Who Writes the Rules for Hostile Takeovers, and Why? the Peculiar Divergence of US and UK Takeover Regulation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Plutocracy: the Marketising of ‘Equality’ Within Neoliberalism

City Research Online City, University of London Institutional Repository Citation: Littler, J. (2013). Meritocracy as plutocracy: the marketising of ‘equality’ within neoliberalism. New Formations: a journal of culture/theory/politics, 80-81, pp. 52-72. doi: 10.3898/NewF.80/81.03.2013 This is the published version of the paper. This version of the publication may differ from the final published version. Permanent repository link: https://openaccess.city.ac.uk/id/eprint/4167/ Link to published version: http://dx.doi.org/10.3898/NewF.80/81.03.2013 Copyright: City Research Online aims to make research outputs of City, University of London available to a wider audience. Copyright and Moral Rights remain with the author(s) and/or copyright holders. URLs from City Research Online may be freely distributed and linked to. Reuse: Copies of full items can be used for personal research or study, educational, or not-for-profit purposes without prior permission or charge. Provided that the authors, title and full bibliographic details are credited, a hyperlink and/or URL is given for the original metadata page and the content is not changed in any way. City Research Online: http://openaccess.city.ac.uk/ [email protected] MERITOCRACY AS PLUTOCRACY: THE MARKETISING OF ‘EQUALITY’ UNDER NEOLIBERALISM Jo Littler Abstract Meritocracy, in contemporary parlance, refers to the idea that whatever our social position at birth, society ought to facilitate the means for ‘talent’ to ‘rise to the top’. This article argues that the ideology of ‘meritocracy’ has become a key means through which plutocracy is endorsed by stealth within contemporary neoliberal culture. -

The Da Vinci Delusion Unions—Their Great Failure What's Wrong With

middle class and broke: new polls issue 208 | july 2013 www.prospect-magazine.co.uk july 2013 | £4.50 Britain’s folly in Syria britain’s folly in syria Plus The Da Vinci delusion CliVe James Unions—their great failure DaViD gooDharT What’s wrong with France? ChrisTine oCkrenT We’re all machiavelli now JonaThan poWell poet of postwar Britain JonaThan Coe True cost of eU exit: richard lambert In 1912 Malcolm Campbell christened his car “Blue Bird” and a legend was born. More than 100 years later this iconic marque continues to challenge for world speed records using futuristic electric vehicles. Christopher Ward is proud to be the Official Timing Partner for Bluebird and, to celebrate our partnership we have released this exceptional timepiece in a limited edition of 1,912 pieces. 174_ChristopherWard_Prospect.indd 1 10/06/2013 08:16 174_ChristopherWard_Prospect.indd 2 10/06/2013 08:16 We explore further. Aberdeen Investment Trusts ISA and Share Plan At Aberdeen, we believe there’s no substitute for getting to know your investments face-to-face. That’s why we make it our goal to visit companies – wherever they are – before we ever invest in their shares and again when we hold them. With 17 investment companies investing around the world – that’s an awfully big commitment. But it’s just one of the ways we aim to seek out the best investment opportunities on your behalf. Please remember, the value of shares and the income from them can go down as well as up and you may get back less than the amount invested. -

Transcript of Interview with David Kynaston (Historian)

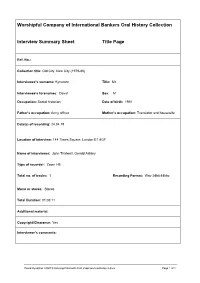

Worshipful Company of International Bankers Oral History Collection Interview Summary Sheet Title Page Ref. No.: Collection title: Old City, New City (1979-86) Interviewee’s surname: Kynaston Title: Mr Interviewee’s forenames: David Sex: M Occupation: Social historian Date of birth: 1951 Father’s occupation: Army officer Mother’s occupation: Translator and housewife Date(s) of recording: 24.04.19 Location of interview: 144 Times Square, London E1 8GF Name of interviewer: John Thirlwell, Gerald Ashley Type of recorder: Zoom H5 Total no. of tracks: 1 Recording Format: Wav 24bit 48khz Mono or stereo: Stereo Total Duration: 01:03:11 Additional material: Copyright/Clearance: Yes Interviewer’s comments: David Kynaston 240419 transcript final with front sheet and endnotes-3.docx Page 1 of 1 Introduction and biography #00:00:00# A club no more: changes from the pre-1980’s village; the #00:0##### aluminium war; Lord Cobbold #00:07:36# Factors of change and external pressures; effects of the abolition of Exchange Control; minimum commissions and single and dual capacity The Stock Exchange ownership question; opening ip to #00:12:17# foreign competition; silly prices paid for firms Cazenove & Co – John Kemp-Welch on partnership and #00:14:57# trust; US capital; Cazenove capital raising Motivations of Big Bang; Philips & Drew; John Craven and #00:18:22# ‘top dollar’ Lloyd’s of London #00:22:26# Bank of England; Margaret Thatcher’s view of the City and #00:25:07# vice versa and her relationship with the Governor, Lord Cobbold Robin Leigh-Pemberton -

Introduction

Notes Introduction 1. Tribune, December 3, 1943, in Paul Anderson ed. Orwell in Tribune (London: Politico’s, 2006), 57. 2. Margaret Tapster, WW2 People’s War, an online archive of wartime memories con- tributed by members of the public and gathered by the BBC. The archive can be found at bbc.co.uk/ww2peopleswar. http://www.bbc.co.uk/history/ww2peopleswar/stories/ 65/a5827665.shtml Accessed May 30, 2013. 3. Paul Addison, No Turning Back: The Peacetime Revolutions of Post-War Britain (Oxford and New York: Oxford University Press, 2010); Peter Hennessy, Having It So Good: Britain in the Fifties (London: Allen Lane, 2006); David Kynaston Aus- terity Britain, 1945–51 (London, Berlin and New York: Bloomsbury, 2007); David Kynaston, Family Britain, 1951–1957 (London, Berlin, New York: Bloomsbury, 2009); Mark Donnelly, Sixties Britain: Culture, Society and Politics (Harlow: Pearson, 2005); Alwyn W. Turner, Crisis? What Crisis? Britain in the 1970s (London: Aurum Press, 2008); Andy Beckett, When the Lights Went Out: Britain in the Seventies (London: Faber and Faber, 2009); Dominic Sandbrook, Seasons in the Sun: The Battle for Britain, 1974–1979 (London: Allen Lane, 2012); Alwyn W. Turner, Rejoice! Rejoice! Britain in the 1980s (London: Aurum, 2010) and Andy McSmith, No Such Thing as Society: A History of Britain in the 1980s (London: Constable, 2011). 4. British and European resistance to American culture is expounded by Dick Hebdige, Subculture: The Meaning of Style (London and New York: Routledge, 1979); Rob Kroes et al. Cultural Transmissions and Receptions: American Mass Culture in Europe (Amsterdam: VU University Press, 1993) and Rob Kroes, If You’ve Seen One, You’ve Seen the Mall: Europeans and American Mass Culture (Urbana, IL: University of Illinois Press, 1996). -

The Modernisation of Elite British Mountaineering

The Modernisation of Elite British Mountaineering: Entrepreneurship, Commercialisation and the Career Climber, 1953-2000 Thomas P. Barcham Thesis submitted in partial fulfilment of the requirements of De Montfort University for the degree of Doctor of Philosophy Submission date: March 2018 Contents Abstract ................................................................................................................................................... 4 Acknowledgments ................................................................................................................................... 5 Table of Abbreviations and Acronyms .................................................................................................... 6 Table of Figures ....................................................................................................................................... 7 Chapter 1. Introduction .......................................................................................................................... 8 Literature Review ............................................................................................................................ 14 Definitions, Methodology and Structure ........................................................................................ 29 Chapter 2. 1953 to 1969 - Breaking a New Trail: The Early Search for Earnings in a Fast Changing Pursuit .................................................................................................................................................. -

Private Lives, Public Histories: the Diary in Twentieth-Century Britain

LJMU Research Online Moran, J Private Lives, Public Histories: The Diary in Twentieth-Century Britain http://researchonline.ljmu.ac.uk/id/eprint/208/ Article Citation (please note it is advisable to refer to the publisher’s version if you intend to cite from this work) Moran, J (2015) Private Lives, Public Histories: The Diary in Twentieth- Century Britain. Journal of British Studies, 54 (1). ISSN 1545-6986 LJMU has developed LJMU Research Online for users to access the research output of the University more effectively. Copyright © and Moral Rights for the papers on this site are retained by the individual authors and/or other copyright owners. Users may download and/or print one copy of any article(s) in LJMU Research Online to facilitate their private study or for non-commercial research. You may not engage in further distribution of the material or use it for any profit-making activities or any commercial gain. The version presented here may differ from the published version or from the version of the record. Please see the repository URL above for details on accessing the published version and note that access may require a subscription. For more information please contact [email protected] http://researchonline.ljmu.ac.uk/ PRIVATE LIVES, PUBLIC HISTORIES: THE DIARY IN TWENTIETH-CENTURY BRITAIN In recent years, the diary of the private citizen has emerged as a fertile source for both academic and non-academic historians. Diaries bring together a range of interests in academic cultural and social history: the development of modern ideas of selfhood, the recovery of overlooked or marginalized lives (particularly those of women, who have often been diligent diarists), and the history of everyday, domestic and private life. -

David Kynaston's Till Time's Last Sand: a History of the Bank of England, 1694-2013: a Review Essay

Charles R. Bean David Kynaston's till time's last sand: a history of the Bank of England, 1694-2013: a review essay Article (Accepted version) (Refereed) Original citation: Bean, Charles R. (2018) David Kynaston's till time's last sand: a history of the Bank of England, 1694-2013: a review essay. American Economic Review. ISSN 0002-8282 © 2018 American Economic Association This version available at: http://eprints.lse.ac.uk/90516/ Available in LSE Research Online: October 2018 LSE has developed LSE Research Online so that users may access research output of the School. Copyright © and Moral Rights for the papers on this site are retained by the individual authors and/or other copyright owners. Users may download and/or print one copy of any article(s) in LSE Research Online to facilitate their private study or for non-commercial research. You may not engage in further distribution of the material or use it for any profit-making activities or any commercial gain. You may freely distribute the URL (http://eprints.lse.ac.uk) of the LSE Research Online website. This document is the author’s final accepted version of the journal article. There may be differences between this version and the published version. You are advised to consult the publisher’s version if you wish to cite from it. David Kynaston’s Till Time’s Last Sand: A History of the Bank of England, 1694-2013. A review essay by Charles R Bean* 28 August 2018 Abstract This essay reviews Till Time’s Last Sand, David Kynaston’s history of the Bank of England from its foundation in 1694 to the present day. -

The Necessity of Reforming Britain's Private Schools Francis Green* And

The Necessity of Reforming Britain’s Private Schools Francis Green* and David Kynaston. [email protected]. UCL Institute of Education, Bedford Way, London WC1H 0AL Abstract The existence of extremely expensive private schools – about one in ten of all our schools -- presents a major problem for Britain’s education system. A new public education system could not coexist with the current, unreformed, private school system: therefore reform is a necessary condition for this project. Private schools are, on the whole, good schools, owing their successes largely to a massive resource input, some three times that of the state sector. But this distortion of our educational resources, is enormously unjust, as well as inefficient and supportive of a democratic deficit in British society. Some solutions are noted; while not dogmatic about which should be adopted, we explain why our preferred solution is a partial integration of the sectors, in particular what we term, in our book Engines of Privilege, a ‘Fair Access Scheme’. The existence of extremely expensive private schools – about one in ten of all our schools -- presents a major problem for Britain’s education system. We argue in this paper that a new public education could not coexist with the existing, unreformed, private school system. If private schools remained untouched, their presence would persistently undermine the desired new public education system. Britain’s private schools offer, on the whole and with one important proviso, a good education in the broadest sense. The left has sometimes found this fact difficult to accept, in the context of supporting public education; nevertheless, the evidence is compelling. -

Bank of England: History, Role and Current Policy Debates

Library Briefing Bank of England: History, Role and Current Policy Debates Summary The Bank of England (‘the Bank’) is a key player in the design and execution of UK economic and regulatory policy. It was founded in 1694 as a private bank. Over time, the Bank’s public role became more prominent. It was nationalised in 1946 and in 1997 the Bank was granted operational independence. The Bank has four main roles. First, it regulates other banks. This function moved away from the Bank in 1997 but returned in 2012. Second, it issues banknotes; it is the only institution in England and Wales that can do so, although certain banks in Scotland and Northern Ireland may also. Third, it sets monetary policy with the aim of meeting the Government’s target for the rate of inflation. And fourth, it is responsible for maintaining financial stability. In addition, the Bank acts as banker to the Government, collects certain economic statistics and carries out and publishes research. The activities of the Bank are the subject of public debate in a range of areas, from the appropriate aims of monetary policy and its links with fiscal policy to the design of banknotes. Some commentators have questioned the political consensus that the Bank should remain independent, while others have accused the Bank of acting too politically, particularly in its communications on Brexit and environmental policy. Discussions also continue about the effectiveness of the Bank’s policy of ‘quantitative easing’ since the financial crisis. Some commentators have also argued that the Bank’s appointments process for senior posts should be more transparent and promote diversity to a greater degree. -

British Conservatism, 1945-1951: Adapting to the Age of Collectivism

THE UNIVERSITY OF ADELAIDE British Conservatism, 1945-1951: Adapting to the Age of Collectivism William Prescott, BA(Hons), LLB(Hons) A Thesis submitted in fulfilment of the requirements for the degree of Master of Philosophy, Department of History, Faculty of Arts, University of Adelaide. March, 2015 Contents Abstract ..................................................................................................................................................... ii Declaration ............................................................................................................................................... iii Acknowledgements .................................................................................................................................. iv List of Abbreviations ................................................................................................................................ vi A Note on Titles and Spelling .................................................................................................................. vii Introduction .............................................................................................................................................. 1 Chapter One: Conservatism and the State: 1834-1945 .......................................................................... 18 Introduction ........................................................................................................................................ 18 Change and the Organic Nature of -

A New Model for Marriage and Motherhood in Postwar Britain, 1945-1960

Dominican Scholar Humanities & Cultural Studies | Senior Liberal Arts and Education | Theses Undergraduate Student Scholarship 5-2020 A New Model for Marriage and Motherhood in Postwar Britain, 1945-1960 Caroline Bland Dominican University of California https://doi.org/10.33015/dominican.edu/2020.HCS.ST.03 Survey: Let us know how this paper benefits you. Recommended Citation Bland, Caroline, "A New Model for Marriage and Motherhood in Postwar Britain, 1945-1960" (2020). Humanities & Cultural Studies | Senior Theses. 3. https://doi.org/10.33015/dominican.edu/2020.HCS.ST.03 This Senior Thesis is brought to you for free and open access by the Liberal Arts and Education | Undergraduate Student Scholarship at Dominican Scholar. It has been accepted for inclusion in Humanities & Cultural Studies | Senior Theses by an authorized administrator of Dominican Scholar. For more information, please contact [email protected]. A NEW MODEL FOR MARRIAGE AND MOTHERHOOD IN POSTWAR BRITAIN 1945-1960 By Caroline Bland A senior thesis submitted to the Humanities Faculty of Dominican University of California in partial fulfillment of the requirements for the Bachelor of Arts in Humanities Dominican University of California San Rafael, California May 16, 2020 ii This thesis, written under the direction of the candidate’s thesis advisor and approved by the department chair, has been presented to and accepted by the Department of Humanities and Cultural Studies, Religion, Philosophy, in partial fulfillment of the requirements for the degree of the Bachelor of Arts in Humanities and Cultural Studies. The content and research methodologies presented in this work represent the work of the candidate alone. -

The Peculiar Divergence of Us and Uk Takeover Regulation

WHO WRITES THE RULES FOR HOSTILE TAKEOVERS, AND WHY?— THE PECULIAR DIVERGENCE OF US AND UK TAKEOVER REGULATION Centre for Business Research, University Of Cambridge Working Paper No. 331 by John Armour Centre for Business Research University of Cambridge Judge Business School Building Trumpington Street Cambridge CB21AG and Faculty of Law University of Cambridge Email: [email protected] and David A. Skeel, Jr University of Pennsylvania Law School 3400 Chestnut Street Philadelphia PA 19104USA Email: [email protected] September 2006 This working paper forms part of the CBR Research Programme on Corporate Governance. Abstract Hostile takeovers are commonly thought to play a key role in rendering managers accountable to dispersed shareholders in the “Anglo-American” system of corporate governance. Yet surprisingly little attention has been paid to the very significant differences in takeover regulation between the two most prominent jurisdictions. In the UK, defensive tactics by target managers are prohibited, whereas Delaware law gives US managers a good deal of room to maneuver. Existing accounts of this difference focus on alleged pathologies in competitive federalism in the US. In contrast, we focus on the “supply-side” of rule production, by examining the evolution of the two regimes from a public choice perspective. We suggest that the content of the rules has been crucially influenced by differences in the mode of regulation. In the UK, self-regulation of takeovers has led to a regime largely driven by the interests of institutional investors, whereas the dynamics of judicial law-making in the US have benefited managers by making it relatively difficult for shareholders to influence the rules.