Scale and Regionality of Nonelectric Markets for U.S. Nuclear Light Water Reactors

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MILL RUINS PARK RESEARCH STUDY Expansion of The

MILL RUINS PARK RESEARCH STUDY Expansion of the Waterpower Canal (1885) and Rebuilding of Tailrace Canals (1887-1892) Prepared for Minneapolis Park and Recreation Board 3800 Bryant Avenue South Minneapolis, Minnesota 55409-1029 Prepared by Hess, Roise and Company, Historical Consultants Marjorie Pearson, Ph.D., Principal Investigator Penny A. Petersen Nathan Weaver Olson The Foster House, 100 North First Street, Minneapolis, Minnesota 55401 With curriculum program by Dawn Peterson Ann Ericson May 2003 Expansion of the Waterpower Canal (1885) and Rebuilding of Tailrace Canals (1887-1892) The Construction of the Expanded Waterpower Canal and Rebuilding of the Tailrace Canals By the mid-1880s, the increasing number of mills and the demand for waterpower was jeopardizing the availability of that power, particularly as the height and flow of the Mississippi fluctuated from season to season. In 1883, the Minneapolis Mill Company hired William de la Barre as an engineer and agent for the waterpower works. A number of the mills had installed auxiliary steam engines to supplement the waterpower. Meanwhile De la Barre proposed to solve the waterpower problem by increasing the head and fall available. Working on the West Side canal (Minnesota Historical Society) According to Kane, “De la Barre undertook to deepen the canal and lower the tailraces under his jurisdiction, while the millers promised to lower their wheel pits, tailraces, and headraces. Before the year ended, De la Barre had deepened the canal from 14 to 20 feet and lengthened it from 600 to 950 feet. The expansion increased its flowage capacity from 30 to 40 per cent and raised the water level to produce more power by bring water to the lessees’ wheels at a greater head. -

The Marlboro Mixer

Sept/Oct 2013 Volume 10, Issue 5 The Marlboro Mixer A FREE newsletter for the town of Marlboro, Vermont. 31st Annual Marlboro Community Fair, September 14th!! In this Issue: Marlboro Cares….2 The Fair is almost here! Please join us on Saturday, September 14th. Select Board……….3 This year we are celebrating “The Makers of Marlboro,” all of those Store…………………..3 friends and neighbors who build, create, craft, make, sing, strum, write, Apples………….…….4 repair, harvest, raise, bake, imagine... MES……………………5 Poetry……………..…6 This year we are very glad to have a number of demonstrations of the skill and ingenuity that make Energy……………….6 our Town such a unique place. The Arts & Crafts Tent will host exhibits of wool yarn spinning, toy VPL……………..…….7 making, an oral history, tool sharpening, video productions, and others. Come learn about birds of prey and enjoy a hard cider or maple syrup tasting in the Ag Tent. We encourage everyone to bring flowers, fruits, and vegetables, as well as jams and beers, for display and to enter to win prizes - and entries from all ages are welcome, so please come and bring the best of your harvest. We are glad once again to be hosting a baking contest with prizes donated by King Arthur Flour, with entries being accepted up to 9:30 AM. The stage will be packed with great music all day long, including Rich Grumbine, Singcrony, Michael Hertz, T. Fredric and Lillian Jones, Jesse Lepkoff and friends, the MacArthur Family, Julia Slone, and Red Heart the Ticker. We will have a poetry reading at 3:00 and wrap up the day with A FREE newsletter the Fair Song at 4:00. -

Transportation on the Minneapolis Riverfront

RAPIDS, REINS, RAILS: TRANSPORTATION ON THE MINNEAPOLIS RIVERFRONT Mississippi River near Stone Arch Bridge, July 1, 1925 Minnesota Historical Society Collections Prepared by Prepared for The Saint Anthony Falls Marjorie Pearson, Ph.D. Heritage Board Principal Investigator Minnesota Historical Society Penny A. Petersen 704 South Second Street Researcher Minneapolis, Minnesota 55401 Hess, Roise and Company 100 North First Street Minneapolis, Minnesota 55401 May 2009 612-338-1987 Table of Contents PROJECT BACKGROUND AND METHODOLOGY ................................................................................. 1 RAPID, REINS, RAILS: A SUMMARY OF RIVERFRONT TRANSPORTATION ......................................... 3 THE RAPIDS: WATER TRANSPORTATION BY SAINT ANTHONY FALLS .............................................. 8 THE REINS: ANIMAL-POWERED TRANSPORTATION BY SAINT ANTHONY FALLS ............................ 25 THE RAILS: RAILROADS BY SAINT ANTHONY FALLS ..................................................................... 42 The Early Period of Railroads—1850 to 1880 ......................................................................... 42 The First Railroad: the Saint Paul and Pacific ...................................................................... 44 Minnesota Central, later the Chicago, Milwaukee and Saint Paul Railroad (CM and StP), also called The Milwaukee Road .......................................................................................... 55 Minneapolis and Saint Louis Railway ................................................................................. -

The University of Minnesota Twin Cities Combined Heat and Power Project

001 p-bp15-01-02a 002 003 004 005 MINNESOTA POLLUTION CONTROL AGENCY RMAD and Industrial Divisions Environment & Energy Section; Air Quality Permits Section The University of Minnesota Twin Cities Combined Heat and Power Project (1) Request for Approval of Findings of Fact, Conclusions of Law, and Order and Authorization to Issue a Negative Declaration on the Need for an Environmental Impact Statement; and (2) Request for Approval of Findings of Fact, Conclusion of Law, and Order, and Authorization to Issue Permit No. 05301050 -007. January 27, 2015 ISSUE STATEMENT This Board Item involves two related, but separate, Citizens’ Board (Board) decisions: (1) Whether to approve a Negative Declaration on the need for an Environmental Impact Statement (EIS) for the proposed University of Minnesota Twin Cities Campus Combined Heat and Power Project (Project). (2) If the Board approves a Negative Declaration on the need for an EIS, decide whether to authorize the issuance of an air permit for the Project. The Minnesota Pollution Control Agency (MPCA) staff requests that the Board approve a Negative Declaration on the need for an EIS for the Project and approve the Findings of Fact, Conclusion of Law, and Order supporting the Negative Declaration. MPCA staff also requests that the Board approve the Findings of Fact, Conclusions of Law, and Order authorizing the issuance of Air Emissions Permit No. 05301050-007. Project Description. The University of Minnesota (University) proposes to construct a 22.8 megawatt (MW) combustion turbine generator with a 210 million British thermal units (MMBTU)/hr duct burner to produce steam for the Twin Cities campus. -

HOW to Eat Crabs!

washingtonFAMILY.com JULY 2019 HOW to Eat Crabs! STUDENT-CENTERED LEARNING AT ONENESS-FAMILY SCHOOL Kenwood School Dedicated to Educational Excellence for over 50 years BEFORE & AFTER SCHOOL CARE KINDERGARTEN THRU 6TH GRADE LEARNING • Small class sizes — allows one-on-one instruction with the teacher • Follows and exceeds Fairfax County curriculum • Standardized testing twice a year to evaluate school ability and achievement; no SOL’s • Integration of reading, writing, oral language, phonics, science, social studies, spelling and math • Extracurricular classes in computers, music, gym and Spanish • Manners and strong social skills are developed in everyday interactions Kindergarten cut o November 30th play • On-site gym for indoor exercise Kindergarten • Daily indoor/outdoor free play cut o • Spacious playground November 30th Extras • Daily interactions with your child’s teacher • Invention Convention, Science Fairs, Fall Festival • Children are able to excel at their own pace • Hot catered lunches and snacks provided • Variety of educational fi eld trips throughout the year • Summer / Holiday Camps • Centrally located — minutes from downtown and major highways 703-256-4711 4955 Sunset Lane Annondale, VA [email protected] www.kenwoodschool.com mommy & me JULY 17TH jokes & WEDNESDAY · 11AM COMMUNITY ROOM juggles Enjoy Mommy’s Lounge while your children play and nurture their magical & creative side. Interactive entertainment provided by Mandy Dalton. Enjoy exclusive discounts from retailers and refreshments provided by Starbucks Coffee and Auntie Anne’s Pretzel Perfect/Planet Smoothie I-95 & I-295 | 6800 Oxon Hill Road | (301) 567-3880 | TangerOutlets.com 51488_NAT_Mommy&Me_PrintAd_7x10_FIN.indd 1 6/19/19 1:24 PM CONTENTS JULY 2019 ON THE COVER STUDENTS AT THE ONENESS-FAMILY SCHOOL Keep your child learning all summer long. -

University of Minnesota A..""1Nual Record

UNIVERSITY OF MINNESOTA A..""1NUAL RECORD 1979-80 June 30, 1980 TABLE OF CONTENTS page BOARD OF REGENTS ............................................. 1 OFFICE OF TilE PRESIDENT. • • . • . • . • . • . • . • . • . 3 Office of Equal Opportunity and Affirmative Action ......• 4 University Relations . • . • . • . • . • . 5 University of Minnesota, Duluth ..............•.....•...•. 6 School of Business and Economics ...........•.....•.... 8 College of Education ...•....•.......•..•••...•........ 10 School of Fine Arts . • . • . • . • . 12 College of Letters and Science .......••.•.•.••......•. 14 School of Medicine •.•....•....••..•.•.......•...•....• 16 School of Social Development ••..•..••.•..••.....•..•.. 17 University of Minnesota, Morris ...•...•.•.....•....•..... 19 University of Minnesota Technical College, Crookston ...•. 21 University of Minnesota Technical College, Waseca .•...... 24 DIVISIONS OF ACADEMIC AFFAIRS ...•.•••....•..•......•...•.•.. 26 Institute of Agriculture, Forestry, and Home Economics ... 27 College of Agriculture • • . • . • • . • . • • . • . 28 College of Forestry •..............•....•••••.......... 29 College of Home Economics . • . • . • . • . • . • • . • . • . 30 Agricultural Experiment Station ........•••••.........• 31 Agricultural Extension Service ..•••......••...•....•.• 32 College of Biological Sciences ..•...•.......•............ 33 College and Graduate School of Business Administration ... 34 Continuing Education and Extension ...•...•.•....•.•.....• 36 College of Education ...............••.•.....••..•..•....• -

The Wingfoot Clan - August 4, 1966 - Page 3

.... - .......·-· , z <1,; .... I.042,'-•L.,· .042042·042.... - - ./1.- 1·415 -<&2:- ./ I ...... + 2./1 "ING= :•CIT<1••tr:SrA r• LAN 1'' I '4 I ' ..1 '1 t*» ., « Ii U Y,9'* TH" 0/' EAR TIRE & RUBBER COMPANY AKRON EDITION ..»7 *f 44 ** V 01. 5 Akron, Ohio (3.-ti•ip August 4, 1966 No.31 :<fi) -- S THIS THE CLUB? Pam- e Moore ponders as she Teys a big problem - how 'e:...v» . Sales & Earnings Again get this giant ball in the - . .... 4....'::, " Pamela is just one of I + 07:, empl()yes' children to : n a weekly Rolf ..r. - .... e the others and Top All Previous Records /./. 4 2 2 b problems, turn .. ,'. The highest sales and earnings in history Goodyear's record quarterly earnings of •lit . 1- $33,589,000 were equivalent to 93 cents a ..'-34 i: .4/. -- were achieved by Goodyear during the first + - 1 - .- .-1-&44-.00 . I i .-'.*6 9, ..G.-.-'1•.1.•=••'- .... 4**4 42.4.-. six months and the second quarter of 1966, share, based on 35,792,174 shares outstand- ing June 30, 1966. They were 17.4 per cent \ 1.A- Russell DeYoung, chairman and chief ex- ,/). 6-... ecutive officer, announcd. higher than the $28,606,000, or 80 cents a share, recorded in the second quarter of 1965. Spurred by gains in virtually all lines of 1 The previous record for quarterly earnings " .'*V- ........ activity worldwide, the company recorded 41 I. was $31,215,000, achieved in the last three • six-month sales of $1,220,472,000 and net aA months of 1965. -

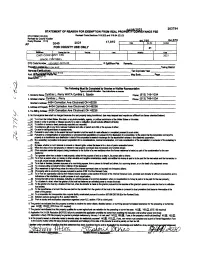

04/08/2021 Year Countynumber 31 Number

263794 STATEMENT OF REABON FOR EXEMPTION FROM REAL PROP#RfauyANCE FEE OTE FORM 100 (EX) RevII,d Code Sections 319.202 and 319.54 (G) (3) Revisid by County Auditor Dusty Rhodes 11/12 66.760 84,570 2021 17,810 1 D- Co. la Numbs, AF 3040 1 FOR COUNTY USE ONLY 31 A66.. T.Ung Dlet No. Tax 1* Bulldng Total CINTI CORP-(INTI CSD 2021 SPAnf CYNTHIA L DTE Code Number 180-OA81-0075-00 0 SPHUNew Plat Remalks: ROP|*198»'.MKFION A\/F Taxing District Narne®Xem,plicate Tax Duplicate Year Acct. 8*611TigAUFT E Map Book page Descrl;RETTI (9 Thi Following Must BI Compl,tod by Grantee or Hls*Her Represintatlve Typs orpIN d In#Innalon. 5,0 In#„EASons on Mine. 1, Grantofs N,ne: Cynthia L. Perry WATA Cynnla L. Spade Phone: (513) 748-1034 2. Grant,0'8 Name: Cynthia L. Perry Phone: (513) 748-1034 Gran*8 Addross: 4434 Camation Ave Cincinnati OH 45238 3. Address 01 Plopelly: 4434 Camation Ave Cincinnati OH 45238 4, Tax ailing Addis: 4434 Carnation Ave Cincinnati OH 45238 5. No Convoyance 100, shall be charged because the real prope,4 being hnsferred: (wo mq request and requirl an amdavlt on lms checked below) Us) To or frorn 08 United Stilm, thts state, or any hamentality, agincy, or pollocal subdlviston of the llilted Stat,6 or thls :tate; h _lb) Soldyin order to providior Mloase secl*lor a debt or obllgaion; (muillneludiamdevitoffhc,1) 1(c) To con#trn or correct a deed previously execulid and recorded; A _(d) To evidence 8 glft, in any fonn, beh,-n husband and w#B, or parent and dilld or tte spouse of •1er; _(0) Onsalifor delinqulnt lax,8 or.,omment,; _(f) Pursuant to court order, to #te dint thst such *slw 18 noi the muit of a sale ellegled or complet,d purtuant to such order; Ug) Pursuant toi leargankation of corporabs or uninootporatidis,ociations or pursuarito the (Ns,oh*on of a corporadon, to the e,dent that the corporation COrNeys the 0'\ properly to a stocltolder as a ¢1*lbudon in Idnd of the corpor@Uon's assets in exchange for the *dholder's shares In the dissolved corpor:San; _(Jt) By asublidiary , . -

Sales by Date 2020

Sales By Sale Date - 2020 Date Owner Address Sale Price GPIN 01/02/2020 JI CHENG REALTY INC 736 MERRIMAC TRL $465,000 F14d-3352-1091 01/02/2020 BEASLEY TERRELL P & ASHANTI S 124 LEWIS DR $385,000 T08b-2783-4727 01/02/2020 ZAVALA MIGUEL & BARBARA A 115 STAGECOACH WATCH $199,900 S06a-0379-4281 01/02/2020 AMAYA RODOLFO SARMIENTO 146 RUSTLING OAK RDG $210,000 S06a-0074-3540 01/02/2020 JONES STEPHANIE & CHRISTOPHER W 102 MIMADO CT $374,000 S04c-0080-0035 01/02/2020 KIMBRELL MICHAEL R & CASSANDRA A 316 KANAWAH RUN $590,000 V03c-0168-0032 01/02/2020 GARCIA TERESA & ERICK 220 GALTS MILL ARCH $459,990 H14c-1630-1814 01/02/2020 KEYSTONE HOMES CORPORATION 207 WROUGHT IRON BND $151,291 T02d-4740-1352 01/03/2020 MCQUIGG ZACHARY W 106 TRIVALON CT $250,000 S03c-2037-1610 01/03/2020 RALLS DEAN S & CHARLENE J 206 PRINCE HENRY CT $378,000 V02b-4417-3101 01/03/2020 HENDERSON JAMES JR & DONNA J 1003 MARQUIS PKWY $293,490 I13c-0158-0859 01/03/2020 HARRAH BENJAMIN A 217 CAROL DR $186,000 R07b-4566-3538 01/06/2020 SAUER WAYNE M & BRENDA R ROBBINS 513 CAROLINE CIR $385,000 D16c-1925-0946 01/06/2020 CAMPBELL RONEY L JR & SONIA M 105 KELLY ST $249,900 O11a-0270-4907 01/06/2020 HALL RONALD & CAROLE 402 YORK WARWICK DR $521,900 Q09c-1270-0530 01/06/2020 FISHER WILLIAM W & INA F 227 TIMBERLINE LOOP $169,500 S06a-0475-2805 01/06/2020 PAJEVIC ZORAN & BILJANA SOLDO 101 ADELE CT $330,000 S03d-4400-0318 01/06/2020 MOTRENKO MAKSIM 327 CLEMENTS MILL TRCE $255,225 H13a-1679-4769 01/06/2020 WALKER CECIL L & THERESA A 304 YORK WARWICK DR $266,000 Q09c-1485-0803 01/06/2020 -

Horticultural Studies 1998 John R

University of Arkansas, Fayetteville ScholarWorks@UARK Research Series Arkansas Agricultural Experiment Station 5-1-1999 Horticultural Studies 1998 John R. Clark University of Arkansas, Fayetteville Michael D. Richardson University of Arkansas, Fayetteville Follow this and additional works at: https://scholarworks.uark.edu/aaesser Part of the Agronomy and Crop Sciences Commons, and the Horticulture Commons Recommended Citation Clark, John R. and Richardson, Michael D., "Horticultural Studies 1998" (1999). Research Series. 137. https://scholarworks.uark.edu/aaesser/137 This Report is brought to you for free and open access by the Arkansas Agricultural Experiment Station at ScholarWorks@UARK. It has been accepted for inclusion in Research Series by an authorized administrator of ScholarWorks@UARK. For more information, please contact [email protected], [email protected]. HORTICULTURAL STUDIES 1998 Edited by John R. Clark and Michael D. Richardson ARKANSAS AGRICULTURAL EXPERIMENT STATION Division of Agriculture University of Arkansas May 1999 Research Series 466 Editing and cover design by Karen Eskew Arkansas Agricultural Experiment Station, University of Arkansas Division of Agriculture, Fayetteville. Milo J. Shult, Vice President for Agriculture and Director; Charles J. Scifres, Associate Vice President for Agriculture. PS1.20599PM65.The Arkansas Agricultural Experiment Station follows a nondiscriminatory policy in programs and employment. ISSN:0099-5010 CODEN:AKAMA6 HORTICULTURAL STUDIES 1998 John R. Clark, editor Associate Professor Horticulture University of Arkansas Michael D. Richardson, editor Assistant Professor Horticulture University of Arkansas Arkansas Agricultural Experiment Station Fayetteville, Arkansas 72701 PREFACE This initial volume of Horticultural Studies reports results of numerous investiga- tions on a range of horticultural crops in Arkansas. This publication is intended to give the reader increased information on current activities underway in the Division of Ag- riculture in the area of horticulture and its many related disciplines. -

Annual Progress/Final Progress Report Format

Annual Report 2011: Hard Cider Carol Miles, Jonathan Roozen, Andrew Zimmerman, Karen Hasenoehrl, and Jacqueline King WSU Mount Vernon NWREC 16650 State Route 536, Mount Vernon, WA 98273 Tel. 360-848-6150 Email [email protected] http://maritimefruit.wsu.edu/ TITLE : Evaluation of Apple Varieties for Hard Cider Production PERSONNEL: Carol A. Miles, Vegetable Extension Specialist, WSU Mount Vernon NWREC Jonathan Roozen, Associate in Research, WSU Mount Vernon NWREC Jacqueline King, Technical Assistant, WSU Mount Vernon NWREC Karen Hasenoehrl, Technical Assistant, WSU Mount Vernon NWREC Andrew (Drew) Zimmerman, Tulip Valley Vineyard and Orchard, 16163 State Route 536, Mount Vernon, WA 98273 OBJECTIVES: 1. To evaluate certain hard cider apple varieties and determine bloom dates, fruit set, and juice characteristics (brix, pH, percent acid, percent tannin) in northwest Washington. 2. To test mechanical harvest of cider apples with a berry harvester and evaluate impact on fruit yield and quality. SUMMARY: Bottling of 2 cider apples harvested in 2010 was done in January 2011, and 9 cider apple varieties were harvested and pressed for cider making in 2011; they will be bottled Spring 2012. Observations of bloom time and bloom density of 62 cultivars were recorded in April-May 2011. At harvest, juice samples were collected from 59 cider apple varieties grown at WSU Mount Vernon NWREC, and analyzed for percent tannin, brix, pH and titratable acid. A replicated trial comparing machine harvest of cider apples with hand harvest was conducted on October 25, 2011. Cider School courses were conducted at WSU Mount Vernon NWREC by the Northwest Agriculture Business Center; introductory courses were held June 27-July 1 and December 12-16, 2011. -

Pioneer1939.Pdf

* * * * Member 1938-39 * :\ r i:::vl.BER S OUTll ER:-1 f NTERSCllOLASTIC * Piu:ss : \ ss<KIATIOX * * * * * * * * * * Clay Model by \ .AN GnvER * Photograph by \Vooo EX * L BR IS * * .. ,. .. ~ '5> ..... PYJU<.;llT , . co , C u EWNINt. Sui::AH AN H1; 1. i:::-r Editor KJ::ISTER GREJ::R . Busmns. Ma11age1 . 0 1195 03350934 if{,> l . r. The 1939 ;onE-E~ * * * * * * EDICftTIOn T o the student of the past who helped to make the traditions of our school what ther are today; to the student of the present who is pro udly loyal to those ideals, e,·er seeking to maintain and ath·ancc them; to the student of the future who will con tinue to carry o n in t he same trustwo rthy manner, we wish to pay tribute by dedicating this 1939 Edition of T11~ ProNEER. Clo\' .\/odt'ls by \·Ax GELDER · Pliutogropli by \\'oou * * * * * * * * * * * * * * * ... _ _ O~EWOfZD M ASTERPif.CES of art in sculpture and painting ha,·c been produced throughout the :igcs which perpetuate for the world great moments - moments of glory or moments of suffering which s tir the human soul. \·erses ha,·e been written and melodics created "·hich inspire the sou l of man to noble thoughts an<l actions. Books ha,·e been written which immortalize great mo ments in the histo ry of mankind. \\·c, TIII·: PIO>.:"EER STAFF, have sought to capture and record for you, the students of Andrew Lewis High School, t h e rapture o f such a moment a moment which you yourseh·es have made as you went on "striving, seeking, finding," each day.