Jupiter Fund of Investment Trusts RICHARD CURLING Fund Manager

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The VT Redlands Portfolios

The VT Redlands Portfolios What are the VT Redlands Portfolios? The VT Redlands Portfolio funds each invest in one of four defined “asset classes” namely the Equity, Multi-Asset, Property and Fixed Income categories. Each fund carries a prescribed Risk Profile on a scale of 1 to 7 – with for example Equity being the highest at a factor 5. Each one is used as a building block in the creation of bespoke risk rated investment portfolios for clients of David Williams IFA. By combining the four VT Redlands funds with other asset classes such as With Profits/ Smoothed Managed and Structured Equity funds, our clients can enjoy the benefits of a very wide level of diversification within their portfolios. This reduces volatility and creates the potential for rewarding rates of return year after year. Each Portfolio fund is constructed as a Fund of Funds providing access to the “best of the best” sector funds from a huge investment universe. The Portfolios are designed to meet their objectives as efficiently as possible whilst keeping costs to a minimum and are run according to a strict risk-control criteria. Typically, 15 to 25 different funds are held in each portfolio, with each one in turn managed by leading investment houses such as Fundsmith, Fidelity and Invesco as well as specialist boutiques including Ruffer, Fulcrum and Somerset. Underlying funds have exposure to a great many shares, bonds and other assets, Therefore, a single investment into one of the Redlands Portfolios gives a spread across a myriad of different holdings, countries and investment styles. -

Parker Review

Ethnic Diversity Enriching Business Leadership An update report from The Parker Review Sir John Parker The Parker Review Committee 5 February 2020 Principal Sponsor Members of the Steering Committee Chair: Sir John Parker GBE, FREng Co-Chair: David Tyler Contents Members: Dr Doyin Atewologun Sanjay Bhandari Helen Mahy CBE Foreword by Sir John Parker 2 Sir Kenneth Olisa OBE Foreword by the Secretary of State 6 Trevor Phillips OBE Message from EY 8 Tom Shropshire Vision and Mission Statement 10 Yvonne Thompson CBE Professor Susan Vinnicombe CBE Current Profile of FTSE 350 Boards 14 Matthew Percival FRC/Cranfield Research on Ethnic Diversity Reporting 36 Arun Batra OBE Parker Review Recommendations 58 Bilal Raja Kirstie Wright Company Success Stories 62 Closing Word from Sir Jon Thompson 65 Observers Biographies 66 Sanu de Lima, Itiola Durojaiye, Katie Leinweber Appendix — The Directors’ Resource Toolkit 72 Department for Business, Energy & Industrial Strategy Thanks to our contributors during the year and to this report Oliver Cover Alex Diggins Neil Golborne Orla Pettigrew Sonam Patel Zaheer Ahmad MBE Rachel Sadka Simon Feeke Key advisors and contributors to this report: Simon Manterfield Dr Manjari Prashar Dr Fatima Tresh Latika Shah ® At the heart of our success lies the performance 2. Recognising the changes and growing talent of our many great companies, many of them listed pool of ethnically diverse candidates in our in the FTSE 100 and FTSE 250. There is no doubt home and overseas markets which will influence that one reason we have been able to punch recruitment patterns for years to come above our weight as a medium-sized country is the talent and inventiveness of our business leaders Whilst we have made great strides in bringing and our skilled people. -

The Virgin UK Index Tracking Trust

The Virgin UK Index Tracking Trust Final Report and Financial Statements For the year ended 15 March 2021 2 The Virgin UK Index Tracking Trust Contents Manager's report 3 Management and professional services 3 Manager's investment report 4 Comparative tables 11 Portfolio statement 12 Top purchases and sales of investments 30 Securities Financing Transactions (SFTs) 32 Statement of total return 36 Statement of change in net assets attributable to unitholders 37 Balance sheet 38 Notes to the financial statements 39 Distribution tables 53 Statement of the Manager’s responsibilities 54 Independent auditor’s report to the unitholders of the Virgin UK Index Tracking Trust 55 Manager’s remuneration 58 Statement of the Trustee’s responsibilities in respect of the Scheme and Report of the Trustee to the Unitholders of the Virgin UK Index Tracking Trust 59 The Virgin UK Index Tracking Trust 3 Management and professional services For the year ended 15 March 2021 Manager (the ‘Manager’) Virgin Money Unit Trust Managers Limited Jubilee House Directors: S. Bruce (appointed 29 September 2020) Gosforth J. Byrne (appointed 24 May 2021) Newcastle upon Tyne H. Chater NE3 4PL S. Fennessy (resigned 29 September 2020) F. Murphy (appointed 19 October 2020) M. Phibbs J. Scott (resigned 4 December 2020) I. Smith (resigned 19 October 2020) D. Taylor (appointed 29 September 2020) N. L. Tu (resigned 24 May 2021) S. Wemyss (appointed 8 December 2020) Telephone 03456 10 20 30* Authorised and regulated by the Financial Conduct Authority. Investment adviser Aberdeen Asset Managers Limited 10 Queen’s Terrace Aberdeen Aberdeenshire AB10 1XL Authorised and regulated by the Financial Conduct Authority. -

2020 Annual Report

Mercantile A4 Cover.qxp 15/04/2020 11:32 Page 1 THE MERCANTILE INVESTMENT TRUST PLC ANNUAL REPORT & FINANCIAL STATEMENTS FOR THE YEAR ENDED 31ST JANUARY 2020 PUTTING THE BRIGHTEST SPARKS IN YOUR PORTFOLIO Mercantile A4 Cover.qxp 15/04/2020 11:32 Page B1 FEATURES Your Company Objective Long term capital growth from a portfolio of UK medium and smaller companies. Investment Policy • To emphasise capital growth from medium and smaller companies. • To achieve long term dividend growth at least in line with inflation. • To use long term gearing to increase potential returns to shareholders. The Company’s gearing policy is to operate within a range of 10% net cash to 20% geared. • To invest no more than 15% of gross assets in other UK listed closed-ended investment funds (including investment trusts). Benchmark The FTSE All-Share Index, excluding constituents of the FTSE 100 Index and investment trusts, with net dividends reinvested. Capital Structure At 31st January 2020 the Company’s share capital comprised 944,492,180 ordinary shares of 2.5p each, including 152,969,287 shares held in Treasury. At 31st January 2020, the Company also had in issue a £3.85 million 4.25% perpetual debenture and a £175 million 6.125% debenture repayable on 25th February 2030. Management Company and Company Secretary The Company employs JPMorgan Funds Limited (‘JPMF’ or the ‘Manager’) as its Alternative Investment Fund Manager and Company Secretary. JPMF is approved by the Financial Conduct Authority and delegates the management of the Company’s portfolio to JPMorgan Asset Management (UK) Limited (‘JPMAM’). -

Changing Times INVESTING for a NEW WORLD ORDER?

SUMMER 2018 Changing times INVESTING FOR A NEW WORLD ORDER? alliancetrustsavings.co.uk Welcome to the latest edition of Taking Stock. Changing times If this edition had a theme tune it might be something like Bob Dylan’s 1960s classic The Times They Are A-Changin’. Or at least that’s how it feels to many of us. US protectionism, Trump-style diplomacy, North Korea, Iran, Syria, Russia, China, Brexit, Facebook, Cambridge Analytica. These have all been headline makers for 2018 so far, and some have undoubtedly been implicated in increased market volatility. Around the world the political and economic power of nation states has always ebbed and flowed. Alliances are made and undone. And the fortunes of individual corporations rise and fall. But the question for investors today is, are we just looking at a variation on a theme of business as usual for the world’s established economic power base? Or is something else going on? Are we on the cusp of some more fundamental change in the world economic order? Keeping ahead of the curve Views on this matter because searching for growth necessarily involves looking ahead and understanding where the longer-term opportunities and threats are likely to be. In this edition of Taking Stock our expert contributors explore the potential implications of the developing picture. From how it’s influencing investment decisions today, to steps any investor can take to make the most of their money in uncertain times. As always, I hope you will find it an informative read. If you have any feedback or suggestions for future editions, please get in touch. -

Life After Lockdown

www.whatinvestment.co.uk Issue 460 | July 2021 | £4.50 LIFE AFTER LOCKDOWN A growing concern Are you switched on? A high stakes game Investing in trees could How artifi cial intelligence Peter Elston on why be the antidote to some of is transforming life as infl ation is far more Earth’s biggest challenges we know it complex than it appears Pages 34-35 Pages 50-52 Page 82 001_WI_0721.indd 1 17/06/2021 10:42 ad template.indd 1 17/06/2021 12:02 First word 3 July 2021 On life and investing www.whatinvestment.co.uk Issue 460 | July 2021 | £4.50 LIFE AFTER LOCKDOWN after the pandemic A growing concern Are you switched on? A high stakes game Investing in trees could How artificial intelligence Peter Elston on why be the antidote to some of is transforming life as inflation is far more Earth’s biggest challenges we know it complex than it appears Pages 34-35 Pages 50-52 Page 82 elcome to the July issue As you will learn in this month’s Editorial of What Investment, which issue, some investment trust Editor-in-chief comes at a time when it managers believe there will be a Lawrence Gosling 020 7250 7027 W [email protected] looks like the economy is on the very strong recovery, particularly verge of opening up for the fi rst in areas like consumer spending, Subscriptions Lara Rossett 020 7250 7011 time since March of last year. housebuilding and specialist [email protected] How we view this situation industrial businesses; others don’t Advertising depends largely on what kind of Lawrence Gosling think things will be so simple. -

FTSE Factsheet

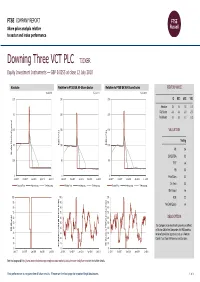

FTSE COMPANY REPORT Share price analysis relative to sector and index performance Data as at: 12 July 2018 Downing Three VCT PLC TICKER Equity Investment Instruments — GBP 0.0255 at close 12 July 2018 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 12-Jul-2018 12-Jul-2018 12-Jul-2018 0.25 250 250 1D WTD MTD YTD Absolute 0.0 0.0 0.0 0.0 Rel.Sector -0.4 -0.8 -0.5 -2.0 0.2 200 200 Rel.Market -0.7 -0.5 -0.1 0.3 0.15 150 150 VALUATION (local currency) (local Trailing 0.1 Relative Price 100 Relative Price 100 PE 0.4 Absolute Price Price Absolute EV/EBITDA 0.3 0.05 50 50 PCF -ve PB 0.0 0 0 0 Price/Sales 0.2 Jul-2017 Oct-2017 Jan-2018 Apr-2018 Jul-2018 Jul-2017 Oct-2017 Jan-2018 Apr-2018 Jul-2018 Jul-2017 Oct-2017 Jan-2018 Apr-2018 Jul-2018 Div Yield 0.0 Absolute Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Relative Price 4-wk mov.avg. 13-wk mov.avg. Div Payout +ve 100 100 100 ROE 2.2 90 90 90 Net Debt/Equity -ve 80 80 80 70 70 70 60 60 60 DESCRIPTION 50 50 50 The Company is an investment company as defined 40 40 40 RSI (Absolute) RSI in Section 266 of the Companies Act 1985 and has 30 30 30 received provisional approval to act as a Venture 20 20 20 Capital Trust from HM Revenue and Customs. -

Chrysalis Investments Limited

THIS PROSPECTUS IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. If you are in any doubt as to what action you should take you are recommended to seek your own financial advice immediately from your stockbroker, bank, solicitor, accountant or other independent financial adviser who is authorised under the Financial Services and Markets Act 2000 (the “FSMA”) if you are in the United Kingdom, or from another appropriately authorised independent financial adviser if you are in a territory outside the United Kingdom. This Prospectus comprises a prospectus relating to Chrysalis Investments Limited (the “Company”) in connection with the issue of Shares, prepared in accordance with the Prospectus Regulation Rules of the Financial Conduct Authority made pursuant to section 73A of the FSMA. This Prospectus has been approved by the Financial Conduct Authority for the purposes of the UK version of Regulation (EU) 2017/1129 (the “EU Prospectus Regulation”) which forms part of UK law by virtue of the European Union (Withdrawal) Act 2018 (the “UK Prospectus Regulation”). The Financial Conduct Authority only approves this Prospectus, as the competent authority under the Prospectus Regulation Rules, as meeting the standards of completeness, comprehensibility and consistency imposed by the UK Prospectus Regulation. Such approval should not be considered as an endorsement of the Company that is the subject of this Prospectus or of the quality of the Shares. This Prospectus has been drawn up and published in accordance with the UK Prospectus Regulation. Investors should make their own assessment as to the suitability of investing in the Shares. The Shares are only suitable for investors: (i) who understand and are willing to assume the potential risks of capital loss and that there may be limited liquidity in the underlying investments of the Company; (ii) for whom an investment in the Shares is part of a diversified investment programme; and (iii) who fully understand and are willing to assume the risks involved in such an investment. -

Blackrock European Dynamic D Acc When Their Style Is in Favour, We Expect Them (GB00B5W2QB11) and Liontrust Special to Outperform Strongly

STOCKS | FUNDS | INVESTMENT TRUSTS | PENSIONS AND SAVINGS VOL 20 / ISSUE 19 / 17 MAY 2018 / £4.49 SHARES WE MAKE INVESTING EASIER 14.6% 13.7% 12.7% 12.2% 10.7% COULD YOU GET THREE 6% YIELD INVESTMENT TRUSTS FROM ROYAL BANK TO PLAY THE OF SCOTLAND? RISING OIL PRICE EARLY RETIREMENT: IS IT POSSIBLE ANYMORE? SCOTTISHTHE MONKSMORTGAGE INVESTMENT INVESTMENT TRUST TRUST PLC MONKS HAS OVER £1.5BN IN NET ASSETS UNDER MANAGEMENT, WHILE ITS ONGOING CHARGE IS A MODEST 0.59%*. THE KEY TO A WELL TUNED PORTFOLIO. Monks Investment Trust, we believe, could be a core investment for anyone seeking long-term growth. It is managed according to Baillie Gifford’s £33bn Global Alpha strategy. As a result, Monks takes a highly active approach to investment and its portfolio looks nothing like the index. The managers group their holdings into four different growth categories – stalwart, rapid, cyclical and latent. This allows for excellent diversifi cation and offers the chance to unearth some of the more interesting companies listed on global stock markets. Please remember that changing stock market conditions and currency exchange rates will affect the value of the investment in the fund and any income from it. Investors may not get back the amount invested. If in doubt, please seek fi nancial advice. If you’re looking for a fund to shine at the centre of your portfolio, call 0800 917 2112 or visit www.monksinvestmenttrust.co.uk A Key Information Document is available by contacting us. Long-term investment partners *Ongoing charges as at 30.04.17. -

FTSE Russell Publications

2 FTSE Russell Publications 19 August 2021 FTSE 250 Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) 3i Infrastructure 0.43 UNITED Bytes Technology Group 0.23 UNITED Edinburgh Investment Trust 0.25 UNITED KINGDOM KINGDOM KINGDOM 4imprint Group 0.18 UNITED C&C Group 0.23 UNITED Edinburgh Worldwide Inv Tst 0.35 UNITED KINGDOM KINGDOM KINGDOM 888 Holdings 0.25 UNITED Cairn Energy 0.17 UNITED Electrocomponents 1.18 UNITED KINGDOM KINGDOM KINGDOM Aberforth Smaller Companies Tst 0.33 UNITED Caledonia Investments 0.25 UNITED Elementis 0.21 UNITED KINGDOM KINGDOM KINGDOM Aggreko 0.51 UNITED Capita 0.15 UNITED Energean 0.21 UNITED KINGDOM KINGDOM KINGDOM Airtel Africa 0.19 UNITED Capital & Counties Properties 0.29 UNITED Essentra 0.23 UNITED KINGDOM KINGDOM KINGDOM AJ Bell 0.31 UNITED Carnival 0.54 UNITED Euromoney Institutional Investor 0.26 UNITED KINGDOM KINGDOM KINGDOM Alliance Trust 0.77 UNITED Centamin 0.27 UNITED European Opportunities Trust 0.19 UNITED KINGDOM KINGDOM KINGDOM Allianz Technology Trust 0.31 UNITED Centrica 0.74 UNITED F&C Investment Trust 1.1 UNITED KINGDOM KINGDOM KINGDOM AO World 0.18 UNITED Chemring Group 0.2 UNITED FDM Group Holdings 0.21 UNITED KINGDOM KINGDOM KINGDOM Apax Global Alpha 0.17 UNITED Chrysalis Investments 0.33 UNITED Ferrexpo 0.3 UNITED KINGDOM KINGDOM KINGDOM Ascential 0.4 UNITED Cineworld Group 0.19 UNITED Fidelity China Special Situations 0.35 UNITED KINGDOM KINGDOM KINGDOM Ashmore -

FTSE Factsheet

FTSE COMPANY REPORT Share price analysis relative to sector and index performance BB Healthcare Trust BBH Closed End Investments — GBP 2.01 at close 16 April 2021 Absolute Relative to FTSE UK All-Share Sector Relative to FTSE UK All-Share Index PERFORMANCE 21-Apr-2015 1D WTD MTD YTD Absolute - - - - Rel.Sector - - - - Rel.Market - - - - VALUATION Data unavailable Trailing PE 6.0 EV/EBITDA 5.4 PB 1.1 PCF -ve Div Yield 2.6 Price/Sales 5.7 Net Debt/Equity 0.0 Div Payout 15.4 ROE 21.6 DESCRIPTION Data unavailable The Company is a closed-ended investment company which to invest in a concentrated portfolio of listed or quoted equities in the global healthcare industry. Past performance is no guarantee of future results. Please see the final page for important legal disclosures. 1 of 4 FTSE COMPANY REPORT: BB Healthcare Trust 16 April 2021 Valuation Metrics Price to Earnings (PE) EV to EBITDA Price to Book (PB) 31-Mar-2021 31-Mar-2021 31-Mar-2021 25 25 1.5 1.4 20 20 +1SD 1.3 +1SD +1SD 1.2 Avg 15 15 1.1 Avg Avg -1SD 1 10 10 0.9 -1SD -1SD 5 5 0.8 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Apr-2016 Apr-2017 Apr-2018 Apr-2019 Apr-2020 Murray International Trust (Ord) 120.0 Murray International Trust (Ord) 100.0 CVC Credit Partners European Opportunities (GBP) 2.3 European Opportunities Trust 120.0 European Opportunities Trust 100.0 Hipgnosis Songs Fund 2.2 Law Debenture Corp 120.0 Law Debenture Corp 100.0 Pacific Horizon Investment Trust 2.0 HICL Infrastructure 64.6 HICL Infrastructure 64.5 Scottish -

21 Apr, 2021 the Third Way – Why Choose

SUPPLEMENT | APRIL 2021 STOCKS AND SHARES ISAs Healthcare and technology could be the best medicine to revitalise your growth ISA The recommended dose for your ISA Seize the day Small and mighty School of thought Don’t dally, act now to profit The Aim market is going Learn about the opportunities from the financials rally from strength to strength in the edtech sector Pages 5 & 6 Pages 12 & 13 Pages 14 & 15 ad template.indd 1 18/03/2021 09:28 Contents Stocks and shares ISAs | April 2021 3 LEADER ‘ Regular investing has a smoothing effect’ Lawrence Gosling , editor-in-chief, What Investment In an ideal world we’d all be smooth ISA operators, contributing regularly and avoiding the mad dash to make investments ahead of a new tax year t is a quirk of human nature that many of us only do I something when we are It is a quirk of human facing a deadline. What else could explain the interest in ISAs and nature that many of us Junior ISAs in March and the fi rst only do something when week of April each year? we are facing a deadline Of course, we can make a contribution into an ISA on any day of a tax year starting from So if you don’t already, perhaps 4 Comfort fi rst 6 April, and there is a strong consider making monthly ISA Why the trend may not always be argument for investing earlier contributions, rather than a your friend when investing for an ISA rather than later. single lump sum at the start That is easy to say in retrospect, or end of a tax year.