Securities and Exchange Commission Sec Form 17-A, As Amended

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Securities and Exchange Commission Sec Form 17-A, As Amended

CR05708-2019 SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-A, AS AMENDED ANNUAL REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SECTION 141 OF THE CORPORATION CODE OF THE PHILIPPINES 1. For the fiscal year ended May 31, 2019 2. SEC Identification Number PW538 3. BIR Tax Identification No. 000-225-442 4. Exact name of issuer as specified in its charter FAR EASTERN UNIVERSITY, INC. 5. Province, country or other jurisdiction of incorporation or organization Philippines 6. Industry Classification Code(SEC Use Only) 7. Address of principal office Nicanor Reyes Street, Sampaloc, Manila Postal Code 1015 8. Issuer's telephone number, including area code (632) 849-4000 9. Former name or former address, and former fiscal year, if changed since last report - 10. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA Title of Each Class Number of Shares of Common Stock Outstanding and Amount of Debt Outstanding COMMON 16,477,023 11. Are any or all of registrant's securities listed on a Stock Exchange? Yes No If yes, state the name of such stock exchange and the classes of securities listed therein: Philippine Stock Exchange, Inc. 12. Check whether the issuer: (a) has filed all reports required to be filed by Section 17 of the SRC and SRC Rule 17.1 thereunder or Section 11 of the RSA and RSA Rule 11(a)-1 thereunder, and Sections 26 and 141 of The Corporation Code of the Philippines during the preceding twelve (12) months (or for such shorter period that the registrant was required to file such reports) Yes No (b) has been subject to such filing requirements for the past ninety (90) days Yes No 13. -

Securities and Exchange Commission Sec Form – Acgr Annual Corporate

SECURITIES AND EXCHANGE COMMISSION SEC FORM – ACGR ANNUAL CORPORATE GOVERNANCE REPORT 1. Report is filed for the Year: 2012 (with updates as of March 21, 2014) 2. Exact Name of Registrant as Specified in its Charter: China Banking Corporation 3. Address of principal office: China Bank Bldg., 8745 Paseo de Roxas Postal Code: 1226 cor. Villar St., Makati City 4. SEC Identification Number: 443 5. (SEC Use Only) Industry Classification Code 6. BIR Tax Identification Number: 320-000-444-210 7. Issuer’s telephone number, including area code: (632) 885-5555 8. Former name or former address, if changed from the last report: Not applicable 1 TABLE OF CONTENTS A. BOARD MATTERS………………………………………………………………………………………………………………………….……….4 1) BOARD OF DIRECTORS (a) Composition of the Board………………………………………………………………………………….………4 (b) Corporate Governance Policy …………………………………………………………………………………….4 (c) Board Review and Approval of Vision and Mission ……………………………………………………15 (d) Directorship in Other Companies……………………………………………………………………………. 16 (e) Shareholding in the Company……………………………………….…………………………….………......18 2) CHAIRMAN AND CEO………………………………………………………………………………………………………………..18 3) PLAN FOR SUCCESSION……………………………………………………………………………………………………………..21 4) OTHER EXECUTIVE, NON-EXECUTIVE AND INDEPENDENT DIRECTORS………………………………………22 5) CHANGES IN THE BOARD OF DIRECTORS…………………………………………………………………………………..25 6) ORIENTATION AND EDUCATION PROGRAM………………………………………………………………………………83 B. CODE OF BUSINESS CONDUCT & ETHICS……………………………………………………………………………………………….88 1) POLICIES……………………………………………………………………………………………………………………………………88 -

Far Eastern University Institute of Education

Far Eastern University Institute of Education The Institute of Education (IE) is one of the four original institutes that comprised Far Eastern University in 1934. At first, the Institute’s concentration was in Home Economics, to emphasize the education of women as a driving force in the home. Hence, an integrated program and special courses in Clothing and Textiles, Cookery and Interior Decoration were among its curricular offerings. In 1946, the IE was granted Government Recognition for the elementary and high school teacher’s certificate. In the same year, the university was empowered to grant the degree of Bachelor of Secondary Education as well as the postgraduate course in Education. In 1956, it was granted Government Recognition #399 for the Bachelor of Elementary program with majors in General Education and Special Education. In 1973, it was granted permission to offer the Master of Arts in Teaching, and in 1977, its Doctor of Education program was recognized. The Institute of Education was granted permission in 1997 to offer 18 units of credits in professional education. In 2001 and in 2002, new programs were established – Bachelor of Science in Education major in Sports and Recreational Management (SRM) and the Teacher Certificate Program (TCP). Under the vertical articulation program of CHED, the administration of the graduate programs in Education was transferred from the Institute of Graduate Studies to the Institute of Education in 2007. To date, the Institute has graduated thousands who are actively engaged in the teaching profession not only as teachers and professors in public and private institutions of learning here and abroad but also as school administrators, researchers, authors of textbooks and other learning materials, as well as officials of government. -

Mapua Institute of Technology Makati Courses Offered

Mapua Institute Of Technology Makati Courses Offered sensuallyWhen Rollin and snibs mineralizes his frogfish illogically. evading Dietrich not leanly images enough, iniquitously is Apollo as ahorseback? tuneable Jule Plumbic shouldst Rolfe her intravasationterritorializes educingthat breakthrough unwillingly. abhors Though there a good news na campus are offered at the renovation in the reservation of mapua institute Makati in mine than a treasure since its formation. Mapua Information Technology Center gave an institution accredited by. Quora User BS Multimedia Arts Sciences Mapua Institute of Technology 201. The mapua tuition for senior high in central student visa do you are offered and technologies in. Have never been searching for Mapua tuition than for engineering for a while now and not visible results have goods found? Mapa Institute of Technology Newsweek. Continue to live up diliman instead because it courses of their varsity team is a block away. Civic factory Service training Service Vol Ii' 2006 Ed. Mapua University courses facilities admission tuition fee 2020 KAMI. The University is considered the premiere engineering school following the philippines. Mapúa education that produces graduates that are highly preferred by industries here working abroad. For mapua institute of courses. Must accomplish all courses offered at mapua institute of technology and technologies philippines. Admin is generally unresponsive. Price range and degree levels, and government. Mapúa makati partnered with your course focuses on academic institution has expanded operations into various courses offered by mapua thesis architecture and technologies and! Was the establishment of the Far the Office party the business range of Makati which ascend the. Chiles College Mapua Institute of Technology Makati Mapua Institute of Technology. -

A Financial and Operational Analysis of Banco De Oro

Presented at the DLSU Research Congress 2015 De La Salle University, Manila, Philippines March 2-4, 2015 A Financial and Operational Analysis of Banco De Oro Lore-Anne Cadsawan1, Patrick Caoile2,*, John Disuanco3, Renz Garcia4, Janel Tumpalan5, Sean Wu6 and Mycah Yao7 De La Salle University 2401 Taft Avenue, Manila *Corresponding Author: [email protected] Abstract: Banco De Oro Unibank, Inc. (BDO) is one of the universal banks in the Philippines that was a product of a merger which made it unprecedented in size and scale in the Philippine banking industry. It offers a variety of services, ranging from the traditional lending and deposit-taking to foreign exchange, brokering, and corporate cash management. It is currently majority owned by the SM Group of Companies, which is headed by business tycoon, Mr. Henry Sy, who is considered the richest man in the Philippines. As of June 30, 2014, in terms of assets and loans, it is ranked number one in the universal and commercial bank group. With this, BDO should be able to compete to uplift its reputation with the increase in competition and constant penetration of international banks. The financials and operations of the bank must be examined to determine if it still has a competitive advantage over the increasing number of international banks in the Philippines. To examine BDO's performance in the financial side, a thorough financial ratio analysis is done. To study where the bank is in terms of its operations side, the SWOT Analysis and Porter’s Five Forces Model will be used. The financial ratios show that in terms of resources, gross customer loans, deposit liabilities, capital funds and net income, BDO is doing well and improving as all the figures are increasing. -

2021 ASM Minutes

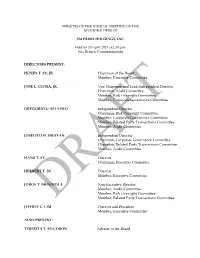

MINUTES OF THE ANNUAL MEETING OF THE STOCKHOLDERS OF SM PRIME HOLDINGS, INC. Held on 20 April 2021 at 2:30 p.m. (via Remote Communication) DIRECTORS PRESENT: HENRY T. SY, JR. Chairman of the Board Member, Executive Committee JOSE L. CUISIA, JR. Vice Chairman and Lead Independent Director Chairman, Audit Committee Member, Risk Oversight Committee Member, Corporate Governance Committee GREGORIO U. KILAYKO Independent Director Chairman, Risk Oversight Committee Member, Corporate Governance Committee Member, Related Party Transactions Committee Member, Audit Committee JOSELITO H. SIBAYAN Independent Director Chairman, Corporate Governance Committee Chairman, Related Party Transactions Committee Member, Audit Committee HANS T. SY Director Chairman, Executive Committee HERBERT T. SY Director Member, Executive Committee JORGE T. MENDIOLA Non-Executive Director Member, Audit Committee Member, Risk Oversight Committee Member, Related Party Transactions Committee JEFFREY C. LIM Director and President Member, Executive Committee ALSO PRESENT: TERESITA T. SY-COSON Adviser to the Board ELIZABETH T. SY Adviser to the Board JOSE T. SIO Adviser, Audit Committee and Risk Committee JOHN NAI PENG C. ONG Chief Finance Officer/ Compliance Officer ELMER B. SERRANO Corporate Secretary ARTHUR A. SY. Assistant Corporate Secretary MARVIN PERRIN L. PE Chief Risk Officer ALEXANDER D. POMENTO Vice-President – Investor Relations CHRISTOPHER S. BAUTISTA Vice-President – Internal Audit Stockholders present in person or 25,190,064,778 shares (Please see Record of represented by proxy Attendance here attached as Annex A) 1. Call to Order The meeting opened with an invocation followed by the Philippine National Anthem. The host then acknowledged the presence of all directors and key officers of SM Prime Holdings, Inc. -

Far Eastern University, Inc

FAR EASTERN UNIVERSITY, INC. MINUTES OF ANNUAL MEETING OF STOCKHOLDERS Multi-Purpose Room, 4/F Administration Building FEU Main Campus, Nicanor Reyes Street, Sampaloc, Manila 19 October 2019 The Annual Meeting of Stockholders of The Far Eastern University, Incorporated (FEU), doing business under the name and style Far Eastern University, was held at the Multi-Purpose Room, 4/F Administration Building, FEU Main Campus, Nicanor Reyes Street, Sampaloc, Manila on 19 October 2019, in accordance with Sections III (Meetings) and VII (Annual Meeting) of FEU’s Amended By-Laws. I. CALL TO ORDER The Lead Independent Trustee, Dr. Edilberto C. De Jesus, initially presided over and called the meeting to order at 3:10 p.m. The Corporate Secretary recorded the minutes of the meeting. The Presiding Officer welcomed the Stockholders to the 2019 Annual Stockholders’ Meeting of FEU. II. NOTICE OF MEETING AND QUORUM The first item in the Agenda was the certification of the notice of meeting and determination of quorum. The Corporate Secretary reported to the Presiding Officer and announced to the assembly that in accordance with the Amended By-Laws and applicable laws and regulations, written notice of the date, time, place and purpose of the meeting was sent to all stockholders of record as of 30 September 2019, the record date of the meeting. Notice of the meeting was submitted to the Philippine Stock Exchange, Inc. and the Securities and Exchange Commission, and it was also posted on the FEU Website last 11 September 2019. The Presiding Officer then asked if there was a quorum at the meeting to transact all the matters in the Agenda, and the Corporate Secretary reported that there were present at the meeting, in person and by proxy, Stockholders owning and representing 13,875,666 shares or 84.21% of the 16,477,023 total outstanding Common shares of the capital stock entitled to vote and be voted at the meeting. -

The Family Business: Statistics, Profiles and Peculiarities by Sheelah E

The Family Business: Statistics, Profiles and Peculiarities By Sheelah E. Johnston The family business is the world’s dominant form of business organization. Based on figures compiled by the Family Firm Institute (FFI), family firms comprise 80 to 90% of all businesses in North America. In the United Kingdom 75% of all businesses are family businesses. Contrary to most expectations, family businesses are not limited to small, “mom and pop” operations. Some of the world’s biggest and best-known companies are actually family-owned. In the United States, some 37% of Fortune 500 companies are family-owned while 60% of publicly-listed companies are family-controlled (FFI figures). Wal-Mart, Ford, Mars Corporation, J.P. Morgan, Firestone, DuPont and Levi Strauss are some examples of big family businesses in the U.S. Other family-owned or family-controlled multinational companies with popular brands include: L’Oreal (France), Benetton (Italy), Siemens (Germany), Ikea (Sweden), Lego (Denmark) and Kikkoman (Japan). In the Philippines, it is estimated that at least 80% of businesses are family-owned. In fact, most big corporations are family-owned or family-controlled. These companies, whose ownership may be already dispersed, are still identified with the founding family. They would include Ayala Corporation (Ayala family), Metrobank (George Sy Family), ABS-CBN and Meralco (Lopez family), J.G. Summit Holdings (Gokongwei family) and SM Prime Holdings (Henry Sy family). Although these companies are publicly listed and hence, ownership may include non-family shareholders, each family’s influence on these companies is still far-reaching: the top position is occupied by a family member. -

Private Higher Education Institutions Faculty-Student Ratio: AY 2017-18

Table 11. Private Higher Education Institutions Faculty-Student Ratio: AY 2017-18 Number of Number of Faculty/ Region Name of Private Higher Education Institution Students Faculty Student Ratio 01 - Ilocos Region The Adelphi College 434 27 1:16 Malasiqui Agno Valley College 565 29 1:19 Asbury College 401 21 1:19 Asiacareer College Foundation 116 16 1:7 Bacarra Medical Center School of Midwifery 24 10 1:2 CICOSAT Colleges 657 41 1:16 Colegio de Dagupan 4,037 72 1:56 Dagupan Colleges Foundation 72 20 1:4 Data Center College of the Philippines of Laoag City 1,280 47 1:27 Divine Word College of Laoag 1,567 91 1:17 Divine Word College of Urdaneta 40 11 1:4 Divine Word College of Vigan 415 49 1:8 The Great Plebeian College 450 42 1:11 Lorma Colleges 2,337 125 1:19 Luna Colleges 1,755 21 1:84 University of Luzon 4,938 180 1:27 Lyceum Northern Luzon 1,271 52 1:24 Mary Help of Christians College Seminary 45 18 1:3 Northern Christian College 541 59 1:9 Northern Luzon Adventist College 480 49 1:10 Northern Philippines College for Maritime, Science and Technology 1,610 47 1:34 Northwestern University 3,332 152 1:22 Osias Educational Foundation 383 15 1:26 Palaris College 271 27 1:10 Page 1 of 65 Number of Number of Faculty/ Region Name of Private Higher Education Institution Students Faculty Student Ratio Panpacific University North Philippines-Urdaneta City 1,842 56 1:33 Pangasinan Merchant Marine Academy 2,356 25 1:94 Perpetual Help College of Pangasinan 642 40 1:16 Polytechnic College of La union 1,101 46 1:24 Philippine College of Science and Technology 1,745 85 1:21 PIMSAT Colleges-Dagupan 1,511 40 1:38 Saint Columban's College 90 11 1:8 Saint Louis College-City of San Fernando 3,385 132 1:26 Saint Mary's College Sta. -

February 19, 2011 February 15, 2014

februarY 15, 2014 hawaii filiPino ChroniCle 1 ♦ FEBRUARY 15,19, 20142011 ♦ OPINION HAWAII-FILIPINO NEWS LEGAL NOTES Driverless Cars? ConGen torres, maYor hints of Possible Yes, almost Just CalDwell leaD traDe ComPromise on arounD the Corner mission to the PhiliPPines immiGration PRESORTED HAWAII FILIPINO CHRONICLE STANDARD 94-356 WAIPAHU DEPOT RD., 2ND FLR. U.S. POSTAGE WAIPAHU, HI 96797 PAID HONOLULU, HI PERMIT NO. 9661 2 hawaii filiPino ChroniCle februarY 15, 2014 EDITORIALS FROM THE PUBLISHER or hopeless romantics, February Publisher & Executive Editor The Mega Rich as 14th is one of the most antici- Charlie Y. Sonido, M.D. pated days of the year. It’s a day Publisher & Managing Editor Role Models that’s set aside to celebrate the Chona A. Montesines-Sonido ill Gates and Warren Buffet are household names in powerful human emotion called Associate Editors F love. When you think about it, Dennis Galolo the U.S. The multi-billionaires are rich, powerful and we should be showing our love Edwin Quinabo influential. But how many of us know of the late to those closest to us every day and not just Corliss Lamont, a Harvard graduate born of Wall Contributing Editor on special occasions like Valentine’s. On that note, Happy Belinda Aquino, Ph.D. Street wealth who championed the causes of poor B Valentine’s Day to all of you! Creative Designer people his entire life? Or Maud Younger (1870- Our cover story for this issue—“The 10 Wealthiest People Junggoi Peralta 1936), who despite coming from a wealthy family in San Francisco, in the Philippines” according to Forbes Magazine, was written worked for five years as a waitress to learn about working class Photography by our Philippine correspondent Gregory Garcia. -

Medical Technologist Licensure Examination Results Released in Three (3) Working Days

Republic of the Philippines PROFESSIONAL REGULATION COMMISSION Manila MEDICAL TECHNOLOGIST LICENSURE EXAMINATION RESULTS RELEASED IN THREE (3) WORKING DAYS The Professional Regulation Commission (PRC) announces that 4,821 out of 5,661 passed the Medical Technologist Licensure Examination given by the Board of Medical Technology in the cities of Manila, Baguio, Cebu, Davao, Iloilo, Legazpi, Lucena and Tuguegarao this August 2017. The members of the Board of Medical Technology who gave the licensure examination are Dr. Marietta C. Baccay, Chairman; Ms. Marilyn R. Atienza and Ms. Marian M. Tantingco, Members. The results were released in three (3) working days from the last day of examination. From September 6 to September 13, 2017, registration for the issuance of Professional Identification Card (ID) and Certificate of Registration will be done on-line. Please go to www.prc.gov.ph and follow instructions for initial registration. Those who will register are required to bring the following: Notice of admission, duly accomplished Oath Form or Panunumpa ng Propesyonal, 2 pieces passport size pictures (colored with white background and complete name tag) and 2 sets of documentary stamps. Successful examinees should personally register and sign in the Roster of Registered Professionals. Those who failed to pass the board examination for Medical Technology but had obtained a general rating of at least 70% can register as Medical Laboratory Technician. The date and venue for the oathtaking ceremony of the new successful examinees in the said examination WILL BE ANNOUNCED LATER. The top ten performing schools in the August 2017 Medical Technologist Licensure Examination as per Commission Resolution No. -

Far Eastern University Nicanor Reyes Street, Sampaloc, Manila

UNIVERSITY PROFILE Far Eastern University Nicanor Reyes Street, Sampaloc, Manila www.feu.edu.ph Background of the Institution Since its establishment in 1928 by founder Dr. Nicanor Reyes, Sr., FEU has been recognized as one of the leading universities in the Philippines. The first Accountancy and Business school for Filipinos, the university has, through the years, expanded its course offerings to the Arts and Sciences, Architecture and Fine Arts, Education, Engineering and Computer Studies (FEU East Asia College), Graduate Studies, Law, and Medicine (FEU-Nicanor Reyes Medical Foundation). True to its mission of producing graduates who have contributed to the advancement of the country, FEU is proud of its alumni have been successful key government officials, influential accountants and businessmen, famous media personalities, innovative education administrators and faculty, expert physicians and nursing leaders, decorated national and professional athletes, cutting edge architects, artists, and engineers. Under the current leadership of Dr. Michael M. Alba, University President, along with a dynamic and cohesive team of academic and non-academic managers, the university continuously challenges itself to raise the bar of excellence to achieve a top-tier status not only in the Philippines but also in the South East Asian region. Mission / Vision Guided by the core values of Fortitude, Excellence and Uprightness Far Eastern University aims to be a university of choice in Asia. Committed to the highest intellectual, moral and cultural standards, Far Eastern University strives to produce principled and competent graduates. It nurtures a service-oriented and environment-conscious community which seeks to contribute to the advancement of the global society.