Presentation Title Slide, No Image: One-Line Title Preferred

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

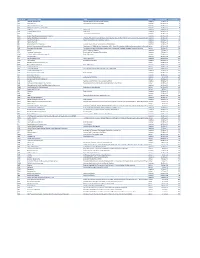

Mvx List.Pdf

MVX_CODE manufacturer_name Notes status last updated date manufacturer_id AB Abbott Laboratories includes Ross Products Division, Solvay Inactive 16-Nov-17 1 ACA Acambis, Inc acquired by sanofi in sept 2008 Inactive 28-May-10 2 AD Adams Laboratories, Inc. Inactive 16-Nov-17 3 ALP Alpha Therapeutic Corporation Inactive 16-Nov-17 4 AR Armour part of CSL Inactive 28-May-10 5 AVB Aventis Behring L.L.C. part of CSL Inactive 28-May-10 6 AVI Aviron acquired by Medimmune Inactive 28-May-10 7 BA Baxter Healthcare Corporation-inactive Inactive 28-May-10 8 BAH Baxter Healthcare Corporation includes Hyland Immuno, Immuno International AG,and North American Vaccine, Inc./acquired somInactive 16-Nov-17 9 BAY Bayer Corporation Bayer Biologicals now owned by Talecris Inactive 28-May-10 10 BP Berna Products Inactive 28-May-10 11 BPC Berna Products Corporation includes Swiss Serum and Vaccine Institute Berne Inactive 16-Nov-17 12 BTP Biotest Pharmaceuticals Corporation New owner of NABI HB as of December 2007, Does NOT replace NABI Biopharmaceuticals in this codActive 28-May-10 13 MIP Emergent BioSolutions Formerly Emergent BioDefense Operations Lansing and Michigan Biologic Products Institute Active 16-Nov-17 14 CSL bioCSL bioCSL a part of Seqirus Inactive 26-Sep-16 15 CNJ Cangene Corporation Purchased by Emergent Biosolutions Inactive 29-Apr-14 16 CMP Celltech Medeva Pharmaceuticals Part of Novartis Inactive 28-May-10 17 CEN Centeon L.L.C. Inactive 28-May-10 18 CHI Chiron Corporation Part of Novartis Inactive 28-May-10 19 CON Connaught acquired by Merieux Inactive 28-May-10 21 DVC DynPort Vaccine Company, LLC Active 28-May-10 22 EVN Evans Medical Limited Part of Novartis Inactive 28-May-10 23 GEO GeoVax Labs, Inc. -

Consolidation Revisited Is the Founder of Managing Resources, a Date Received *In Revised Form) 8Th October, 2001 Consultancy Focused on the Life Science Industries

Alan Williams Consolidation revisited is the founder of Managing Resources, a Date received *in revised form) 8th October, 2001 consultancy focused on the life science industries. The Alan Williams company undertakes strategic assignments and also assists public and private sector clients with regulatory affairs, investor Abstract In 1998, the author produced two papers that argued that consolidation was relations and human a necessary activity for biotechnology companies to pay greater attention to. Three resources development. years later a further consideration of the subject seems worthwhile. Examples of Alan has also been an investment manager in successful consolidators are reviewed. a venture capital company, and held Keywords: consolidation, mergers, acquisitions marketing and licensing positions in Fisons. Introduction drink, vaccines and animal health but there is now greater focus on the highest In the early/mid-1970s, the pharmaceutical pro®tability sector, human pharmaceuticals. industry consisted of more than 100 At the time of writing, GSK is rumoured to research-based businesses of some be a possible purchaser of Bayer's signi®cant size, although none of them pharmaceutical business, the future of could convincingly claim a global presence. which has been questioned after the Typically, a leading company had a strong withdrawal of cerivastatin. position in its local market "examples Aventis, the eighth largest pharmaceutical included Merck and P®zer in the USA, company by sales in 2000,1 includes the Bayer in Germany, Beecham in the UK, operations of 1970s companies such as Roussel-Uclaf in France and Fujisawa in Rhone-Poulenc, Rorer, Fisons, Hoechst, Japan) and possibly some other Marion, Richardson Merrell, and some neighbouring countries "US companies in smaller companies. -

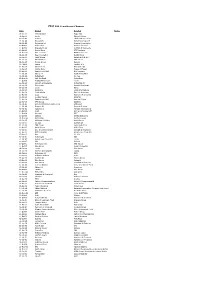

FTSE 100 Constituent History Updated

FTSE 100 Constituent Changes Date Added Deleted Notes 19-Jan-84 CJ Rothschild Eagle Star 02-Apr-84 Lonrho Magnet Sthrns. 02-Jul-84 Reuters Edinburgh Inv. Trust 02-Jul-84 Woolworths Barrat Development 19-Jul-84 Enterprise Oil Bowater Corporation 01-Oct-84 Willis Faber Wimpey (George) 01-Oct-84 Granada Group Scottish & Newcastle 01-Oct-84 Dowty Group MFI Furniture 04-Dec-84 Brit. Telecom Matthey Johnson 02-Jan-85 Dee Corporation Dowty Group 02-Jan-85 Argyll Group Berisford (S.& W.) 02-Jan-85 MFI Furniture RMC Group 02-Jan-85 Dixons Group Dalgety 01-Feb-85 Jaguar Hambro Life 01-Apr-85 Guinness (A) Enterprise Oil 01-Apr-85 Smiths Inds. House of Fraser 01-Apr-85 Ranks Hovis McD. MFI Furniture 01-Jul-85 Abbey Life Ranks Hovis McD. 01-Jul-85 Debenhams I.C. Gas 06-Aug-85 Bnk. Scotland Debenhams 01-Oct-85 Habitat Mothercare Lonrho 02-Jan-86 Scottish & Newcastle Rothschild (J) 08-Jan-86 Storehouse Habitat Mothercare 08-Jan-86 Lonrho B.H.S. 01-Apr-86 Wellcome EXCO International 01-Apr-86 Coats Viyella Sun Life Assurance 01-Apr-86 Lucas Harrisons & Crosfield 01-Apr-86 Cookson Group Ultramar 21-Apr-86 Ranks Hovis McD. Imperial Group 22-Apr-86 RMC Group Distillers 01-Jul-86 British Printing & Comms. Corp Abbey Life 01-Jul-86 Burmah Oil Bank of Scotland 01-Jul-86 Saatchi & S. Ferranti International 01-Oct-86 Bunzl Brit. & Commonwealth 01-Oct-86 Amstrad BICC 01-Oct-86 Unigate Smiths Industries 09-Dec-86 British Gas Northern Foods 02-Jan-87 Hillsdown Holdings Argyll Group 02-Jan-87 I.C. -

Commercial Biotechnology: an International Analysis (January 1984)

Commercial Biotechnology: An International Analysis January 1984 NTIS order #PB84-173608 — Recommended Citation: Commercial Biotechnology: An International Analysis (Washington, D. C.: U.S. Congress, Office of Technology Assessment, OTA-BA-218, January 1984). Library of Congress Catalog Card Number 84-601000 For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, D.C. 20402 — Foreword This report assesses the competitive position of the United States with respect to Japan and four European countries believed to be the major competitors in the commercial development of “new biotechnology.” This assessment continues a series of OTA studies on the competitiveness of U.S. industries. It was requested by the House Committee on Science and Technology and the Senate Com- mittee on Commerce, Science, and Transportation. Additionally, a letter of support for this study was received from the Senate Committee on Labor and Human Resources. New biotechnology, as defined in this report, focuses on the industrial use of recombinant DNA) cell fusion, and novel bioprocessing techniques. These techniques will find applications across many industrial sectors including pharmaceuticals, plant and animal agriculture, specialty chemicals and food additives, environmental applications, commodity chemicals and energy production, and bioelec- tronics. Over 100 new firms have been started in the United States in the last several years to capitalize on the commercial potential of biotechnology. Additionally, throughout the world, many established companies in a diversity of industrial sectors have invested in this technology. A well developed life science base, the availability of financing for high-risk ventures, and an entre- preneurial spirit have led the United States to the forefront in the commercialization of biotechnol- ogy. -

Mixed Amphetamine Salts Extended Release for the Treatment of ADHD in Adults: Current Evidence

December 2005 Volume 10 - Number 12 - Suppl 20 CNS SPEGTRUMS The International Journal of Neuropsychiatric Medicine ACADEMIC SUPPLEMENT Mixed Amphetamine Salts Extended Release for the Treatment of ADHD in Adults: Current Evidence Introduction /. Biederman Single- and Multiple-Dose Pharmacokinetics of an Oral Mixed Amphetamine Salts Extended-Release Formulation in Adults S.B. Clausen, S.C. Read, S.J. TuUoch Long-Term Safety and Effectiveness of Mixed Amphetamine Salts Extended Release in Adults With ADHD J. Biederman, TJ Spencer, T.E. Wilens, R.H. Weisler, S.C. Read, S.J. TuUoch An Interim Analysis of the Quality of Life, Effectiveness, Safety, and Tolerability (QU.E.S.T.) Evaluation of Mixed Amphetamine Salts Extended Release in Adults With ADHD D. W. Goodman, L. Ginsberg, R.H. Weisler, A.J. Cutler, P. Hodgkins Long-Term Cardiovascular Effects of Mixed Amphetamine Salts Extended Release in Adults With ADHD R.H. Weisler, J. Biederman, TJ. Spencer, T.E. Wilens Index /Wed/cus/MEDLINE citation: CNS Spectr Downloaded from https://www.cambridge.org/core. IP address: 170.106.34.90, on 28 Sep 2021 at 11:35:36, subject to the Cambridge Core terms of use, available at https://www.cambridge.org/core/terms. https://doi.org/10.1017/S1092852900002364 Faculty Affiliations and Disclosures Joseph Biederman, MD, is chief of the Pediatric Psychopharmacology Research Unit at the Massachusetts General Hospital in Boston. He has been a speaker for Cephalon, Eli Lilly, McNeil, and Shire; is on the advisory boards of Cephalon, Eli Lilly, Janssen, McNeil, Novartis, and Shire; and has received research support from Abbott, Bristol-Myers Squibb, Cephalon, Eli Lilly, the Lilly Foundation, Janssen, McNeil, the National Institute of Child Health and Human Development (NICMH), the National Institute on Drug Abuse (NIDA), the National Institute of Mental Health (NIMH), Neurosearch, New River, Pfizer, Prechter Foundation, Shire, and the Stanley Medical Institute. -

FTSE 100 Historic Additions and Deletions

FTSE 100 Historic Additions and Deletions ftserussell.com An LSEG Business September 2021 FTSE 100 – Historic Additions and Deletions Date Added Deleted Notes 19-Jan-84 Charterhouse J Rothschild Eagle Star Corporate Event - Acquisition of Eagle Star by BAT Industries 02-Apr-84 Lonrho Magnet & Southerns 02-Jul-84 Reuters Edinburgh Investment Trust 02-Jul-84 Woolworths Barratt Development 19-Jul-84 Enterprise Oil Bowater Corporation Corporate Event - Sub division of company into Bowater Inds and Bowater Inc 01-Oct-84 Willis Faber Wimpey (George) & Co 01-Oct-84 Granada Group Scottish & Newcastle Breweries 01-Oct-84 Dowty Group MFI Furniture Corporate Event - Acquisition of MFI Furniture by Associated Dairies Group 04-Dec-84 British Telecom Johnson Matthey Fast Entry 02-Jan-85 Dee Corporation Dowty Group 02-Jan-85 Argyll Group Berisford (S & W) 02-Jan-85 MFI Furniture RMC Group 02-Jan-85 Dixons Group Dalgety 01-Feb-85 Jaguar Hambro Life Corporate Event - Acquisition of Hambro Life by BAT Industries 01-Apr-85 Guinness (Arthur) & Son Enterprise Oil 01-Apr-85 Smith Industries House of Fraser Corporate Event - Acquisition of House of Fraser by Alfayed Investment Trust 01-Apr-85 Ranks Hovis McDougall MFI Furniture Corporate Event - Acquisition of MFI Furniture by Associated Dairies Group 01-Jul-85 Abbey Life Ranks Hovis McDougall 01-Jul-85 Debenhams Imperial Continental Gas Ass. 06-Aug-85 Bank of Scotland Debenhams 01-Oct-85 Habitat Mothercare Lonrho 02-Jan-86 Scottish & Newcastle Rothschild (J) Holdings 08-Jan-86 Storehouse Habitat Mothercare -

What Science Can Do Can Science What

What science can do AstraZeneca Annual Report and Form 20-F Information 2016 AstraZeneca Annual Report and 20-F Form Information 2016 Preparation of the Financial Statements and Directors’ Responsibilities The Directors are responsible for preparing this > for the Parent Company Financial Directors’ responsibility statement Annual Report and Form 20-F Information and Statements, state whether FRS 101 has pursuant to DTR 4 the Group and Parent Company Financial been followed, subject to any material The Directors confirm that to the best of Statements in accordance with applicable law departures disclosed and explained in the our knowledge: and regulations. Parent Company Financial Statements > The Financial Statements, prepared in > prepare the Financial Statements on the Company law requires the Directors to accordance with the applicable set of going concern basis unless it is inappropriate prepare Group and Parent Company Financial accounting standards, give a true and to presume that the Group and the Parent Statements for each financial year. Under that fair view of the assets, liabilities, financial Company will continue in business. law they are required to prepare the Group position and profit or loss of the Company Financial Statements in accordance with The Directors are responsible for keeping and the undertakings included in the IFRSs as adopted by the EU and applicable adequate accounting records that are consolidation taken as a whole. law and have elected to prepare the Parent sufficient to show and explain the Parent > The Directors’ Report includes a fair review Company Financial Statements in accordance Company’s transactions and disclose with of the development and performance of with UK Accounting Standards, including reasonable accuracy at any time the financial the business and the position of the issuer FRS 101 ‘Reduced Disclosure Framework’ position of the Parent Company and enable and the undertakings included in the and applicable law. -

Creating Excellence and Innovation Multiple Delivery Technologies

HEAD OFFICE SKYEPHARMA PLC 46–48 grOSVENOR GARDENS LoNDON SW1W 0EB REGISTERED NO: 107582 TELEPHONE: +44 (0)207 881 0524 FAX: +44 (0)207 881 1199 email: [email protected] MULTIPLE www.skyepharma.com DELIVERY TECHNOLOGIES ANNU A L REPO R T A N D ACCOUNTS FO D ACCOUNTS CREATING EXCELLENCE AND INNOVATION R THE YE AR EN D E D 31 D ECEMBE R ENHANCING 2010 QUALITY OF LIFE FOR PATIENTS ANNUAL REPORT AND ACCOUNTS FOR THE YEAR ENDED 31 DECEMBER 2010 ADVISERS AUDItoRS ADR DEPOSITARY SkyePharma PLC Ernst & Young LLP Bank of New York Mellon Apex Plaza 101 Barclay Stret SKYEPHarma’s missiON IS TO BECOME Reading New York NY 10286 ONE OF THE WOrld’s leading RG1 1YE USA SPECIALITY DRUG DELIVERY COMPANIES, SOLICItoRS REGISTRARS Fasken Martineau LLP Capita Registrars POWERED THROUGH EXCELLENCE IN ITS 17 Hanover Square The Registry London 34 Beckenham Road ORAL AND INHALATION TECHNOLOGIES. W1S 1HU Beckenham Kent SKYEPHARMA STRIVES TO DELIVER Clifford Chance LLP BR3 4TU CLINICAL BENEFITS FOR PATIENTS 10 Upper Bank Street London Telephone: 0871 664 0300 BY USING ITS MULTIPLE DELIVERY E14 5JJ (Calls cost 10 pence per minute plus network extras) (from outside the UK: +44 (0) 20 8639 3399) TECHNOLOGIES TO CREATE CORPORATE BROKER & FINANCIAL ADVISER ENHANCED VERSIONS OF EXISTING Singer Capital Markets Ltd Lines are open Monday – Friday 8:30 a.m. – 5:30 p.m. One Hanover Street Facsimile: +44 (0) 20 8639 2220 PHARMACEUTICAL PRODUCTS. London Email: [email protected] W1S 1YZ Website:www.capitaregistrars.com Capita Share Portal: www.capitashareportal.com BANKERS -

Celltech Group Plc Annual Report and Accounts 2003

Celltech Group plc Annual Report and Accounts 2003 Celltech is a leading European complementary capabilities through biotechnology company with a long-term collaborations with other pharma and commitment to the research and biotech companies.This strategy, development of innovative therapies for supported by its strong revenue stream, patients with serious diseases.Celltech is enables Celltech to maintain a substantial a recognised global leader in advanced investment in research and development antibody technologies, which together whilst maintaining its financial strength with its innovative small molecule and flexibility. capabilities, provide a strong platform for Corporate Statement development of first-in-class or best-in- The combination of these strengths class treatments for immune and underpins Celltech’s goal of becoming a inflammatory disorders and cancer. global biotechnology leader, which will be furthered by the successful Celltech is focused on maximising value development and commercialisation of its from its products by marketing its own key late-stage development product, products to specialist prescribers through CDP870, and by the rapid progression of its extensive US and European its promising early-stage pipeline commercial operations and by accessing products. 1 Chairman’s Statement 2 Chief Executive’s Statement 3 2003 Highlights 4 Development Portfolio Contents 6 Operational Review – Research and Development 14 Operational Review – Global Commercial 18 Financial Review 24 Board of Directors 26 Directors’ Report -

Europe's Pharmaceutical Industry an Innovation

EUROPEAN INNOVATION MONITORING SYSTEM (ElMS) ElMS PUBLICATION N° 32 EUROPE'S PHARMACEUTICAL INDUSTRY AN INNOVATION PROFILE BY SPRU, U Diversity of Sussex, UK EUROPEAN COMMISSION DIRECTORATE GENERAL XIII - The Innovation Programme -)( U,j uJ (..) ElMS Project N° 94/114 ... .. ! w THIS STUDY WAS COMMISSIONED BY THE I EUROPEAN COMMISSION, I DIRECTORATE-GENERAL "TELECOMMUNICATIONS, INFORMATION MARKET AND ExPLOITATION OF RESEARCH", UNDER THE INNOVATION PROGRAMME STUDY FINISHED ON: AUGUST96 © 1996, European Commission {'15 b: Ytir/17 I ., Ii • !' .. Contents Page 1 Introduction 1 2 Current Developments in the Pharmaceutical Industry 2 3 Major Market and Technology Trends 12 4 Firm Level Analysis 24 5 Biotechnology - A New Route to Drug Discovery 40 6 Alliances, Linkages and Technology Transfer 49 7 Conclusions 56 REFERENCES 61 Tables: 1: Trends in R&D Intensity of the Pharmaceuticals Sector 4 2: Major Take-overs 1990-1996 8 3: Top Twelve World Market Share with Newly Merged Companies 9 4: Health Expenditure and Pharmaceutical Consumption in Developed Countries 13 5: Pharmaceutical Production in Major World Markets 15 6: R&D Intensity by Industry 18 7: Trends in the Distribution of Pharmaceutical R&D 19 8: Trends in the Distribution of US Patenting in Pharmaceuticals 21 9: Top 50 Branded Products by Country of Origin 23 10: Company Rankings by sales 1993 26 11: Changing Places -the world's top 20 pharmaceutical corporations 1976-94 27 12: Seller Concentration Ratios in the Pharmaceutical Industry 30 13: Top 20 companies in terms of Pharmaceutical R&D expenditures 31 14: Company market share in Europe, United States and Japan 34 15: Geographic Location of Pharmaceutical Firms' US Patenting Activities 37 16: Top Non-national firms patenting in Europe 38 17: Top Ten Biotechnology drugs on the Market in 1993 48 18: Alliances and Joint Ventures between US DBFs and leading European multinationals 50 19a: US-DBFs involved in biotechnology alliances 1982-91 '' . -

Delivering Precision Engineered Medicines

Delivering precision engineered medicines ANNUAL REPORT 2020 Silence Therapeutics Annual Report 2020 Therapeutics Annual Silence CONTENTS Welcome STRATEGIC REPORT Highlights 1 Our vision is to transform Chairman’s statement 2 Chief Executive Officer’s review 3 peoples’ lives around the world How RNAi Works 5 Our strategy 6 by silencing diseases through our Our pipeline 8 SLN360 for cardiovascular disease precision engineered medicines due to high lipoprotein(a) 9 SLN124 for iron loading anaemias 12 and driving positive change for Collaborations 14 Financial review 15 the communities around us. Principal risks 16 Corporate Social Responsibility 17 Resources and relationships 18 GOVERNANCE WHO WE ARE Board of Directors 20 We are pioneers in RNAi therapeutics with know-how accumulated Corporate Governance report 22 over two decades. Silence is proud to be a global and diverse company from our locations to our culture and expertise spanning Audit and Risk Committee report 26 across bioinformatics to drug discovery and clinical development. Remuneration Committee report 28 Directors’ Report 40 WHAT WE DO Statement of Directors’ responsibilities We are developing a deep pipeline of innovative siRNA therapies in respect of the financial statements 43 – in-house and with our partners – for diseases with a genetic basis. The depth and versatility of our mRNAi GOLD™ platform gives us the opportunity to address a wide range of conditions in FINANCIAL STATEMENTS virtually any therapeutic area. Independent auditors’ report to the members of Silence Therapeutics plc 44 OUR TECHNOLOGY Consolidated income statement 50 Our mRNAi GOLD™ platform leverages a naturally occurring Consolidated statement of process in the body, RNAi, to create medicines that precisely target comprehensive income 51 and ‘silence’ disease-associated genes in the liver. -

Faculty Disclosure

Faculty Disclosure In accordance with the ACCME Standards for Commercial Support, course directors, planning committees, faculty and all others in control of the educational content of the CME activity must disclose all relevant financial relationships with any commercial interest that they or their spouse/partner may have had within the past 12 months. If an individual refuses to disclose relevant financial relationships, they will be disqualified from being a part of the planning and implementation of this CME activity. Owners and/or employees of a commercial interest with business lines or products relating to the content of the CME activity will not be permitted to participate in the planning or execution of any accredited activity. Nature of Relevant Financial Relationship Last Name Role in Activity Commercial Interest What Was Received For What Role AbbVie, Inc., Prometheus Honoraria Consultant Laboratories Inc. Boland Planning Committee Janssen Biotech, Inc., Takeda Grant Research Pharmaceutical Company, Ltd. Textbook Lippincott, Oxford University Publications Press Royalties Advisory Board and Elsevier Bonakdar Faculty Honoria Editorial contributor Thorne Research Inc., Consulting Fee PracticeUpdate.com Metagenics, Inc., American Consultant in the Specialty Health area of pain Takeda Pharmaceutical Company, Cohen Faculty Honoraria Speaker Fee Ltd. Advisory Committee, AbbVie, Inc. Honoraria Speaker’s Bureau Collins Faculty Janssen Pharmaceutica Honoraria Speaker’s Bureau Takeda Pharmaceutical Company,