Europe's Pharmaceutical Industry an Innovation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cholesterol How Kos Beat Big Pharma to HDL

The Other Cholesterol How Kos Beat Big Pharma to HDL www.pharmexec.com | ANADVANSTAR★ PUBLICATION Kos CEO Adrian Adams PHARMACEUTICAL EXECUTIVE Contents OCTOBER 2004 www.pharmexec.com Cover Story Under Construction Patrick Clinton Editor-in-Chief How Kos Pharmaceuticals turned a 50-year-old drug for raising HDL cholesterol into a brand-new, burgeoning business. Mulling the Future Kos CEO Adrian Adams, seated, maps strategy with key executives: (from left) Ralf Rosskamp, Christopher Kiritsy, Richard King, and Mark McGovern “We didn’t start with the idea of being a $200 million company. Growing as fast as possible: That was our goal from the get-go.” Kos Pharmaceuticals was first to market with a product to raise HDL cholesterol, and it wants to join pharma’s billion-dollar club by 2007. Big plan. Under Here’s how it’s going. Construction t’s hard to imagine that many pharma companies experienced more plain old good news this summer than Kos Pharmaceuticals. First, there were the second-quarter financials. Revenues for the quarter were $120.3 million, almost double last year’s figure. Net income for the quarter grew 245 percent to $38.5 million. The company raised its guidance for the year, predicting that full-year sales would be $480 million, 60 percent over last year— and CEO Adrian Adams boasted that Kos was the fastest-growing specialty pharma company in the United States. A few weeks later came encouraging results from a Phase II trial of IKos’ new inhalable insulin product for diabetes, and recruitment began for pivotal trials of a new combination product to consolidate Kos’ position in the burgeoning cholesterol market. -

Board of Director Candidates

2021 Annual General Meeting Board of Director Candidates James I. Healy, M.D., Ph.D. (Current Board Member) James I. Healy, M.D., Ph.D. has served as a member of our board of directors since November 2014. Dr. Healy has been a General Partner of Sofinnova Investments, Inc. (formerly Sofinnova Ventures), a venture capital firm, since June 2000. Prior to June 2000, Dr. Healy held various positions at Sanderling Ventures, Bayer Healthcare Pharmaceuticals (as successor to Miles Laboratories) and ISTA Pharmaceuticals, Inc. Dr. Healy is currently on the board of directors of Bolt Therapeutics, Inc. (Nasdaq: BOLT), Coherus BioSciences, Inc. (Nasdaq: CHRS), Karuna Therapeutics, Inc. (Nasdaq: KRTX), Natera, Inc. (Nasdaq: NTRA), NuCana plc (Nasdaq: NCNA), ObsEva SA (Nasdaq: OBSV) and Y-mAbs Therapeutics, Inc. (Nasdaq: YMAB) and two private companies. Previously, he served as a board member of Amarin Corporation, Auris Medical Holding AG, Edge Therapeutics, Inc., Hyperion Therapeutics, Inc., InterMune, Inc., Iterum Therapeutics PLC, Anthera Pharmaceuticals, Inc., Durata Therapeutics, Inc., CoTherix, Inc., Movetis NV and several private companies. Dr. Healy holds an M.D. and a Ph.D. in Immunology from Stanford University School of Medicine and holds a B.A. in Molecular Biology and a B.A. in Scandinavian Studies from the University of California, Berkeley. Jan Møller Mikkelsen (Current Board Member) Jan Møller Mikkelsen founded Ascendis Pharma and has served as President and Chief Executive Officer as well as Board member since December 2007 and currently serves on the board of Visen. From 2002 to 2006, Mr. Mikkelsen served as President and Chief Executive Officer of LifeCycle Pharma A/S, now Veloxis Pharmaceuticals A/S, which was a publicly traded biotechnology company. -

Mvx List.Pdf

MVX_CODE manufacturer_name Notes status last updated date manufacturer_id AB Abbott Laboratories includes Ross Products Division, Solvay Inactive 16-Nov-17 1 ACA Acambis, Inc acquired by sanofi in sept 2008 Inactive 28-May-10 2 AD Adams Laboratories, Inc. Inactive 16-Nov-17 3 ALP Alpha Therapeutic Corporation Inactive 16-Nov-17 4 AR Armour part of CSL Inactive 28-May-10 5 AVB Aventis Behring L.L.C. part of CSL Inactive 28-May-10 6 AVI Aviron acquired by Medimmune Inactive 28-May-10 7 BA Baxter Healthcare Corporation-inactive Inactive 28-May-10 8 BAH Baxter Healthcare Corporation includes Hyland Immuno, Immuno International AG,and North American Vaccine, Inc./acquired somInactive 16-Nov-17 9 BAY Bayer Corporation Bayer Biologicals now owned by Talecris Inactive 28-May-10 10 BP Berna Products Inactive 28-May-10 11 BPC Berna Products Corporation includes Swiss Serum and Vaccine Institute Berne Inactive 16-Nov-17 12 BTP Biotest Pharmaceuticals Corporation New owner of NABI HB as of December 2007, Does NOT replace NABI Biopharmaceuticals in this codActive 28-May-10 13 MIP Emergent BioSolutions Formerly Emergent BioDefense Operations Lansing and Michigan Biologic Products Institute Active 16-Nov-17 14 CSL bioCSL bioCSL a part of Seqirus Inactive 26-Sep-16 15 CNJ Cangene Corporation Purchased by Emergent Biosolutions Inactive 29-Apr-14 16 CMP Celltech Medeva Pharmaceuticals Part of Novartis Inactive 28-May-10 17 CEN Centeon L.L.C. Inactive 28-May-10 18 CHI Chiron Corporation Part of Novartis Inactive 28-May-10 19 CON Connaught acquired by Merieux Inactive 28-May-10 21 DVC DynPort Vaccine Company, LLC Active 28-May-10 22 EVN Evans Medical Limited Part of Novartis Inactive 28-May-10 23 GEO GeoVax Labs, Inc. -

Medication Precautions

MEDICATION PRECAUTIONS If you want to be pro-active to decrease bruising during injection treatments such as Restylane, Botox and Mesotherapy; the following prescriptions and non-prescription medications may be discontinued for at least two weeks prior to having any injection procedure to ensure that your platelets have time to recover. These specific preparations have been found to affect your blood by decreasing the amount of time it takes for coagulation and decreasing the amount of red blood cell production which can lead to increased bruising. If you are taking any antiarthritics or anticoagulants for control of a medical disorder, you will need to consult your treating physician for recommendations as to the alternatives. If you must take these medications, appropriate determinations as to whether they may be a detriment during the procedure may be discussed. NONPRESCRIPTION MEDICATIONS • Aspirin combinations • Alka-Seltzer Effervescent Antacid & Pain Reliever (Miles Laboratories) • Alka-Seltzer (Flavored) Effervescent Antacid & Pain Reliever (Miles Laboratories) • Alka-Seltzer Extra Strength Effervescent Antacid & Pain Reliever (Miles Laboratories) • Anacin Analgesic Coated Caplets (Whitehall) • Anacin Analgesic Coated Tablets (Whitehall) • Anacin Maximum Strength Coated Analgesic Tablets (Whitehall) • Arthritis Pain Formula by the Makers of Anacin Analgesic Tablets and Caplets (Whitehall) • Arthritis Strength BC Powder (Block) • Ascriptin Tablets (Rorer) • Ascriptin A/D Tablets (Rorer) • Bayer Children’s Chewable Aspirin (Glenbrook) -

Editorial Board L

EDITORIAL BOARD L. LEON CAMPBELL, Editor-in-Chief University ofIllinois, Urbana L. S. BARON, Editor (1969) L. JOE BERRY, Editor (1968) Ifalter Reed Army Institute ofResearch, Washington, D.C. Bryn Mawr College, Bryn Mawr, Pa. R. D. DeMOSS, Editor (1970) University ofIllinois, Urbana R. L. Anderson (1969) Herman Friedman (1969) Robert C. Parlett (1969) Robert Austian (1969) Lorraine Friedman (1968) Harry D. Peck (1970) W. Lane Barksdale (1969) Ruth E. Gordon (1969) Michael J. Pelczar, Jr. (1969) S. S. Barkulis (1969) Joseph S. Gots (1969) H. J. Phaff (1969) Alan W. Berheimer (1969) Leonard Hayflick (1969) Roy Repaske (1969) Robert W. Bernlohr (1970) James G. Hirsch (1969) H. V. Rickenberg (1970) S. Gaylen Bradley (1969) John G. Holt (1969) C. F. Robinow (1969) Arnold F. Brodie (1970) Paul Howard-Flanders (1969) W. R. Romig (1969) Allan Campbell (1969) Jerard Hurwitz (1969) NM R. J. Salton (1969) George B. Chapman (1969) Arthur G. Johnson (1969) Russell W. Schaedler (1969) V. P. Cirillo (1970) Elliot Juni (1967) W. R. Sistrom (1969) A. J. Clark (1969) R. E. Kallio (1969) Louis DS. Smith (1968) V. W. Cochrane (1969) Carl Lamanna (1970) Paul F. Smith (1970) S. F. Conti (1969) Maurice Landy (1970) Roger Y. Stanier (1970) C. D. Cox (1969) H. S. Levinson (1969) M. P. Starr (1970) William J. Cromartie (1969) H. C. Lichstein (1970) B. A. D. Stocker (1969) Roy Curtiss m (1969) W. R. Lockhart (1969) Bernard S. Strauss (1969) A. L. Demain (1969) Donald G. Lundgren (1968) Curtis B. Thorne (1969) Eliznbe McCoy (1969) John A. DeMoss (1969) H. -

Biogen Idec Inc. (Exact Name of Registrant As Specified in Its Charter)

Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K (Mark One) ☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2003 or o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission file number: 0-19311 Biogen Idec Inc. (Exact name of registrant as specified in its charter) Delaware 33-0112644 (State or other jurisdiction of (I.R.S. Employer incorporation or organization) Identification No.) 14 Cambridge Center, Cambridge, Massachusetts 02142 (Address of principal executive offices) (Zip code) (617) 679-2000 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: None Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.0005 par value Series X Junior Participating Preferred Stock Purchase Rights (Title of class) Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No o Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. -

Alternatives to Animal Use in Research, Testing, and Education

Appendix Laboratory-Animal Facilities Fully Accredited by the American Association for Accreditation of Laboratory Animal Care As of April 1, 1985, there were 483 facilities listed Michigan: as fully accredited by the American Association for University of Michigan, Ann Arbor, Dearborn, Accreditation of Laboratory Animal Care (AAALAC) and Flint (New Lenox, IL). Institutions are categorized as univer- Wayne State University, Detroit sities, medical schools, combined facilities for health Missouri: sciences, veterinary schools, dental schools, colleges University of Missouri-Kansas City, Kansas City of pharmacy, colleges of biological science, colleges of Montana: arts, colleges of engineering, Veterans’ Administration University of Montana, Missoula medical centers, pharmaceutical manufacturers, gov- Nebraska: ernment laboratories, commercial laboratories, hos- University of Nebraska at Omaha, Omaha pitals, nonprofit research laboratories, or laboratory New York: animal breeders. The following list of AAALAC-accred- St. John’s University, Jamaica ited facilities numbers 538, as some institutions are State University of New York at Buffalo, Buffalo listed in more than one category. (Facilities receiving Rockefeller University, New York accreditation since April 1, 1985, are not listed.) North Carolina: Duke University, Durham Oklahoma: Universities Oral Roberts University, Tulsa (Programs serving an entire campus) Rhode Island: Brown University, Providence Alabama: South Carolina: University of Alabama, University University of South Carolina, -

Robert J. Desalvo Papers Business Combinations in the Cosmetic and Pharmaceutical Industries 1944

Robert J. DeSalvo Papers Business Combinations in the Cosmetic and Pharmaceutical Industries 1944 - 1990 Collection #107 Abstract Robert J. DeSalvo’s research focused on business combinations (acquisitions, mergers, and joint ventures in the cosmetic and pharmaceutical industries. This topic was the basis for his master’s thesis in pharmacy administration at the University of Pittsburgh and continued as a life-long interest. This collection consists of two series of notebooks that Dr. DeSalvo developed to record relevant business combinations. The first series records acquisitions, proposed acquisitions, mergers, and joint ventures for the period of 1944 –1990 in an alphabetical arrangement. The information on these entries is cumulative so that the history of an organization is collected in one place. The second series of notebooks is arranged in chronological blocks. The information is arranged alphabetically by the name of the acquirer. The name of the acquired (merged), type of combination (acquisition, proposed acquisition, joint venture) and the date is also provided. The information is cross-referenced between the two series so that the researcher can approach the information by the name of the parent company or chronologically. Dr. DeSalvo used this resource for many of his publications as well as his master’s thesis. A copy of these publications and his thesis make up the remainder of the collection. Donor Gift of Barbara DeSalvo, 2000 Biography Robert James DeSalvo was born on July 20, 1933 in Toledo, OH. He died on January 23, 1993 in Cincinnati, OH. DeSalvo graduated from high school in Toledo and attended pharmacy school at the University of Toledo where he received his B.S. -

Presentation Title Slide, No Image: One-Line Title Preferred

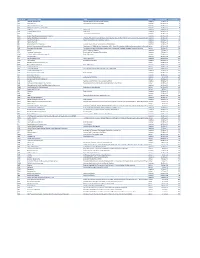

Analysis of the Global TB Drug Market and Country-Specific Case Studies of TB Drug Distribution Channels UK Case Study Prepared with IMS Consulting November 2006 Country table of contents • TB Control in the UK • Procurement and Distribution of TB Drugs • Value and Volume of the UK TB Market •Appendix 2 TB Control in the UK After years of increases, the incidence of TB in the UK has only recently begun to plateau • Prevalence and incidence of TB has been rising in the UK for more than 15 years • This has been attributed to increased migration from countries with high TB burden • The ageing UK population and increase in HIV/AIDS has also contributed Prevalence and incidence of TB and HIV/AIDS in the UK Distribution of age groups in the UK in 1971 RATE OF ANNUAL PERCENTAGE and 2004 NUMBER NUMBER OF TB CHANGE IN TB YEAR OF TB HIV/AIDS (PER NO. OF Age 1971 2004 CASES RATE CASES 100 000) CASES group 1999 5761 10.8 - - 41 585 Under 16 25% 19% 2000 6323 11.8 +9.8 +9.4 45 449 16-65 62% 65% 2001 6652 12.4 +5.2 +4.8 50 511 Over 65 13% 16% 2002 6861 12.7 +3.1 +2.4 56 738 2003 6837 12.5 -0.3 -1.0 64 005 Source: Health Protection Agency; www.avert.org; Office of National Statistics 3 T B C o TB casesnt are concentrated in in ro has by far thel in highest number of cases th e U K Prevalence and incid 3500 3000 S ASE2500 C F 2000 O R E B 1500 t M h U e U N 1000 K 500 (2003)e nce of TB across 0 London ner city areas -- West Midlands North West Sour East Midlands c e : Health Protecti Yorkshire&Humber 45 • South East T 40 he largest proportion (45%) of TB cas East of England 35 o n R Agen located in London 30 A • South West T E 25 ( c A London y P e North East 20 E majority of scases repo in the UK R occur in inner cities (there is 15 100 almost no incidence in rural Wales 10 000) locations). -

Consolidation Revisited Is the Founder of Managing Resources, a Date Received *In Revised Form) 8Th October, 2001 Consultancy Focused on the Life Science Industries

Alan Williams Consolidation revisited is the founder of Managing Resources, a Date received *in revised form) 8th October, 2001 consultancy focused on the life science industries. The Alan Williams company undertakes strategic assignments and also assists public and private sector clients with regulatory affairs, investor Abstract In 1998, the author produced two papers that argued that consolidation was relations and human a necessary activity for biotechnology companies to pay greater attention to. Three resources development. years later a further consideration of the subject seems worthwhile. Examples of Alan has also been an investment manager in successful consolidators are reviewed. a venture capital company, and held Keywords: consolidation, mergers, acquisitions marketing and licensing positions in Fisons. Introduction drink, vaccines and animal health but there is now greater focus on the highest In the early/mid-1970s, the pharmaceutical pro®tability sector, human pharmaceuticals. industry consisted of more than 100 At the time of writing, GSK is rumoured to research-based businesses of some be a possible purchaser of Bayer's signi®cant size, although none of them pharmaceutical business, the future of could convincingly claim a global presence. which has been questioned after the Typically, a leading company had a strong withdrawal of cerivastatin. position in its local market "examples Aventis, the eighth largest pharmaceutical included Merck and P®zer in the USA, company by sales in 2000,1 includes the Bayer in Germany, Beecham in the UK, operations of 1970s companies such as Roussel-Uclaf in France and Fujisawa in Rhone-Poulenc, Rorer, Fisons, Hoechst, Japan) and possibly some other Marion, Richardson Merrell, and some neighbouring countries "US companies in smaller companies. -

Board of Director Candidates

2017 Annual General Meeting Board of Director Candidates James I. Healy, M.D., Ph.D. (Current Board Member) James I. Healy, M.D., Ph.D. has served as a member of our board of directors since November 2014. Dr. Healy has been a General Partner of Sofinnova Ventures, a venture capital firm, since June 2000. Prior to June 2000, Dr. Healy held various positions at Sanderling Ventures, Bayer Healthcare Pharmaceuticals (as successor to Miles Laboratories) and ISTA Pharmaceuticals, Inc. Dr. Healy is currently on the board of directors of Auris Medical Holding AG, Coherus BioSciences, Inc., Edge Therapeutics, Inc., natera, Inc., ObsEva SA and several private companies. Previously, he served as a board member of Amarin Corporation, Hyperion Therapeutics, Inc., InterMune, Inc., Anthera Pharmaceuticals, Inc., Durata Therapeutics, Inc., CoTherix, Inc., Movetis NV and several private companies. Dr. Healy is currently a Director on the Board of the National Venture Capital Association (NVCA) and the Board of the Biotechnology Industry Organization (BIO). In 2011, Dr. Healy won the IBF Risk Innovator Award and was named as one of the industry’s top leading Life Science investors in 2013 by Forbes Magazine. Dr. Healy holds an M.D. and a Ph.D. in Immunology from Stanford University School of Medicine and holds a B.A. in Molecular Biology and a B.A. in Scandinavian Studies from the University of California, Berkeley. Jan Møller Mikkelsen (Current Board Member) Jan Møller Mikkelsen founded Ascendis Pharma and has served as our President and Chief Executive Officer and as a member of our board of directors since December 2007. -

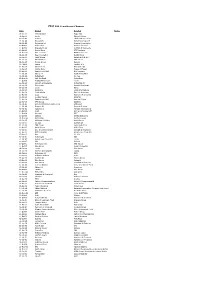

FTSE 100 Constituent History Updated

FTSE 100 Constituent Changes Date Added Deleted Notes 19-Jan-84 CJ Rothschild Eagle Star 02-Apr-84 Lonrho Magnet Sthrns. 02-Jul-84 Reuters Edinburgh Inv. Trust 02-Jul-84 Woolworths Barrat Development 19-Jul-84 Enterprise Oil Bowater Corporation 01-Oct-84 Willis Faber Wimpey (George) 01-Oct-84 Granada Group Scottish & Newcastle 01-Oct-84 Dowty Group MFI Furniture 04-Dec-84 Brit. Telecom Matthey Johnson 02-Jan-85 Dee Corporation Dowty Group 02-Jan-85 Argyll Group Berisford (S.& W.) 02-Jan-85 MFI Furniture RMC Group 02-Jan-85 Dixons Group Dalgety 01-Feb-85 Jaguar Hambro Life 01-Apr-85 Guinness (A) Enterprise Oil 01-Apr-85 Smiths Inds. House of Fraser 01-Apr-85 Ranks Hovis McD. MFI Furniture 01-Jul-85 Abbey Life Ranks Hovis McD. 01-Jul-85 Debenhams I.C. Gas 06-Aug-85 Bnk. Scotland Debenhams 01-Oct-85 Habitat Mothercare Lonrho 02-Jan-86 Scottish & Newcastle Rothschild (J) 08-Jan-86 Storehouse Habitat Mothercare 08-Jan-86 Lonrho B.H.S. 01-Apr-86 Wellcome EXCO International 01-Apr-86 Coats Viyella Sun Life Assurance 01-Apr-86 Lucas Harrisons & Crosfield 01-Apr-86 Cookson Group Ultramar 21-Apr-86 Ranks Hovis McD. Imperial Group 22-Apr-86 RMC Group Distillers 01-Jul-86 British Printing & Comms. Corp Abbey Life 01-Jul-86 Burmah Oil Bank of Scotland 01-Jul-86 Saatchi & S. Ferranti International 01-Oct-86 Bunzl Brit. & Commonwealth 01-Oct-86 Amstrad BICC 01-Oct-86 Unigate Smiths Industries 09-Dec-86 British Gas Northern Foods 02-Jan-87 Hillsdown Holdings Argyll Group 02-Jan-87 I.C.