Various German Banks Downgraded on Persistent Profitability Challenges and Slow Digitalization Progress

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fitch Revises Outlooks on German Cooperative Banks and DZ BANK to Stable; Affirms at 'AA-'

01 JUL 2021 Fitch Revises Outlooks on German Cooperative Banks and DZ BANK to Stable; Affirms at 'AA-' Fitch Ratings - Frankfurt am Main - 01 Jul 2021: Fitch Ratings has revised Genossenschaftliche FinanzGruppe (GFG) and the members of its mutual support scheme, including GFG's central institution DZ BANK AG Deutsche Zentral-Genossenschaftsbank (DZ BANK) and 814 local cooperative banks, to Stable Outlook from Negative Outlook. Their Long-Term Issuer Default Ratings (IDRs) have been affirmed at 'AA-'. The revisions of the Outlooks reflect our view that the risk of significant deterioration of the operating environment, leading to a durable weakening of GFG's asset quality and profitability, has subsided since our last rating action in August 2020. GFG is not a legal entity but a cooperative banking network whose cohesion is ensured by a mutual support scheme managed by the National Association of German Cooperative Banks (BVR). GFG's IDRs apply to each member bank, in accordance with Annex 4 of Fitch's criteria for rating banking structures backed by mutual support schemes. The ratings are underpinned by the high effectiveness of the scheme given its long and successful record of ensuring GFG's cohesion, monitoring members' risks and enforcing corrective measures when needed. The scheme has effectively protected its members' viability and averted losses for their creditors since its inception. Fitch has also downgraded Deutsche Apotheker- und Aerztebank eG's (apoBank) Long-Term Deposit Rating because we no longer expect the bank's buffer of senior non-preferred and more junior debt to remain sustainably above 10% of risk weighted assets (RWAs) as the bank is not required to maintain resolution debt buffers. -

Annual Report 2008

Annual Report 2008 hannover re R CONTENTS 1 Boards and officers 6 Management report 6 Economic climate 7 Business development 10 Development of the individual lines of business 15 Investments 17 Human resources 20 Sustainability report 22 Risk report 28 Forecast 33 Other information 35 Accounts 36 Balance sheet 40 Profit and loss account 43 Notes 69 Auditors' report 70 Report of the Supervisory Board 74 Declaration of conformity 75 Glossary KEY FIGURES of Hannover Re +/- previous Figures in EUR million 2008 2007 2006 2005 2004 year Gross written premium 7,328.7 +10.2% 6,652.6 7,644.6 6,340.4 6,095.2 Net premium earned 5,429.4 +9.0% 4,979.3 5,685.3 4,383.8 4,030.8 Underwriting result 1) 78.9 -171.0% (111.1) 145.6 (95.5) (42.8) Allocation to the equalisation 33.6 110.9% (309.1) 145.4 228.3 232.5 reserve and similar provisions Investment result 66.9 -85.2% 451.2 799.9 895.7 584.7 Pre-tax profit (104.2) -123.8% 438.1 258.7 376.1 149.1 Profit or loss for the financial year (209.6) -177.1% 272.0 196.0 374.6 120.6 Investments 17,885.1 -1.2% 18,106.1 18,499.7 16,699.4 13,465.3 Capital and reserve 1,878.82) -9.9% 2,085.82) 2,085.82) 2,085.82)3) 1,215.8 Equalisation reserve and similar provisions 1,440.1 +2.4% 1,406.5 1,715.6 1,570.3 1,342.0 Net technical provisions 14,145.0 +6.5% 13,286.7 13,022.7 12,471.9 9,844.2 Total capital, reserves and technical provisions 17,463.9 +4.1% 16,779.0 16,824.1 16,128.0 12,402.0 Number of employees 708 +48 660 654 628 599 Retention 75.2% 73.9% 74.2% 68.3% 67.8% Loss ratio 1)4) 74.0% 80.0% 72.7% 76.7% 79.6% Expense ratio 4) 24.5% 25.2% 25.4% 26.4% 20.1% Combined ratio 1)4) 98.5% 105.2% 98.1% 103.1% 99.7% 1) including allocation to reserves proposed by the Annual General Meeting 2) including subordinated liabilities 3) excluding life reinsurance 4) from the 2006 financial year onwards the option of including special allocations to the provisions for outstanding claims in the non-technical account rather than the technical account will no longer be exercised. -

2020 Sample Delegate List

2020 Sample Delegate List Join 600+ institutional and private investors alongside fund managers, developers, telecoms, energy companies and the world's governments for four days of unrivalled networking opportunities and cutting-edge content. Here is a sample of some of the biggest names in the industry who you could meet in March: • Arendt & Medernach • Ancala Partners • 3i Group • APFC • 4IP Group • APG Asset Management • A.P. Moller Capital • Apollo Global Management • Aarden • Aquila Capital Management • Abu Dhabi Investment Authority • Arcus Infrastructure Partners • ABVCAP • Ardian • Access Capital Partners • Arjun Infrastructure • Achmea Investment Management • Arpinge • Actis • ASFO • Africa Investor • Ashurst • Africa50 • Asian Infrastructure Investment Bank • Al Saheal Property Development & • Asper Investment Management Management • Astarte Capital Partners • Alberta Teachers' Retirement Fund • Asterion Industrial Partners • Alberta Teachers' Retirement Fund Board • Astrid Advisors • Allen & Overy • ATLAS Infrastructure • Allianz Capital Partners • ATP • Altamar Capital Partners • AXA Real Estate Investment Managers • AMF Pension • Axium Infrastructure • AMP Capital • Bain & Company • Analysys Mason • Barmenia For more information, visit the website here. Last updated 21/01/2020 • Basalt Infrastructure Partners • Cooperatie • Bases Conversion and Development • Copenhagen Infrastructure Partners Authority (BCDA) • Covalis Capital • BayWa r.e. renewable energy • CPPIB • bfinance • CPV-CAP Pensionskasse Coop • Bimcor • Credit -

+01 Text Edeka

Kapitel 2 / Mechanismen und Folgen / Wo ist das Problem? Edeka Die Edeka-Gruppe (Eigenschreibweise: EDEKA) ist 1923 begann im Unternehmen die Zentralverrech- seit 2005 durch die Übernahme der Spar-Handels- nung. 1931 erreichten die Umsätze der inzwischen gesellschaft der größte Verbund im deutschen 430 Genossenschaften die Summe von 267 Millionen Einzelhandel. Eigentümer der Edeka-Gruppe sind Reichsmark. Die Stimmenverluste der Wirtschafts- Genossenschaften, in denen sich selbständige partei im Jahr 1932 lösten einen Druck der Edeka- Einzelhändler*innen zusammengeschlossen haben. Genossen auf die Verbandsführung aus, sich mehr Regionalgesellschaften sind für das Großhandelsge- den Positionen der Nationalsozialisten zuzuwen- schäft verantwortlich und beliefern die selbständi- den, doch die NSDAP honorierte das nicht. Ab 1933 gen Händler*innen wie die Filialbetriebe, die über stand Edeka mit seinen Genossenschaften unter die Regionalgesellschaften oder die Edeka-Zentrale Druck. Die Edeka-Gruppe forderte ihre Mitglieder AG & Co KG zur Gruppe gehören oder mit ihr ko- auf, den NS-„Kampfbünden für den gewerblichen operieren. Mittelstand“ beizutreten. Am 18. April erklärte sie freiwillig ihre Gleichschaltung mit der Folge, dass Geschichte ein Erster und ein Zweiter Präsident, jeweils mit Anfangszeit NSDAP-Parteibuch, dem Generaldirektor auf die Finger sahen. Borrmann wurde 1933 Parteimitglied. Die Edeka-Gruppe entstand 1898, als sich 21 Ab 1936 wurde das Handeln des Unternehmens Einkaufsvereine aus dem Deutschen Reich im dirigistisch reglementiert. Halleschen Torbezirk in Berlin zur Einkaufsgenos- Das Geschäftsgebiet von Edeka wurde auf das Saar- senschaft der Kolonialwarenhändler im Halleschen land und nach dem so genannten „Anschluss“ auch Torbezirk zu Berlin – kurz E. d. K. – zusammen- auf Österreich ausgedehnt. 1937 schied Borrmann schlossen. als Generaldirektor aus und Paul König übernahm Dreizehn solcher Genossenschaften vereinigten (bis 1966) dessen Funktion. -

Unternehmensbericht 2013 Unternehmensbericht 2013 EDEKA-Verbund Der EDEKA-Verbund – „Unternehmer-Unternehmen“ Und Treibende Kraft Im Deutschen Lebensmittelhandel

Unternehmensbericht 2013 EDEKA-Verbund EDEKA-Verbund ∙ Unternehmensbericht 2013 Unternehmensbericht ∙ EDEKA-Verbund Der EDEKA-Verbund – „Unternehmer-Unternehmen“ und treibende Kraft im deutschen Lebensmittelhandel Seit Jahrzehnten prägt der EDEKA-Verbund maßgeblich die Entwicklungen in der deutschen Lebensmittelwirtschaft. Mit ausgefeilten Strategien, dem ihm traditionell innewohnenden Unternehmergeist sowie einem ausgeprägten Innovationswillen. Ein eingespieltes Team aus mehr als 4.000 selbstständigen Kaufleuten, sieben regiona- len Großhandelsbetrieben und der Hamburger EDEKA-Zentrale repräsentiert dabei die unverkennbare Struktur aus drei leistungsstarken und flexibel agierenden Ver- bundstufen. Angetrieben von dem genossenschaftlichen Auftrag zur kontinuierlichen Schaffung und Förderung mittelständischer Betriebe im Lebensmitteleinzelhandel. Als der qualifizierte Nahversorger Deutschlands steht EDEKA für generationenüber- greifenden, nachhaltigen und ökonomisch verantwortungsvollen Handel. Umsatzentwicklung EDEKA-Verbund Nettoumsätze in Mrd. € 2009* 2010* 2011* 2012 2013 % Selbstständiger Einzelhandel 17,0 18,4 20,0 21,3 22,6 5,8 Regie-Einzelhandel 9,1 8,6 8,4 8,3 8,0 -3,7 Netto Marken-Discount 9,9 10,4 10,7 11,3 11,8 4,5 Backwaren-Einzelhandel 0,6 0,6 0,7 0,7 0,7 -1,2 Lebensmitteleinzelhandel 36,6 38,1 39,8 41,6 43,0 3,4 C+C / Großverbrauchergeschäft 1,7 1,7 1,9 1,9 1,9 0,2 Drittumsätze 1,4 1,5 1,5 1,3 1,3 -1,7 EDEKA-Verbund gesamt 39,7 41,2 43,2 44,8 46,2 3,1 * bereinigt um Umsätze von NETTO Stavenhagen und Kooperationspartnern -

Recipe for Social Security Why a Universal Basic Income Could Be a Model for Germany

Special Topic: Sustainability 01 2017 The research magazine of the University of Freiburg | www.wissen.uni-freiburg.de Recipe for Social Security Why a universal basic income could be a model for Germany Setting the record straight: Shaping the future: Coordinating stimuli: Why a newly discovered virus Why citizens and researchers Why nerve cells have to in bats is not dangerous are brainstorming ideas for communicate closely to for humans > page 8 sustainability in Freiburg > page 20 trigger movement > page 40 01 2017 Bundesweit für Sie da: Mit Direktbank und wachsendem Filialnetz. Contents Research A Model for Human Dignity 4 Karl Justus Bernhard Neumärker’s research suggests that a universal basic income would have a chance in Germany Who’s Afraid of Vampire Flu? 8 1 A newly discovered virus in bats Für mich: das kostenfreie Bezügekonto is not transmittable to humans All at the Same Time 12 1 Voraussetzung: Bezügekonto mit Online-Überweisungen; Genossenschaftsanteil von 15,– Euro/Mitglied. University of Freiburg psychologists are searching Banken gibt es viele. Aber die BBBank ist die einzige bundesweit tätige genossenschaftliche for strategies to facilitate multitasking Privat kundenbank, die Beamten und Arbeit nehmern des öffentlichen Dienstes einzigartige Angebote macht. Zum Beispiel das Bezügekonto mit kostenfreier Kontoführung.1 Special Topic: Sustainability Informieren Sie sich jetzt über die vielen weiteren Vorteile Ihres neuen Kontos unter An Interdisciplinary Thread 16 Tel. 0 800/40 60 40 160 (kostenfrei) oder www.bezuegekonto.de -

Annual Financial Statements and Management Report of DZ BANK AG

2017 Annual Financial Statements and Management Report of DZ BANK AG DZ BANK AG 1 2017 Annual Financial Statements and Management Report Contents Contents 02 Management report of DZ BANK AG 06 DZ BANK AG fundamentals 16 Business report 30 Events after the balance sheet date 32 Human resources report and sustainability 38 Outlook 44 Combined opportunity and risk report 152 Annual financial statements of DZ BANK AG 154 Balance sheet as at December 31, 2017 156 Income statement for the period January 1 to December 31, 2017 158 Notes 212 Responsibility statement 213 Independent auditors’ report (translation) 2 DZ BANK AG 2017 Annual Financial Statements and Management Report Management report of DZ BANK AG Contents Management report of DZ BANK AG 06 DZ BANK AG fundamentals 30 Events after the balance sheet date 06 Business model 32 Human resources report 07 Strategic focus as a network-oriented and sustainability central institution and financial services group 32 Human resources report 07 Cooperative Banks / Verbund 32 HR work in the year of the migration 08 Corporate Banking 32 Professional development 08 Retail Banking 32 Training and development of young talent 09 Capital Markets 33 Health management 09 Transaction Banking 33 Work-life balance 33 TeamUp trainee program 10 Management of DZ BANK 33 ‘Verbund First’ career development program 10 Management units 33 Corporate Campus for Management & Strategy 10 Governance 34 DZ BANK Group’s employer branding campaign 13 Key performance indicators 34 Employer awards 13 Management process 34 -

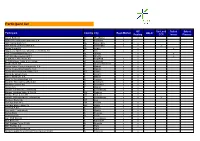

Participant List

Participant list GC SecLend Select Select Participant Country City Repo Market HQLAx Pooling CCP Invest Finance Aareal Bank AG D Wiesbaden x x ABANCA Corporaction Bancaria S.A E Betanzos x ABN AMRO Bank N.V. NL Amsterdam x x ABN AMRO Clearing Bank N.V. NL Amsterdam x x x Airbus Group SE NL Leiden x x Allgemeine Sparkasse Oberösterreich Bank AG A Linz x x ASR Levensverzekering N.V. NL Utrecht x x ASR Schadeverzekering N.V. NL Utrecht x x Augsburger Aktienbank AG D Augsburg x x B. Metzler seel. Sohn & Co. KGaA D Frankfurt x x Baader Bank AG D Unterschleissheim x x Banco Bilbao Vizcaya Argentaria, S.A. E Madrid x x Banco Cooperativo Español, S.A. E Madrid x x Banco de Investimento Global, S.A. PT Lisbon x x Banco de Sabadell S.A. E Alicante x x Banco Santander S.A. E Madrid x x Bank für Sozialwirtschaft AG D Cologne x x Bank für Tirol und Vorarlberg AG A Innsbruck x x Bankhaus Lampe KG D Dusseldorf x x Bankia S.A. E Madrid x x Banque Centrale du Luxembourg L Luxembourg x x Banque Lombard Odier & Cie SA CH Geneva x x Banque Pictet & Cie AG CH Geneva x x Banque Internationale à Luxembourg L Luxembourg x x x Bantleon Bank AG CH Zug x Barclays Bank PLC GB London x x Barclays Bank Ireland Plc IRL Dublin x x BAWAG P.S.K. A Vienna x x Bayerische Landesbank D Munich x x Belfius Bank B Brussels x x Berlin Hyp AG D Berlin x x BGL BNP Paribas L Luxembourg x x BKS Bank AG A Klagenfurt x x BNP Paribas Fortis SA/NV B Brussels x x BNP Paribas S.A. -

Exchange Council Election Eurex Deutschland Preliminary Voter List – As of 16 August 2019

Exchange Council Election Eurex Deutschland Preliminary Voter List – as of 16 August 2019 Voter group 1a cooperative credit institutions Company State DZ BANK AG Deutsche Zentral-Genossenschaftsbank Germany Page - 1 - Exchange Council Election Eurex Deutschland Preliminary Voter List – as of 16 August 2019 Voter group 1b credit institutions under public law Company State Bayerische Landesbank Germany DekaBank Deutsche Girozentrale Germany Hamburger Sparkasse AG Germany Kreissparkasse Köln Germany Landesbank Hessen-Thüringen Girozentrale Germany Landesbank Saar Germany Norddeutsche Landesbank - Girozentrale Germany NRW.BANK Germany Sparkasse Pforzheim Calw Germany Page - 2 - Exchange Council Election Eurex Deutschland Preliminary Voter List – as of 16 August 2019 Voter group 1c other credit institutions Company State ABN AMRO Bank N.V. Netherlands ABN AMRO Clearing Bank N.V. Netherlands B. Metzler seel. Sohn & Co. KGaA Germany Baader Bank Aktiengesellschaft Germany Banca Akros S.p.A. Italy Banca IMI S.p.A Italy Banca Sella Holding S.p.A. Italy Banca Simetica S.p.A. Italy Banco Bilbao Vizcaya Argentaria S.A. Spain Banco Comercial Português S.A. Portugal Banco Santander S.A. Spain Bank J. Safra Sarasin AG Switzerland Bank Julius Bär & Co. AG Switzerland Bank Vontobel AG Switzerland Bankhaus Lampe KG Germany Bankia S.A. Spain Bankinter Spain Banque de Luxembourg Luxemburg Banque Lombard Odier & Cie SA Switzerland Banque Pictet & Cie SA Switzerland Barclays Bank Ireland Plc Ireland Barclays Bank PLC United Kingdom Basler Kantonalbank Switzerland Berner Kantonalbank AG Switzerland Bethmann Bank AG Germany BNP Paribas United Kingdom BNP Paribas (Suisse) SA Switzerland BNP Paribas Fortis SA/NV Belgium BNP Paribas S.A. Niederlassung Deutschland Germany BNP Paribas Securities Services S.C.A. -

Technology Parks

ANNUAL REPORT 2019 L-Bank in Figures OVERVIEW 2015–2019 in EUR millions 2015 2016 2017 2018 2019 Total assets 73,294.92 75,075.39 70,669.98 69,608.87 77,622.56 Equity 2,765.31 2,814.64 2,865.23 2,963.98 3,013.96 Net interest income1 365.41 368.93 323.41 331.37 302.04 Net income 50.63 49.33 50.59 50.18 49.98 2015 2016 2017 2018 2019 ‘Hard’ Tier I capital ratio (CET1 ratio) 16.38% 18.00% 18.67% 18.59% 20.06% Total capital ratio 19.00% 20.29% 20.73% 20.59% 22.20% Return on equity 10.28% 12.19% 5.44% 6.29% 4.39% Cost-income ratio 42.82% 41.65% 52.39% 44.53% 53.45% Leverage ratio 3.91% 4.37% 4.81% 5.12% 4.86% 2019 Moody’s Standard & Poor’s Rating Aaa AAA 1 Based on business operations. Annual Report 2019 L-Bank 03 A Letter to our Business Partners Dear Business Partners, A good result, important strategic decisions for the future… although 2019 was a chal- lenging year for L-Bank, there were many positive outcomes. We were delighted by the European Parliament’s positive decision, taken on 16 April 2019, to take Germany’s legally independent development banks out of the European Single Supervisory M echanism (SSM). This means that development banks now operate in a more appropriate regulatory envir- onment. Among the important factors influencing the political decision-making process, our objection to banking supervision by the ECB undoubtedly played a part. -

Interim Report As at 30 June 2020 Hamburg Commercial Bank

Interim Report as at 30 June 2020 Hamburg Commercial Bank Group overview INCOME STATEMENT (€ million ) BALANCE SHEET (€ billion) Net income before restructuring and Reported equity privatisation January - June 2020 30.06.2020 (cf. January - June 2019: 104) (cf. 31.12.2019: 4.4) ↘ 76 → 4.4 Net income before taxes Total assets 30.06.2020 (cf. January - June 2019: 96) (cf. 31.12.2019: 47.7) ↘ 71 ↘ 41.8 Group net result Business volume 30.06.2020 (cf. January - June 2019: 5) (cf. 31.12.2019: 55.6) ↘ 4 ↘ 48.0 CAPITAL RATIO & RWA (%)1) EMPLOYEES (computed on full-time equivalent basis) CET1 ratio 30.06.2020 (cf. 31.12.2019: 18.5) Total 30.06.2020 (cf. 31.12.2019: 1,482) ↗ 21.7 ↘ 1,215 Total capital ratio 30.06.2020 Germany 30.06.2020 (cf. 31.12.2019: 23.5) (cf. 31.12.2019: 1,421) ↗ 27.0 ↘ 1,180 Risk weighted assets (RWA) 30.06.2020 Abroad 30.06.2020 (€ billion) (cf. 31.12.2019: 21.0) (cf. 31.12.2019: 61) ↘ 19.0 ↘ 35 Due to rounding, numbers presented throughout this report may not add up to the totals disclosed and percentages may not precisely reflect the absolute figures. 1) Not in-period: regulatory disclosure pursuant to the CRR Content Interim Management Interim group financial Report statements 2 Economic report 46 Group statement of income 2 Underlying economic and industry conditions 7 Business development 47 Group statement of comprehensive income 9 Earings, net assets and financial position 17 Segment results 48 Group statement of financial position 19 Employees of Hamburg Commercial Bank 50 Group statement of changes in equity 21 -

Annual Financial Statements and Management Report of DZ BANK AG Key Figures

2016 Annual Financial Statements and Management Report of DZ BANK AG Key figures DZ BANK AG Dec. 31, Dec. 31, € million 2016 2015 2016 2015 FINANCIAL PERFORMANCE LIQUIDITY ADEQUACY Operating profit before allowances Economic liquidity adequacy for losses on loans and advances 827 769 (€ billion)2 3.8 4.0 Allowances for losses on loans and Liquidity coverage ratio – LCR advances -313 123 (percent) 139.9 106.6 Operating profit 514 892 Net income for the year 323 399 CAPITAL ADEQUACY Cost/income ratio (percent) 64.7 63.1 Economic capital adequacy (percent)3 4 163.5 173.5 Dec. 31, Jan. 1, Common equity Tier 1 capital ratio 2016 2016 (percent)5 18.1 19.0 NET ASSETS Common equity Tier 1 capital ratio applying CRR in full (percent)6 18.1 19.0 Assets Tier 1 capital ratio (percent)5 19.1 20.2 Loans and advances to banks 118,095 101,022 Total capital ratio (percent)5 24.4 26.6 Loans and advances to customers 33,744 31,710 Leverage ratio (percent)5 4.0 4.6 Bonds and other fixed-income Leverage ratio applying CRR in full securities 45,591 48,253 (percent)6 4.0 4.6 Shares and other variable-yield securities 68 56 AVERAGE NUMBER OF EMPLOYEES Trading assets 38,187 45,929 DURING THE YEAR 5,673 5,590 Other assets 17,630 17,681 LONG-TERM RATING Equity and liabilities Standard & Poor’s AA- AA- Deposits from banks 120,150 119,986 Moody’s Investors Service Aa3 Aa3 Deposits from customers 27,938 22,720 Fitch Ratings AA- AA- Debt certificates issued including bonds 48,173 45,782 Trading liabilities 31,966 31,889 Other liabilities 14,832 14,131 Equity 10,256 10,143 Total assets/total equity and liabilities 253,315 244,651 Volume of business1 284,037 274,059 1 Total equity and liabilities including contingent liabilities and other obligations.