(A CASE STUDY of GHANA STOCK EXCHANGE) By

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 20th October, 2016 STOCK MARKET ACCRA BOURSE SWINGS BACK Increased bearish sentiment saw major performance INDICATORS WEEK OPEN WEEK END CHANGE indicators on the Ghana Stock Exchange (GSE) swung back last week, following a drop in the shares of blue-chip stocks. Market Capitalization (GH¢'million) 52,780.97 52,542.24 -0.45% Key among these stocks include the shares of Standard Market Capitalization Chartered Bank Limited (SCB, Total Petroleum Ghana Limited (US$'million) 13,299.81 13,254.52 -0.34% (TOTAL), Guinness Ghana Breweries Limited (GGBL) and Volume traded (shares) 348,651.00 1,445,517.00 314.60% GCB Bank Limited (GCB). Value Traded (GH¢) 454,858.25 371,669.73 -18.29% In the end, the yield on the GSE-Composite Index, the GSE Value Traded (US$) 114,615.73 93,758.92 -18.20% Financial Stocks Index (GSE-FSI) and the SIC-FSL Top 15 Table 1: Market Summary liquid Index (T-15 Index) slipped from their previous week losses of 11.25%, 13.08% and 20.52% each to settle at INDEX ANALYSIS 11.98%, 13.79% and 22.18% respectively. INDICATORS Closing Week YTD Level Change CHANGE Total market capitalization of the GSE also dropped from the previous week’s figure of GH¢52.78 billion to GH¢52.54 GSE Composite Index 1,755.90 -0.83% -11.98% billion, whilst an equivalent dollar value also dipped from the previous week’s USD 13.30 billion to USD13.25 billion SIC-FSL Top 15 Index 2,887.49 -2.09% -22.18% last Thursday. -

Market Report

Market Report December 2017-Full Year MARKET HIGHLIGHTS GSE STOCK INDICES/CAPITALIZATION DEC 2017 YTD CHANGE DEC 2016 YTD CHANGE GSE COMPOSITE INDEX (GSE-CI) 2,579.72 52.73% 1,689.09 -15.33% GSE FINANCIAL STOCK INDEX (GSE-FSI) 2,310.58 49.51% 1,545.41 -19.93% MARKET CAPITALIZATION (GH¢ M) 58,803.96 11.48% 52,690.99 -7.75% DOMESTIC CAPITALIZATION (GH¢ M) 16,244.34 45.23% 10,877.03 -2.75% MARKET TURNOVER - EQUITIES DEC 2017 DEC 2016 VOLUME TRADED 7,013,135 129,056,489 VALUE TRADED (GH¢) 15,250,389.24 8,829,193.14 NUMBER OF TRANSACTIONS 1,002 1,300 TRADING DAYS 18 19 NUMBER OF TRADED SYMBOLS 26 27 MARKET DAILY AVERAGES - EQUITIES DEC 2017 DEC 2016 AVERAGE VOLUME TRADED 389,619 6,792,447 AVERAGE VALUE TRADED (GH¢) 847,243.85 464,694.38 AVERAGE NUMBER OF TRANSACTIONS 56 68 MARKET TURNOVER - EQUITIES JAN TO DEC 2017 JAN TO DEC 2016 VOLUME TRADED 322,725,768 252,833,427 VALUE TRADED (GH¢) 518,381,473.32 242,114,791.53 NUMBER OF TRANSACTIONS 20,755 20,685 TRADING DAYS 247 249 NUMBER OF TRADED SYMBOLS 40 45 MARKET TURNOVER - FIXED INCOME (DEBT) SECURITIES IN GH¢ MILLIONS DEC 2017 DEC 2016 CORPORATE (GH¢ M) - GOG NOTES AND BONDS (GH¢ M) 3,529.73 - MARKET TURNOVER - FIXED INCOME (DEBT) SECURITIES IN GH¢ MILLIONS JAN-DEC 2017 JAN-DEC 2016 CORPORATE (GH¢ M) 990.16 2.84 GOG NOTES AND BONDS (GH¢ M) 27,723.53 12,510.74 LISTINGS DEC 2017 DEC 2016 LISTED COMPANIES (MAIN MARKET AND GAX) 40 41 LISTED EQUITIES (MAIN MARKET) ORDINARY SHARES 36 37 DEPOSITORY SHARES 1 1 PREFERENCE SHARES 1 1 EXCHANGE TRADED FUNDS 1 1 EQUITIES ON GHANA ALTERNATIVE MARKET (GAX) -

Ssnit Investments Series

SSNIT INVESTMENTS SERIES SECOND EDITION INTRODUCTION This edition of the SSNIT Investments Series focuses on the Listed Equities Portfolio, one of the three sub-asset classes of the Equities Portfolio. Listed equity refers to ownership interests in companies whose shares are traded publicly on a Stock Market. The Trust currently has share interests in 23 out of the 37 companies listed on the Ghana Stock Exchange (GSE), with a total value of GH¢1.8 billion as at June 2017. A portion of the Trust’s shares in Tullow Oil Plc is also listed on the London Stock Exchange (LSE). The composition of the Trust’s Listed Equities Portfolio, also referred to as the SSNIT Stock Market Portfolio (SSMP), is shown in Table 1. Table 1: SSNIT Listed Equity Holdings # Company Ticker Shareholding (%) 1 Anglogold Ashanti Ltd. AGA 0.02% 2 Aluworks Limited ALW 62.62% 3 Ayrton Drug Man. Ltd. AYRTN 18.00% 4 Benso Oil Palm Plantation BOPP 4.31% 5 CAL Bank Limited CAL 33.18% 6 Cocoa Processing Co. Ltd. CPC 10.14% 7 Ecobank Ghana Ltd. EGH 16.21% 8 Enterprise Group Ltd EGL 6.22% 9 Ecobank Transnational Inc. ETI 3.86% 10 Fan Milk Limited FML 1.59% 11 GCB Bank GCB 29.89% 12 Guinness Gh. Breweries Ltd. GGBL 7.57% 13 Ghana Oil Co. Ltd. GOIL 25.00% 14 Golden Web Ltd. GWEB 20.78% 15 HFC Bank Ltd. HFC 26.09% 16 Produce Buying Co. Ltd. PBC 38.10% 17 Standard Chartered Bank SCB 14.55% 18 SIC Insurance Ltd. -

Ecobank Full Year Review

Analysts Weekly Markets Update Wilfred Agyei Kofi Busia Kyei Rudolf Cofie Tel: +233(0)302 251137 Website: www.umbcapital.com Our Opinion: SELL FEATURE FOR THE WEEK Ecobank’s full year profit declines by 21.56% Return on Equity (DuPont) Performance on the Stock Market 40.00% 37.18% Ecobank Ghana started 2017 at GHS6.40 and appreciated to GHS7.60 (as at 35.00% 34.19% December 2017), translating to a gain of 18.75%, reflecting positive sentiments 30.00% towards the banking giant. The 18.75% gain is better compared to the -8.70% 25.00% 24.87% and -7.76% recorded the same period a year ago and in 2015 respectively. 20.00% It has posted a 52-Week-High of GHS8.05, and a 52-Week Low of GHS6.40, 15.00% Wilfred Agyei with a PE Ratio of 8.74x, with an average price of GHS7.24 over the past 200 10.00% [email protected] days. 5.00% Trading activity has been brisk; a total volume of 3,395,200 shares of the bank 0.00% 2015 2016 2017 exchanged positions during 2017, this is higher than the 1,268,288 shares traded during 2016. Total value of shares traded amounted to GHS22,799,190 significantly higher than the GHS8,607,580 recorded in 2016. Return on Equity fell from 34% to 25% due to the sharp decline in the Net Profit Margin from 37% to 29%. Common Size Analysis FINANCIAL STATEMENT SUMMARY Proportion of Interest income 2017 2016 2015 100.00% INCOME STATEMENT GHS 000 GHS 000 GHS 000 81.92% Interest Income 885,483 878,914 790,961 80.00% Net Profit 255,384 325,594 327,523 64.36% 66.00% 60.00% BALANCE SHEET 41.41% Total Assets 9,098,692 8,025,510 6,587,487 -

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 7th December, 2017 Address: No. 67A & B Switchback Road, Email: [email protected] Website: www.sic-fsl.com Phone: +233-302-767-051 +233-302-767-123 STOCK MARKET GSE STARTS ON POOR NOTE The Ghana Stock Exchange (GSE) started the festive month on INDICATORS WEEK OPEN WEEK END CHANGE a poor note despite strong numerical strength of gainers over Market Capitalization laggards. Out of the seven (7) price movers, four (4) equities (GH¢'million) 58,503.37 58,219.42 -0.49% were ticked-up with the rest dipping. Shares of Access Bank Market Capitalization (US$'million) 13,259.46 13,198.09 -0.46% Limited (ACCESS), Ecobank Transnational Incorporated (ETI) and Ghana Oil Company Limited (GOIL) were the most Volume traded (shares) 5,019,353.00 2,297,271.00 -54.23% affected. Value Traded (GH¢) 13,765,756.99 2,664,838.94 -80.64% The yield on the GSE Composite Index (GSE-CI) dropped from Value Traded (US$) 3,119,930.42 604,107.49 -80.64% 2,521.67 points to 2,508.53 points, resulting in year-to-date Table 1: Market Summary gain 48.51%. Similarly, the GSE Financial Stocks Index (GSE- CI) and the SIC-FSL Top 15 Index (SIC-FSL T-15) closed at INDEX ANALYSIS year-to-date returns of 43.15% and 50.42% respectively INDICATORS CLOSING WEEK YTD lower than 44.19% and 52.42% recorded in the previous LEVEL CHANGE CHANGE week. GSE Composite Index 2,508.53 -0.52% 48.51% Total market capitalization dropped from the previous week’s SIC-FSL Top 15 Index 3,922.78 -1.31% 50.42% figure of GH¢58.50 billion to GH¢58.22 billion last Thursday. -

Databank Weekly Market Watch

March 3, 2017 GSE MARKET STATISTICS SUMMARY Weekly Stock Market Review SCB Tops Gainers Chart for 3rd Consecutive Week: The bulls maintained their Current Previous % Change hold on the equities market this week, supported by price gains in 7 counters. Databank Stock Index 24,460.95 24,329.82 0.54 The Ghana Stock Exchange’s Composite Index (GSE-CI) increased by 11.09 points GSE-CI Level 1,868.19 1,857.10 0.60 w/w to ~1,868 points, while the Databank Stock Index advanced by 131.13 points Market Cap (GH¢ m) 49,147.28 52,310.92 -6.05 w/w to ~24,461 points. The year to date returns of the GSE-CI and the Databank YTD Return DSI 9.53% 8.94% Stock Index thus increased to 10.60% and 9.53% respectively. YTD Return GSE-CI 10.60% 9.95% Market activity was vibrant this week. A block trade in Guinness Ghana Weekly Volume Traded (Shares) 3,567,878 921,507 287.18 Breweries pushed up the volume of shares traded by ~% w/w to ~3.57 million Weekly Turnover (GH¢) 4,603,367 4,555,231 1.06 shares, with a value of ~GH¢4.60 million. Out of the 25 counters that traded this Avg. Weekly Volume Traded (Shares) 878,352 861,281 1.98 week, Guinness Ghana Breweries emerged the most active counter, accounting Avg. Weekly Value Traded (GH¢) 1,268,601 1,246,575 1.77 for 56% of aggregate trade volumes. No. of Counters Traded 25 23 The market breath of the Ghana Stock Exchange was positive this week, with 7 No. -

Has Gse Played Its Role in the Economic Development of Ghana?

CAPITAL MARKET 23 YEARS AND COUNTING: HAS GSE PLAYED ITS ROLE IN THE ECONOMIC DEVELOPMENT OF GHANA? 1st CAPITAL MARKET CONFERENCE BY EKOW AFEDZIE, DEPUTY MANAGING DIRECTOR MAY 10, 2013 INTRODUCTION Ghana Stock Exchange (GSE) was established with a Vision: -To be a relevant, significant, effective and efficient instrument in mobilizing and allocating long-term capital for Ghana’s economic development and growth. INTRODUCTION OBJECTIVES - To facilitate the Mobilization of long term capital by Corporate Bodies/Business and Government through the issuance of securities (shares, bonds, etc). - To provide a Platform for the trading of issued securities. MEMBERSHIP OF GHANA STOCK EXCHANGE GSE as a public company limited by Guarantee has No OWNERS OR SHAREHOLDERS. GSE has Members who are either corporate or individuals. There are two categories of members:- - Licensed Dealing Members - 20 - Associate Members - 34 HISTORICAL BACKGROUND 1968 - Pearl report by Commonwealth Development Finance Co. Ltd. recommended the establishment of a Stock Exchange in Ghana within two years and suggested ways of achieving it. 1970 – 1989 - Various committees established by different governments to explore ways of bringing into being a Stock Exchange in the country. HISTORICAL BACKGROUND 1971 - The Stock Exchange Act was enacted. - The Accra Stock Exchange Company incorporated but never operated. Feb, 1989 - PNDC government set up a 10-member National Committee on the establishment of Stock Exchange under the chairmanship of Dr. G.K. Agama, the then Governor of the Bank of Ghana. HISTORICAL BACKGROUND July, 1989 - Ghana Stock Exchange was incorporated as a private company limited by guarantee under the Companies Code, 1963. HISTORICAL BACKGROUND Nov. -

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 9th October, 2014 SIC FINANCIAL SERVICES LIMITED|ADVISORY|FUND MANAGEMENT|STOCK BROKERAGE|INVESTMENT RESEARCH STOCK MARKET MARKET ACTIVITIES SHORE UP Ren ewed investors confidence in capital market investment, INDICATORS WEEK OPEN WEEK END CHANGE shore up performance on the Ghana Stock Exchange (GSE) Market Capitalization (GH¢ last week. Stocks of Aluworks Limited (ALW), PBC Limited 'million) 63,840.80 64,027.40 0.29% (PBC) and SIC Insurance Company Limited (SIC) were the most Market Capitalization (US$' million) 19,965.85 20,024.21 0.29% sought for within the week. Volume traded (shares) 1,933,674.00 5,818,767.00 200.92% Activities in the above stocks saw key market indices rallied across board, as the broader market (GSE Composite Index), Value Traded (GH¢) 3,842,401.95 7,177,990.01 86.81% GSE Financial Services (GSE-CI) and SIC-FSL Top 15 Index Value Traded (US$) 1,201,689.43 2,244,875.69 86.81% (SIC-FSL T-15) posted better returns than the week before. Table 1: Market Summary The returns on the GSE-CI was 15.53% better than the previous 3.09% on the market, hence the yield on the INDEX ANALYSIS broader market was 3.57% last Thursday. Similarly, the yields on the financial stocks (GSE FSI) and the SIC-FSL Top INDICATORS Closing Week YTD Level Change CHANGE 15 index also appreciated 3.21% and 9.91% to see both yields settled at 18.96% and 13.64% respectively. GSE Composite Index 2,221.73 0.46% 3.57% The cumulative value of the Ghanaian market also rose to SIC-FSL Top 15 Index 3,926.96 1.09% 13.64% GH¢64.03 billion from GH¢63.84 billion the week before. -

Market Report

Market Report July 2017 MARKET HIGHLIGHTS GSE STOCK INDICES/CAPITALIZATION JUL 2017 YTD CHANGE JUL 2016 YTD CHANGE GSE COMPOSITE INDEX (GSE-CI) 2,256.78 33.61% 1,796.29 -9.96% GSE FINANCIAL STOCK INDEX (GSE-FSI) 2,079.34 34.55% 1,678.94 -13.01% MARKET CAPITALIZATION (GH¢ M) 57,209.86 8.46% 54,605.56 -4.40% DOMESTIC CAPITALIZATION (GH¢ M) 14,313.06 27.96% 10,443.75 -6.63% MARKET TURNOVER - EQUITIES JUL 2017 JULY 2016 VOLUME TRADED 7,901,264 9,931,686 VALUE TRADED (GH¢) 24,130,590.21 19,385,939.66 NUMBER OF TRANSACTIONS 1,961 1,561 TRADING DAYS 20 19 NUMBER OF TRADED SYMBOLS 30 30 MARKET DAILY AVERAGES - EQUITIES JUL 2017 JUL 2016 AVERAGE VOLUME TRADED 395,063 522,720 AVERAGE VALUE TRADED (GH¢) 1,206,529.51 1,020,312.61 AVERAGE NUMBER OF TRANSACTIONS 98 82 MARKET TURNOVER - EQUITIES JAN TO JUL 2017 JAN TO JUL 2016 VOLUME TRADED 258,757,395 72,981,621 VALUE TRADED (GH¢) 388,178,582.80 156,094,107.20 NUMBER OF TRANSACTIONS 12,348 12,522 TRADING DAYS 143 144 NUMBER OF TRADED SYMBOLS 37 42 MARKET TURNOVER - FIXED INCOME (DEBT) SECURITIES IN GH¢ MILLIONS JUL 2017 JUL 2016 CORPORATE - - GOG NOTES AND BONDS (GH¢ M) *** 724.39 835.93 MARKET TURNOVER - FIXED INCOME (DEBT) SECURITIES IN GH¢ MILLIONS JAN-JUL 2017 JAN-JUL 2016 CORPORATE - - GOG NOTES AND BONDS (GH¢ M) *** 7,559.02 - LISTINGS JUL 2017 JUL 2016 LISTED COMPANIES 41 39 LISTED EQUITIES ORDINARY SHARES 37 35 DEPOSITORY SHARES 1 1 PREFERENCE SHARES 1 1 EXCHANGE TRADED FUNDS 1 1 FOUR (4) EQUITIES ON GHANA ALTERNATIVE MARKET (GAX) 4 4 DELISTINGS-EQUITIES JUL 2017,JUL 2016) 0 0 NUMBER OF LISTED -

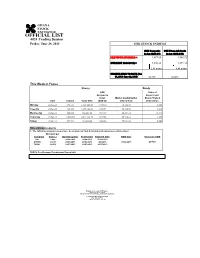

OFFICIAL LIST 4024 Trading Session Friday, June 28, 2013 GSE STOCK INDICES

OFFICIAL LIST 4024 Trading Session Friday, June 28, 2013 GSE STOCK INDICES GSE Composite GSE Financial Stocks Index (GSE-CI) Index (GSE-FSI) PREVIOUS 27/06/2013) = 1,877.65 1,585.72 CURRENT 28/06/2013) = 1,880.26 1,591.18 2.61 points 5.46 points CHANGE-YEAR TO DATE (Jan 01, 2013- June 28, 2013) 56.72% 53.02% This Week in Focus Shares Bonds GSE Value of Composite Government Index Market Capitalization Bonds Traded Date Volume Value GH¢ (GSE-CI) GH¢ million GH¢ million Monday 24-Jun-13 493,511 1,581,041.68 1,900.10 56,154.80 0.000 Tuesday 25-Jun-13 426,550 1,196,438.69 1,891.94 56,110.32 1.240 Wednesday 26-Jun-13 880,088 966,256.30 1,874.67 55,894.32 15.743 Thursday 27-Jun-13 1,553,869 2,844,118.70 1,877.65 55,910.61 4.295 Friday 28-Jun-13 251,546 482,820.80 1,880.26 55,924.82 0.000 Notes/Announcements 1. The following announcements have been made on final dividends and annual general meetings: Dividend per Company Share ¢ Qualifying Date Ex-Div Date Payment Date AGM Date Venue for AGM CAL 0.006 26/06/2013 24/06/2013 30/08/2013 AYRTN 0.0013 25/06/2013 21/06/2013 8/8/2013 27/06/2013 OEPCH TOTAL 0.6900 18/07/2013 16/07/2013 26/07/2013 GCPS:GhanaAICC: Accra International College of Physicians Conference and Centre Surgeons OEPCH:Osu Ebenezer Presbyterian Church HalL Enquiries to: General Manager Ghana Stock Exchange 5th & 6th Floors Cedi House, Liberia Road, Accra Tel: 021 669908, 669914, 669935 Fax: 021 669913 e-mail: [email protected] OFFICIAL LIST 4024 Trading Session ODD LOT Friday, June 28, 2013 ISIN Share Code Total Shares No. -

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 8th January, 2015 STOCK MARKET ACCRA BOURSE MAKES PROMISING START INDICATORS WEEK OPEN WEEK END CHANGE The year 2014 has begun living up to expectations as bullish runs in equities from the petroleum, finance and consumer Market Capitalization (GH¢ goods sectors saw the annual returns of the broader market 'million) 64,352.42 64,229.12 -0.19% Market Capitalization (US$' inch up to 0.42% last Thursday. Though, most equities gave million) 20,109.50 20,014.06 -0.47% up their opening prices, rise in the market value of Ghana Oil Petroleum Company Limited (GOIL), Societe Generale Ghana Volume traded (shares) 783,118.00 573,274.00 -26.80% Table 1: Market Summary Limited (GOIL) and Fan Milk Limited (FML) were enough to close the week’s activities on a positive note. Key benchmark indices closed the week better despite slight volatilities during inter-day trading. The GSE Composite INDEX ANALYSIS index closed at a year-to-date return of 0.42% whiles the GSE Financial Stocks Index settled at 0.67% returns. INDICATORS Closing Week YTD Level Change CHANGE Total market capitalization of the Ghana Stock Exchange was GH¢64.23 billion, an equivalent to USD20.00 billion. GSE Composite Index 2,270.57 0.42% 0.42% GSE Financial Stocks Index 2,258.77 0.67% 0.67% Table 2: Key Stock Market Indices LIQUIDITY The absence of block trades over the period saw liquidity comparatively down last week. All in all, an approximate figure of 573,274 shares exchanged hands within the first trading week of the year, and was also valued about GH¢2.48 million. -

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 14th September, 2017 Address: No. 67A & B Switchback Road, Email: [email protected] Website: www.sic-fsl.com Phone: +233-302-767-051 +233-302-767-123 STOCK MARKET PROFIT-TAKING SLOWS MARKET PERFORMANCE Intense profit-taking on the Ghana Stock Exchange (GSE) INDICATORS WEEK OPEN WEEK END CHANGE saw key performance indicators dip for the first time in Market Capitalization several weeks. Among the nine (9) price movers, five (5) (GH¢'million) 58,810.32 58,022.89 -1.34% equities were ticked-down while the rest gained. Among the Market Capitalization (US$'million) 13,359.91 13,171.45 -1.41% laggards, shares of Standard Chartered Bank Limited (SCB), GCB Bank Limited (GCB), Enterprise Group Limited (EGL) Volume traded (shares) 1,090,896.00 3,860,498.00 253.88% and Trust Bank Gambia Limited (TBL) were the hardest hit on Value Traded (GH¢) 7,134,447.86 9,038,209.20 26.68% the bourse last week. Value Traded (US$) 1,620,728.73 2,051,713.70 26.59% At the close of activities last Thursday yields on the GSE- Table 1: Market Summary Composite Index (GSE-CI), the GSE Financial Stocks Index (GSE-FSI) and the SIC-FSL Top 15 liquid Index (T-15 Index) declined from their previous week year-to-date gains of INDEX ANALYSIS 44.73%, 42.91% and 52.92% to settle at annual returns of 37.08%, 31.38% and 45.33% respectively. INDICATORS Closing Week YTD Level Change CHANGE Total market capitalization dipped from the previous week’s GSE Composite Index 2,315.48 -5.28% 37.08% figure of GH¢58.81 billion to GH¢58.02 billion.