Associated British Ports (“ABP”)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Report-Magazine-Autumn-2019.Pdf

ISSUE NO.11: AUTUMN 2019 04–05 06–07 14 –15 20–23 UK Maritime Minister on London Maritime 2050: turning a British exporters: navigating Brexit-proof: the Port International Shipping Week bold vision into reality a new trading reality of Zeebrugge It’s time to... TURBO--CHARGE TRADE Insight from Britain’s Leading Port Operator 2 REPORT – AUTUMN 2019 REPORT – AUTUMN 2019 3 In this issue Welcome to the Autumn 2019 edition of Report magazine. 04–05 08 –11 20–23 32–33 I am delighted to introduce to you this special UK Maritime Minister It’s time to Brexit-proof: the Port Talking about issue dedicated to London International Also in this issue Shipping Week (LISW) and looking to the on London International turbo-charge trade of Zeebrugge a revolution future of trade. Shipping Week The Government’s intention to In this joint article, Joachim Coens, President Maritime 2050: turning a Among many highlights are a piece by the UK “turbo-charge” the nation’s preparations for CEO at the Port of Zeebrugge, and Patrick Van bold vision into reality Maritime Minister, Nusrat Ghani, discussing UK Maritime Minister Nusrat Ghani MP outlines no deal has been made clear. Whilst leaving Cauwenberghe, Trade Facilitation Director at the Jonathan Spremulli, Principal Director and Head 06–07 the key achievements of the sector and an some of the key features London International the EU without a deal is not a desirable outcome Port of Zeebrugge, examine the port’s trading of the Marine Department at the International — article by the Director for Maritime at the Shipping Week (LISW) visitors can look forward for many, it is vital that British businesses make tradition with the UK and outline steps taken to Chamber of Shipping, looks at the opportunities to this year. -

UK Ports: Delivering a Global Future

ISSUE NO.9: SPRING 2019 08–09 14 –17 18–19 22–23 The Danish connection: ABP sponsors Women in The future of wind Port of Tallinn goes keeping Britain trading Journalism parliamentary reception propulsion technology smart and green 04–07 UK ports: delivering a global future Secretary of State for International Trade, Rt. Hon Dr. Liam Fox MP Insight from Britain’s Leading Port Operator 2 REPORT – SPRING 2019 REPORT – SPRING 2019 3 In this issue Welcome to the Spring 2019 edition of Report magazine. 04–07 08–09 14 –17 18 –19 20– 21 This year’s first issue opens with an article UK ports: delivering The Danish connection: ABP sponsors The future of wind Port of Rotterdam: training by Secretary of State for International Trade, a global future keeping Britain trading Women in Journalism propulsion technology a workforce fit for the Dr Liam Fox MP, who discusses the vital role UK ports continue to play in our national life, parliamentary reception Fourth Industrial Revolution underpinning our current and future prosperity. Secretary of State for International Trade, Rt. Hon HR expert and researcher at the Port of The vital importance of ports is also Dr. Liam Fox MP discusses the vital role ports Trade advisor at the Danish Embassy in the UK, Secretary of International Windship Association Rotterdam, Renee Rotmans, discusses ways in reaffirmed by Danish Embassy Trade Advisor, continue to play in our national identity as Jes Lauritzen, traces the history of the UK and ‘Meet the Women of Westminster’ (IWSA), Gavin Allwright, looks at the latest which the port is focusing on upskilling in order Jes Lauritzen, who shares why ABP’s Ports a great maritime nation. -

Point of Entry

DESIGNATED POINTS OF ENTRY FOR PLANT HEALTH CONTROLLED PLANTS/ PLANT PRODUCTS AND FORESTRY MATERIAL POINT OF ENTRY CODE PORT/ ADDRESS DESIGNATED POINT OF ENTRY AIRPORT FOR: ENGLAND Avonmouth AVO P The Bristol Port Co, St Andrew’s House, Plants/plant products & forestry St Andrew’s Road, Avonmouth , Bristol material BS11 9DQ Baltic Wharf LON P Baltic Distribution, Baltic Wharf, Wallasea, Forestry material Rochford, Essex, SS4 2HA Barrow Haven IMM P Barrow Haven Shipping Services, Old Ferry Forestry material Wharf, Barrow Haven, Barrow on Humber, North Lincolnshire, DN19 7ET Birmingham BHX AP Birmingham International Airport, Birmingham, Plants/plant products B26 3QJ Blyth BLY P Blyth Harbour Commission, Port of Blyth, South Plants/plant products & forestry Harbour, Blyth, Northumberland, NE24 3PB material Boston BOS P The Dock, Boston, Lincs, PE21 6BN Forestry material Bristol BRS AP Bristol Airport, Bristol, BS48 3DY Plants/plant products & forestry material Bromborough LIV P Bromborough Stevedoring & Forwarding Ltd., Forestry material Bromborough Dock, Dock Road South, Bromborough, Wirral, CH62 4SF Chatham (Medway) MED P Convoys Wharf, No 8 Berth, Chatham Docks, Forestry Material Gillingham, Kent, ME4 4SR Coventry Parcels Depot CVT P Coventry Overseas Mail Depot, Siskin Parkway Plants/plant products & forestry West, Coventry, CV3 4HX material Doncaster/Sheffield Robin DSA AP Robin Hood Airport Doncaster, Sheffield, Plants/plant products & forestry Hood Airport Heyford House, First Avenue, material Doncaster, DN9 3RH Dover Cargo Terminal, -

Standards Terms and Conditions of Trade

bylaws, orders, notices, demands, regulations or official guidance issued by any Competent Authority which are applicable to the Customer, the Port and/or any aspect of the performance of these Conditions as the same may be amended or modified from time to time; “Cargo” means cargoes of any description; ASSOCIATED BRITISH PORTS “Cargo Services” means any services provided by, or on behalf of, STANDARD TERMS AND CONDITIONS OF TRADE ABP in relation to the Cargo or Containers including unloading or loading Cargo or Containers from or to Vessel or from or to Customer Transport, handling of Cargo or Containers, management of storage and storage of Cargo or Containers at the Port; IMPORTANT ADVICE “Charges” means all charges, dues, expenses or other sums THE CUSTOMER’S ATTENTION IS DRAWN TO SPECIFIC (including charges for Services, charges for the hire of ABP Plant, CONDITIONS WHICH EXCLUDE OR LIMIT THE LIABILITY OF and dues and charges for Vessels) which are payable by the ABP (INCLUDING CONDITIONS 6.4, 11, 14.1, 16, 18.2, 19.2, 20, Customer to ABP; 22, 23, 24, 25, 26), REQUIRE THE CUSTOMER TO INDEMNIFY OR REIMBURSE ABP IN CERTAIN CIRCUMSTANCES “Competent Authority” means any supranational, national, (INCLUDING CONDITIONS 3.2, 4, 5.3, 6.3, 8.2, 9.3, 10.1, 16, 17, regional, local or municipal government or regulatory authority, body, 18.2, 19.2) AND LIMIT TIME (INCLUDING CONDITION 25) agency, court, ministry, inspectorate or department, or any official, public or statutory person or body, police, customs or port authority, ABP UNDERTAKES NO OBLIGATION TO EFFECT INSURANCE in each case acting in accordance with its or their statutory or legal (AND MAKES NO CHARGE FOR INSURANCE). -

Associated British Ports Port Duty Manager, Southampton

Associated British Ports Port Duty Manager, Southampton Full Time, Permanent Contract Competitive Salary + Excellent Benefits ABP is the UK’s leading port operator, with a unique network of 21 ports across England, Scotland and Wales. Our ports include Immingham, the UK’s busiest port and Southampton, the UK’s leading export port and number one for cars and cruise. The group's other activities include rail terminal operations (Hams Hall Rail Terminal), ship's agency, dredging (UK Dredging Ltd), and marine consultancy (ABPmer). Each port also offers a well-established community of port service providers. Southampton is the UK's number one vehicle handling port, Europe's leading turnaround cruise port and the UK's most productive container port. Operated by DP World Southampton, the terminal is home to the new 500m deepwater quay SCT5, which was purpose built to handle the biggest ships in the world. A major dredging programme ensures that 15.5m draft vessels - the biggest currently afloat - can access the port on most days of the year. The port is less than two miles from the M27 and has direct rail links to the main railway network for both freight and passenger trains. The Port of Southampton is served by Southampton International Airport, while Gatwick and Heathrow airports are within easy reach. The Role We are looking for a Port Duty Manager to manage a team of 5 Service Delivery Operatives and 3 Shift Technicians, being responsible for ensuring the smooth operation of the port. You will lead and motivate the Port Operations Delivery Team to deliver the planned activities of the day, as well as proactively respond to changing circumstances in the port and respond as appropriate. -

Industry Jobs – April 2018

Industry Jobs – April 2018 The following ports industry jobs have been sent to us by our members: Semi-Skilled Engineer – Associated British Ports….………………………..………… 1 Chief Executive – Port of Dover……………………….…………………………………. 3 Port and Harbour Engineer – Port of Ramsgate………….…..………………………… 4 Property Manager – Shoreham Port ……………………………………..……………… 5 The British Ports Association – Speaking for UK Ports a: 1st Floor, 30 Park Street, London SE1 9EQ t: +44 207 260 1780 f: +44 20 3598 1732 e: [email protected] w: www.britishports.org.uk Associated British Ports Semi-Skilled Engineer Full time, Permanent contract Location – Humber Region Competitive Salary + Excellent Benefits Closing Date – 8th May 2018 ABP is the UK’s leading port operator, with a unique network of 21 ports across England, Scotland and Wales. Our ports include Immingham, the UK’s busiest port and Southampton, the UK’s leading export port and number one for cars and cruise. The group's other activities include rail terminal operations (Hams Hall Rail Terminal), ship's agency, dredging (UK Dredging Ltd), and marine consultancy (ABPmer). Each port also offers a well-established community of port service providers. In 2015 ABP and its customers handled 92 million tonnes of cargo. Together with our customers, we support 84,000 jobs and contribute £5.6 billion to the UK economy every year. With the support of our customers, ABP’s Ports on the Humber – Hull, Goole, Grimsby and Immingham - contribute £2.2 billion to the UK economy every year whilst supporting 33,000 jobs and together handling more than 65 million tonnes of cargo. ABP's Humber facilities offer customers close links to markets in mainland Europe and Scandinavia and expertise in a broad range of cargoes, including energy, vehicles, roll-on roll-off, containers, bulks, liquid bulks and forest products. -

MARINE POLICY October 2019

MARINE POLICY October 2019 ABP Marine Policy Revised October 2019 1. Introduction ABP (The Harbour Authority) has developed policies and plans in accordance with the standards set out in the Port Marine Safety Code (PMSC). This document details the policies adopted to achieve the Code’s required standard. The policies and plans are based upon a full assessment of the requirements of the Port Marine Safety Code and the hazards that have to be managed to provide for the marine safety of ABP’s ports and harbours and their users. This document is intended to be read in conjunction with ABP Port Marine Operational Procedures Manuals, which detail how the policies set out in this document will be implemented. These documents, together with other group policies, and local policies and procedures, underpin the ABP Group “Marine Safety Management System” (MSMS). Each section of this policy is cross referenced to the appropriate sections of the current version of Port Marine Safety Code (November 2016), for example (1.1 – 1.5) 2. Accountability for Marine Safety Duties and Powers: ABP as Harbour Authority (1.1 – 1.5) ABP is ultimately owned by ABP (Jersey) Limited, a limited liability company incorporated in Jersey. However, under Part II of the Transport Act 1981 ABP is controlled by Associated British Ports Holdings Ltd (ABPH), a company formed by the Secretary of State. The directors of ABP (of which there must not be less than five or more than thirteen) are appointed by ABPH, but ABPH has no power to give directions to the directors of ABP in respect of the execution of their powers and duties as a Harbour Authority. -

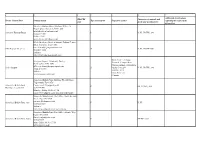

Border Control Post Contact Details TRACES Code Type of Transport

1 2 3 4 5 6 7 Additional specifications TRACES Categories of animals and Border Control Post Contact details Type of transport Inspection centres regarding the scope of the code goods and specifications designation Aberdeen Harbour Board, Harbour Office, 16 Regent Quay, Aberdeen, AB11 5SS [email protected] Aberdeen Harbour Board P P, PP, PP(WP), OO 01224 597000 09:00 - 17:00 www.aberdeen-harbour.co.uk BAA Aberdeen, Aberdeen Airport, Farburn Terrace, Dyce, Aberdeen, AB21 7DU. [email protected] AGS Airport Aberdeen A P, PP, PP(WP),OO 0844 481 6666 24 hours https://www.aberdeenairport.com/ Dnata, Unit 7_8, Cargo Glasgow Airport, Abbotsinch, Paisley, Terminal, Campsie Drive, Renfrewshire, PA3 2SW Glasgow Airport, Abbotsinch, [email protected] AGS Glasgow A Paisley, PA3 2SG P, PP, PP(WP), OO 0844 481 5555 0141 847 4576 24 hours www.dnata.com www.glasgowairport.com 24 hours Associated British Ports Holdings Plc, Old Quay, Teignmouth, TQ14 8ES Associated British Ports [email protected] P PP, PP(WP), OO Holdings, Teignmouth 1626 774044 Monday - Friday 08:30 - 17:00 https://www.abports.co.uk/locations/teignmouth/ Associated British Ports, Port Office, North Harbour Street, Ayr, KA8 8AH [email protected] Associated British Ports, Ayr P P, PP 01292 281687 24 hours https://www.abports.co.uk/locations/ayr Associated British Ports, Port Office, Atlantic Way, Barry, CF63 3US. [email protected] Associated British Ports, Barry P PP(WP), OO 0870609669 Mon - Friday 08:30 - 17:00 www.abports.co.uk -

Annex 06 Humber Final

DEFRA PROJECT FO0108 RESILIENCE OF THE FOOD SUPPLY TO PORT DISRUPTION FINAL ANNEX REPORT 6: IMPORT CORRIDOR: HUMBER September 2012 Peter Baker (PRB Associates Limited) and Andrew Morgan (Global 78 Limited) Contents Section Sub- Title Page section 1 EXECUTIVE SUMMARY 1 2 INTRODUCTION & ACKNOWLEDGEMENTS 2 3 SECTOR OVERVIEW 3 4 PORT DESCRIPTION 6 4.1 Port infrastructure 4.2 Services calling at the port(s) 4.3 Port hinterland 5 PORT TRADE & TRAFFIC 10 5.1 Overall trade and traffic mix 5.2 EU and non EU food imports 6 PORT FLEXIBILITY 13 6.1 Issues and concerns / potential disruption scenarios 6.2 Traffic diversion 6.3 Vessel diversion 7 FOOD SUPPLY RESILIENCE ASSESSMENT 19 8 MESSAGES & FINDINGS 20 Annex 06: Import Corridor: Humber i 1. EXECUTIVE SUMMARY The Humber ports handle 19%, by volume, of all UK maritime imports with high volumes of liquid and dry bulk fuels. Its importance as an entry point for unit load traffic is evident in the fact that 19% of all UK foreign trailer-based imports enter the country through Immingham, Killingholme and Hull. Roughly 11% of the UK’s foreign imports of food come through the range of major Humber ports and smaller terminals and wharves along the River Humber and River Trent, with EU and non EU food imports among the 3.7 million tonnes, being of equal significance compared to the UK’s total food imports from EU and non EU sources (also 11%). The importance of fish imports (mainly in containers), palm oil and sugar is evident. In addition to container loads of fish from Iceland and Norway there are estimated to be 50 containers per week arriving in Immingham from China and the Far East on deep sea feeder services. -

Do You Think the Welsh Government Is Taking a Strategic Approach to Developing the Potential of the Maritime Economy?

Cynulliad Cenedlaethol Cymru National Assembly for Wales Y Pwyllgor Menter a Busnes Enterprise and Business Committee Ymchwiliad i Botensial yr Economi Forol Inquiry into the Potential of the Maritime yng Nghymru Economy in Wales PME 15 PME 15 Cymdeithas Porthladdoedd Prydain Associated British Ports Consultation questions Role of Government Question 1 - Do you think the Welsh Government is taking a strategic approach to developing the potential of the maritime economy? It is widely appreciated that ports are a key part of the supply chain of many large industries in Wales, including steel making, energy production, energy distribution, agriculture, construction and other manufacturing processes. A recent investigation undertaken by Arup (summary attached) indicates that ABP’s ports in South Wales support 15,000 Welsh jobs and contribute over £1bn to the local economy annually. Ports also enable significant value through the potential for regeneration and development of leisure and residential sectors for example Swansea SA1, Barry Waterfront and Cardiff Bay. In addition there are significant opportunities associated with coastal energy projects, wind, tide or wave driven which often require significant port infrastructure for their construction and operation. ABP is encouraged that Welsh Government is focussing on the benefits provided by the maritime sector. ABP would wish to engage closely with WG in respect of inward investment and the potential offered by its strategic land areas on its Port estates and employment sites in close proximity with good access to Ports. Are there any examples of best practice in this area? There are a number of good examples within ABP where cooperation between Government and local authorities has secured significant investment and good quality sustainable employment, for example on the Humber, Greenport Hull is a combined investment in excess of £300m that will provide the offshore wind industry with a manufacturing and logistics hub to feed offshore wind developments in the North Sea. -

Keeping Britain Trading Abp Company Profile

Company Profile KEEPING BRITAIN TRADING ABP COMPANY PROFILE Company background At the heart of international trade Associated British Ports (ABP) is the UK’s leading ABP’s ports serves as vital gateways for international and best-connected port owner and operator, with trade, connecting importers and exporters around a network of 21 ports handling around a quarter of the UK to global markets. the UK’s seaborne trade. By facilitating trade for businesses and manufacturers, ABP’s ports include Immingham, the UK’s largest port by ABP’s ports play an essential role at the heart of the tonnage, and Southampton, the nation’s second largest UK economy, supporting around 120,000 jobs and container port, and the UK’s number one port for cars contributing £7.5 billion to the economy every year. and cruises. Together with its customers, ABP handles around £150 billion of UK trade annually, with £40 billion of UK exports The group’s other activities include rail terminal operations passing through the Port of Southampton, making it the (Hams Hall Rail Freight Terminal), port maintenance UK’s number one export port. and dredging (UK Dredging), and marine and hydrographic consultancy (ABPmer). Each port also offers ABP’s port locations are geographically diverse and well- a well-established community of port service providers. positioned on key global and European trade routes. The ports are located in close proximity to important domestic industrial clusters, logistics hubs and major conurbations. ABP owns a total of 3,743 ha of freehold land, which includes 960 ha of strategic development land in prime locations across the country. -

Ports, Harbours and Commercial Shipping FAQ Document

Humber Management Scheme FAQs – Ports, harbours and commercial shipping Key organisations and involvement in EMS management Associated British Ports (ABP), through the offices of Humber Estuary Services (HES) is the harbour authority for those parts of the Humber, Ouse and Trent as defined in The Humber Navigation Byelaws 1990, the Humber Harbour Reorganisation Scheme 1966, the Humber Conservancy Acts 1852-1907, and the Ouse (lower) improvement Act 1884. This legislation gives the conservancy authority powers for the regulation of the river and traffic in it. The main role of HES is to provide safe navigation for all craft sailing within the confines of ABP- HES harbour jurisdiction and to provide an efficient pilotage service under its remit as Statutory and Competent Harbour Authority. ABP is the beneficial owner of most of the bed and foreshore of the River Humber by virtue of a 999 year lease from the Crown Estate dated 1/1/1869, and bed and foreshore of the rivers Ouse (Skelton Railway Bridge) and Trent (Old Stone Bridge, Gainsborough) 1872 . ABP is also the port operators and harbour authority for the ports of Hull, Grimsby, Immingham and Goole. Associated Petroleum Terminals (APT) is the harbour authority for the 3 facilities which it manages; Immingham Oil Terminal, Immingham Gas Jetty and South Killingholme Jetty. Canal and River Trust (CRT) is main role is as Harbour Authority and as Competent Harbour Authority for pilotage and have responsibility for navigation on the River Ouse from 100 yards below Goole (Skelton) Rail Bridge to Barlby above Selby beyond the Humber Estuary European marine site and upriver of the south side of the stone bridge at Gainsborough on the River Trent (also beyond the marine site limits).