Consolidation Revisited Is the Founder of Managing Resources, a Date Received *In Revised Form) 8Th October, 2001 Consultancy Focused on the Life Science Industries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Biotechnology and the Economics of Discovery in the Pharmaceutical Industry

BIOTECHNOLOGY AND THE ECONOMICS OF DISCOVERY IN THE PHARMACEUTICAL INDUSTRY HELEN SIMPSON Office of Health Economics 12 Whitehall London SWlA 2DY ©October 1998. Office of Health Economics. Price £7.50 ISBN 1 899040 60 9 Printed by BSC Print Ltd, London. About the Author Helen Simpson is currently a researc~ economist at the Institute for Fiscal Studies and was formerly an economist at the Department of Trade and Industry. However, the opinions expressed here are her own and do not necessarily reflect the views of the IFS or of DTI officials or ministers. Acknowledgements This paper has been developed from my MPhil Economics thesis Scientist Entrepreneurs and the Finance of Biotech Companies. I would like to thank Margaret Meyer, Paul David and Gervas Huxley for their valuable suggestions. I am particularly grateful to Hannah Kettler and Jon Sussex for their advice and editorial inputs to the paper. My thanks also go to Adrian Towse and members of the OHE Editorial Board for their comments, and to the following individuals who gave me their insights into the pharmaceutical industry: Dr Trevor Jones, Director General, ABPI; Dr Janet Dewdney, Chairman, Adprotech; Dr Clive Halliday, Head of Global External Scientific Affairs, Glaxo Wellcome; Mr Alan Galloway, Head of Research Administration, Dr Nick Scott-Ram, Director of Corporate Affairs, and Dr Philip Huxley, all of British Biotech; Christine Soden, Finance Director, Chiroscience; Ian Smith, Lehman Brothers Pharmaceutical Research; and Paul Murray, 31. The Office of Health Economics Terms of Reference The Office of Health Economics (OHE) was founded in 1962. Its terms of reference are to: • commission and undertake research on the economics of health and health care; • collect and analyse health and health care data from the UK and other countries; • disseminate the results of this work and stimulate discussion of them and their policy implications. -

Programme 10.00 Registration 10.20 Welcome from the Host

Leadership Seminar: Respiratory and Inflammatory Diseases 22 September 2016 Penningtons Manches, 125 Wood Street, London EC2V 7AW Sponsored by Hosted by Programme 10.00 Registration 10.20 Welcome from the Host 10.30 Introduction Adrian Dawkes, PharmaVentures 10.45 Keynote presentations and discussion on unmet clinical needs including: 10.45 Symptoms vs Disease Modification Approach Lars Larson, TranScrip 11.05 Prospects for the prevention and treatment of respiratory virus-induced exacerbations in asthma and COPD Garth Rapeport, Pulmocide 11.25 Eosinophil depletion with benralizumab (anti-IL-5R) for the management of Severe Asthma and Chronic Obstructive Pulmonary Disease (COPD) Suzanne Cohen, MedImmune 11.45 Breath Biopsy - Breath Volatile Organic Compounds (VOCs) as Markers for Respiratory Disease Billy Boyle, Owlstone Medical 12.05 Panel discussion and Q&A 12.30 Lunch and networking 14.00 Data Protection and Liability in Respiratory Connected Devices Oliver Bett, Penningtons Manches 14.20 Adaptive Design in Respiratory Clinical Trials – A Sponsor’s Business Case Alethea Wieland, Scope International 14.40 Development of Immunoassays and Point-of-Care Tests for the Measurement of Active Protease Biomarkers of Chronic Respiratory Disease David Ribeiro, ProAxsis 15.00 Aiming for the Lungs - Formulation Strategies for Delivery of Inhaled Biologics Charlotte Yates, Vectura 15.30 Tea, coffee and networking 16.00 Innovative therapeutic options 16.00 The Development of an IL-17BR therapeutic antibody for the treatment of Asthma and IPF David Matthews, MRC Technology 16.20 Mycobacterium Tuberculosis Derived Peptide as a Disease Modifying Therapy for Asthma Nicky Cooper, Peptinnovate 16.40 Closing Remarks and Drinks Reception 18.00 Event closes Speaker Profiles Oliver Bett Associate, Penningtons Manches Oliver is an associate in our IP, IT and commercial team of Penningtons Manches, based in the London office. -

The Impact of Secondary Innovation on Firm Market Value in the Pharmaceutical Industry

The Impact of Secondary Innovation on Firm Market Value in the Pharmaceutical Industry By: Maitri Punjabi Honors Thesis Economics Department The University of North Carolina at Chapel Hill March 2016 Approved: ______________________________ Dr. Jonathan Williams Punjabi 2 Abstract This paper analyzes the effect of the changing nature of innovation on pharmaceutical firm market value from the years 1987 to 2010 by using U.S. patent and claim data. Over the years, firms have started shifting focus from primary innovation to secondary innovation as new ideas and new compounds become more difficult to generate. In this study, we analyze the impact of this patent portfolio shift on the market capitalization of pharmaceutical firms. After using firm fixed effects and the instrumental variable approach, we find that there exists a strong positive relationship between secondary innovations and the market value of the firm– in fact, we find a stronger relationship than is observed between primary innovation and market value. When focusing on the different levels of innovation within the industry, we find that this relationship is stronger for less-innovative firms (those that have produced fewer patents) than it is for highly- innovative firms. We also find that this relationship is stronger for firms that spend less on research and development, complementing earlier findings that research productivity is declining over time. Punjabi 3 Acknowledgements I would primarily like to thank my adviser, Dr. Jonathan Williams, for his patience and constant support. Without his kind and helpful attitude, this project would have been a much more frustrating process. Through his knowledge of the industry, I have gained valuable insight and have learned a great deal about a unique and growing field. -

Mvx List.Pdf

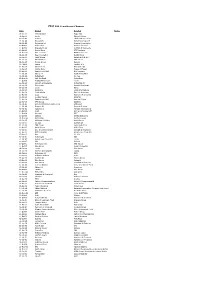

MVX_CODE manufacturer_name Notes status last updated date manufacturer_id AB Abbott Laboratories includes Ross Products Division, Solvay Inactive 16-Nov-17 1 ACA Acambis, Inc acquired by sanofi in sept 2008 Inactive 28-May-10 2 AD Adams Laboratories, Inc. Inactive 16-Nov-17 3 ALP Alpha Therapeutic Corporation Inactive 16-Nov-17 4 AR Armour part of CSL Inactive 28-May-10 5 AVB Aventis Behring L.L.C. part of CSL Inactive 28-May-10 6 AVI Aviron acquired by Medimmune Inactive 28-May-10 7 BA Baxter Healthcare Corporation-inactive Inactive 28-May-10 8 BAH Baxter Healthcare Corporation includes Hyland Immuno, Immuno International AG,and North American Vaccine, Inc./acquired somInactive 16-Nov-17 9 BAY Bayer Corporation Bayer Biologicals now owned by Talecris Inactive 28-May-10 10 BP Berna Products Inactive 28-May-10 11 BPC Berna Products Corporation includes Swiss Serum and Vaccine Institute Berne Inactive 16-Nov-17 12 BTP Biotest Pharmaceuticals Corporation New owner of NABI HB as of December 2007, Does NOT replace NABI Biopharmaceuticals in this codActive 28-May-10 13 MIP Emergent BioSolutions Formerly Emergent BioDefense Operations Lansing and Michigan Biologic Products Institute Active 16-Nov-17 14 CSL bioCSL bioCSL a part of Seqirus Inactive 26-Sep-16 15 CNJ Cangene Corporation Purchased by Emergent Biosolutions Inactive 29-Apr-14 16 CMP Celltech Medeva Pharmaceuticals Part of Novartis Inactive 28-May-10 17 CEN Centeon L.L.C. Inactive 28-May-10 18 CHI Chiron Corporation Part of Novartis Inactive 28-May-10 19 CON Connaught acquired by Merieux Inactive 28-May-10 21 DVC DynPort Vaccine Company, LLC Active 28-May-10 22 EVN Evans Medical Limited Part of Novartis Inactive 28-May-10 23 GEO GeoVax Labs, Inc. -

United States Securities and Exchange Commission Form 10-K Shire Pharmaceuticals Group

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K (Mark One) ፤ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 1999 អ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number 0-29630 SHIRE PHARMACEUTICALS GROUP PLC (Exact name of registrant as specified in its charter) England and Wales (State or other jurisdiction (I.R.S. Employer of incorporation or organization) Identification No.) N.A. East Anton, Andover, Hampshire SP10 5RG England (Address of principal executive offices) (Zip Code) 44 1264 333455 (Registrant's telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of exchange on which registered American Depository Shares, each representing Nasdaq National Market 3 Ordinary Shares, 5 pence nominal value per share Securities registered pursuant to Section 12(g) of the Act: None (Title of class) Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ፤ No អ Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant's knowledge, in definitive proxy or information statements incorporated by reference to Part III of this Form 10-K or any amendment to this Form 10-K. -

Appendix One the CELLTECH CASE STUDY

City Research Online City, University of London Institutional Repository Citation: Mc Namara, P. (2000). Managing the tension between knowledge exploration and exploitation: the case of UK biotechnology. (Unpublished Doctoral thesis, City University London) This is the accepted version of the paper. This version of the publication may differ from the final published version. Permanent repository link: https://openaccess.city.ac.uk/id/eprint/7870/ Link to published version: Copyright: City Research Online aims to make research outputs of City, University of London available to a wider audience. Copyright and Moral Rights remain with the author(s) and/or copyright holders. URLs from City Research Online may be freely distributed and linked to. Reuse: Copies of full items can be used for personal research or study, educational, or not-for-profit purposes without prior permission or charge. Provided that the authors, title and full bibliographic details are credited, a hyperlink and/or URL is given for the original metadata page and the content is not changed in any way. City Research Online: http://openaccess.city.ac.uk/ [email protected] Managing the Tension Between Knowledge Exploration and Exploitation: The Case of UK Biotechnology By Peter Mc Namara Presented in fulfilment of the requirements of the: Degree of Doctor of Philosophy Strategy and International Business City University Business School Department of Strategy and Marketing March 2000 TABLE OF CONTENTS ACKNOWLEDGEMENTS .......................................................................................................................... -

SHIRE PLC (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K [X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2009 [ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number 0-29630 SHIRE PLC (Exact name of registrant as specified in its charter) Jersey (Channel Islands) 98-0601486 (State or other jurisdiction of incorporation or (I.R.S. Employer Identification No.) organization) 5 Riverwalk, Citywest Business Campus, Dublin +353 1 429 7700 24, Republic of Ireland (Address of principal executive offices and zip code) (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of exchange on which registered American Depositary Shares, each representing three NASDAQ Global Select Market Ordinary Shares 5 pence par value per share Securities registered pursuant to Section 12(g) of the Act: None (Title of class) 1 Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes [X] No [ ] Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act Yes [ ] No [X] Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

United States Securities and Exchange Commission Washington, D.C

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K/A (Amendment No. 1) (Mark One) ☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2016 or ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File Number: 001-33500 JAZZ PHARMACEUTICALS PUBLIC LIMITED COMPANY (Exact name of registrant as specified in its charter) Ireland 98-1032470 (State or other jurisdiction of (I.R.S. Employer Identification incorporation or organization) No.) Fifth Floor, Waterloo Exchange Waterloo Road, Dublin 4, Ireland 011-353-1-634-7800 (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) Securities registered pursuant to Section 12(b) of the Act: Name of each exchange on Title of each class which registered Ordinary shares, nominal The NASDAQ Stock Market value $0.0001 per share LLC Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

Presentation Title Slide, No Image: One-Line Title Preferred

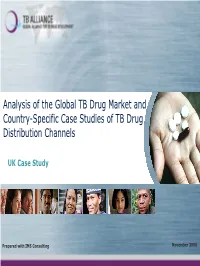

Analysis of the Global TB Drug Market and Country-Specific Case Studies of TB Drug Distribution Channels UK Case Study Prepared with IMS Consulting November 2006 Country table of contents • TB Control in the UK • Procurement and Distribution of TB Drugs • Value and Volume of the UK TB Market •Appendix 2 TB Control in the UK After years of increases, the incidence of TB in the UK has only recently begun to plateau • Prevalence and incidence of TB has been rising in the UK for more than 15 years • This has been attributed to increased migration from countries with high TB burden • The ageing UK population and increase in HIV/AIDS has also contributed Prevalence and incidence of TB and HIV/AIDS in the UK Distribution of age groups in the UK in 1971 RATE OF ANNUAL PERCENTAGE and 2004 NUMBER NUMBER OF TB CHANGE IN TB YEAR OF TB HIV/AIDS (PER NO. OF Age 1971 2004 CASES RATE CASES 100 000) CASES group 1999 5761 10.8 - - 41 585 Under 16 25% 19% 2000 6323 11.8 +9.8 +9.4 45 449 16-65 62% 65% 2001 6652 12.4 +5.2 +4.8 50 511 Over 65 13% 16% 2002 6861 12.7 +3.1 +2.4 56 738 2003 6837 12.5 -0.3 -1.0 64 005 Source: Health Protection Agency; www.avert.org; Office of National Statistics 3 T B C o TB casesnt are concentrated in in ro has by far thel in highest number of cases th e U K Prevalence and incid 3500 3000 S ASE2500 C F 2000 O R E B 1500 t M h U e U N 1000 K 500 (2003)e nce of TB across 0 London ner city areas -- West Midlands North West Sour East Midlands c e : Health Protecti Yorkshire&Humber 45 • South East T 40 he largest proportion (45%) of TB cas East of England 35 o n R Agen located in London 30 A • South West T E 25 ( c A London y P e North East 20 E majority of scases repo in the UK R occur in inner cities (there is 15 100 almost no incidence in rural Wales 10 000) locations). -

FTSE 100 Constituent History Updated

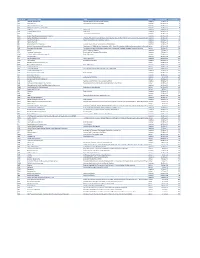

FTSE 100 Constituent Changes Date Added Deleted Notes 19-Jan-84 CJ Rothschild Eagle Star 02-Apr-84 Lonrho Magnet Sthrns. 02-Jul-84 Reuters Edinburgh Inv. Trust 02-Jul-84 Woolworths Barrat Development 19-Jul-84 Enterprise Oil Bowater Corporation 01-Oct-84 Willis Faber Wimpey (George) 01-Oct-84 Granada Group Scottish & Newcastle 01-Oct-84 Dowty Group MFI Furniture 04-Dec-84 Brit. Telecom Matthey Johnson 02-Jan-85 Dee Corporation Dowty Group 02-Jan-85 Argyll Group Berisford (S.& W.) 02-Jan-85 MFI Furniture RMC Group 02-Jan-85 Dixons Group Dalgety 01-Feb-85 Jaguar Hambro Life 01-Apr-85 Guinness (A) Enterprise Oil 01-Apr-85 Smiths Inds. House of Fraser 01-Apr-85 Ranks Hovis McD. MFI Furniture 01-Jul-85 Abbey Life Ranks Hovis McD. 01-Jul-85 Debenhams I.C. Gas 06-Aug-85 Bnk. Scotland Debenhams 01-Oct-85 Habitat Mothercare Lonrho 02-Jan-86 Scottish & Newcastle Rothschild (J) 08-Jan-86 Storehouse Habitat Mothercare 08-Jan-86 Lonrho B.H.S. 01-Apr-86 Wellcome EXCO International 01-Apr-86 Coats Viyella Sun Life Assurance 01-Apr-86 Lucas Harrisons & Crosfield 01-Apr-86 Cookson Group Ultramar 21-Apr-86 Ranks Hovis McD. Imperial Group 22-Apr-86 RMC Group Distillers 01-Jul-86 British Printing & Comms. Corp Abbey Life 01-Jul-86 Burmah Oil Bank of Scotland 01-Jul-86 Saatchi & S. Ferranti International 01-Oct-86 Bunzl Brit. & Commonwealth 01-Oct-86 Amstrad BICC 01-Oct-86 Unigate Smiths Industries 09-Dec-86 British Gas Northern Foods 02-Jan-87 Hillsdown Holdings Argyll Group 02-Jan-87 I.C. -

Overview of Ftc Actions in Pharmaceutical Products and Distribution*

OVERVIEW OF FTC ACTIONS IN PHARMACEUTICAL PRODUCTS AND DISTRIBUTION* Health Care Division Bureau of Competition Federal Trade Commission Washington D.C. 20580 Markus H. Meier Assistant Director Bradley S. Albert Deputy Assistant Director Kara Monahan Deputy Assistant Director September 2019 * Actions involving health care services and products are contained in a separate document, Overview of FTC Actions in Health Care Services and Products. Information about advisory opinions in the health care and pharmaceutical sectors is contained in the document Topic and Yearly Indices of Health Care Antitrust Advisory Opinions by Commission and by Staff. TABLE OF CONTENTS I. INTRODUCTION ...............................................................................................................1 II. CONDUCT INVOLVING PHARMACEUTICAL PRODUCTS .......................................3 A. Monopolization ........................................................................................................3 B. Agreements Not to Compete ..................................................................................14 III. CONDUCT INVOLVING PHARMACEUTICAL DISTRIBUTION ..............................20 A. Monopolization ......................................................................................................20 B. Agreements on Price and Price-Related Terms .....................................................20 C. Agreements to Obstruct Innovative Forms of Health Care Delivery or Financing................................................................................................................27 -

Commercial Biotechnology: an International Analysis (January 1984)

Commercial Biotechnology: An International Analysis January 1984 NTIS order #PB84-173608 — Recommended Citation: Commercial Biotechnology: An International Analysis (Washington, D. C.: U.S. Congress, Office of Technology Assessment, OTA-BA-218, January 1984). Library of Congress Catalog Card Number 84-601000 For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, D.C. 20402 — Foreword This report assesses the competitive position of the United States with respect to Japan and four European countries believed to be the major competitors in the commercial development of “new biotechnology.” This assessment continues a series of OTA studies on the competitiveness of U.S. industries. It was requested by the House Committee on Science and Technology and the Senate Com- mittee on Commerce, Science, and Transportation. Additionally, a letter of support for this study was received from the Senate Committee on Labor and Human Resources. New biotechnology, as defined in this report, focuses on the industrial use of recombinant DNA) cell fusion, and novel bioprocessing techniques. These techniques will find applications across many industrial sectors including pharmaceuticals, plant and animal agriculture, specialty chemicals and food additives, environmental applications, commodity chemicals and energy production, and bioelec- tronics. Over 100 new firms have been started in the United States in the last several years to capitalize on the commercial potential of biotechnology. Additionally, throughout the world, many established companies in a diversity of industrial sectors have invested in this technology. A well developed life science base, the availability of financing for high-risk ventures, and an entre- preneurial spirit have led the United States to the forefront in the commercialization of biotechnol- ogy.