Download the Full Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

I U R E P Orientation Phase R E P O R T G H a 1\F A

International Atomic Energy Agency DRAFT I U R E P ORIENTATION PHASE REPORT G H A 1\F A MR. JEW-PAUL GUELPA MR. WOLFRAM TO GEL December 1982 DISCLAIMER Portions of this document may be illegible in electronic image products. Images are produced from the best available original document UTTEENATIOITAL URANIBK RESOURCES. EVALUATION PROJECT -IURBP- IUSSP ORIENTATION FHAS3 MISSION REPORT BSPTOLIC OP GHANA Dr. J.Fo Guelpa December, 1982. Dro "W. Vogel PREFACE mission, was undertaken, by two consultants, Dr. JoP. Guelpa and Dr. W, Vogel, both, commenced the investigations in Ghana on 5th November, 1982 and completed their work on 16th December, 1982. A total of three days was spent in the field by the consultants* 1. Terse of Ilsferenie .. ., 5 2. General Geography .. .. 4 3. Clirate .. ... 7 4. Population aril I-lain Cities .. .. 9 5. Administrative Regions .. .. S- 6. Official Language, Public Holidays and System of Eeasureaervfc .. ., ll 7. Transport and Consronicatipn .. .. 11 8. Available "aps and Air Photographs .. 12 c. ITCK UB^ITK ICIITIKG n; GH^A • .. .. 13 1. Overview .. .. 13 2. Dianond .. ,. 15 3. Gold .. .. 17 . • 4. Batfzite .. • .. 'IS 5. Manganese .. .. 18 D. IBGI3LATICH ON UEAiTITJK EXPLCHASCtf AlTD XIIIDTG 19 3. KATIOKAL CAFACITI PCS URAFIUI! SXPLORATIC1T AIT3 D272L0P- 1. Ghana Atoiaic Energy CoEE&ssion .. 20 2. Ghana Geological Survey .. .. 22 3. Universities .. .. 24 F. GnOL'OGIC/i 3ST.12r.7 . .. 25 1. Introduction .. ' .. 25 2. The 'vest African Shield Area .. .. 27 2.1 Birician Systec .. .. 27 2.2 Eburnean Granites .. .. 32 2.3 Taria-;aian System .. .. 35 3. Sie Kobile Belt ... .. 3S 3.1 Dahoneyan System •• •• 35 3.2 ?cgc Series •• •• 4C 3 .3 Buen. -

Political Economic Origins of Sekondi‑Takoradi, West Africa's New Oil City

121 UDC: 711.4:711.75+711.453.4(667) DOI: 10.5379/urbani-izziv-en-2012-23-02-005 Franklin OBENG-ODOOM Political economic origins of Sekondi‑Takoradi, West Africa’s new oil city The origins, growth and trajectory of Sekondi‑Takoradi, ure in national and international circles has a historical West Africa’s newest oil city, are considered by using an parallel in the 1920s when, as now, it captured national, “institutional‑analytical” method of economic history. regional and international attention. The evidence sug‑ Particular attention is given to the role of ports, harbours gests that contemporary narratives that strike a determin‑ and railways, and how they evolved and interacted with ist relationship between resource boom and social doom political economic institutions in the last 100 years. This need to be reconsidered. omnibus historical analysis suggests that West Africa’s newest oil city has come full circle. Its contemporary stat‑ Key words: ports, railways, oil, Ghana, Africa Urbani izziv, volume 23, no. 2, 2012 uiiziv-23-2_01.indd 121 26.11.2012 20:26:20 122 F. OBENG-ODOOM 1 Introduction city began its life, grew and rose to fame through economic and political successes. Studies of the city that look at oil (see, e.g., Boohene & Peprah, 2011; Yalley & Ofori‑Darko, 2012; Sekondi‑Takoradi is West Africa’s newest oil city. It is a twin Obeng‑Odoom, 2012a, 2012b) have not been historical. Thus, city in Ghana. Black gold was discovered off its shores in 2007. this paper takes a step in that direction. It looks at the role of By 2010, oil in commercial quantities was flowing in the city political and economic institutions in the origins and trajec‑ and, since 2011, oil has been leaving its shores in pursuit of in‑ tory of Sekondi‑Takoradi in the last 100 years, and it examines ternational currency. -

Ssnit Investments Series

SSNIT INVESTMENTS SERIES SECOND EDITION INTRODUCTION This edition of the SSNIT Investments Series focuses on the Listed Equities Portfolio, one of the three sub-asset classes of the Equities Portfolio. Listed equity refers to ownership interests in companies whose shares are traded publicly on a Stock Market. The Trust currently has share interests in 23 out of the 37 companies listed on the Ghana Stock Exchange (GSE), with a total value of GH¢1.8 billion as at June 2017. A portion of the Trust’s shares in Tullow Oil Plc is also listed on the London Stock Exchange (LSE). The composition of the Trust’s Listed Equities Portfolio, also referred to as the SSNIT Stock Market Portfolio (SSMP), is shown in Table 1. Table 1: SSNIT Listed Equity Holdings # Company Ticker Shareholding (%) 1 Anglogold Ashanti Ltd. AGA 0.02% 2 Aluworks Limited ALW 62.62% 3 Ayrton Drug Man. Ltd. AYRTN 18.00% 4 Benso Oil Palm Plantation BOPP 4.31% 5 CAL Bank Limited CAL 33.18% 6 Cocoa Processing Co. Ltd. CPC 10.14% 7 Ecobank Ghana Ltd. EGH 16.21% 8 Enterprise Group Ltd EGL 6.22% 9 Ecobank Transnational Inc. ETI 3.86% 10 Fan Milk Limited FML 1.59% 11 GCB Bank GCB 29.89% 12 Guinness Gh. Breweries Ltd. GGBL 7.57% 13 Ghana Oil Co. Ltd. GOIL 25.00% 14 Golden Web Ltd. GWEB 20.78% 15 HFC Bank Ltd. HFC 26.09% 16 Produce Buying Co. Ltd. PBC 38.10% 17 Standard Chartered Bank SCB 14.55% 18 SIC Insurance Ltd. -

Has Gse Played Its Role in the Economic Development of Ghana?

CAPITAL MARKET 23 YEARS AND COUNTING: HAS GSE PLAYED ITS ROLE IN THE ECONOMIC DEVELOPMENT OF GHANA? 1st CAPITAL MARKET CONFERENCE BY EKOW AFEDZIE, DEPUTY MANAGING DIRECTOR MAY 10, 2013 INTRODUCTION Ghana Stock Exchange (GSE) was established with a Vision: -To be a relevant, significant, effective and efficient instrument in mobilizing and allocating long-term capital for Ghana’s economic development and growth. INTRODUCTION OBJECTIVES - To facilitate the Mobilization of long term capital by Corporate Bodies/Business and Government through the issuance of securities (shares, bonds, etc). - To provide a Platform for the trading of issued securities. MEMBERSHIP OF GHANA STOCK EXCHANGE GSE as a public company limited by Guarantee has No OWNERS OR SHAREHOLDERS. GSE has Members who are either corporate or individuals. There are two categories of members:- - Licensed Dealing Members - 20 - Associate Members - 34 HISTORICAL BACKGROUND 1968 - Pearl report by Commonwealth Development Finance Co. Ltd. recommended the establishment of a Stock Exchange in Ghana within two years and suggested ways of achieving it. 1970 – 1989 - Various committees established by different governments to explore ways of bringing into being a Stock Exchange in the country. HISTORICAL BACKGROUND 1971 - The Stock Exchange Act was enacted. - The Accra Stock Exchange Company incorporated but never operated. Feb, 1989 - PNDC government set up a 10-member National Committee on the establishment of Stock Exchange under the chairmanship of Dr. G.K. Agama, the then Governor of the Bank of Ghana. HISTORICAL BACKGROUND July, 1989 - Ghana Stock Exchange was incorporated as a private company limited by guarantee under the Companies Code, 1963. HISTORICAL BACKGROUND Nov. -

Fueling the Future of an Oil City a Tale of Sekondi-Takoradi in Ghana

Fueling the Future of an Oil City A Tale of Sekondi-Takoradi in Ghana CONTRIBUTORS FROM GLOBAL COMMUNITIES: Africa in the 21st Century – Rapid Economic Alberto Wilde and Urban Growth Ghana Country Director Africa is experiencing an economic boom period, with many of the fastest growing world economies Ishmael Adams of the last decade in the continent. Ghana is one of the fastest growing economies within Africa, with IncluCity Project Director multiple years of growth in GDP around 7 percent,1 driven by exports of gold and cocoa and, with oil Brian English production that commenced in 2010, further growth is expected. Director, Program Innovation Simultaneously, the continent is transforming due to the effects of rapid urbanization. Africa is the fastest urbanizing continent with urban growth rate of 3.5 percent per year, with that rate expected to hold until 2050.2 Ghana’s rate of urbanization is currently measured at 3.4 percent3 and the country has reached the milestone of 51 percent of its 24 million people living in cities. Urbanization and economic growth spur opportunity but also present challenges such as growth of slums to accommodate the influx of people seeking better jobs and lives in the cities. In turn this can lead to poor quality services and inequalities exacerbated by crime and conflict. Over the last few decades we have also seen an increase in urban disasters. Poor, cramped living conditions, such as those we saw in Port-au-Prince, Haiti, in 2010, can lead to even deadlier and more destructive disasters.4 The world is changing how it views Africa, from seeing the continent through the lens of vulnerability to seeing it through the lens of opportunity. -

Oil City? the Role of Sekondi – Takoradi in Ghana's Emerging Oil Industry

Francisca Amonua Quayson Francisca Amonua Quayson Francisca Oil City? The Role of Sekondi – Takoradi in Ghana’s Emerging Oil Industry Master’s thesis Master’s Oil City? The Role of Sekondi - Takoradi in Ghana’s Emerging Oil Industry Emerging in Ghana’s - Takoradi of Sekondi Oil City? The Role NTNU Science and Technology Science Norwegian University of University Norwegian Faculty of Social Sciences of Social Sciences Faculty Department of Geography Department of Geography and Technology Management Management and Technology Map from: http://crossedcrocodiles.wordpress.com/2009/07/16/ghanas-jubilee-oil-field/jubileefieldmap/ Master Thesis for the Award of Master of Philosophy (MPhil) in Development Studies, Specializing in Geography Trondheim, Spring 2012 Oil City? The Role of Sekondi - Takoradi in Ghana’s Emerging Oil Industry Francisca Amonua Quayson Master Thesis for the Award of Master of Philosophy (MPhil) in Development Studies, Specializing in Geography Department of Geography Norwegian University of Science and Technology Trondheim, June 2012 I II DECLARATION I Francisca Amonua Quayson hereby declare that in exception of references used, which were duly cited and acknowledged, this dissertation is an outcome of a research conducted under the supervision of Professor Stig Jorgensen of the Department of Geography in the Norwegian University of Science and Technology, Trondheim, Norway. ……………………………………………………….. Francisca Amonua Quayson June, 2012 Trondheim, Norway III DEDICATION I dedicate this work to my maker and to my family who have been very supportive of me. To my parents, thank you for being there for me. To my brothers Oppong, Ekow and Ebo, I love you all. I also dedicate this thesis to the memory of my late grandpa who passed on while I was writing this thesis. -

Imperial Travelers: the Formation of West African Urban Culture, Identity, and Citizenship in London and Accra, 1925-1935

Imperial Travelers: The Formation of West African Urban Culture, Identity, and Citizenship in London and Accra, 1925-1935 by Jinny Kathleen Prais A dissertation submitted in partial fulfillment Of the requirements for the degree of Doctor of Philosophy (History and Women‘s Studies) in the University of Michigan 2008 Doctoral Committee: Professor Mamadou Diouf, Co-Chair Professor Carroll Smith-Rosenberg, Co-Chair Associate Professor Michele Mitchell Reader in English, Stephanie M. Newell, University of Sussex © Jinny Kathleen Prais 2008 Dedication For Carroll Smith-Rosenberg Whose example it is my greatest ambition to emulate ii Acknowledgements This dissertation is the product of many institutions and people. First, I would like to acknowledge the West African students who set up clubs and newspapers in London and Accra, sent copies of their journals to the British Museum, and made their way into public archives and records. They have left behind a rich and endlessly stimulating set of documents. I am grateful to a number of schools, programs and departments at the University of Michigan for providing funding for this project: the Rackham Graduate School, the Program in Women‘s Studies, the Department of History, the Center for African and AfroAmerican Studies, the Gayle Morris Sweetland Writing Center, the Seminar on Global and Ethnic Literatures, and the Institute for Research on Women and Gender. I especially acknowledge the generous support of the Center for the Education of Women. The staff and faculty of the Sweetland Writing Center have provided invaluable feedback on this project. I am particularly grateful to Charlotte Boulay for guiding me as I worked through each chapter, and for her editorial assistance. -

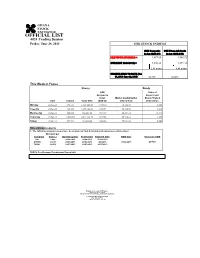

OFFICIAL LIST 4024 Trading Session Friday, June 28, 2013 GSE STOCK INDICES

OFFICIAL LIST 4024 Trading Session Friday, June 28, 2013 GSE STOCK INDICES GSE Composite GSE Financial Stocks Index (GSE-CI) Index (GSE-FSI) PREVIOUS 27/06/2013) = 1,877.65 1,585.72 CURRENT 28/06/2013) = 1,880.26 1,591.18 2.61 points 5.46 points CHANGE-YEAR TO DATE (Jan 01, 2013- June 28, 2013) 56.72% 53.02% This Week in Focus Shares Bonds GSE Value of Composite Government Index Market Capitalization Bonds Traded Date Volume Value GH¢ (GSE-CI) GH¢ million GH¢ million Monday 24-Jun-13 493,511 1,581,041.68 1,900.10 56,154.80 0.000 Tuesday 25-Jun-13 426,550 1,196,438.69 1,891.94 56,110.32 1.240 Wednesday 26-Jun-13 880,088 966,256.30 1,874.67 55,894.32 15.743 Thursday 27-Jun-13 1,553,869 2,844,118.70 1,877.65 55,910.61 4.295 Friday 28-Jun-13 251,546 482,820.80 1,880.26 55,924.82 0.000 Notes/Announcements 1. The following announcements have been made on final dividends and annual general meetings: Dividend per Company Share ¢ Qualifying Date Ex-Div Date Payment Date AGM Date Venue for AGM CAL 0.006 26/06/2013 24/06/2013 30/08/2013 AYRTN 0.0013 25/06/2013 21/06/2013 8/8/2013 27/06/2013 OEPCH TOTAL 0.6900 18/07/2013 16/07/2013 26/07/2013 GCPS:GhanaAICC: Accra International College of Physicians Conference and Centre Surgeons OEPCH:Osu Ebenezer Presbyterian Church HalL Enquiries to: General Manager Ghana Stock Exchange 5th & 6th Floors Cedi House, Liberia Road, Accra Tel: 021 669908, 669914, 669935 Fax: 021 669913 e-mail: [email protected] OFFICIAL LIST 4024 Trading Session ODD LOT Friday, June 28, 2013 ISIN Share Code Total Shares No. -

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 8th January, 2015 STOCK MARKET ACCRA BOURSE MAKES PROMISING START INDICATORS WEEK OPEN WEEK END CHANGE The year 2014 has begun living up to expectations as bullish runs in equities from the petroleum, finance and consumer Market Capitalization (GH¢ goods sectors saw the annual returns of the broader market 'million) 64,352.42 64,229.12 -0.19% Market Capitalization (US$' inch up to 0.42% last Thursday. Though, most equities gave million) 20,109.50 20,014.06 -0.47% up their opening prices, rise in the market value of Ghana Oil Petroleum Company Limited (GOIL), Societe Generale Ghana Volume traded (shares) 783,118.00 573,274.00 -26.80% Table 1: Market Summary Limited (GOIL) and Fan Milk Limited (FML) were enough to close the week’s activities on a positive note. Key benchmark indices closed the week better despite slight volatilities during inter-day trading. The GSE Composite INDEX ANALYSIS index closed at a year-to-date return of 0.42% whiles the GSE Financial Stocks Index settled at 0.67% returns. INDICATORS Closing Week YTD Level Change CHANGE Total market capitalization of the Ghana Stock Exchange was GH¢64.23 billion, an equivalent to USD20.00 billion. GSE Composite Index 2,270.57 0.42% 0.42% GSE Financial Stocks Index 2,258.77 0.67% 0.67% Table 2: Key Stock Market Indices LIQUIDITY The absence of block trades over the period saw liquidity comparatively down last week. All in all, an approximate figure of 573,274 shares exchanged hands within the first trading week of the year, and was also valued about GH¢2.48 million. -

(A CASE STUDY of GHANA STOCK EXCHANGE) By

KWAME NKRUMAH UNIVERSITY OF SCIENCE AND TECHNOLOGY, KUMASI OPTIMAL PORTFOLIO SELECTION (A CASE STUDY OF GHANA STOCK EXCHANGE) By HERMAN YIRBECHAA TAGYANG (B. A. ECONOMICS AND MATHEMATICS) A THESIS SUBMITTED TO THE DEPARTMENT OF MATHEMATICS, KWAME NKRUMAH UNIVERSITY OF SCIENCE AND TECHNOLOGY IN PARTIAL FUFILLMENT OF THE REQUIREMENT FOR THE DEGREE OF MSc. INDUSTRIAL MATHEMATICS MAY, 2014 DECLARATION I hereby declare that this submission is my own work towards the award of the MSc. degree and that, to the best of my knowledge, it contains no material previously published by another person nor material which had been accepted for the award of any other degree of the university, except where due acknowledgement had been made in the text. Tagyang Yirbechaa Herman ....................................... Student Signature Date Certified by: Mr. Kwaku Darkwa ....................................... Supervisor Signature Date Certified by: Prof. S. K. Amponsah ....................................... Head of Department Signature Date i DEDICATION I wish to dedicate this work to the Glory of God Almighty who has been our help in ages past, our fortress now and is still our hope for many years to come. Also to my lovely wife, Irene Kumah and my parents, Mr and Mrs Tagyang. ii Abstract The knapsack model is employed in many fields of study including Business, Engineering and Economics to solve problems related to resource constraints. The knapsack problem is a form of integer programming problem that has only one constraint and can be used to strengthen cutting planes for general integer programs. These facts make the studies of the knapsack problems and their variants extremely important area of research in the field of operations research. -

History of Ghana Advisory Board

THE HISTORY OF GHANA ADVISORY BOARD John T. Alexander Professor of History and Russian and European Studies, University of Kansas Robert A. Divine George W. Littlefield Professor in American History Emeritus, University of Texas at Austin John V. Lombardi Professor of History, University of Florida THE HISTORY OF GHANA Roger S. Gocking The Greenwood Histories of the Modern Nations Frank W. Thackeray and John E. Findiing, Series Editors Greenwood Press Westport, Connecticut • London Library of Congress Cataloging-in-Publication Data Cocking, Roger. The history of Ghana / Roger S. Gocking. p. cm. — (The Greenwood histories of the modern nations, ISSN 1096-2905) Includes bibliographical references (p. ) and index. ISBN 0-313-31894-8 (alk. paper) 1. Ghana—History. I. Title. II. Series. DT510.5.G63 2005 966.7—dc22 2004028236 British Library Cataloguing in Publication Data is available. Copyright © 2005 by Roger S. Gocking All rights reserved. No portion of this book may be reproduced, by any process or technique, without the express written consent of the publisher. Library of Congress Catalog Card Number: 2004028236 ISBN: 0-313-31894-8 ISSN: 1096-2905 First published in 2005 Greenwood Press, 88 Post Road West, Westport, CT 06881 An imprint of Greenwood Publishing Group, Inc. www.greenwood.com Printed in the United States of America The paper used in this book complies with the Permanent Paper Standard issued by the National Information Standards Organization (Z39.48-1984). 10 987654321 Contents Series Foreword vii Frank W. Thackeray and John -

Weekly Markets Update Wilfred Agyei Kofi B

Analysts: Weekly Markets Update Wilfred Agyei Kofi B. Kyei Yaw Saifah For the week ending January 13,2017 Tel: +233(0)302 251137 Email: [email protected] Equities Market Performance Indicators Ga ine rs Stock Market Data: Januray 13, 2017 Indic a tor This We e k Previous Week Cha nge Y TD Tic ke r Price (GHS) Cha nge Div GSE Composite Index (GSE- CI) 1,735.67 1,699.42 36.25 2.76% ETI 0.13 30.00% Price Close 52 Week Market Cap P/E Yield P/B GSE Financial Stock Index (GSE- FSI) 1,613.19 1,564.82 48.37 4.39% EGH 6.85 5.40% Industry/EquitiesTicker GHS USD High Low Volume Traded Value Traded Ratio (%) Ratio GHS MN USD MN Market Cap (GHS MN) 53,588.83 52,756.81 832.02 GCB 3.67 1.10% AGRO PROCESSING 4.22 4.22 Value Traded (GHS MN) 1.63 4.34 - 2.71 TOTAL 2.04 1.00% Volume Traded (MN) 10.76 13.15 - 2.40 BensoBOPP Oil Palm2.40 Plantation0.57 3.13 2.08 29 60 9.49 2.94 1.21 83.52 19.77 Lose rs CocoaCPC Processing0.02 Company0.00 0.02 0.01 0 0 n.m. n.m. 3.96 22.02 5.21 Equities Market Commentary & News Tic ke r Price (GHS) Cha nge GoldenGWEB Web0.01 Ltd 0.00 0.01 0.01 0 0 n.m. n.m. -0.13 0.35 0.08 Investor sentiments swayed in the positive direction during the week in focus as the search for positions in blue CAL 0.76 - 1.30% chip stocks resulted in the values of Ecobank Transnational Incorporated, Ecobank Ghana, GCB Bank and BANKING Total Petroleum closing on the north side of the bourse.