Impact on European Aviation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Evolución De Las C Repercusión En El Transporte Ción De Las Compañías

Máster Universitario en Dirección y Planificación del Turismo Trabajo Final de Máster Evolución de las C ompañías de Bajo Coste en España y su repercusión en el transporte aéreo de pasajer os desde el comienzo del s. XXI Análisis empírico de la infl uencia de las CBC en el flujo turístico que generan en la ciudad de Zaragoza y su aeropuerto Autor: Francisco Javier Royo Castaño [email protected] Director: Jorge Infante Díaz Facultad de Empresa y Gestión Pública (Huesca) Universidad de Zaragoza Curso académico 2012-2013 Julio de 2013 Evolución de las CBC en España y su repercusión en el transporte aéreo de pasajeros desde el comienzo del s.XXI A ti, porque, estés donde estés, seguro que estás orgulloso 2 Evolución de las CBC en España y su repercusión en el transporte aéreo de pasajeros desde el comienzo del s.XXI Agradecimientos No sería de recibo empezar un trabajo tan laborioso como éste sin antes acordarme de algunas personas que en mayor o menor medida han contribuido a que culmine mi labor. En primer lugar, me gustaría agradecer a todas aquellas personas- conocidas o desconocidas- que dedicaron unos minutos de su tiempo a leer y rellenar la encuesta sobre la que asienta mi contribución académica al tema propuesto. Del mismo modo, quisiera dar también las gracias a David Ramos, Ana Isabel Escalona, Juan Carlos Trillo, Mario Samaniego y Enrique Morales por haber accedido amablemente a ser entrevistados, queriendo aportar visiones diferentes sobre este proyecto. Por otro lado, quisiera también dar las gracias a David Rodrigo por haberme ayudado con sus habilidades cartográficas, a Luis Casaló y Jorge Matute por sus consejos sobre la realización de los cuestionarios y el manejo de programas estadísticos, así como a mi buen amigo Andranik Ayvazyan por haber compartido conmigo información y conocimientos. -

Airline Routes and Second Home Tourism. the French Market in the Algarve

AIRLINE ROUTES AND SECOND HOME TOURISM. THE FRENCH MARKET IN THE ALGARVE Cláudia Ribeiro Almeida1 ABSTRACT The new routes and services provided by low cost carriers enable the emergence of new tourist destinations in Europe and the development of new market segments that value the cheap and easy air accessibilities. One of the best examples is second home tourism (normally associated with residential tourism) that grew in recent years, mainly in tourism destinations in the south of Europe and Mediterranean. One of them is the Algarve that receive nowadays new second home owners coming from several countries, mainly because of the region’ great weather conditions, security and air accessibilities. France is one of the new second home market in Algarve, mainly because of the new Non-Habitual Residents (NHR) regime, that provides to new residents a very attractive tax benefits for their 10 years living in Portugal, as well as the new routes provided by low cost carriers since 2016 to eleven airports of France. Keywords: Low Cost Carriers, Residential Tourism, Algarve, French Market. JEL Classification: L85, L93, Z32 1. INTRODUCTION In recent years, air transport significantly increased the number of flights, routes, destinations and passengers, heavily contributing to the process of airspace liberalisation. This process led to a shift from a management model with heavy state intervention to a competitive market model, allowing the entry of low cost carriers. These carriers have enabled consumers to enjoy a wider range of supply and low airfares (Costa & Almeida, 2018). In Europe, this process began in 1987 in the United Kingdom and Ireland, and strong growth allowed these carriers to capture quickly a large market share (Costa & Almeida, 2018). -

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

Liste-Exploitants-Aeronefs.Pdf

EN EN EN COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, XXX C(2009) XXX final COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) EN EN COMMISSION REGULATION (EC) No xxx/2009 of on the list of aircraft operators which performed an aviation activity listed in Annex I to Directive 2003/87/EC on or after 1 January 2006 specifying the administering Member State for each aircraft operator (Text with EEA relevance) THE COMMISSION OF THE EUROPEAN COMMUNITIES, Having regard to the Treaty establishing the European Community, Having regard to Directive 2003/87/EC of the European Parliament and of the Council of 13 October 2003 establishing a system for greenhouse gas emission allowance trading within the Community and amending Council Directive 96/61/EC1, and in particular Article 18a(3)(a) thereof, Whereas: (1) Directive 2003/87/EC, as amended by Directive 2008/101/EC2, includes aviation activities within the scheme for greenhouse gas emission allowance trading within the Community (hereinafter the "Community scheme"). (2) In order to reduce the administrative burden on aircraft operators, Directive 2003/87/EC provides for one Member State to be responsible for each aircraft operator. Article 18a(1) and (2) of Directive 2003/87/EC contains the provisions governing the assignment of each aircraft operator to its administering Member State. The list of aircraft operators and their administering Member States (hereinafter "the list") should ensure that each operator knows which Member State it will be regulated by and that Member States are clear on which operators they should regulate. -

G410020002/A N/A Client Ref

Solicitation No. - N° de l'invitation Amd. No. - N° de la modif. Buyer ID - Id de l'acheteur G410020002/A N/A Client Ref. No. - N° de réf. du client File No. - N° du dossier CCC No./N° CCC - FMS No./N° VME G410020002 G410020002 RETURN BIDS TO: Title – Sujet: RETOURNER LES SOUMISSIONS À: PURCHASE OF AIR CARRIER FLIGHT MOVEMENT DATA AND AIR COMPANY PROFILE DATA Bids are to be submitted electronically Solicitation No. – N° de l’invitation Date by e-mail to the following addresses: G410020002 July 8, 2019 Client Reference No. – N° référence du client Attn : [email protected] GETS Reference No. – N° de reference de SEAG Bids will not be accepted by any File No. – N° de dossier CCC No. / N° CCC - FMS No. / N° VME other methods of delivery. G410020002 N/A Time Zone REQUEST FOR PROPOSAL Sollicitation Closes – L’invitation prend fin Fuseau horaire DEMANDE DE PROPOSITION at – à 02 :00 PM Eastern Standard on – le August 19, 2019 Time EST F.O.B. - F.A.B. Proposal To: Plant-Usine: Destination: Other-Autre: Canadian Transportation Agency Address Inquiries to : - Adresser toutes questions à: Email: We hereby offer to sell to Her Majesty the Queen in right [email protected] of Canada, in accordance with the terms and conditions set out herein, referred to herein or attached hereto, the Telephone No. –de téléphone : FAX No. – N° de FAX goods, services, and construction listed herein and on any Destination – of Goods, Services, and Construction: attached sheets at the price(s) set out thereof. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

THE AIRPORT COMMERCIAL SALES BENCHMARKING REPORT (Sample Document)

THE AIRPORT COMMERCIAL SALES BENCHMARKING REPORT (sample document) by 1 TABLE OF CONTENTS Introduction Disclaimer Methodology and Assumptions Summary of Findings : Duty-Free Summary of Findings : Duty-Free and Duty-Paid Summary of Findings : Food & Beverage Summary Tables: Duty-Free Summary Tables: Duty-Free and Duty-Paid Summary Tables: Food & Beverage Airport Profiles : Argentina – Aeropuertos Argentina 2000 Airport Profiles : Australia – Sydney Airport Airport Profiles : Australia – Melbourne Airport Airport Profiles : Australia – Selected Australian Airports Airport Profiles : Austria – Vienna International Airport Airport Profiles : Bahrain – Bahrain International Airport Airport Profiles : Belgium – Brussels Airport Airport Profiles : Bulgaria – Sofia Airport Airport Profiles : Canada – Airports of Canada Airport Profiles : Canada – Ottawa International Airport The Airport Commercial Sales Benchmarking Report 2 TABLE OF CONTENTS Airport Profiles : Canada – Toronto Pearson International Airport Airport Profiles : Chile – Arturo Benitez International Airport Airport Profiles : China – Beijing Capital International Airport Airport Profiles : China – Guangzhou Baiyun International Airport Airport Profiles : China – Shenzhen Bao’an International Airport Airport Profiles : China – Shanghai Airports Airport Profiles : Costa Rica – Airports of Costa Rica Airport Profiles : Croatia – Dubrovnik Airport Airport Profiles : Croatia – Franjo Tuđman Airport Zagreb Airport Profiles : Czech Republic - Václav Havel Airport Prague Airport Profiles -

Portugal Ecovia Littoral of the Algarve

Portugal Ecovia Littoral of the Algarve cycling along the Algarve coast – 7 nights Cycling through 237 km on a 6 day journey, surrounded of a vast diversity of sceneries. The amazing cliffs of Sagres, the sweet surroundings of Vilamoura, the wonders of the Ria Formosa Natural Park, the Islamic culture of Cacela Velha, the fascinating view upon the Algarve coast together with the typical small coastal towns and villages pass on some of the most wonderful experiences you will not want to miss. The 8 days / 7 nights Itinerary has it’s beginning at the historical village of Sagres and ending at the called “Enlightenment City” – Vila Real de Stº António. Cycling to the East side of the Algarve till Lagos you will come across marvelous scenery of the cliffs and Atlantic Ocean. Following the Ecovia trail is highlighted the piscatorial traditions as well as the coastal diversity that characterizes each region. Is to highlight the crossing along the Ria Formosa Natural Park (7 Natural wonders of Portugal) enjoying a magnificent natural environment and diverse types of animals in their natural habitat. The combination of the chosen hotel units ( 4* sport and nature resorts) is an essential complement for the entire experience, bringing out the best of what each region has to offer. Explore the piscatorial traditions Discover incredible sights upon the coast Cross Portuguese traditional villages and towns through the Algarve coastal region Hotel diversity – 4* hotels, sports and nature resort. General Information The ecovia is a great route that runs along the Algarve coastline, allowing you to visit many of the coastal towns and cities in the Algarve and also trace various paths of nature. -

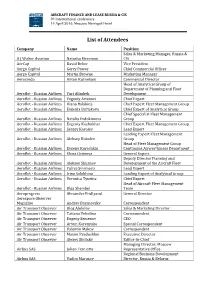

List of Attendees

AIRCRAFT FINANCE AND LEASE RUSSIA & CIS 8th international conference 14 April 2016, Moscow Metropol Hotel List of Attendees Company Name Position Sales & Marketing Manager, Russia & A J Walter Aviation Natasha Meerman CIS AerCap David Beker Vice President Aergo Capital Gerry Power Chief Commercial Officer Aergo Capital Martin Browne Marketing Manager Aerocredo Anton Kuznetsov Commercial Director Head of Analytical Group of Department of Planning and Fleet Aeroflot - Russian Airlines Yuri Alimbek Development Aeroflot - Russian Airlines Evgeniy Artemov Chief Expert Aeroflot - Russian Airlines Diana Balakina Chief Expert Fleet Management Group Aeroflot - Russian Airlines Evgenia Burlakova Chief Expert of Analytical Group Chief Specialist Fleet Management Aeroflot - Russian Airlines Natalia Evdokimova Group Aeroflot - Russian Airlines Evgeniy Kozhukhar Chief Expert Fleet Management Group Aeroflot - Russian Airlines Sergey Korolev Lead Expert Leading Expert Fleet Management Aeroflot - Russian Airlines Aleksey Kukolev Group Head of Fleet Management Group Aeroflot - Russian Airlines Evgeny Kurochkin Continuing Airworthiness Department Aeroflot - Russian Airlines Elena Ozimova General Expert Deputy Director Planning and Aeroflot - Russian Airlines Aleksey Siluanov Development of the Aircraft Fleet Aeroflot - Russian Airlines Yuliya Smirnova Lead Expert Aeroflot - Russian Airlines Irina Solokhina Leading Expert of Analytical Group Aeroflot - Russian Airlines Veronica Tyurina Chief Expert Head of Aircraft Fleet Management Aeroflot - Russian Airlines -

Air Transport in Russia and Its Impact on the Economy

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Tomsk State University Repository Вестник Томского государственного университета. Экономика. 2019. № 48 МИРОВАЯ ЭКОНОМИКА UDC 330.5, 338.4 DOI: 10.17223/19988648/48/20 V.S. Chsherbakov, O.A. Gerasimov AIR TRANSPORT IN RUSSIA AND ITS IMPACT ON THE ECONOMY The study aims to collect and analyse statistics of Russian air transport, show the in- fluence of air transport on the national economy over the period from 2007 to 2016, compare the sector’s role in Russia with the one in other countries. The study reveals the significance of air transport for Russian economy by comparing airlines’ and air- ports’ monetary output to the gross domestic product. On the basis of the research, the policies in the aviation sector can be adjusted by government authorities. Ключевые слова: Russia, aviation, GDP, economic impact, air transport, statistics. Introduction According to Air Transport Action Group, the air transport industry supports 62.7 million jobs globally and aviation’s total global economic impact is $2.7 trillion (approximately 3.5% of the Gross World Product) [1]. Aviation transported 4 billion passengers in 2017, which is more than a half of world population, according to the International Civil Aviation Organization [2]. It makes the industry one of the most important ones in the world. It has a consid- erable effect on national economies by providing a huge number of employment opportunities both directly and indirectly in such spheres as tourism, retail, manufacturing, agriculture, and so on. Air transport is a driving force behind economic connection between different regions because it may entail economic, political, and social effects. -

Time Departure FLIGHTS from SABİHA GÖKÇEN AIRPORT

Wings of Change Europe Master of Ceremony Montserrat Barriga Director General European Regions Airline Association (ERA) Wings of Change Europe – 13/14 November 2018 – Madrid , Spain Wifi Hilton Honors Password APMAD08 Wings of Change Europe – 13/14 November 2018 – Madrid , Spain Welcome remarks Luis Gallego CEO Iberia Wings of Change Europe – 13/14 November 2018 – Madrid , Spain Welcome to Madrid Iberia in figures Flying since Member of Three Business: Airline Maintenance 1927 3 Handing Employees Incomes 2017 €376 Operating profits 2017 17.500 €4.85 Billion (+39% vs 2016) What does Iberia bring to Madrid? 17,500 109 23,000,000 142 employees International aircraft destinations passengers 50% 5,5% 50,000 GDP Indirect Madrid Airport employees Our strategic roadmap The 2013 2014 2017 2012 future Transformation Plan de Futuro Plan de Futuro Struggling Transforming Plan Phase 2 for survival to reach excellence On the verge of Loses cut by half Back to profitability The most punctual airline bankruptcy in the world Four star Skytrax Highest operational profits in Iberia’s 90 years of history 2018 had significant challenges for IB. How are we doing? Financial People Results Customer Muchas gracias The Value of Aviation & importance of Competitiveness for Spain Jose Luis Ábalos Minister of Public Works Government of Spain Wings of Change Europe – 13/14 November 2018 – Madrid , Spain The European Commission’s perspective on the future of aviation in the EU and its neighboring countries Henrik Hololei Director General for Mobility & Transport European -

Seasonal Schedule of the International Airport Borispol, Winter 2019-2020

BORYSPIL INTERNATIONAL AIRPORT SEASON TIMETABLE WINTER 2019-2020 Notes: The timetable is for information only and may not contain the most up-to-date information. For the most up-to-date information, please visit online timetable at https://kbp.aero. Thetimetable contains information on scheduled passenger flights. The arrival/departure time is local (UTC +2h) Numbers in «Days of Operation» column correspond to the day of week (1 – Monday, … 7 – Sunday), 0 – no flights in this day of the week. Airport Flight Departure Days of Date of Date of Destination City Airlines Terminal Code Number Time Operation Ops Start Ops End DEPARTURES Alicante ALC SkyUP Airlines PQ 731 12:00 0200000 24.12.2019 24.03.2020 F Alicante ALC SkyUP Airlines PQ 731 12:00 0004000 31.10.2019 26.03.2020 F Alicante ALC SkyUP Airlines PQ 731 12:00 0000007 10.11.2019 22.03.2020 F Almaty ALA Air Astana KC 406 09:40 1000000 28.10.2019 23.03.2020 D Almaty ALA Air Astana KC 406 09:40 0000500 01.11.2019 27.03.2020 D Almaty ALA Air Astana KC 402 20:40 0200000 29.10.2019 24.12.2019 D Almaty ALA Air Astana KC 402 20:40 0200000 07.01.2020 24.03.2020 D Almaty ALA Air Astana KC 402 20:40 0030000 30.10.2019 25.03.2020 D Almaty ALA Air Astana KC 402 20:40 0000007 27.10.2019 22.03.2020 D Almaty ALA Air Astana KC 402 21:15 0004060 31.10.2019 28.03.2020 D Amman AMM Bravo Airways BAY 781 11:15 0000060 23.11.2019 28.03.2020 F Amsterdam AMS Ukraine International Airlines PS 101 10:00 1234567 27.10.2019 28.03.2020 D Amsterdam AMS KLM KL 1386 13:55 1234567 28.10.2019 28.03.2020 D Ankara ESB