A Statistical Model for the Projection of Flow of Cargo Traffic at the Tema Port

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

I U R E P Orientation Phase R E P O R T G H a 1\F A

International Atomic Energy Agency DRAFT I U R E P ORIENTATION PHASE REPORT G H A 1\F A MR. JEW-PAUL GUELPA MR. WOLFRAM TO GEL December 1982 DISCLAIMER Portions of this document may be illegible in electronic image products. Images are produced from the best available original document UTTEENATIOITAL URANIBK RESOURCES. EVALUATION PROJECT -IURBP- IUSSP ORIENTATION FHAS3 MISSION REPORT BSPTOLIC OP GHANA Dr. J.Fo Guelpa December, 1982. Dro "W. Vogel PREFACE mission, was undertaken, by two consultants, Dr. JoP. Guelpa and Dr. W, Vogel, both, commenced the investigations in Ghana on 5th November, 1982 and completed their work on 16th December, 1982. A total of three days was spent in the field by the consultants* 1. Terse of Ilsferenie .. ., 5 2. General Geography .. .. 4 3. Clirate .. ... 7 4. Population aril I-lain Cities .. .. 9 5. Administrative Regions .. .. S- 6. Official Language, Public Holidays and System of Eeasureaervfc .. ., ll 7. Transport and Consronicatipn .. .. 11 8. Available "aps and Air Photographs .. 12 c. ITCK UB^ITK ICIITIKG n; GH^A • .. .. 13 1. Overview .. .. 13 2. Dianond .. ,. 15 3. Gold .. .. 17 . • 4. Batfzite .. • .. 'IS 5. Manganese .. .. 18 D. IBGI3LATICH ON UEAiTITJK EXPLCHASCtf AlTD XIIIDTG 19 3. KATIOKAL CAFACITI PCS URAFIUI! SXPLORATIC1T AIT3 D272L0P- 1. Ghana Atoiaic Energy CoEE&ssion .. 20 2. Ghana Geological Survey .. .. 22 3. Universities .. .. 24 F. GnOL'OGIC/i 3ST.12r.7 . .. 25 1. Introduction .. ' .. 25 2. The 'vest African Shield Area .. .. 27 2.1 Birician Systec .. .. 27 2.2 Eburnean Granites .. .. 32 2.3 Taria-;aian System .. .. 35 3. Sie Kobile Belt ... .. 3S 3.1 Dahoneyan System •• •• 35 3.2 ?cgc Series •• •• 4C 3 .3 Buen. -

Political Economic Origins of Sekondi‑Takoradi, West Africa's New Oil City

121 UDC: 711.4:711.75+711.453.4(667) DOI: 10.5379/urbani-izziv-en-2012-23-02-005 Franklin OBENG-ODOOM Political economic origins of Sekondi‑Takoradi, West Africa’s new oil city The origins, growth and trajectory of Sekondi‑Takoradi, ure in national and international circles has a historical West Africa’s newest oil city, are considered by using an parallel in the 1920s when, as now, it captured national, “institutional‑analytical” method of economic history. regional and international attention. The evidence sug‑ Particular attention is given to the role of ports, harbours gests that contemporary narratives that strike a determin‑ and railways, and how they evolved and interacted with ist relationship between resource boom and social doom political economic institutions in the last 100 years. This need to be reconsidered. omnibus historical analysis suggests that West Africa’s newest oil city has come full circle. Its contemporary stat‑ Key words: ports, railways, oil, Ghana, Africa Urbani izziv, volume 23, no. 2, 2012 uiiziv-23-2_01.indd 121 26.11.2012 20:26:20 122 F. OBENG-ODOOM 1 Introduction city began its life, grew and rose to fame through economic and political successes. Studies of the city that look at oil (see, e.g., Boohene & Peprah, 2011; Yalley & Ofori‑Darko, 2012; Sekondi‑Takoradi is West Africa’s newest oil city. It is a twin Obeng‑Odoom, 2012a, 2012b) have not been historical. Thus, city in Ghana. Black gold was discovered off its shores in 2007. this paper takes a step in that direction. It looks at the role of By 2010, oil in commercial quantities was flowing in the city political and economic institutions in the origins and trajec‑ and, since 2011, oil has been leaving its shores in pursuit of in‑ tory of Sekondi‑Takoradi in the last 100 years, and it examines ternational currency. -

Fueling the Future of an Oil City a Tale of Sekondi-Takoradi in Ghana

Fueling the Future of an Oil City A Tale of Sekondi-Takoradi in Ghana CONTRIBUTORS FROM GLOBAL COMMUNITIES: Africa in the 21st Century – Rapid Economic Alberto Wilde and Urban Growth Ghana Country Director Africa is experiencing an economic boom period, with many of the fastest growing world economies Ishmael Adams of the last decade in the continent. Ghana is one of the fastest growing economies within Africa, with IncluCity Project Director multiple years of growth in GDP around 7 percent,1 driven by exports of gold and cocoa and, with oil Brian English production that commenced in 2010, further growth is expected. Director, Program Innovation Simultaneously, the continent is transforming due to the effects of rapid urbanization. Africa is the fastest urbanizing continent with urban growth rate of 3.5 percent per year, with that rate expected to hold until 2050.2 Ghana’s rate of urbanization is currently measured at 3.4 percent3 and the country has reached the milestone of 51 percent of its 24 million people living in cities. Urbanization and economic growth spur opportunity but also present challenges such as growth of slums to accommodate the influx of people seeking better jobs and lives in the cities. In turn this can lead to poor quality services and inequalities exacerbated by crime and conflict. Over the last few decades we have also seen an increase in urban disasters. Poor, cramped living conditions, such as those we saw in Port-au-Prince, Haiti, in 2010, can lead to even deadlier and more destructive disasters.4 The world is changing how it views Africa, from seeing the continent through the lens of vulnerability to seeing it through the lens of opportunity. -

Oil City? the Role of Sekondi – Takoradi in Ghana's Emerging Oil Industry

Francisca Amonua Quayson Francisca Amonua Quayson Francisca Oil City? The Role of Sekondi – Takoradi in Ghana’s Emerging Oil Industry Master’s thesis Master’s Oil City? The Role of Sekondi - Takoradi in Ghana’s Emerging Oil Industry Emerging in Ghana’s - Takoradi of Sekondi Oil City? The Role NTNU Science and Technology Science Norwegian University of University Norwegian Faculty of Social Sciences of Social Sciences Faculty Department of Geography Department of Geography and Technology Management Management and Technology Map from: http://crossedcrocodiles.wordpress.com/2009/07/16/ghanas-jubilee-oil-field/jubileefieldmap/ Master Thesis for the Award of Master of Philosophy (MPhil) in Development Studies, Specializing in Geography Trondheim, Spring 2012 Oil City? The Role of Sekondi - Takoradi in Ghana’s Emerging Oil Industry Francisca Amonua Quayson Master Thesis for the Award of Master of Philosophy (MPhil) in Development Studies, Specializing in Geography Department of Geography Norwegian University of Science and Technology Trondheim, June 2012 I II DECLARATION I Francisca Amonua Quayson hereby declare that in exception of references used, which were duly cited and acknowledged, this dissertation is an outcome of a research conducted under the supervision of Professor Stig Jorgensen of the Department of Geography in the Norwegian University of Science and Technology, Trondheim, Norway. ……………………………………………………….. Francisca Amonua Quayson June, 2012 Trondheim, Norway III DEDICATION I dedicate this work to my maker and to my family who have been very supportive of me. To my parents, thank you for being there for me. To my brothers Oppong, Ekow and Ebo, I love you all. I also dedicate this thesis to the memory of my late grandpa who passed on while I was writing this thesis. -

Imperial Travelers: the Formation of West African Urban Culture, Identity, and Citizenship in London and Accra, 1925-1935

Imperial Travelers: The Formation of West African Urban Culture, Identity, and Citizenship in London and Accra, 1925-1935 by Jinny Kathleen Prais A dissertation submitted in partial fulfillment Of the requirements for the degree of Doctor of Philosophy (History and Women‘s Studies) in the University of Michigan 2008 Doctoral Committee: Professor Mamadou Diouf, Co-Chair Professor Carroll Smith-Rosenberg, Co-Chair Associate Professor Michele Mitchell Reader in English, Stephanie M. Newell, University of Sussex © Jinny Kathleen Prais 2008 Dedication For Carroll Smith-Rosenberg Whose example it is my greatest ambition to emulate ii Acknowledgements This dissertation is the product of many institutions and people. First, I would like to acknowledge the West African students who set up clubs and newspapers in London and Accra, sent copies of their journals to the British Museum, and made their way into public archives and records. They have left behind a rich and endlessly stimulating set of documents. I am grateful to a number of schools, programs and departments at the University of Michigan for providing funding for this project: the Rackham Graduate School, the Program in Women‘s Studies, the Department of History, the Center for African and AfroAmerican Studies, the Gayle Morris Sweetland Writing Center, the Seminar on Global and Ethnic Literatures, and the Institute for Research on Women and Gender. I especially acknowledge the generous support of the Center for the Education of Women. The staff and faculty of the Sweetland Writing Center have provided invaluable feedback on this project. I am particularly grateful to Charlotte Boulay for guiding me as I worked through each chapter, and for her editorial assistance. -

History of Ghana Advisory Board

THE HISTORY OF GHANA ADVISORY BOARD John T. Alexander Professor of History and Russian and European Studies, University of Kansas Robert A. Divine George W. Littlefield Professor in American History Emeritus, University of Texas at Austin John V. Lombardi Professor of History, University of Florida THE HISTORY OF GHANA Roger S. Gocking The Greenwood Histories of the Modern Nations Frank W. Thackeray and John E. Findiing, Series Editors Greenwood Press Westport, Connecticut • London Library of Congress Cataloging-in-Publication Data Cocking, Roger. The history of Ghana / Roger S. Gocking. p. cm. — (The Greenwood histories of the modern nations, ISSN 1096-2905) Includes bibliographical references (p. ) and index. ISBN 0-313-31894-8 (alk. paper) 1. Ghana—History. I. Title. II. Series. DT510.5.G63 2005 966.7—dc22 2004028236 British Library Cataloguing in Publication Data is available. Copyright © 2005 by Roger S. Gocking All rights reserved. No portion of this book may be reproduced, by any process or technique, without the express written consent of the publisher. Library of Congress Catalog Card Number: 2004028236 ISBN: 0-313-31894-8 ISSN: 1096-2905 First published in 2005 Greenwood Press, 88 Post Road West, Westport, CT 06881 An imprint of Greenwood Publishing Group, Inc. www.greenwood.com Printed in the United States of America The paper used in this book complies with the Permanent Paper Standard issued by the National Information Standards Organization (Z39.48-1984). 10 987654321 Contents Series Foreword vii Frank W. Thackeray and John -

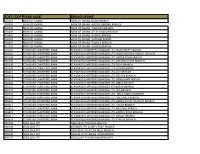

Sort Code Bank Name Branch Name

SORT CODE BANK NAME BRANCH NAME 010101 BANK OF GHANA BANK OF GHANA ACCRA BRANCH 010303 BANK OF GHANA BANK OF GHANA -AGONA SWEDRU BRANCH 010401 BANK OF GHANA BANK OF GHANA -TAKORADI BRANCH 010402 BANK OF GHANA BANK OF GHANA -SEFWI BOAKO BRANCH 010601 BANK OF GHANA BANK OF GHANA -KUMASI BRANCH 010701 BANK OF GHANA BANK OF GHANA -SUNYANI BRANCH 010801 BANK OF GHANA BANK OF GHANA -TAMALE BRANCH 011101 BANK OF GHANA BANK OF GHANA - HOHOE BRANCH 020101 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-HIGH STREET BRANCH 020102 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD- INDEPENDENCE AVENUE BRANCH 020104 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-LIBERIA ROAD BRANCH 020105 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-OPEIBEA HOUSE BRANCH 020106 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-TEMA BRANCH 020108 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-LEGON BRANCH 020112 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-OSU BRANCH 020118 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-SPINTEX BRANCH 020121 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-DANSOMAN BRANCH 020126 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD-ABEKA BRANCH 020127 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH)-ACHIMOTA BRANCH 020129 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD- NIA BRANCH 020132 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD- TEMA HABOUR BRANCH 020133 STANDARD CHARTERED BANK STANDARD CHARTERED BANK(GH) LTD- WESTHILLS BRANCH 020436 -

Download the Full Report

Social Responsibility CONTENTS Page Notice of Annual General Meeting 2 Five-Year Financial Summary 3 Board of Directors, Officials and Registered Office 4 Profile of Board of Directors 5 Chairman’s Report 6 Managing Director’s Report 9 Report of the Directors 13 Report of the Auditors 16 Consolidated Statement of Profit or Loss 18 Consolidated Statement of Other Comprehensive Income 19 Consolidated Statement of Financial Position 20 Consolidated Statement of Changes in Equity 21 Consolidated Statement of Cash Flows 22 Notes to the Consolidated Financial Statements 23 Notes on Resolutions to be Passed 76 Proxy Form 77 ANNUAL REPORT 2014 1 NOTICE OF ANNUAL GENERAL MEETING OF CAL BANK LIMITED TO BE HELD ON FRIDAY, 27 MARCH 2015 AT THE GHANA COLLEGE OF PHYSICIANS RIDGE, ACCRA NOTICE IS HEREBY GIVEN that the Annual General Meeting of CAL Bank Limited will be held at 10 a.m. on Friday, 27 March, 2015 at the Conference Auditorium of Ghana College of Physicians and Surgeons, Ridge, Accra to transact the following business: AGENDA 1. To receive and consider the Reports of the Directors and the Auditors, and the Accounts of the Company for the year ended December 31, 2014 2. To declare a final dividend for the year ended December 31, 2014 3. To authorise the Directors to fix the fees of the Auditors 4. To re-elect Directors retiring by rotation 5. To re-elect newly-appointed Directors 6. To approve directors’ remuneration Dated this 19th day of February, 2015 BY ORDER OF THE BOARD VERITAS ADVISORS LIMITED COMPANY SECRETARY Note A member entitled to attend and vote at the Annual General Meeting may appoint a proxy to attend and vote on his/her behalf. -

BANK of GHANA Banks' Swift and Sort Codes

BANK OF GHANA ___ ________ _____________ _________________ ______________________ ______________________________ _____________________________________ ___________________________________________ ___________________________________________ Banks’ Swift and Sort Codes _____________________________________________ ________________________________________ ________________________________ __________________________ ______________________ _______________ _________ ______ ___ JUNE 2012 C o n t e n t Page 1. Introduction … … … … 2 2. Components of the Sort Code … … … … 2 3. Clearing Cycle … … … … 2 4. Bank and Swift Codes … … … … 3 5. Bank Branch Sort Code … … … … 4 6. Bank of Ghana … … … … 4 7. Standard Chartered Bank (Gh) Ltd … … … … 4 8. Barclays Bank (Gh) Ltd. … … … … 5 9. Ghana Commercial Bank Ltd. … … … … 7 10. National Investment Bank Ltd. … … … … 12 11. United Bank for Africa (Gh). Ltd. … … … … 13 12. ARB Apex Bank Ltd. … … … … 13 13. Accra Area … … … … 13 14. Koforidua Area … … … … 14 15. Cape Coast Area … … … … 15 16. Takoradi Area … … … … 15 17. Ho Area … … … … 15 18. Kumasi Area … … … … 16 19. Sunyani Area … … … … 17 20. Tamale Area … … … … 17 21. Bolgatanga Area … … … … 18 22. Wa Area … … … … 18 23. Hohoe Area … … … … 18 24. Agricultural Development Bank … … … … 18 25. SG-SSB Bank Ltd. … … … … 20 26. Merchant Bank (Gh) Ltd. … … … … 22 27. HFC Bank Ltd. … … … … 22 28. Zenith Bank (Gh) Ltd. … … … … 23 29. Ecobank (Gh) Ltd. … … … … 24 30. Cal Bank Ltd. … … … … 25 31. The Trust Bank Ltd. … … … … 26 32. UT Bank Ghana Ltd. … … … … 27 33. First Atlantic Merchant Bank Ltd. … … … … 27 34. Prudential Bank Ltd. … … … … 28 35. Stanbic Bank Ghana Ltd. … … … … 28 36. International Commercial Bank Ltd. … … … … 29 37. Amalgamated Bank Ltd. … … … … 30 38. Unibank (Gh) Ltd. … … … … 30 39. Guaranty Trust Bank Ltd. … … … … 31 40. Fedelity Bank Ghana Ltd. … … … … 31 41. Intercontinental Bank (Gh) Ltd. … … … … 32 42. Bank of Baroda (Gh) Ltd. … … … … 33 43. -

AR 2016 Final

ANNUAL REPORT & 20 FINANCIAL STATEMENTS 16 Ghana Oil Company Limited Annual Report and Financial Statements 2016 CONTENTS COMPANY INFORMATION 2 NOTICE OF ANNUAL GENERAL MEETING 3 RESOLUTIONS 4 BOARD OF DIRECTORS 5 MANAGEMENT TEAM 6 CHAIRMAN’S ADDRESS 7 - 10 CORPORATE EVENTS 11 - 12 PERFORMANCE AT A GLANCE (2012 - 2016) 13 REPORT OF DIRECTORS 14 REPORT OF AUDITORS 15 - 16 STATEMENT OF COMPREHENSIVE INCOME 17 - 18 STATEMENT OF FINANCIAL POSITION 19 STATEMENT OF CHANGES IN EQUITY 20 STATEMENT OF CASH FLOW 21 NOTES TO THE FINANCIAL STATEMENTS 22 - 44 CONSOLIDATED COMPREHENSIVE INCOME 45 NOTES 46 PROXY FORM 47 Good energy Company Information Board Of Directors: Prof. William A. Asomaning - Chairman Mr. Patrick Akpe Kwame Akorli - Group CEO & MD Nana Esuman Kwesi Yankah - Member Mr. Eugene Akoto-Bamfo - Member Mr. Chris A-Ackummey - Member Mad. Faustina Nelson - Member Mr. Thomas Kofi Manu - Member Mr. Damian Yelbonkang Zaato - Member Aihaji Razak El-Alawa - Member Secretary: Nana Ama Kusi-Appouh Auditors: PKF Chartered Accountants Farrar Avenue P.O. Box 1219 Accra Registered Office: D 659/4, Kojo Thompson Road P.O. Box GP 3183 Accra Registrars: UMB Registrars 123 Kwame Nkrumah Avenue Sethi Plaza Adabraka, Accra Bankers: GCB Bank Limited Standard Chartered Bank Ghana Limited Barclays Bank of Ghana Limited Ecobank Ghana Limited Universal Merchant Bank Limited Agricultural Development Bank Limited Prudential Bank Limited Zenith Bank Ghana Limited First Atlantic Bank Ghana Limited National Investment Bank Limited Societe Generale Ghana Limited Stanbic Bank Ghana Limited United Bank for Africa (Ghana) Limited GN Bank Unibank (Ghana) Limited Access Bank Ghana Limited Ghana Oil Company Limited Annual Report and Financial Statements 2016 2 Notice Of 48th Annual General Meeting NOTICE IS HEREBY GIVEN that the 48th Annual General Meeting of the Shareholders of Ghana Oil Company Limited will be held at the Auditorium, College of Physicians and Surgeons, Ridge, Accra on Thursday, 18th May, 2017 at 11:00 am for the transaction of the following business: AGENDA ORDINARY BUSINESS 1. -

Tullow Ghana Ltd Jubilee Project

REPORT OF THE: EXTERNAL INDEPENDENT MONITORING GROUP TULLOW GHANA LTD JUBILEE PROJECT Site visit: April 2013 Ghana FINAL REPORT Prepared for International Finance Corporation REPORT EXTERNAL INDEPENDENT MONITORING GROUP TULLOW GHANA LTD JUBILEE PROJECT FINAL REPORT GHANA Site Visit: APRIL 2013 Prepared for: International Finance Corporation Prepared by: D’Appolonia S.p.A. Via San Nazaro, 19 16145 Genova, Italia www.dappolonia.it Team Members: Massimiliano Monetti Team Leader - Environmental Engineer Fiorenzo Calò Health and Safety Specialist Laura Elena Ferretti Socio-economic Specialist 3 CONTENTS TABLES ................................................................................................................................................. 4 FREQUENTLY USED ACRONYMS ................................................................................................. 5 EXECUTIVE SUMMARY ................................................................................................................... 7 1 INTRODUCTION ....................................................................................................................... 10 1.1 REPORT ORGANIZATION ................................................................................................ 11 2 INDEPENDENT VERIFICATION SCOPE OF THE WORK AND ADOPTED METHODOLOGY ...................................................................................................................... 12 3 SITE VISIT DESCRIPTION .................................................................................................... -

Download [PDF, 5.38

REPUBLIC OF GHANA 2010 POPULATION AND HOUSING CENSUS ENUMERATOR’S MANUAL ******************************** STATISTICAL SERVICE 31ST AUGUST, 2010 TABLE OF CONTENTS CHAPTER 1: THE CONCEPT OF POPULATION AND HOUSING CENSUS ................................... 1 1.1 What is a Population Census? ............................................................................................................. 1 1.2 What is a Housing Census? ................................................................................................................ 1 1.3 The essential features of a Population and Housing Census ............................................................... 1 1.4 Why are we conducting the 2010 Census? ......................................................................................... 2 1.5 History of Census taking in Ghana ..................................................................................................... 2 CHAPTER 2: LEGAL FRAMEWORK FOR THE CENSUS .................................................................. 3 2.1 Legal Authority for the Census ........................................................................................................... 3 2.2 Legal right for entering premises to conduct the Census .................................................................... 3 2.3 Law requires the public to respond to Census enquiries ..................................................................... 3 2.4 Law prohibits divulging Census information .....................................................................................