Behind Headlines

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

CC22 N848AE HP Jetstream 31 American Eagle 89 5 £1 CC203 OK

CC22 N848AE HP Jetstream 31 American Eagle 89 5 £1 CC203 OK-HFM Tupolev Tu-134 CSA -large OK on fin 91 2 £3 CC211 G-31-962 HP Jetstream 31 American eagle 92 2 £1 CC368 N4213X Douglas DC-6 Northern Air Cargo 88 4 £2 CC373 G-BFPV C-47 ex Spanish AF T3-45/744-45 78 1 £4 CC446 G31-862 HP Jetstream 31 American Eagle 89 3 £1 CC487 CS-TKC Boeing 737-300 Air Columbus 93 3 £2 CC489 PT-OKF DHC8/300 TABA 93 2 £2 CC510 G-BLRT Short SD-360 ex Air Business 87 1 £2 CC567 N400RG Boeing 727 89 1 £2 CC573 G31-813 HP Jetstream 31 white 88 1 £1 CC574 N5073L Boeing 727 84 1 £2 CC595 G-BEKG HS 748 87 2 £2 CC603 N727KS Boeing 727 87 1 £2 CC608 N331QQ HP Jetstream 31 white 88 2 £1 CC610 D-BERT DHC8 Contactair c/s 88 5 £1 CC636 C-FBIP HP Jetstream 31 white 88 3 £1 CC650 HZ-DG1 Boeing 727 87 1 £2 CC732 D-CDIC SAAB SF-340 Delta Air 89 1 £2 CC735 C-FAMK HP Jetstream 31 Canadian partner/Air Toronto 89 1 £2 CC738 TC-VAB Boeing 737 Sultan Air 93 1 £2 CC760 G31-841 HP Jetstream 31 American Eagle 89 3 £1 CC762 C-GDBR HP Jetstream 31 Air Toronto 89 3 £1 CC821 G-DVON DH Devon C.2 RAF c/s VP955 89 1 £1 CC824 G-OOOH Boeing 757 Air 2000 89 3 £1 CC826 VT-EPW Boeing 747-300 Air India 89 3 £1 CC834 G-OOOA Boeing 757 Air 2000 89 4 £1 CC876 G-BHHU Short SD-330 89 3 £1 CC901 9H-ABE Boeing 737 Air Malta 88 2 £1 CC911 EC-ECR Boeing 737-300 Air Europa 89 3 £1 CC922 G-BKTN HP Jetstream 31 Euroflite 84 4 £1 CC924 I-ATSA Cessna 650 Aerotaxisud 89 3 £1 CC936 C-GCPG Douglas DC-10 Canadian 87 3 £1 CC940 G-BSMY HP Jetstream 31 Pan Am Express 90 2 £2 CC945 7T-VHG Lockheed C-130H Air Algerie -

![Contents [Edit] Africa](https://docslib.b-cdn.net/cover/9562/contents-edit-africa-79562.webp)

Contents [Edit] Africa

Low cost carriers The following is a list of low cost carriers organized by home country. A low-cost carrier or low-cost airline (also known as a no-frills, discount or budget carrier or airline) is an airline that offers generally low fares in exchange for eliminating many traditional passenger services. See the low cost carrier article for more information. Regional airlines, which may compete with low-cost airlines on some routes are listed at the article 'List of regional airlines.' Contents [hide] y 1 Africa y 2 Americas y 3 Asia y 4 Europe y 5 Middle East y 6 Oceania y 7 Defunct low-cost carriers y 8 See also y 9 References [edit] Africa Egypt South Africa y Air Arabia Egypt y Kulula.com y 1Time Kenya y Mango y Velvet Sky y Fly540 Tunisia Nigeria y Karthago Airlines y Aero Contractors Morocco y Jet4you y Air Arabia Maroc [edit] Americas Mexico y Aviacsa y Interjet y VivaAerobus y Volaris Barbados Peru y REDjet (planned) y Peruvian Airlines Brazil United States y Azul Brazilian Airlines y AirTran Airways Domestic y Gol Airlines Routes, Caribbean Routes and y WebJet Linhas Aéreas Mexico Routes (in process of being acquired by Southwest) Canada y Allegiant Air Domestic Routes and International Charter y CanJet (chartered flights y Frontier Airlines Domestic, only) Mexico, and Central America y WestJet Domestic, United Routes [1] States and Caribbean y JetBlue Airways Domestic, Routes Caribbean, and South America Routes Colombia y Southwest Airlines Domestic Routes y Aires y Spirit Airlines Domestic, y EasyFly Caribbean, Central and -

Solidarite 1991 Livre.Pdf

Du même auteur Histoire du mouvement ouvrier au Québec (1825-1976), 150 ans de luttes, en collaboration, Montréal, coédition CSN CEQ, 1984 (nouvelle édition revue et augmentée). FLQ, Histoire d’un mouvement clandestin, Montréal, Éditions Québec/Amérique, 1982. La police secrète au Québec, en collaboration, Montréal, Éditions Québec/Amérique, 1978. 23 dossiers de Québec-Presse, en collaboration, Montréal, Réédition-Québec, 1971. * La forme masculine généralement utilisée dans ce livre désigne aussi bien les femmes que les hommes. Données de catalogage avant publication (Canada) Fournier, Louis, 1945 Solidarité inc. : un nouveau syndicalisme créateur d’emplois (Collection Succès d’Amérique) ISBN 2-89037-558-7 1. Fédération des travailleurs et travailleuses du Québec — Histoire. 2. Création d’emplois — Québec (Province). 3. Syndicalisme — Aspect social — Québec (Province). I. Titre. II. Collection. HD6529.Q8F68 1991 331.88’09714 C91-096895-0 Tous droits de traduction, de reproduction et d’adaptation réservés ©1991, Éditions Québec/Amérique Dépôt légal: 4e trimestre 1991 Bibliothèque nationale du Québec Bibliothèque nationale du Canada Montage Andréa Joseph Table des matières PROLOGUE Un jour de février 1991.............................................................13 PREMIÈRE PARTIE: LA NAISSANCE Chapitre Premier — En pleine crise ..........................................17 Le Sommet de Québec ............................................................18 Le vieux Lion ..........................................................................21 -

B-201635 Claim for Air Transportation and Warehousing Services

THE CO MPTROLLER GENERAL DECISION .0 -i).) OF T H E U NITED S TATES W A S H I N G T C N. C 2 0 5 4 8 FILE: B-201635 DATE: February 25, 1981 MATTER OF: Nordair Ltd. DIGEST: 1. Claim based on 12 invoices for air transporta- tion and warehousing services provided under Air Force contract may not be considered since services under invoices were performed more than 6 years before claim was received by General Accounting Office. Therefore, 31 U.S.C. § 71a (1976) prevents considera- tion of claim. 2. Claim based on three invoices for similar services is denied since: (1) first invoice evidences claim against private party, not Government; (2) copy of second invoice has not been sub- mitted and record does not show any other documentation to support payment of claimed amount; and (3) third invoice evidences fuel charge which was cost to contractor, not Govern- ment. On November 7, 1979, our Office received a claim for $6,699.22 from Nordair Ltd. for the pay- ment of 15 invoices dating back to 1972 and 1973 /Nit for air transportation and warehousing services) provided to the Air Force. On November 13, 1980, our Claims Group informed Nordair that the claimed payment for 12 of the invoices (X207011, X208020, X209032, N209072, X211024, X301012, X302020, X303006, X304028, X305051, X306022, and X307013) could not be considered since the claim was received by our Office more than 6 years after the invoices' dates (all prior to September 1973), therefore, the claim for -these invoices was considered to be barred by 31 U.S.C. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Report on Transformation: a Leaner NDHQ?

• INDEPENDENT AND INFORMED • AUTONOME ET RENSEIGNÉ ON TRACK The Conference of Defence Associations Institute • L’Institut de la Conférence des Associations de la Défense Autumn 2011 • Volume 16, Number 3 Automne 2011 • Volume 16, Numéro 3 REPORT ON TRANSFORMATION: A leaner NDHQ? Afghanistan: Combat Mission Closure Reflecting on Remembrance ON TRACK VOLUME 16 NUMBER 3: AUTUMN / AUTOMNE 2011 PRESIDENT / PRÉSIDENT Dr. John Scott Cowan, BSc, MSc, PhD VICE PRESIDENT / VICE PRÉSIDENT Général (Ret’d) Raymond Henault, CMM, CD CDA INSTITUTE BOARD OF DIRECTORS LE CONSEIL D’ADMINISTRATION DE L’INSTITUT DE LA CAD EXECUTIVE DIRECTOR / DIRECTEUR EXÉCUTIF Colonel (Ret) Alain M. Pellerin, OMM, CD, MA Admiral (Ret’d) John Anderson SECRETARY-TREASURER / SECRÉTAIRE TRÉSORIER Mr. Thomas d’Aquino Lieutenant-Colonel (Ret’d) Gordon D. Metcalfe, CD Dr. David Bercuson HONOURARY COUNSEL / AVOCAT-CONSEIL HONORAIRE Dr. Douglas Bland Mr. Robert T. Booth, QC, B Eng, LL B Colonel (Ret’d) Brett Boudreau DIRECTOR OF RESEARCH / Dr. Ian Brodie DIRECTEUR DE LA RECHERCHE Mr. Paul Chapin, MA Mr. Thomas S. Caldwell Mr. Mel Cappe PUBLIC AFFAIRS / RELATIONS PUBLIQUES Captain (Ret’d) Peter Forsberg, CD Mr. Jamie Carroll Dr. Jim Carruthers DEFENCE POLICY ANALYSTS / ANALYSTES DES POLITIQUES DE DÉFENSE Mr. Paul H. Chapin Ms. Meghan Spilka O’Keefe, MA Mr. Terry Colfer Mr. Arnav Manchanda, MA M. Jocelyn Coulon Mr. Dave Perry, MA Dr. John Scott Cowan PROJECT OFFICER / AGENT DE PROJET Mr. Dan Donovan Mr. Paul Hillier, MA Lieutenant-général (Ret) Richard Evraire Conference of Defence Associations Institute Honourary Lieutenant-Colonel Justin Fogarty 151 Slater Street, Suite 412A Ottawa ON K1P 5H3 Colonel, The Hon. -

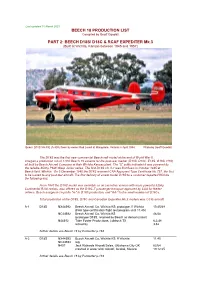

BEECH D18S/ D18C & RCAF EXPEDITER Mk.3 (Built at Wichita, Kansas Between 1945 and 1957)

Last updated 10 March 2021 BEECH 18 PRODUCTION LIST Compiled by Geoff Goodall PART 2: BEECH D18S/ D18C & RCAF EXPEDITER Mk.3 (Built at Wichita, Kansas between 1945 and 1957) Beech D18S VH-FIE (A-808) flown by owner Rod Lovell at Mangalore, Victoria in April 1984. Photo by Geoff Goodall The D18S was the first new commercial Beechcraft model at the end of World War II. It began a production run of 1,800 Beech 18 variants for the post-war market (D18S, D18C, E18S, G18S, H18), all built by Beech Aircraft Company at their Wichita Kansas plant. The “S” suffix indicated it was powered by the reliable 450hp P&W Wasp Junior series. The first D18S c/n A-1 was first flown in October 1945 at Beech field, Wichita. On 5 December 1945 the D18S received CAA Approved Type Certificate No.757, the first to be issued to any post-war aircraft. The first delivery of a new model D18S to a customer departed Wichita the following day. From 1947 the D18C model was available as an executive version with more powerful 525hp Continental R-9A radials, also offered as the D18C-T passenger transport approved by CAA for feeder airlines. Beech assigned c/n prefix "A-" to D18S production, and "AA-" to the small number of D18Cs. Total production of the D18S, D18C and Canadian Expediter Mk.3 models was 1,035 aircraft. A-1 D18S NX44592 Beech Aircraft Co, Wichita KS: prototype, ff Wichita 10.45/48 (FAA type certification flight test program until 11.45) NC44592 Beech Aircraft Co, Wichita KS 46/48 (prototype D18S, retained by Beech as demonstrator) N44592 Tobe Foster Productions, Lubbock TX 6.2.48 retired by 3.52 further details see Beech 18 by Parmerter p.184 A-2 D18S NX44593 Beech Aircraft Co, Wichita KS: ff Wichita 11.45 NC44593 reg. -

The Transition to Safety Management Systems (SMS) in Aviation: Is Canada Deregulating Flight Safety?, 81 J

Journal of Air Law and Commerce Volume 81 | Issue 1 Article 3 2002 The rT ansition to Safety Management Systems (SMS) in Aviation: Is Canada Deregulating Flight Safety? Renè David-Cooper Federal Court of Appeal of Canada Follow this and additional works at: https://scholar.smu.edu/jalc Recommended Citation Renè David-Cooper, The Transition to Safety Management Systems (SMS) in Aviation: Is Canada Deregulating Flight Safety?, 81 J. Air L. & Com. 33 (2002) https://scholar.smu.edu/jalc/vol81/iss1/3 This Article is brought to you for free and open access by the Law Journals at SMU Scholar. It has been accepted for inclusion in Journal of Air Law and Commerce by an authorized administrator of SMU Scholar. For more information, please visit http://digitalrepository.smu.edu. THE TRANSITION TO SAFETY MANAGEMENT SYSTEMS (SMS) IN AVIATION: IS CANADA DEREGULATING FLIGHT SAFETY? RENE´ DAVID-COOPER* ABSTRACT In 2013, the International Civil Aviation Organization (ICAO) adopted Annex 19 to the Chicago Convention to implement Safety Management Systems (SMS) for airlines around the world. While most ICAO Member States worldwide are still in the early stages of introducing SMS, Canada became the first and only ICAO country in 2008 to fully implement SMS for all Canadian-registered airlines. This article will highlight the documented shortcomings of SMS in Canada during the implementation of the first ever SMS framework in civil aviation. While air carriers struggled to un- derstand and introduce SMS into their operations, this article will illustrate how Transport Canada (TC) did not have the knowledge or the necessary resources to properly guide airline operators during this transition, how SMS was improperly tai- lored for smaller air carriers, and how the Canadian govern- ment canceled safety inspections around the country, leaving many air carriers partially unregulated. -

2004 Annual General Meeting

2004 ANNUAL GENERAL MEETING Address by Garth F. Atkinson President and Chief Executive Officer April 21, 2004 Thank you Tom and good morning ladies and gentlemen. At this point, it is my great pleasure to introduce the other members of our senior staff who are here this morning: Mr. Julien DeShutter - Vice President Airport Marketing Mr. Frank Jakowski - Vice President Finance and Chief Financial Officer Mr. Bob Schmitt -Vice President Airport Development Mr. John Terpstra - Senior Director Terminal Operations Mr. Wayne Smook - Senior Director Airside Operations Mrs. Myrna Dube – Senior Director Land & Business Development Mr. Stephan Poirier, Senior Director, Passenger & Air Cargo Development is currently away on business. I would also like to acknowledge all Airport Authority staff members who have taken time out of their day to join us here this morning. This Annual General Meeting is one of our key opportunities to demonstrate accountability to our stakeholders, by reporting on both the results of operations for the past year, as well as the main objectives for 2004. Our responsibility to be accountable is exercised in a number other ways, including the preparation of an annual report which is being released today, annual meetings with the four bodies that appoint members to our Board of Directors, independent reviews every five years, an extensive regulatory environment for airport operations, extensive commitments to Transport Canada under our Canada Lease and a wide range of meetings with airlines, three levels of government and many civic groups throughout the year. 1 We operate both the Calgary International and Springbank Airports. 2003 was an exciting year for these airports and I am pleased to report that the Airport Authority met all key financial and operational objectives. -

363 Part 238—Contracts With

Immigration and Naturalization Service, Justice § 238.3 (2) The country where the alien was mented on Form I±420. The contracts born; with transportation lines referred to in (3) The country where the alien has a section 238(c) of the Act shall be made residence; or by the Commissioner on behalf of the (4) Any country willing to accept the government and shall be documented alien. on Form I±426. The contracts with (c) Contiguous territory and adjacent transportation lines desiring their pas- islands. Any alien ordered excluded who sengers to be preinspected at places boarded an aircraft or vessel in foreign outside the United States shall be contiguous territory or in any adjacent made by the Commissioner on behalf of island shall be deported to such foreign the government and shall be docu- contiguous territory or adjacent island mented on Form I±425; except that con- if the alien is a native, citizen, subject, tracts for irregularly operated charter or national of such foreign contiguous flights may be entered into by the Ex- territory or adjacent island, or if the ecutive Associate Commissioner for alien has a residence in such foreign Operations or an Immigration Officer contiguous territory or adjacent is- designated by the Executive Associate land. Otherwise, the alien shall be de- Commissioner for Operations and hav- ported, in the first instance, to the ing jurisdiction over the location country in which is located the port at where the inspection will take place. which the alien embarked for such for- [57 FR 59907, Dec. 17, 1992] eign contiguous territory or adjacent island. -

Exchange Industrial Income Fund Since Its Units Began Trading on the Toronto Venture Exchange on May 6, 2004

EEXXCCHHAANNGGEE IINNDDUUSSTTRRIIAALL IINNCCOOMMEE FFUUNNDD 2004 Annual Report TABLE OF CONTENTS LETTER FROM THE CHAIRMAN................................................................................................1 CORPORATE PROFILE ..............................................................................................................4 THE FUND’S ACQUISITION STRATEGY ...................................................................................5 PERIMETER AVIATION LTD.......................................................................................................7 KEEWATIN AIR LIMITED ACQUISITION ANNOUNCED APRIL 2005.......................................7 MANAGEMENT’S DISCUSSION AND ANALYSIS .....................................................................8 MANAGEMENT’S RESPONSIBILITY FOR FINANCIAL REPORTING ....................................15 AUDITORS’ REPORT ................................................................................................................16 AUDITED CONSOLIDATED FINANCIAL STATEMENTS.........................................................17 NOTES TO CONSOLIDATED FINANCIAL STATEMENT ........................................................23 UNITHOLDER INFORMATION ..................................................................................................33 LETTER FROM THE CHAIRMAN To Exchange Unitholders: On behalf of the Trustees and management, I am pleased to report on the accomplishments of Exchange Industrial Income Fund since its units began trading on the Toronto -

Revisiting the Relationship Between Competition and Price Discrimination∗

Revisiting the Relationship between Competition and Price Discrimination∗ Ambarish Chandraa;b Mara Ledermana June 7, 2017 a: University of Toronto, Rotman School of Management b: University of Toronto at Scarborough, Department of Management Abstract We revisit the relationship between competition and price discrimination. Theoretically, we show that, if consumers differ in terms of both their un- derlying willingness-to-pay and their brand loyalty, competition may increase price differences between some consumers while decreasing them between oth- ers. Empirically, we find that competition has little impact at the top or the bottom of the price distribution but a significant impact in the middle, thus increasing some price differentials but decreasing others. Our findings highlight the importance of understanding the relevant sources of consumer heterogeneity and can reconcile earlier conflicting findings. 1 Introduction Price discrimination occurs when firms charge different mark-ups to different con- sumers. While intuition might suggest that competition would limit a firm’s ability to price discriminate, it is well established that firms can price discriminate in non- monopoly settings. There is now a large theoretical literature on oligopoly price discrimination (for an extensive review, see Stole, 2007). There is also a growing body of empirical work that investigates how market structure impacts equilibrium outcomes under price discrimination. This empirical literature has developed along several tracks. One track investigates whether competition influences the type of price discrimination strategies firms use; ∗Corresponding author: [email protected]. This research was supported by the Social Sciences and Humanities Research Council. Zhe Yuan provided excellent research assistance. We thank Heski Bar-Isaac, Ken Corts, Joshua Gans, Eugene Orlov, Christian Ruzzier and seminar participants at the Kellogg School of Management, the University of Toronto, the 2015 UBC Summer IO conference and the 2015 IIOC for helpful comments.