Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ghana Gazette

GHANA GAZETTE Published by Authority CONTENTS PAGE Facility with Long Term Licence … … … … … … … … … … … … 1236 Facility with Provisional Licence … … … … … … … … … … … … 201 Page | 1 HEALTH FACILITIES WITH LONG TERM LICENCE AS AT 12/01/2021 (ACCORDING TO THE HEALTH INSTITUTIONS AND FACILITIES ACT 829, 2011) TYPE OF PRACTITIONER DATE OF DATE NO NAME OF FACILITY TYPE OF FACILITY LICENCE REGION TOWN DISTRICT IN-CHARGE ISSUE EXPIRY DR. THOMAS PRIMUS 1 A1 HOSPITAL PRIMARY HOSPITAL LONG TERM ASHANTI KUMASI KUMASI METROPOLITAN KPADENOU 19 June 2019 18 June 2022 PROF. JOSEPH WOAHEN 2 ACADEMY CLINIC LIMITED CLINIC LONG TERM ASHANTI ASOKORE MAMPONG KUMASI METROPOLITAN ACHEAMPONG 05 October 2018 04 October 2021 MADAM PAULINA 3 ADAB SAB MATERNITY HOME MATERNITY HOME LONG TERM ASHANTI BOHYEN KUMASI METRO NTOW SAKYIBEA 04 April 2018 03 April 2021 DR. BEN BLAY OFOSU- 4 ADIEBEBA HOSPITAL LIMITED PRIMARY HOSPITAL LONG-TERM ASHANTI ADIEBEBA KUMASI METROPOLITAN BARKO 07 August 2019 06 August 2022 5 ADOM MMROSO MATERNITY HOME HEALTH CENTRE LONG TERM ASHANTI BROFOYEDU-KENYASI KWABRE MR. FELIX ATANGA 23 August 2018 22 August 2021 DR. EMMANUEL 6 AFARI COMMUNITY HOSPITAL LIMITED PRIMARY HOSPITAL LONG TERM ASHANTI AFARI ATWIMA NWABIAGYA MENSAH OSEI 04 January 2019 03 January 2022 AFRICAN DIASPORA CLINIC & MATERNITY MADAM PATRICIA 7 HOME HEALTH CENTRE LONG TERM ASHANTI ABIREM NEWTOWN KWABRE DISTRICT IJEOMA OGU 08 March 2019 07 March 2022 DR. JAMES K. BARNIE- 8 AGA HEALTH FOUNDATION PRIMARY HOSPITAL LONG TERM ASHANTI OBUASI OBUASI MUNICIPAL ASENSO 30 July 2018 29 July 2021 DR. JOSEPH YAW 9 AGAPE MEDICAL CENTRE PRIMARY HOSPITAL LONG TERM ASHANTI EJISU EJISU JUABEN MUNICIPAL MANU 15 March 2019 14 March 2022 10 AHMADIYYA MUSLIM MISSION -ASOKORE PRIMARY HOSPITAL LONG TERM ASHANTI ASOKORE KUMASI METROPOLITAN 30 July 2018 29 July 2021 AHMADIYYA MUSLIM MISSION HOSPITAL- DR. -

Ministry of Transport

MINISTRY OF TRANSPORT DRAFT SECTOR MEDIUM-TERM DEVELOPMENT PLAN FOR 2014 - 2017 January 2014 Ministry of Transport SMTDP 2014-2017 Page 1 Ministry of Transport SMTDP 2014-2017 Page 2 EXECUTIVE SUMMARY This is the first Draft of the Ministry of Transport Sector’s Medium Term Development Plan (SMTDP) which has been developed through a consultative process involving the Ministry of Transport and the transport sector Agencies over which it has oversight responsibility. Led by the Ministry, the process commenced in April with consultations and briefings, progressed through August. This SMTDP broadly follows the guidelines and structure proposed by NDPC although, in a search for more detailed and relevant guidance. Chapter 3 looked at the challenges typically presented by the sector to discover the underlying reasons particularly for the perpetually reported ‘lack of financing’, the policy objectives and strategies of the sector. Every effort has been made to harmonize the performance review undertaken in Chapters 1 and 2 with: The sector objectives set out in the Ghana Shared Growth and Development Agenda (GSGDA); the analysis undertaken as part of the Integrated Transport Planning (ITP) project; and the annual performance and operational reviews undertaken by the Agencies. The transport sector benefits from alignment between the objectives set out in the GSGDA with the policy goals and objectives set out in the National Transport Policy (NTP). Chapter 3, provides the adopted policy objectives and strategies from the National Medium Term Development framework 2014-2017 to achieve MDA and National goals in relation to the appropriate theme and also make development projections for 2014-2017 It is the intent of the Ministry and its Agencies to update and integrate more of the ITP recommendations into future plans for the sector. -

National Teacher Licensing Project Movement Plan/Time Table

NATIONAL TEACHER LICENSING PROJECT MOVEMENT PLAN/TIME TABLE GREATER ACCRA REGION NATIONAL TEACHER LICENSING PROJECT MOVEMENT PLAN/TIME TABLE REGION: GREATER ACCRA METRO/MUNICIPAL/DISTRICT: ACCRA METRO & ABLEKUMA WEST MMD_MANE CIRCUIT TR CENTRE_NAM LOCATION/TO CT MACHS START S E WN RS DATE LUNCHING OF THE PORJECT MIN. OF MINISTRIES 1 2 14/05/2 EDUCATION 021 ACCRA AYALOLO 75 RICHARD AROUND 8 16 17/05/2 METRO USSHER 15 ACQUAYE TIMBER 021 5 MEMORIAL MARKET SCHOOL GA MASHIE 19 INDEPENDEN AROUND 7 CE AVE. HALL MAKOLA LAW SCH. KANESHIE 29 KANESHIE AROUND 1 KINGSWAY COCOA CLUST. CLINIC KORLE 25 NANKA GONNO 2 BRUCE JHS MAMPROBI 11 DR. HS NEAR 5 BANNERMAN M'PROBI BASIC SCH. POLICE STAT. OJOO 16 St. GEORGE'S 7 ANG. CHURCH BUBUASHIE 22 St. JOSEPHS AROUND 1 ANGLICAN. BUBUASHIE SCH. R/ABT ACCRA AROUND METRO ED. KIMBU SHS OFF TOTAL 14 73 MMD_MANE CIRCUIT TR CENTRE_NAM LOCATION/TO CT MACHS START S E WN RS DATE ABLEKUMA DANSOMAN 27 DANSOMAN OKPOTI 2 4 18/05/2 WEST 1 COMM. BASIC COMPOUND- 021 SCH. SAHARA GBEGBEYISE 21 GBEGBEYISE LAST STOP- 6 BASIC LASPALMAS SCHOOL FOOD TOTAL 48 7 MMD_MANE CIRCUIT TR CENTRE_NAM LOCATION/TO CT MACHS START S E WN RS DATE LLA MADINA 33 SDA BASIC MADINA NEW 5 9 18/05/2 NKWANTAN NEW ROAD 2 SCHOOL ROAD 021 ANG- ESTATE OPPOSITE MADINA MADINA POLYCLINIC PRESEC 34 PRESEC SHS ON LEGON- 5 MADINA ROAD PANTANG 28 WASS SHS MAKE A U- 1 TURN B/4 ADENTA JN FIRE ARMOR 25 NKWANTANA TURN RIGHT NKWANTANA 3 NG CLUSTER AFTER G OF SCH. -

KPARIB YEN-WON DOUGLAS.Pdf

KWAME NKRUMAH UNIVERSITY OF SCIENCE AND TECHNOLOGY KUMASI INSTITUTE OF DISTANCE LEARNING A BUS REPLACEMENT MODEL FOR THE STATE TRANSPORT COMPANY, KUMASI. THESIS SUBMITTED TO KNUST MATHEMATICS DEPARTMENT IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR THE AWARD OF MASTER OF SCIENCE DEGREE IN INDUSTRIAL MATHEMATICS BY KPARIB YEN-WON DOUGLAS (B Ed) DECEMBER 2009. DECLARATION I hereby declare that, except for the specific references, which have been duly acknowledge, this work is the result of my own field research and it has not been submitted either in part or whole for any other degree elsewhere. Kparib Yen-won Douglas ………………….. …………. PG1836107 Student name & ID Signature Date Certified by: Mr. Kwaku Darkwah ………………….. ……………… Supervisor Signature Date Certified by: Prof E. Badu ………………….. ……………… Dean of IDL Signature Date Certified by: Dr. S.K Amponsah ……………….. ……………. Head of Department Signature Date i ABSTRACT The State Transport Company, like many service organizations, faces the problem of how long a bus should be on the road before it is replaced. The aim of this thesis is therefore to determine a schedule of disposals and replacements of the Higher bus, taking into account the revenue generated, operating cost and the salvage values, such that the total cost of these activities is minimized. Data was collected from the State Transport Company Office in Kumasi on the revenue generated, operating cost, and the salvage values on the bus with time. The problem was solved by using dynamic programming. It was found out that the company should always dispose its buses when they are two years old. ii DEDICATION I give thanks and praises to the Most High God on whose grace alone bring all good things into fruition. -

Ssnit Investments Series

SSNIT INVESTMENTS SERIES SECOND EDITION INTRODUCTION This edition of the SSNIT Investments Series focuses on the Listed Equities Portfolio, one of the three sub-asset classes of the Equities Portfolio. Listed equity refers to ownership interests in companies whose shares are traded publicly on a Stock Market. The Trust currently has share interests in 23 out of the 37 companies listed on the Ghana Stock Exchange (GSE), with a total value of GH¢1.8 billion as at June 2017. A portion of the Trust’s shares in Tullow Oil Plc is also listed on the London Stock Exchange (LSE). The composition of the Trust’s Listed Equities Portfolio, also referred to as the SSNIT Stock Market Portfolio (SSMP), is shown in Table 1. Table 1: SSNIT Listed Equity Holdings # Company Ticker Shareholding (%) 1 Anglogold Ashanti Ltd. AGA 0.02% 2 Aluworks Limited ALW 62.62% 3 Ayrton Drug Man. Ltd. AYRTN 18.00% 4 Benso Oil Palm Plantation BOPP 4.31% 5 CAL Bank Limited CAL 33.18% 6 Cocoa Processing Co. Ltd. CPC 10.14% 7 Ecobank Ghana Ltd. EGH 16.21% 8 Enterprise Group Ltd EGL 6.22% 9 Ecobank Transnational Inc. ETI 3.86% 10 Fan Milk Limited FML 1.59% 11 GCB Bank GCB 29.89% 12 Guinness Gh. Breweries Ltd. GGBL 7.57% 13 Ghana Oil Co. Ltd. GOIL 25.00% 14 Golden Web Ltd. GWEB 20.78% 15 HFC Bank Ltd. HFC 26.09% 16 Produce Buying Co. Ltd. PBC 38.10% 17 Standard Chartered Bank SCB 14.55% 18 SIC Insurance Ltd. -

Logistics Capacity Assessment Ghana Country Name Ghana Official Name Ghana

LCA - Ghana Version 1.05 Logistics Capacity Assessment Ghana Country Name Ghana Official Name Ghana Assessment Assessment Dates: From To 11th February 2011 Name of Assessor Izzeldin Abdalla Title & Position Logistics Officer Email contact [email protected] 1/72 LCA - Ghana Version 1.05 Table of Contents………………………………………………………………… ……………….. 1. Country Profile ......................................................................................................................... 3 1.1. Introduction & Background ................................................................................................ 3 1.2. Humanitarian Background ................................................................................................ 4 1.3. National Regulatory Departments ..................................................................................... 7 1.4. Customs Information ......................................................................................................... 8 2. Logistics Infrastructure ........................................................................................................... 13 2.1. Port Assessment............................................................................................................. 13 2.2. Airport Assessment ......................................................................................................... 25 2.3. Road Assessment ........................................................................................................... 31 2.4. Railway Assessment -

Has Gse Played Its Role in the Economic Development of Ghana?

CAPITAL MARKET 23 YEARS AND COUNTING: HAS GSE PLAYED ITS ROLE IN THE ECONOMIC DEVELOPMENT OF GHANA? 1st CAPITAL MARKET CONFERENCE BY EKOW AFEDZIE, DEPUTY MANAGING DIRECTOR MAY 10, 2013 INTRODUCTION Ghana Stock Exchange (GSE) was established with a Vision: -To be a relevant, significant, effective and efficient instrument in mobilizing and allocating long-term capital for Ghana’s economic development and growth. INTRODUCTION OBJECTIVES - To facilitate the Mobilization of long term capital by Corporate Bodies/Business and Government through the issuance of securities (shares, bonds, etc). - To provide a Platform for the trading of issued securities. MEMBERSHIP OF GHANA STOCK EXCHANGE GSE as a public company limited by Guarantee has No OWNERS OR SHAREHOLDERS. GSE has Members who are either corporate or individuals. There are two categories of members:- - Licensed Dealing Members - 20 - Associate Members - 34 HISTORICAL BACKGROUND 1968 - Pearl report by Commonwealth Development Finance Co. Ltd. recommended the establishment of a Stock Exchange in Ghana within two years and suggested ways of achieving it. 1970 – 1989 - Various committees established by different governments to explore ways of bringing into being a Stock Exchange in the country. HISTORICAL BACKGROUND 1971 - The Stock Exchange Act was enacted. - The Accra Stock Exchange Company incorporated but never operated. Feb, 1989 - PNDC government set up a 10-member National Committee on the establishment of Stock Exchange under the chairmanship of Dr. G.K. Agama, the then Governor of the Bank of Ghana. HISTORICAL BACKGROUND July, 1989 - Ghana Stock Exchange was incorporated as a private company limited by guarantee under the Companies Code, 1963. HISTORICAL BACKGROUND Nov. -

Options and Challenges for Connectivity and Energy in Ghana

Rural Access: Options and Challenges for Connectivity and Energy in Ghana Jonnie Akakpo October 2008 Rural Access: Options and Challenges for Connectivity and Energy in Ghana A study carried out for the International Institute for Communication and Development (IICD) and the Ghana Information Network for Knowledge Sharing (GINKS) by Jonnie Akakpo, Consolidated Solutions Limited (CSL) Jointly published by GINKS and IICD October 2008 GINKS DTD 173 Cantonments Accra Ghana Email: [email protected] Tel: +233 21 785654 Fax: +233 21 786554 Colophon Author: Jonnie Akakpo, CSL Coordinator: Martine Koopman, IICD Editor: Theresa Stanton, IICD Publisher: GINKS/IICD Contents List of Abbreviations and Acronyms………………………………………………………………………………..5 Purpose of this Report.......................................................................................8 Executive Summary ..........................................................................................9 A Historical Perspective on Connectivity ............................................................. 10 Rural Connectivity: The Challenges ................................................................... 12 Applications and Uses of Connectivity ................................................................ 15 Main Types of Connectivity Available ................................................................. 16 Technical Considerations on Connectivity ........................................................... 19 Geographic Coverage ..................................................................................... -

Country Report: Ghana

Report by INTALInC Transport and Social Exclusion in Ghana June 2019 Supported by the Volvo Research and Educational Foundations i Authors Albert M. Abane, Regina O. Amoako-Sakyi, Samuel A. Owusu, Kwabena K. Agyemang, Prince K. Odame, University of Cape Coast, Ghana International Network for Transport and Accessibility in Low Income Countries (INTALInC) Volvo Research and Education Foundations (VREF) Photographic Contributors Regina O. Amoako-Sakyi, University of Cape Coast, Ghana Emma Tsoneva, University of Leeds, UK Executive Summary Ghana, a country of about 29 million people is classified as a lower middle-income economy gradually being taken over by the services sector after a long ride with the agricultural sector. Currently, about 55.3% of the population is urbanised, rising from 4 million to 14 million over the past three decades. The nation’s capital and largest city by population size, Accra, has an estimated urban population of 2.27 million whilst Cape Coast, the seventh ranked city, has a population of 227,269. Poverty is still a challenge to its citizens and, over the years, several programmes have been rolled out to tackle its effects on vulnerable populations such as orphaned children, people with disabilities and the elderly. Among these initiatives are the Livelihood Empowerment Against Poverty (LEAP), Capitation Grant, School Feeding programme, free distribution of school uniforms and books, Community-based Health Planning Services (CHPS), free bus rides for school children (FBRSC) and, just recently, free Senior High School Education. Most of these programmes have chalked various levels of success since their implementation. The country was able to half poverty between 1992 and 2013, reducing it from 56.5% to 24% and extreme poverty from 16.5 to 8.4%. -

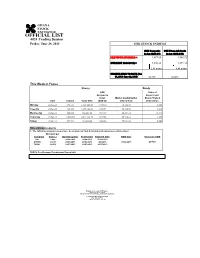

OFFICIAL LIST 4024 Trading Session Friday, June 28, 2013 GSE STOCK INDICES

OFFICIAL LIST 4024 Trading Session Friday, June 28, 2013 GSE STOCK INDICES GSE Composite GSE Financial Stocks Index (GSE-CI) Index (GSE-FSI) PREVIOUS 27/06/2013) = 1,877.65 1,585.72 CURRENT 28/06/2013) = 1,880.26 1,591.18 2.61 points 5.46 points CHANGE-YEAR TO DATE (Jan 01, 2013- June 28, 2013) 56.72% 53.02% This Week in Focus Shares Bonds GSE Value of Composite Government Index Market Capitalization Bonds Traded Date Volume Value GH¢ (GSE-CI) GH¢ million GH¢ million Monday 24-Jun-13 493,511 1,581,041.68 1,900.10 56,154.80 0.000 Tuesday 25-Jun-13 426,550 1,196,438.69 1,891.94 56,110.32 1.240 Wednesday 26-Jun-13 880,088 966,256.30 1,874.67 55,894.32 15.743 Thursday 27-Jun-13 1,553,869 2,844,118.70 1,877.65 55,910.61 4.295 Friday 28-Jun-13 251,546 482,820.80 1,880.26 55,924.82 0.000 Notes/Announcements 1. The following announcements have been made on final dividends and annual general meetings: Dividend per Company Share ¢ Qualifying Date Ex-Div Date Payment Date AGM Date Venue for AGM CAL 0.006 26/06/2013 24/06/2013 30/08/2013 AYRTN 0.0013 25/06/2013 21/06/2013 8/8/2013 27/06/2013 OEPCH TOTAL 0.6900 18/07/2013 16/07/2013 26/07/2013 GCPS:GhanaAICC: Accra International College of Physicians Conference and Centre Surgeons OEPCH:Osu Ebenezer Presbyterian Church HalL Enquiries to: General Manager Ghana Stock Exchange 5th & 6th Floors Cedi House, Liberia Road, Accra Tel: 021 669908, 669914, 669935 Fax: 021 669913 e-mail: [email protected] OFFICIAL LIST 4024 Trading Session ODD LOT Friday, June 28, 2013 ISIN Share Code Total Shares No. -

Co-Modality: Opportunities and Barriers in the Greater Toronto Area

Co-Modality: Opportunities and Barriers in the Greater Toronto Area by Bernard Adu-Mensah A thesis presented to the University of Waterloo in fulfilment of the thesis requirement for the degree of Master of Environmental Studies in Planning Waterloo, Ontario, Canada, 2019 ©Bernard Adu-Mensah 2019 Author’s Declaration I hereby declare that I am the sole author of this thesis. This is a true copy of the thesis, including any required final revisions, as accepted by my examiners. I understand that my thesis may be made electronically available to the public. ii Abstract The Greater Toronto Area is said to be one of the fastest growing regions in Ontario experiencing many challenges due to the influx of population and the demand for goods and services. Amongst the challenges include externalities associated with the last mile delivery of goods such as traffic congestion, emissions of Green House Gases, and illegal parking of delivery vehicles posing as threats to active transportation. The purpose of this study was to identify opportunities for combining both passengers and freight (parcels) in the same vehicle at the same time (co-modality) and barriers that might hinder such a practice in the city of Toronto. The study also sought to identify current co-modal practices in the Greater Toronto Area. The methodology employed for the research was the exploratory research design using semi-structured interview guides to collect valuable information from stakeholders in the city of Toronto through telephone interviews and face-face interviews. Again, information was obtained through literature review. The information collected from the interview process were analysed using the thematic framework analysis. -

Weekly Market Watch Sic-Fsl Investment+ Research| Market Reviews|Ghana

WEEKLY MARKET WATCH SIC-FSL INVESTMENT+ RESEARCH| MARKET REVIEWS|GHANA 8th January, 2015 STOCK MARKET ACCRA BOURSE MAKES PROMISING START INDICATORS WEEK OPEN WEEK END CHANGE The year 2014 has begun living up to expectations as bullish runs in equities from the petroleum, finance and consumer Market Capitalization (GH¢ goods sectors saw the annual returns of the broader market 'million) 64,352.42 64,229.12 -0.19% Market Capitalization (US$' inch up to 0.42% last Thursday. Though, most equities gave million) 20,109.50 20,014.06 -0.47% up their opening prices, rise in the market value of Ghana Oil Petroleum Company Limited (GOIL), Societe Generale Ghana Volume traded (shares) 783,118.00 573,274.00 -26.80% Table 1: Market Summary Limited (GOIL) and Fan Milk Limited (FML) were enough to close the week’s activities on a positive note. Key benchmark indices closed the week better despite slight volatilities during inter-day trading. The GSE Composite INDEX ANALYSIS index closed at a year-to-date return of 0.42% whiles the GSE Financial Stocks Index settled at 0.67% returns. INDICATORS Closing Week YTD Level Change CHANGE Total market capitalization of the Ghana Stock Exchange was GH¢64.23 billion, an equivalent to USD20.00 billion. GSE Composite Index 2,270.57 0.42% 0.42% GSE Financial Stocks Index 2,258.77 0.67% 0.67% Table 2: Key Stock Market Indices LIQUIDITY The absence of block trades over the period saw liquidity comparatively down last week. All in all, an approximate figure of 573,274 shares exchanged hands within the first trading week of the year, and was also valued about GH¢2.48 million.