1995 Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Southwest Airlines 1996 Annual Report

1996 Annual Report TABLE OF CONTENTS Consolidated Highlights 2 Introduction 3 Letter to Shareholders 4 People and Planes 6 Southwest Spirit 8 THE Low Fare Airline 10 Productivity 12 Ontime Performance 14 Customer Satisfaction 16 Mintenance and Safety 18 What’s Next? 20 Financial Review 22 Management’s Discussion and Analysis 22 Consolidated Financial Statements 31 Report of Independent Auditors 49 Quarterly Financial Data 50 Common Stock Price Ranges and Dividends 50 Corporate Data 51 Directors and Officers 52 Ten Year Summary 55 CONSOLIDATED HIGHLIGHTS (DOLLARS IN THOUSANDS PERCENT EXCEPT PER SHARE AMOUNTS) 1996 1995 CHANGE Operating revenues $3,406,170 $2,872,751 18.6 Operating expenses $3,055,335 $2,559,220 19.4 Operating income $350,835 $313,531 11.9 Operating margin 10.3% 10.9% (0.6)pts. Net income $207,337 $182,626 13.5 Net margin 6.1% 6.4% (0.3)pts. Net income per common and common equivalent share $1.37 $1.23 11.4 Stockholders’ equity $1,648,312 $1,427,318 15.5 Return on average stockholders’ equity 13.5% 13.7% (0.2)pts. Debt as a percentage of invested capital 28.3% 31.7% (3.4)pts. Stockholders’ equity per common share outstanding $11.36 $9.91 14.6 Revenue passengers carried 49,621,504 44,785,573 10.8 Revenue passenger miles (RPMs)(000s) 27,083,483 23,327,804 16.1 Available seat miles (ASMs)(000s) 40,727,495 36,180,001 12.6 Passenger load factor 66.5% 64.5% 2.0 pts. Passenger revenue yield per RPM 12.07¢ 11.83¢ 2.0 Operating revenue yield per ASM 8.36¢ 7.94¢ 5.3 Operating expenses per ASM 7.50¢ 7.07¢ 6.1 Number of Employees at yearend 22,944 19,933 15.1 NET INCOME (in millions) $207 $179 $183 250 $154 200 $97 150 100 50 0 1992 1993 1994 1995 1996 2 NET INCOME PER SHARE $1.37 $1.22 $1.23 1.40 $1.05 1.20 1.00 $.68 0.80 0.60 0.40 0.20 0.00 1992 1993 1994 1995 1996 SOUTHWEST AIRLINES CO. -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

David Neeleman

David Neeleman David Neeleman is that rarest of entrepreneurs, a man who has created and launched four successful, independent airlines, including the USA’s JetBlue and Morris Air, Canada’s WestJet and Brazil’s Azul. Azul, just seven years old, has already boarded tens of millions of customers. Born in Brazil while his father was Reuter’s São Paulo Bureau Chief, David has always had a deep love for the country. After his family moved to Utah while he was still a child, David would return to Brazil many times throughout his life. A dual citizen, David today relishes the dream before him to make flying cheaper and easier for Brazilians, giving access to air travel for many who have never experienced the opportunity before. Azul serves more than 100 destinations with an operating fleet of more than 140 aircraft, including Brazilian-built Embraer E-190 and E-195 jets, and ATR-72s. Just as JetBlue in the US before it, Azul is the first airline in Latin America to offer LiveTV inflight TV programming via satellite. It has been named Best Low Cost Airline in South America for the last five years at the Skytrax World Airline Awards. In June 2015, it was announced that the Gateway consortium, led by David, had won the bidding to acquire a stake in Portugal’s national carrier TAP. Gateway’s investment represents 50% of the airline. With the new investment, TAP is taking delivery of A330s and inaugurated new daily service from both Boston’s Logan airport and New York’s John F Kennedy International in June and July, respectively. -

Save a Turbine Engine: Serve It Water

Clare Leavens Award Joe Chase Award Aviall High Achievement Award Transport Canada Approved for R/T Save a turbine engine: serve it water Minimum equipment lists and dispatch deviation guides PAMA and AME news February -March 2015 Volume 13/Issue 5 Publication Mail Agreement No. 0041039024 and Return Undeliverable Canadian Addresses to Alpha Publishing Group (2004) Inc. Unit 7, 11771 Horseshoe Way, Richmond, BC, V7A 4V4 email: [email protected] $7.95 AMU-OFC-IFC.indd 1 1/29/15 7:28 PM AMU-OFC-IFC.indd 2 1/29/15 7:28 PM In perspective: Departments the P&WC PT6 nd here some of you thought Gran- 4 Upcoming Events dad put a lot of miles and years on his good ol’ Harley Flathead 45. Hah! 6 STCs & New Products AThat was nothing. Pratt & Whitney Canada 8 Industry Forum recently tweeted out that its venerable PT6 turbine has now clocked 400 million hours 20 AME Association of flight operation. and PAMA News Four hundred million! What does that 39 Classified even mean? Let’s calculate (roughly): There are 8,760 hours in any 365-day year. Di- 42 AMU Chronicles vide 400 million by 8,760 and you get By Sam Longo 45,662.100456621. Round that number off — without fac- toring in Leap, Aztec or dog years (this is al- Features ready getting too complicated for my lousy math)—and you’re now standing at 46,000 10 subscribe and download at www.amumagazine.com AMU is viewable online: years of service. Did I just do that right? As- Save a Turbine Engine: Serve it Water 10 suming I did (and that’s a big ask, I know) By Mike Broderick then we can break down that history into bite-sized pieces. -

Adaptive Connected.Xlsx

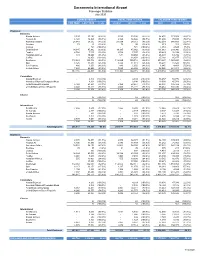

Sacramento International Airport Passenger Statistics July 2020 CURRENT MONTH FISCAL YEAR TO DATE CALENDAR YEAR TO DATE THIS YEAR LAST YEAR % +/(-) 2020/21 2019/20 % +/(-) 2020 2019 % +/(-) Enplaned Domestic Alaska Airlines 3,593 33,186 (89.2%) 3,593 33,186 (89.2%) 54,432 173,858 (68.7%) Horizon Air 6,120 14,826 (58.7%) 6,120 14,826 (58.7%) 31,298 75,723 (58.7%) American Airlines 28,089 54,512 (48.5%) 28,089 54,512 (48.5%) 162,319 348,689 (53.4%) Boutique 79 95 (16.8%) 79 95 (16.8%) 613 201 205.0% Contour - 721 (100.0%) - 721 (100.0%) 4,461 2,528 76.5% Delta Airlines 14,185 45,962 (69.1%) 14,185 45,962 (69.1%) 111,063 233,946 (52.5%) Frontier 4,768 7,107 (32.9%) 4,768 7,107 (32.9%) 25,423 38,194 (33.4%) Hawaiian Airlines 531 10,660 (95.0%) 531 10,660 (95.0%) 26,393 64,786 (59.3%) Jet Blue - 16,858 (100.0%) - 16,858 (100.0%) 25,168 85,877 (70.7%) Southwest 112,869 300,716 (62.5%) 112,869 300,716 (62.5%) 899,647 1,963,253 (54.2%) Spirit 8,425 11,318 (25.6%) 8,425 11,318 (25.6%) 38,294 15,526 146.6% Sun Country 886 1,650 (46.3%) 886 1,650 (46.3%) 1,945 4,401 (55.8%) United Airlines 7,620 46,405 (83.6%) 7,620 46,405 (83.6%) 98,028 281,911 (65.2%) 187,165 544,016 (65.6%) 187,165 544,016 (65.6%) 1,479,084 3,288,893 (55.0%) Commuters Alaska/Skywest - 4,304 (100.0%) - 4,304 (100.0%) 36,457 50,776 (28.2%) American/Skywest/Compass/Mesa - 8,198 (100.0%) - 8,198 (100.0%) 18,030 45,781 (60.6%) Delta/Skywest/Compass 5,168 23,651 (78.1%) 5,168 23,651 (78.1%) 62,894 146,422 (57.0%) United/Skywest/GoJet/Republic 4,040 16,221 (75.1%) 4,040 16,221 (75.1%) -

FY20 Main Stats- Adaptive Connected.Xlsx

Sacramento International Airport Passenger Statistics April 2020 CURRENT MONTH FISCAL YEAR TO DATE CALENDAR YEAR TO DATE THIS YEAR LAST YEAR % +/(-) 2019/20 2018/19 % +/(-) 2020 2019 % +/(-) Enplaned Domestic Alaska Airlines 254 28,618 (99.1%) 224,058 220,143 1.8% 47,617 78,326 (39.2%) Horizon Air 930 9,009 (89.7%) 83,551 91,930 (9.1%) 19,285 37,628 (48.7%) American Airlines 5,310 48,633 (89.1%) 409,920 487,335 (15.9%) 107,335 187,996 (42.9%) Boutique 33 - 0.0% 749 - 0.0% 265 - 0.0% Contour - 356 (100.0%) 12,339 356 3366.0% 4,461 356 1153.1% Delta Airlines 3,279 32,727 (90.0%) 326,111 320,143 1.9% 80,412 114,168 (29.6%) Frontier 377 4,882 (92.3%) 57,938 38,146 51.9% 17,415 15,939 9.3% Hawaiian Airlines - 10,114 (100.0%) 88,524 76,513 15.7% 25,862 33,152 (22.0%) Jet Blue 200 10,670 (98.1%) 108,591 118,825 (8.6%) 24,751 38,730 (36.1%) Southwest 17,308 288,513 (94.0%) 2,416,279 2,754,196 (12.3%) 650,717 1,066,115 (39.0%) Spirit 306 - 0.0% 95,033 - 0.0% 27,531 - 0.0% Sun Country - - 0.0% 13,538 - 0.0% 526 - 0.0% United Airlines 1,694 44,250 (96.2%) 328,432 409,471 (19.8%) 81,057 141,974 (42.9%) 29,691 477,772 (93.8%) 4,165,063 4,517,058 (7.8%) 1,087,234 1,714,384 (36.6%) Commuters Alaska/Skywest 1,124 8,489 (86.8%) 74,773 85,618 (12.7%) 30,401 33,050 (8.0%) American/Skywest/Compass/Mesa 17 5,226 (99.7%) 62,461 66,389 (5.9%) 18,030 21,698 (16.9%) Delta/Skywest/Compass 1,669 20,212 (91.7%) 178,479 198,099 (9.9%) 49,697 74,471 (33.3%) United/Skywest/GoJet/Republic 616 15,458 (96.0%) 111,450 135,979 (18.0%) 28,937 53,523 (45.9%) 3,426 49,385 -

U.S. Department of Transportation Federal

U.S. DEPARTMENT OF ORDER TRANSPORTATION JO 7340.2E FEDERAL AVIATION Effective Date: ADMINISTRATION July 24, 2014 Air Traffic Organization Policy Subject: Contractions Includes Change 1 dated 11/13/14 https://www.faa.gov/air_traffic/publications/atpubs/CNT/3-3.HTM A 3- Company Country Telephony Ltr AAA AVICON AVIATION CONSULTANTS & AGENTS PAKISTAN AAB ABELAG AVIATION BELGIUM ABG AAC ARMY AIR CORPS UNITED KINGDOM ARMYAIR AAD MANN AIR LTD (T/A AMBASSADOR) UNITED KINGDOM AMBASSADOR AAE EXPRESS AIR, INC. (PHOENIX, AZ) UNITED STATES ARIZONA AAF AIGLE AZUR FRANCE AIGLE AZUR AAG ATLANTIC FLIGHT TRAINING LTD. UNITED KINGDOM ATLANTIC AAH AEKO KULA, INC D/B/A ALOHA AIR CARGO (HONOLULU, UNITED STATES ALOHA HI) AAI AIR AURORA, INC. (SUGAR GROVE, IL) UNITED STATES BOREALIS AAJ ALFA AIRLINES CO., LTD SUDAN ALFA SUDAN AAK ALASKA ISLAND AIR, INC. (ANCHORAGE, AK) UNITED STATES ALASKA ISLAND AAL AMERICAN AIRLINES INC. UNITED STATES AMERICAN AAM AIM AIR REPUBLIC OF MOLDOVA AIM AIR AAN AMSTERDAM AIRLINES B.V. NETHERLANDS AMSTEL AAO ADMINISTRACION AERONAUTICA INTERNACIONAL, S.A. MEXICO AEROINTER DE C.V. AAP ARABASCO AIR SERVICES SAUDI ARABIA ARABASCO AAQ ASIA ATLANTIC AIRLINES CO., LTD THAILAND ASIA ATLANTIC AAR ASIANA AIRLINES REPUBLIC OF KOREA ASIANA AAS ASKARI AVIATION (PVT) LTD PAKISTAN AL-AAS AAT AIR CENTRAL ASIA KYRGYZSTAN AAU AEROPA S.R.L. ITALY AAV ASTRO AIR INTERNATIONAL, INC. PHILIPPINES ASTRO-PHIL AAW AFRICAN AIRLINES CORPORATION LIBYA AFRIQIYAH AAX ADVANCE AVIATION CO., LTD THAILAND ADVANCE AVIATION AAY ALLEGIANT AIR, INC. (FRESNO, CA) UNITED STATES ALLEGIANT AAZ AEOLUS AIR LIMITED GAMBIA AEOLUS ABA AERO-BETA GMBH & CO., STUTTGART GERMANY AEROBETA ABB AFRICAN BUSINESS AND TRANSPORTATIONS DEMOCRATIC REPUBLIC OF AFRICAN BUSINESS THE CONGO ABC ABC WORLD AIRWAYS GUIDE ABD AIR ATLANTA ICELANDIC ICELAND ATLANTA ABE ABAN AIR IRAN (ISLAMIC REPUBLIC ABAN OF) ABF SCANWINGS OY, FINLAND FINLAND SKYWINGS ABG ABAKAN-AVIA RUSSIAN FEDERATION ABAKAN-AVIA ABH HOKURIKU-KOUKUU CO., LTD JAPAN ABI ALBA-AIR AVIACION, S.L. -

Redalyc.Engineering and Strategy: Returning to the Case of Southwest

Revista Escuela de Administración de Negocios ISSN: 0120-8160 [email protected] Universidad EAN Colombia Berrío Zapata, Cristian Engineering and strategy: returning to the case of southwest airlines, an analysis in production and technology management Revista Escuela de Administración de Negocios, núm. 73, julio-diciembre, 2012, pp. 209-217 Universidad EAN Bogóta, Colombia Available in: http://www.redalyc.org/articulo.oa?id=20625032013 How to cite Complete issue Scientific Information System More information about this article Network of Scientific Journals from Latin America, the Caribbean, Spain and Portugal Journal's homepage in redalyc.org Non-profit academic project, developed under the open access initiative Casos empresariales ENGINEERING AND STRATEGY: RETURNING TO THE CASE OF SOUTHWEST AIRLINES, AN ANALYSIS IN PRODUCTION AND TECHNOLOGY MANAGEMENT Cristian Berrío Zapata 1. INTRODUCTION ome company cases let us see what was a network that makes every part of it shake, when any done to produce business model innovation component is touched. This network, immersed into Sthat creates ruptures in the market, changing the environment evolution, is a complete systemic the rules of competition. One of these cases is the unit, where paradigm changes must be supported with story of Southwest Airlines (SWA). This article tries to operational actions so innovation becomes a living demonstrate that engineering operational excellence is force that changes competing profiles. This virtuous fruitless without a compatible moving in other conceptual cycle between thought and action, when successful axes like service, finances, administration and human in producing adaptative and innovative competing resources. The areas of a company are bounded into structures, revolves the markets and generates new rules for competition. -

2013 Jetsuite

JetSuite’s vision to provide the freedom and exhilaration of private air travel to more people than ever is realized through efficient operations, acute attention to detail, acclaimed customer service, and industry-leading safety practices. And JetSuite continues to be the only jet charter company to guarantee its instant, online quotes for its fleet of WiFi-equipped JetSuite Edition CJ3 and Phenom 100 aircraft. Refreshingly transparent! ©©2013 2014 JetSuiteJetSuite || jetsuite.com JetSuite.com THE EXECUTIVE TEAM ALEX WILCOX, CEO With over two decades of experience in creating highly innovative air carriers in ways that have improved air travel for millions, Alex Wilcox now serves as CEO of JetSuite – a private jet airline which launched operations in 2009. In co-founding JetSuite in 2006, Alex brought new technology and unprecedented value to an industry in dire need of it. JetSuite is a launch customer for the Embraer Phenom 100, an airplane twice as efficient and more comfortable than other jets performing its missions, as well as the JetSuite Edition CJ3 from Cessna. Also a founder of JetBlue, Alex was a driving force behind many airline industry changing innovations, including the implementation of live TV on board and all-leather coach seating. Alex was also named a Henry Crown Fellow by the Aspen Institute. KEITH RABIN, PRESIDENT AND CHIEF FINANCIAL OFFICER With a background that spans over a decade in the financial services and management consulting industries, Keith Rabin has served as President of JetSuite since 2009. Prior to co-founding JetSuite, Keith was a Partner at New York based hedge fund Verity Capital, where he was responsible for portfolio management and the development of Verity’s sector shorting strategy. -

Biz Tips: Know Your End-Game Sunday, October 31, 2004 by Art Hill

BIZTIPS - October 31, 2004 Biz Tips: Know Your End-Game Sunday, October 31, 2004 By Art Hill Like the world champion Red Sox, you need a clear objective for your business when you start the season. You might not be setting out to win your first World Series in 86 years, but knowing your business objective can be just as important. Remember to “begin with the end in mind.” Whether your business is just forming or has sustained your family for generations, you need to think about your last day in business as well as your first. Take Morris Air for example. In 1984, David Neeleman and June Morris, then travel agency execs, started a modest charter airline in Salt Lake City. Some airlines had brightly painted planes and slogans like “Your Top Banana to Reno.” Others adopted a slightly older sales technique and cut flight attendant uniforms to fit the miniskirt craze. Neeleman and Morris were a bit more creative. They offered discount fares to undermine traditional (expensive) airlines in a city with explosive growth and an ideal location for popular west coast destinations. But the key to their long range success was their end-game plan. Using only Boeing 737 aircraft and adopting the highly successful “no frills” approach of Southwest Airlines, they built a company designed to be sold. In 1994 Southwest purchased its little look-alike for the tidy sum of $129 million. Morris Air had begun with the end in mind and ended on a note of stunning success. Not all businesses achieve the goals of their owners. -

Essays on Strategic Behavior in the U.S. Airline Industry

Essays on Strategic Behavior in the U.S. Airline Industry Dissertation Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of The Ohio State University By Kerria Measkhan Tan, B.A., M.A. Graduate Program in Economics The Ohio State University 2012 Dissertation Committee: Matthew Lewis, Advisor James Peck Huanxing Yang c Copyright by Kerria Measkhan Tan 2012 Abstract In my first dissertation essay, \Incumbent Response to Entry by Low-Cost Carri- ers in the U.S. Airline Industry," I analyze the price response of incumbents to entry by low-cost carriers in the U.S. airline industry. Previous theoretical papers suggest that airlines might respond to entry by lowering prices to compete harder for existing customers or they might increase prices to exploit their brand-loyal customers. This paper tests which effect is more prominent in the airline industry. I find that when one of four low-cost carriers enters a particular route, legacy carrier incumbents respond differently than low-cost carrier incumbents to new low-cost carrier entry. Legacy carriers decrease their mean airfare, 10th percentile airfare, and 90th percentile air- fare before and after entry by a low-cost carrier. However, low-cost carriers do not significantly alter their pricing strategy. The differing incumbent responses can be attributed to the finding that low-cost carrier entrants tend to match the price set by rival low-cost carriers in the quarter of entry and tend to enter with a lower price than that of legacy carrier incumbents. The results also suggest that entry does not affect price dispersion by incumbent carriers. -

Analysis of Global Airline Alliances As a Strategy for International Network Development by Antonio Tugores-García

Analysis of Global Airline Alliances as a Strategy for International Network Development by Antonio Tugores-García M.S., Civil Engineering, Enginyer de Camins, Canals i Ports Universitat Politècnica de Catalunya, 2008 Submitted to the MIT Engineering Systems Division and the Department of Aeronautics and Astronautics in Partial Fulfillment of the Requirements for the Degrees of Master of Science in Technology and Policy and Master of Science in Aeronautics and Astronautics at the Massachusetts Institute of Technology June 2012 © 2012 Massachusetts Institute of Technology. All rights reserved Signature of Author__________________________________________________________________________________ Antonio Tugores-García Department of Engineering Systems Division Department of Aeronautics and Astronautics May 14, 2012 Certified by___________________________________________________________________________________________ Peter P. Belobaba Principal Research Scientist, Department of Aeronautics and Astronautics Thesis Supervisor Accepted by__________________________________________________________________________________________ Joel P. Clark Professor of Material Systems and Engineering Systems Acting Director, Technology and Policy Program Accepted by___________________________________________________________________________________________ Eytan H. Modiano Professor of Aeronautics and Astronautics Chair, Graduate Program Committee 1 2 Analysis of Global Airline Alliances as a Strategy for International Network Development by Antonio Tugores-García