. E Madrid x x Bank für Sozialwirtschaft AG D Cologne x x Bank für Tirol und Vorarlberg AG A Innsbruck x x Bankhaus Lampe KG D Dusseldorf x x Bankia S.A. E Madrid x x Banque Centrale du Luxembourg L Luxembourg x x Banque Lombard Odier & Cie SA CH Geneva x x Banque Pictet & Cie AG CH Geneva x x Banque Internationale à Luxembourg L Luxembourg x x x Bantleon Bank AG CH Zug x Barclays Bank PLC GB London x x Barclays Bank Ireland Plc IRL Dublin x x BAWAG P.S.K. A Vienna x x Bayerische Landesbank D Munich x x Belfius Bank B Brussels x x Berlin Hyp AG D Berlin x x BGL BNP Paribas L Luxembourg x x BKS Bank AG A Klagenfurt x x BNP Paribas Fortis SA/NV B Brussels x x BNP Paribas S.A. -

Exchange Council Election Eurex Deutschland Preliminary Voter List – As of 16 August 2019

Exchange Council Election Eurex Deutschland Preliminary Voter List – as of 16 August 2019 Voter group 1a cooperative credit institutions Company State DZ BANK AG Deutsche Zentral-Genossenschaftsbank Germany Page - 1 - Exchange Council Election Eurex Deutschland Preliminary Voter List – as of 16 August 2019 Voter group 1b credit institutions under public law Company State Bayerische Landesbank Germany DekaBank Deutsche Girozentrale Germany Hamburger Sparkasse AG Germany Kreissparkasse Köln Germany Landesbank Hessen-Thüringen Girozentrale Germany Landesbank Saar Germany Norddeutsche Landesbank - Girozentrale Germany NRW.BANK Germany Sparkasse Pforzheim Calw Germany Page - 2 - Exchange Council Election Eurex Deutschland Preliminary Voter List – as of 16 August 2019 Voter group 1c other credit institutions Company State ABN AMRO Bank N.V. Netherlands ABN AMRO Clearing Bank N.V. Netherlands B. Metzler seel. Sohn & Co. KGaA Germany Baader Bank Aktiengesellschaft Germany Banca Akros S.p.A. Italy Banca IMI S.p.A Italy Banca Sella Holding S.p.A. Italy Banca Simetica S.p.A. Italy Banco Bilbao Vizcaya Argentaria S.A. Spain Banco Comercial Português S.A. Portugal Banco Santander S.A. Spain Bank J. Safra Sarasin AG Switzerland Bank Julius Bär & Co. AG Switzerland Bank Vontobel AG Switzerland Bankhaus Lampe KG Germany Bankia S.A. Spain Bankinter Spain Banque de Luxembourg Luxemburg Banque Lombard Odier & Cie SA Switzerland Banque Pictet & Cie SA Switzerland Barclays Bank Ireland Plc Ireland Barclays Bank PLC United Kingdom Basler Kantonalbank Switzerland Berner Kantonalbank AG Switzerland Bethmann Bank AG Germany BNP Paribas United Kingdom BNP Paribas (Suisse) SA Switzerland BNP Paribas Fortis SA/NV Belgium BNP Paribas S.A. Niederlassung Deutschland Germany BNP Paribas Securities Services S.C.A. -

Norddeutsche Landesbank Girozentrale

Banks Wholesale Commercial Banks Germany Norddeutsche Landesbank Ratings Issuer Ratings Long-Term IDR A- Girozentrale Short-Term IDR F1 Derivative Counterparty Rating A(dcr) Viability Rating bb Support Rating 1 Sovereign Risk Long-Term Foreign-Currency AAA Key Rating Drivers IDR Long-Term Local-Currency IDR AAA Owners Support Drives Ratings: Norddeutsche Landesbank Girozentrale’s (NORD/LB) Country Ceiling AAA support-driven Issuer Default Ratings (IDRs) reflect its public sector owners’ commitment to the bank, which was recapitalised in 2019. They also reflect the bank’s statutory role and its Outlooks membership of Sparkassen Finanzgruppe’s (SFG; A+/Negative) institutional protection scheme Long-Term Foreign-Currency Negative (IPS). The Negative Outlook mirrors that of SFG and reflects medium downside risks of the IDR economic fallout from the coronavirus pandemic lasting longer than we expect. Sovereign Long-Term Foreign- Stable Currency IDR Profitability Drives VR: NORD/LB’s Viability Rating (VR) reflects the bank’s shifting business Sovereign Long-Term Local- Stable model and poor profitability. The bank’s adequate capitalisation and funding are relative rating Currency IDR strengths and should support the VR in the ‘bb’ range through the crisis. High Execution Risk: NORD/LB’s restructuring is progressing satisfactorily in terms of balance- sheet and headcount reduction and the wind-down of its remaining shipping exposure. However, the implementation of measures to achieve its ambitious medium-term cost and revenue targets are at an early stage. The pandemic could weigh on the programme’s success, despite Fitch Ratings’ expectation of an economic recovery in 2021. Weak Performance Prospects: High loan impairment charges (LICs), payments for guarantees received and restructuring costs could result in a net loss in 2020. -

List of Industry Respondents to the Second Consultation We Received a Total of 88 Respondents' Submissions

List of Industry Respondents to the Second Consultation We received a total of 88 respondents' submissions. No. Category Name of Bank/Merchant Bank Respondent Reference 1 Wholesale Bank ABN Amro Bank N.V. ABN 2 Wholesale Bank Banco Bilbao Vizcaya Argentaria, S.A. BBVA 3 Wholesale Bank Bank Julius Baer & Co Ltd Julius Baer 4 Qualifying Full Bank Bank of China Limited BOC 5 Wholesale Bank Barclays Bank PLC Barclays 6 Qualifying Full Bank BNP Paribas BNP 7 Wholesale Bank China Merchants Bank Co Ltd CMBC 8 Full Bank Citibank N.A. Citibank 9 Qualifying Full Bank Citibank Singapore Limited Citibank 10 Merchant Bank Citicorp Investment Bank (Singapore) Ltd Citicorp 11 Wholesale Bank Commerzbank Aktiengesellschaft Commerzbank 12 Wholesale Bank Commonwealth Bank of Australia CBA 13 Local Bank DBS Bank Ltd DBS 14 Wholesale Bank Deutsche Bank Aktiengesellschaft Deutsche 15 Merchant Bank DB International (Asia) Limited DB 16 Wholesale Bank DZ Bank AG DZ 17 Wholesale Bank EFG Bank AG EFG 18 Wholesale Bank Emirates NBD PJSC Emirates 19 Qualifying Full Bank ICICI Bank Limited ICICI 20 Full Bank Indian Bank Indian Bank 21 Qualifying Full Bank Industrial and Commercial Bank of China Limited ICBC 22 Wholesale Bank ING Bank N.V. ING 23 Full Bank JPMorgan Chase Bank, N.A. JPMorgan 24 Wholesale Bank KBC Bank N.V. KBC 25 Merchant Bank LGT Bank (Singapore) Ltd LGT 26 Offshore Bank Lloyds Bank PLC Lloyds 27 Merchant Bank LLoyds Merchant Bank Asia Limited Lloyds MB 28 Wholesale Bank Mitsubishi UFJ Trust & Banking Corporation MUTB 29 Full Bank Mizuho Bank Limited -

Interim Report As at 30 June 2020 Hamburg Commercial Bank

Interim Report as at 30 June 2020 Hamburg Commercial Bank Group overview INCOME STATEMENT (€ million ) BALANCE SHEET (€ billion) Net income before restructuring and Reported equity privatisation January - June 2020 30.06.2020 (cf. January - June 2019: 104) (cf. 31.12.2019: 4.4) ↘ 76 → 4.4 Net income before taxes Total assets 30.06.2020 (cf. January - June 2019: 96) (cf. 31.12.2019: 47.7) ↘ 71 ↘ 41.8 Group net result Business volume 30.06.2020 (cf. January - June 2019: 5) (cf. 31.12.2019: 55.6) ↘ 4 ↘ 48.0 CAPITAL RATIO & RWA (%)1) EMPLOYEES (computed on full-time equivalent basis) CET1 ratio 30.06.2020 (cf. 31.12.2019: 18.5) Total 30.06.2020 (cf. 31.12.2019: 1,482) ↗ 21.7 ↘ 1,215 Total capital ratio 30.06.2020 Germany 30.06.2020 (cf. 31.12.2019: 23.5) (cf. 31.12.2019: 1,421) ↗ 27.0 ↘ 1,180 Risk weighted assets (RWA) 30.06.2020 Abroad 30.06.2020 (€ billion) (cf. 31.12.2019: 21.0) (cf. 31.12.2019: 61) ↘ 19.0 ↘ 35 Due to rounding, numbers presented throughout this report may not add up to the totals disclosed and percentages may not precisely reflect the absolute figures. 1) Not in-period: regulatory disclosure pursuant to the CRR Content Interim Management Interim group financial Report statements 2 Economic report 46 Group statement of income 2 Underlying economic and industry conditions 7 Business development 47 Group statement of comprehensive income 9 Earings, net assets and financial position 17 Segment results 48 Group statement of financial position 19 Employees of Hamburg Commercial Bank 50 Group statement of changes in equity 21 -

Norddeutsche Landesbank Girozentrale Hanover (Incorporated

9 April 2014 PROSPECTUS Norddeutsche Landesbank Girozentrale Hanover (incorporated as public law institution (Anstalt des öffentlichen Rechts) established under, and governed by, the laws of the Federal Republic of Germany and the German Federal States (Bundesländer) of Lower Saxony (Niedersachsen) and Saxony-Anhalt (Sachsen- Anhalt)) ("Norddeutsche Landesbank – Girozentrale –", "NORD/LB" or the "Issuer") U.S.$500,000,000 Subordinated Fixed Rate Tier 2 Notes due 2024 (the "Notes") Issue Price of the Notes: 100.00 per cent. of the principal amount The Notes constitute direct, unconditional, subordinated and unsecured liabilities of the Issuer, as described in Section 2 of the Terms and Conditions of the Notes, and, unless previously redeemed or repurchased and cancelled, will mature on 10 April 2024 (the "Maturity Date"). The Notes will bear interest on their Par Value (as defined in Section 1 of the Terms and Conditions of the Notes), payable semi- annually in arrear on 10 April and 10 October of each year (each an "Interest Payment Date"), from 10 April 2014 (the "Issue Date") (inclusive) until the Maturity Date (exclusive) at the rate of 6.25 per cent. per annum. The Issuer may, at its option, redeem the Notes, in whole but not in part, for certain withholding tax reasons or upon the occurrence of a Regulatory Event (as defined in Section 5 Paragraph (2) of the Terms and Conditions of the Notes) at their Par Value plus accrued interest. Any such redemption is subject to the prior permission of the competent regulatory authority, if required, as described in Section 5 Paragraph (4) of the Terms and Conditions of the Notes. -

Greek Shipping Portfolios

Key Developments and Growth in Greek Ship-Finance June 2020 By Ted Petropoulos, Head, Petrofin Research ©. Petrofin Research© presents, for the 19th year running, an overview and an in-depth analysis of the bank loan portfolios to Greek shipping, as of 31st December 2019. Petrofin wish to thank all participating banks for their steadfast support, without which this research would not have been possible. The portfolios show both the shipping loans outstanding, as well as loans committed but undrawn. The committed but undrawn loans may be viewed as an indication of each bank’s ship lending momentum and / or the extent of its involvement in newbuilding finance. Contents 1. Main Findings p. 2 2. Petrofin Index Of Greek Shipfinance p. 3 3. Total Greek Shipfinance Portfolio As Of End 2019 p. 4 4. Research And Analysis A. The Greek shipfinance market as of end 2019 p. 6 B. Analysis of the 3 Bank Groups p. 14 C. Newbuilding finance research p. 27 D. The Greek Shipping Syndications market p. 28 5. Highlights Of This Year’s Research p. 29 6. The Outlook For 2020 And Beyond p. 30 1 Petrofin Research© - www.petrofin.gr June 2020 1. Main findings Highlight points of this year’s results for Greek ship finance are as follows: Bank shipfinance for Greek shipping has slowed down its decline further to -0.13% compared to -1.52% during 2018 from -5.62% in 2017 and -8.77% during 2016. The Petrofin Index for Greek Shipfinance, which commenced at 100 in 2001 and peaked at 443 in 2008, fell from 322 to 321. -

Patrick Cichy

Patrick Cichy Partner Corporate and M&A excellent content, strong client focus Client, JUVE Handbook 2018/2019 Primary practice Corporate and M&A 29/09/2021 Patrick Cichy | Freshfields Bruckhaus Deringer About Patrick Cichy <p><strong>Patrick is a partner in our global transaction practice. </strong></p> <p>Since joining the firm, he has worked across many industries with a particular focus on financial institutions.</p> <p>Patrick is often recommended for financial institutions and corporate/M&A advice and has built long-term relationships with clients for whom he has acted.</p> <p>He is very comfortable with complex, high-profile transactions. His MBA enables him to focus on and add value to the commercial aspects of each deal, while his nine-month secondment to Deutsche Bank’s M&A department in New York and his long-term advice in particular for Hamburg Commercial Bank mean Patrick understands the workings of large financial institutions. He also has good knowledge of the renewable energy and infrastructure/transport sectors.</p> <p>Patrick is our lead country partner for the Nordics, the author of various publications and a regular speaker at conferences.</p> <p>A native German speaker, Patrick also speaks English and French.</p> Recent work <ul> <li>Advising Hamburg Commercial Bank (ex HSH Nordbank) since 2009 on several large projects, including its restructuring, EU subsidy proceedings, recovery and resolution planning, AQR/stress test, sale of a €5bn non-performing shipping portfolio to a state-owned -

NORD/LB Covered Bond Special

1 / Covered Bond & SSA View 16. März 2021 Transparency requirements §28 PfandBG Q4/2020 Markets Strategy & Floor Research 16 March 2021 Marketing communication (see disclaimer on the last pages) 2 / Transparency requirements §28 PfandBG 16 March 2021 Agenda Authors: Dr. Frederik Kunze // Henning Walten, CIIA Market overview 4 Mortgage covered bonds 9 Aareal Bank 10 Bausparkasse Mainz 11 Bausparkasse Schwäbisch Hall 12 Bayerische Landesbank 13 Berlin Hyp 14 Commerzbank 15 DekaBank 16 Deutsche Apotheker- und Ärztebank 17 Deutsche Bank 18 Deutsche Hypothekenbank 19 Deutsche Kreditbank 20 Deutsche Pfandbriefbank 21 DSK Hyp 22 DZ HYP 23 Hamburg Commercial Bank 24 Hamburger Sparkasse 25 ING-DiBa 26 Kreissparkasse Köln 27 Landesbank Baden-Württemberg 28 Landesbank Berlin 29 Landesbank Hessen-Thüringen 30 M.M.Warburg & CO Hypothekenbank 31 Münchener Hypothekenbank 32 Natixis Pfandbriefbank 33 Norddeutsche Landesbank 34 PSD Bank Nürnberg 35 PSD Bank Rhein-Ruhr 36 SaarLB 37 Santander Consumer Bank 38 Sparkasse Hannover 39 Sparkasse KölnBonn 40 Stadtsparkasse Düsseldorf 41 UniCredit Bank 42 Wüstenrot Bausparkasse 43 3 / Transparency requirements §28 PfandBG 16 March 2021 Public sector covered bonds 44 Aareal Bank 45 Bayerische Landesbank 46 Berlin Hyp 47 Commerzbank 48 DekaBank 49 Deutsche Bank 50 Deutsche Hypothekenbank 51 Deutsche Kreditbank 52 Deutsche Pfandbriefbank 53 DSK Hyp 54 DZ HYP 55 Hamburg Commercial Bank 56 Kreissparkasse Köln 57 Landesbank Baden-Württemberg 58 Landesbank Berlin 59 Landesbank Hessen-Thüringen 60 LIGA Bank 61 M.M. Warburg