9 Post & Telecommunications

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Public Notice-Merged.Pdf

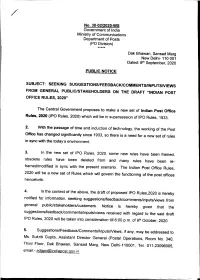

No. 30-02/202 0-ws Government of lndia Ministry of Communications Department of Posts (PO Division) Dak Bhawan, Sansad Marg New Delhi- 110 001 Dated: 8th September, 2020 PUBLIC NOTICE SUBJECT: SEEKtNG suGGEsrloNs/FEEDBAcK/coMMENTS/|NpursrurEWs FROM GENERAL PUBLIC/STAKEHOLDERS ON THE DRAFT "INDIAN POST OFFICE RULES,2020" The central Government proposes to make a new set of lndian post office Rules' 2020 (lPo Rules, 2020) which wiil be in supersession of lpo Rures, 1933. passage 2- with the of time and induction of technorogy, the working of the post office has changed significanfly since 1933, so there is a need for a new set of rules in sync with the today's environment. 3. ln the new set of rpo Rures, 2020. some new rures have been framed, obsolete rules have been dereted from and many rures have been re- framed/modified in sync with the present scenario. The lndian post office Rules, 2020 will be a new set of Rures which wiil govern the functioning of the post offices henceforth. 4. ln the context of the above, the draft of proposed rpo Rures,2020 is hereby notified for information, seeking suggestions/feedbacucomments/inputs/views from general public/stakehorders/customers. Notice is hereby given that the suggestions/feedbacucomments/inputs/views received with regard to the said draft lPo Rules, 2020 will be taken into consideration tilr 6:00 p.m. of 9th october, 2020. 5. Suggestions/Feedback/comments/rnputsA/iews, if any, may be addressed to Ms. Sukriti Gupta, Assistant Director General (postal Operations, Room No. 340, Third Floor, Dak Bhawan, sansad Marg, New Derhi-i10001 , Ter. -

POSTAL SAVINGS Reaching Everyone in Asia

POSTAL SAVINGS Reaching Everyone in Asia Edited by Naoyuki Yoshino, José Ansón, and Matthias Helble ASIAN DEVELOPMENT BANK INSTITUTE Postal Savings - Reaching Everyone in Asia Edited by Naoyuki Yoshino, José Ansón, and Matthias Helble ASIAN DEVELOPMENT BANK INSTITUTE © 2018 Asian Development Bank Institute All rights reserved. First printed in 2018. ISBN: 978 4 89974 083 4 (Print) ISBN: 978 4 89974 084 1 (PDF) The views in this publication do not necessarily reflect the views and policies of the Asian Development Bank Institute (ADBI), its Advisory Council, ADB’s Board or Governors, or the governments of ADB members. ADBI does not guarantee the accuracy of the data included in this publication and accepts no responsibility for any consequence of their use. ADBI uses proper ADB member names and abbreviations throughout and any variation or inaccuracy, including in citations and references, should be read as referring to the correct name. By making any designation of or reference to a particular territory or geographic area, or by using the term “recognize,” “country,” or other geographical names in this publication, ADBI does not intend to make any judgments as to the legal or other status of any territory or area. Users are restricted from reselling, redistributing, or creating derivative works without the express, written consent of ADBI. ADB recognizes “China” as the People’s Republic of China. Note: In this publication, “$” refers to US dollars. Asian Development Bank Institute Kasumigaseki Building 8F 3-2-5, Kasumigaseki, Chiyoda-ku Tokyo 100-6008, Japan www.adbi.org Contents List of illustrations v List of contributors ix List of abbreviations xi Introduction 1 Naoyuki Yoshino, José Ansón, and Matthias Helble PART I: Global Overview 1. -

Advancing Financial Inclusion Through Access to Insurance: the Role Of

Advancing financial inclusion through access to insurance: the role of postal networks Published by the Universal Postal Union (UPU) Berne, Switzerland and by the International Labour Organization (ILO) Geneva, Switzerland. Printed in Switzerland by the printing services of the International Bureau of the UPU. Copyright © 2016 UPU / ILO All rights reserved Except as otherwise indicated, the copyright in this publication is owned by the UPU and the ILO. Reproduction is authorized for non-commercial purposes, subject to proper acknowledgement of the source. This authorization does not extend to any material identified in this publication as being the copyright of a third party. Authorization to reproduce such third party materials must be obtained from the copyright holders concerned. AUTHOR: Guilherme Suedekum TITLE: Advancing financial inclusion through access to insurance: the role of postal networks ISBN: 978-92-95025-84-4 DESIGN: UPU Graphic Unit CONTACT: Nils Clotteau, UPU, [email protected] Craig Churchill, ILO, [email protected] COVER PICTURE: © 2009 Indian Post This study is the result of a joint effort between the International Labour Organization (ILO) and the Universal Postal Union (UPU). It was prepared by Guilherme Suedekum, financial inclusion independent consultant, with the guidance and advice of Craig Churchill, team leader of the ILO’s Impact Insurance Facility, and Nils Clotteau, Acknowledgements Partnerships and Resource Mobilization Expert at the UPU. The team is especially grateful to Dauren Turysbekov, Director of the Department of External Affairs at Kazpost, Michel Kabré, Director of Financial Services at SONAPOST, Titus Juma, Director of Payment Services at the Postal Corporation of Kenya, M’hamed El-Moussaoui, Assistant Director General of Al Barid Bank, and Rajagopal Krishnaswamy, Managing Director at Professional Life Assurance. -

2 A. What Is Money Laundering 2 B. What Is Financing of Terrorism 3 2

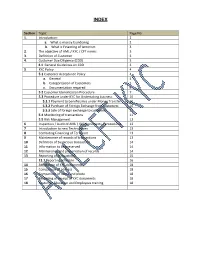

INDEX Section Topic Page No 1. Introduction: 2 a. What is money laundering 2 b. What is Financing of terrorism 3 2. The objective of AML / KYC / CFT norms 3 3. Definition of Customer 3 4. Customer Due Diligence (CDD) 3 4.1 General Guidelines on CDD 3 5 KYC Policy 4 5.1 Customer Acceptance Policy 4 a. General 4 b. Categorization of Customers 5 c. Documentation required 6 5.2 Customer Identification Procedure 7 5.3 Procedure under KYC for Undertaking business 10 5.3.1 Payment to beneficiaries under Money Transfer 10 5.3.2 Purchase of Foreign Exchange from customers 10 5.3.3 Sale of foreign exchange to customers 11 5.4 Monitoring of transactions 11 5.5 Risk Management 12 6 Inspection / Audit of AML \ KYC documents / procedures 13 7 Introduction to new Technologies 13 8 Combating Financing of Terrorism 13 9 Maintenance of records of transactions 13 10 Definition of Suspicious transaction 14 11 Information to be preserved 14 12 Maintenance and preservation of records 14 13 Reporting of transactions 15 13.1 Reporting schedule 16 14 Attestation of KYC documents 18 15 Comparison of address 18 16 Comparison of name and photo 18 17 Recording of receipt of KYC documents 18 18 Customer Education and Employees training 18 Guidelines on Know Your Customer (KYC) Norms / Anti-Money Laundering (AML) Standards / Combating Financing of Terrorism (CFT) Norms under Prevention of Money Laundering Act, PMLA, 2002 as amended by Prevention of Money Laundering (Amendment) Act, 2009 for International Money Transfer Services(Inward) under the Money Transfer Service Scheme (MTSS) and Money Changing Services in India Post 1. -

Logistics System and Process in Express Delivery Service Companies

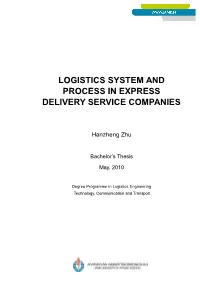

LOGISTICS SYSTEM AND PROCESS IN EXPRESS DELIVERY SERVICE COMPANIES Hanzheng Zhu Bachelor’s Thesis May, 2010 Degree Programme in Logistics Engineering Technology, Communication and Transport DESCRIPTION Author(s) Type of publication Date Bachelor´s Thesis 25/05/2010 Zhu Hanzheng Pages Language 53+7 English Confidential Permission for web ( ) Until publication ( X ) Title LOGISTICS SYSTEM AND PROCESS IN EXPRESS DELIVERY SERVICE COMPANIES Degree Programme Degree Programme in Logistics Engineering Tutor(s) Salmijärvi Olli Assigned by Xi’an Express Mail Service Logistics Company of China Post Abstract Express delivery services (EDS), as a young industry, are currently experiencing a rapid growth to fulfill the increasing demand. With the aims of being fast, safe, controllable and traceable, EDS companies have developed a quite different logistics network and systems in their logistics process. The purpose of this study was to describe EDS network models, like the spoke-hub paradigm, as well as the way of EDS processing. It was also studied how much of advanced and automated technologies and methods, like geographical information system, are used for optimizing the network, accelerating the delivery speed and improving services. The whole logistics chain of EDS was to be presented in this thesis. Express Mail Service (EMS), a large Chinese express delivery corporation, plays an important role in this market. Its significant part, EMS of China Post corporation, is now experiencing hard competition. This thesis went deeper inside the Chinese EMS company and found reasons that have led to competitive advantages and weaknesses through using the SWOT analysis. The research material included a lot of information and data from EMS company and its market and from the author’s internship experience. -

Allocation of Postal Circle to Candidates Recommended by SSC

No. W-04-7/2018-SPB-I Govemment of India Ministry of Communications Department of Posts Dak Bhawan, Sansad Marg New Delhi, dated 11.06.2018 Subject:-Allocation of Postal Circle to candidates recommended by SSC for appointment as Postal Assistant / Sorting Assistant on the basis of Combined Higher Secondary Level Examination, 2016. Attention is invited to Department of Posts letter No. W-04-712017-SPB-I dated 07.03.2018 read with letter dated 14.05.2018 wherein candidates recommended by Staff Selection Commission (SSC), on the basis of Combined Higher Secondary Level (CHSL) Examination,2016, for appointment as Postal Assistant / Sorting Assistant, were advised to submit their preference / option for allocation of Postal Circles by email and Speed Post / Register Post. 2. Although SSC has recommended 3295 candidates for appointment as Postal Assistant / Sorting Assistant on the basis of CHSL Examination,2016; SSC has confirmed nomination of 3215 candidates and their dossiers have been received till date. Postal Circles have been allocated to all 3295 cmdidates, as per the criteria stipulated in aforesaid letter dated 07.03.2018, irrespective of the status of receipt of dossiers in Department of Posts. All those candidates whose dossiers are yet to be forwarded by the SSC, their candidature shall be subject to confirmation of nomination / forwarding of dossiers by SSC and they shall have no claim over the appointment to the said posts in the Department of Posts. Consequently, in case of candidates whose nominations are yet to be confirmed / dossiers are yet to be forwarded by SSC, the appointing authority shall not issue offer of appointment till confirmation of nomination by SSC and receipt of dossiers by Department of Posts. -

Government Response to Self-Determination Movements: a Case Study Comparison in India

GOVERNMENT RESPONSE TO SELF-DETERMINATION MOVEMENTS: A CASE STUDY COMPARISON IN INDIA By Pritha Hariharan Submitted to the graduate degree program in MA Global and International Studies and the Graduate Faculty of the University of Kansas in partial fulfillment of the requirements for the degree of Master of Arts. ________________________________ Chairperson: John James Kennedy ________________________________ Committee Member: MichaelWuthrich ________________________________ Committee Member: Eric Hanley Date Defended: November 18th 2014 The Thesis Committee for Pritha Hariharan certifies that this is the approved version of the following thesis: GOVERNMENT RESPONSE TO SELF-DETERMINATION MOVEMENTS: A CASE STUDY COMPARISON IN INDIA ________________________________ Chairperson: John James Kennedy Date approved: November 18th 2014 ii Abstract The Indian government’s response to multiple separatist and self-determination movements the nation has encountered in its sixty-six year history has ranged from violent repression to complete or partial accommodation of demands. My research question asks whether the central government of India’s response to self-determination demands varies based on the type of demand or type of group. The importance of this topic stems from the geopolitical significance of India as an economic giant; as the largest and fastest growing economy in the subcontinent, the stability of India as a federal republic is crucial to the overall strength of the region. While the dispute between India and Pakistan in the state of Kashmir gets international attention, other movements that are associated with multiple fatalities and human rights abuses are largely ignored. I conduct a comparative case study analysis comparing one movement each in the states of Tamil Nadu, Punjab, Assam, Kashmir, and Mizoram; each with a diverse set of demands and where agitation has lasted more than five years. -

Government of India, Ministry of Communications & IT, Department

Government of India, Ministry of Communications & IT, Department of Posts, Dak Bhawan, Sansad Marg, New Delhi – 110116 Department of Posts has set up Investment Division in Mumbai under the Postal Life Insurance Directorate of the Department for investment of the Post Office Life Insurance Fund (POLIF) and Rural Post Office Life Insurance Fund (RPOLIF). Applications in the prescribed format from eligible candidates are invited for one ex‐cadre post of Chief Investment Officer (HAG level) in the Investment Division to be filled on deputation (ISTC) or contract or absorption from the officers of the Central or State Governments or Union Territories or Universities or recognized research institutions or Public Sectors Undertakings or semi‐governments or statutory or autonomous organizations including banking institutions or financial institutions. Applications in the prescribed format (Annex ‘B’) alongwith copies of all testimonials/ certificates should reach the office of Deputy Director General (Personnel), Department of Posts, Dak Bhawan, Sansad Marg, New Delhi ‐ 110116 within 30 days of publication of this advertisement in the Employment News. No application will be entertained after prescribed time of 30 days. This advertisement can also be viewed on the website of INDIA POST http://www.indiapost.gov.in. The particulars regarding name of the post, remuneration, required qualification, job description are given in Annexure ‘A’. Annexure ‘A’ Sl. Name of Number of Age Limit Pay Band Required qualifications and Job No. Post Post and Grade experience description Pay or Pay Scale 1. Chief One Not HAG Rs. (A) CIO would be Investment applicable 67000‐ i. Holding analogous post on responsible Officer 79000 regular basis in the parent for taking cadre or department; or day‐to‐day ii. -

The Role of Postal Networks in Digital Financial Services

International Telecommunication Union ITU-T FG-DFS TELECOMMUNICATION STANDARDIZATION SECTOR OF ITU (10/2016) ITU-T Focus Group Digital Financial Services The Role of Postal Networks in Digital Financial Services Focus Group Technical Report ITU-T Focus Group Digital Financial Services: The Role of Postal Networks in Digital Financial Services FOREWORD The International Telecommunication Union (ITU) is the United Nations specialized agency in the field of telecommunications, information and communication technologies (ICTs). The ITU Telecommunication Standardization Sector (ITU-T) is a permanent organ of ITU. ITU-T is responsible for studying technical, operating and tariff questions and issuing Recommendations on them with a view to standardizing telecommunications on a worldwide basis. The procedures for establishment of focus groups are defined in Recommendation ITU-T A.7. TSAG set up the ITU-T Focus Group Digital Financial Services (FG DFSs) at its meeting in June 2014. TSAG is the parent group of FG DFS. Deliverables of focus groups can take the form of technical reports, specifications, etc., and aim to provide material for consideration by the parent group in its standardization activities. Deliverables of focus groups are not ITU-T Recommendations. ITU 2016 This work is licensed to the public through a Creative Commons Attribution-Non-Commercial-Share Alike 4.0 International license (CC BY-NC-SA 4.0). For more information visit https://creativecommons.org/licenses/by-nc-sa/4.0/ ITU-T Focus Group Digital Financial Services: The Role of Postal Networks in Digital Financial Services The Role of Postal Networks in Digital Financial Services ITU-T Focus Group Digital Financial Services: The Role of Postal Networks in Digital Financial Services About this Report This Technical Report was written by the following authors, contributors, and reviewers: The authors of this Technical Report are Nils Clotteau, David Avsec and Yury Grin. -

70 POLICIES THAT SHAPED INDIA 1947 to 2017, Independence to $2.5 Trillion

Gautam Chikermane POLICIES THAT SHAPED INDIA 70 POLICIES THAT SHAPED INDIA 1947 to 2017, Independence to $2.5 Trillion Gautam Chikermane Foreword by Rakesh Mohan © 2018 by Observer Research Foundation All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without permission in writing from ORF. ISBN: 978-81-937564-8-5 Printed by: Mohit Enterprises CONTENTS Foreword by Rakesh Mohan vii Introduction x The First Decade Chapter 1: Controller of Capital Issues, 1947 1 Chapter 2: Minimum Wages Act, 1948 3 Chapter 3: Factories Act, 1948 5 Chapter 4: Development Finance Institutions, 1948 7 Chapter 5: Banking Regulation Act, 1949 9 Chapter 6: Planning Commission, 1950 11 Chapter 7: Finance Commissions, 1951 13 Chapter 8: Industries (Development and Regulation) Act, 1951 15 Chapter 9: Indian Standards Institution (Certification Marks) Act, 1952 17 Chapter 10: Nationalisation of Air India, 1953 19 Chapter 11: State Bank of India Act, 1955 21 Chapter 12: Oil and Natural Gas Corporation, 1955 23 Chapter 13: Essential Commodities Act, 1955 25 Chapter 14: Industrial Policy Resolution, 1956 27 Chapter 15: Nationalisation of Life Insurance, 1956 29 The Second Decade Chapter 16: Institutes of Technology Act, 1961 33 Chapter 17: Food Corporation of India, 1965 35 Chapter 18: Agricultural Prices Commission, 1965 37 Chapter 19: Special Economic Zones, 1965 39 iv | 70 Policies that Shaped India The Third Decade Chapter 20: Public Provident Fund, 1968 43 Chapter 21: Nationalisation of Banks, 1969 45 Chapter -

PGPPM Placement Brochure 2020-21

POST GRADUATE PROGRAMME IN PUBLIC POLICY & MANAGEMENT PGPPM 2020-21 ONE-YEAR FULL-TIME RESIDENTIAL MASTER’S PROGRAMME Class of 2021 Contents About IIM Bangalore 1 Director’s Message 2 Message from the Chairperson, Post Graduate Programme in Public Policy and Management 3 Message from the Chairperson, Career Development Services 4 About the Programme 5 List of Core and Elective Courses 6 Class Profile 2021 7 Student Profiles 8 Balasubramanian Navamani 9 Gururaj Laxmi 10 Jayant Shrivastava 11 Narenchoudary Amaraneni 12 Sankalp Abhishek 13 Mohammad Saquib Imran 14 Shivangi Thakur 15 Rishi Kumar 16 Rural Immersion 17 Policy Speakers 18 Policy Blog 19 Faculty Quotes 20 Organizations where PGPPM Alumni Work 22 Recruiter Testimonials 23 Alumni Quotes 24 Placement Process 26 2 About IIM Bangalore Indian Institute of Management Bangalore (IIMB) is a leading graduate school of management in Asia. Under the IIM Act of 2017, IIMB is an Institute of National Importance. IIMB has 150+ faculty members, more than 1200 students across various programmes and nearly 5000 annual Executive Education participants. Our logo carries a proclamation in Sanskrit, (tejasvi navadhitamastu), which translates as ‘let our study be enlightening’. Our vision is to be a global, renowned academic institution fostering excellence in management, innovation and entrepreneurship for business, government and society. Located in India’s high technology capital, IIMB is in close proximity to some of the leading corporate houses in the country, ranging from information technology -

ANSWERED ON:14.12.2016 Task Force on Post Offices Koli Shri Bahadur Singh

GOVERNMENT OF INDIA COMMUNICATIONS LOK SABHA UNSTARRED QUESTION NO:4449 ANSWERED ON:14.12.2016 Task Force on Post Offices Koli Shri Bahadur Singh Will the Minister of COMMUNICATIONS be pleased to state: (a) whether the Government has constituted any special task force to study the use of post office network in the country; (b) if so, the details thereof and the recommendations made by the said task force; (c) whether the Government''s thrust is on increasing PIL business and grab e-commerce bazaar under postal service; (d) if so, the details thereof; and (e) the action taken in this regard? Answer THE MINISTER OF STATE (IC) OF THE MINISTRY OF COMMUNICATIONS & MINISTER OF STATE IN THE MINISTRY OF RAILWAYS (SHRI MANOJ SINHA) (a) & (b) Yes, Madam. A Task Force on Leveraging the Post Office Network was set up under the Chairmanship of Shri T. S. R. Subramanian, retired Cabinet Secretary. The Task Force submitted its recommendations on 4th December, 2014. Recommendations given by the Task Force are at Annexure-A. (c) to (e) Constant efforts are being made by the Government to increase Postal Life Insurance (PLI)/Rural Postal Life Insurance (RPLI) business. It has also focused approach to fulfill the needs of eCommerce sector, and thereby increase its revenue receipts. As a part of strategy to increase its market share and revenue, the Government has rationalized its service offerings. The parcel booking and handling facilities have been upgraded to cater to the expanding eCommerce market. The details of the actions taken to increase the PLI, RPLI and eCommerce are at Annexure-B.