Corporate Profile

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

SML Isuzu Ltd., Honda R&D Ltd

DEPARTMENT OF MECHANICAL NAAC ‘A’ GRADE ENGINEERING NIRF RANKED AICTE APPROVED 1 PUNJABI UNIVERSITY, PATIALA Punjabi University Patiala, one of the premier institutions of higher educationinthenorthofIndia,wasestablishedonthe30thApril, 1962 under the Punjabi University Act 1961. University has been awarded ‘A’ Grade Status by the National Assessment and Accreditation Council (NAAC) Lush Green, Pollution Free Environment Spread over 600 acres of land 2 DEPARTMENT OF MECHANICAL ENGINEERING Department of Mechanical Engineering was established at Punjabi University Campus in the year 2003. 3 DEPARTMENT OF MECHANICAL ENGINEERING Why Mechanical Engineering? Mechanical Engineers & professionals work in nearly every industry such as commercial, industrial, military or scientific companies. Job opportunities are available in both Software and Mechanical, Automobile, Chemical, Civil, Electronics, Shipping, Marine, Railways, Aviation, Defense, Agricultural companies. One may also enter into Research and Development. 4 DEPARTMENT OF MECHANICAL ENGINEERING Job Opportunities for Mechanical Engineers Wide array of career possibilities. Govt. Jobs – DRDO, Defense, Atomic Energy, ONGC, NTPC, Energy Sector, Railways, Engineers India Ltd. etc. Aerospace, Automotive, Agricultural and Manufacturing. Important emerging areas, such as Nuclear Technology, Robotics, Biomedical Technology, Automation, Mechatronics. Any engineering industry, consulting and management. 5 DEPARTMENT OF MECHANICAL ENGINEERING Why Mechanical Engineering? HIGHER STUDIES -

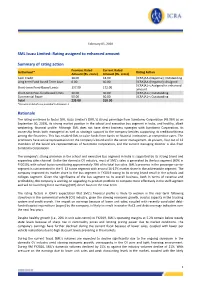

SML Isuzu Limited: Rating Assigned to Enhanced Amount Summary Of

February 05, 2020 SML Isuzu Limited: Rating assigned to enhanced amount Summary of rating action Previous Rated Current Rated Instrument* Rating Action Amount (Rs. crore) Amount (Rs. crore) Cash Credit 18.00 18.00 [ICRA]AA-(Negative); Outstanding Long term Fund based Term Loan 0.00 40.00 [ICRA]AA-(Negative); Assigned [ICRA]A1+; Assigned to enhanced Short-term Fund-Based Limits 137.00 172.00 amount Short-term Non-fund based limits 30.00 30.00 [ICRA]A1+; Outstanding Commercial Paper 50.00 50.00 [ICRA]A1+; Outstanding Total 235.00 310.00 *Instrument details are provided in Annexure-1 Rationale The rating continues to factor SML Isuzu Limited’s (SML’s) strong parentage from Sumitomo Corporation (43.96% as on September 30, 2019), its strong market position in the school and executive bus segment in India, and healthy, albeit weakening, financial profile. Although SML does not have direct business synergies with Sumitomo Corporation, its ownership lends both managerial as well as strategic support to the company besides supporting its creditworthiness among the financiers. This has enabled SML to raise funds from banks or financial institutions at competitive rates. The promoters have active representation on the company’s board and in the senior management. At present, four out of 12 members of the board are representatives of Sumitomo Corporation, and the current managing director is also from Sumitomo Corporation. The company’s strong presence in the school and executive bus segment in India is supported by its strong brand and expanding sales channel. Unlike the domestic CV industry, most of SML’s sales is generated by the bus segment (60% in FY2019), with school buses constituting approximately 70% of its total bus sales. -

FADA Releases July'21 Vehicle Retail Data

FEDERATION OF AUTOMOBILE DEALERS ASSOCIATIONS 804-805-806, Surya Kiran, 19, K G Marg New Delhi - 110 001 (INDIA) T +91 11 6630 4852, 2332 0095, 4153 1495 E [email protected] CIN U74140DL2004PNL130324 FOR IMMEDIATE RELEASE FADA Releases July’21 Vehicle Retail Data • Total vehicle retails for the month of July’21 rise by 34.12% on YoY basis. When compared to July’19 (a regular pre-covid month), recovery is visible as the deficit reduces to low double digits of -13.22%. • On YoY basis, all categories were in green with 2W up by 28%, 3W up by 83%, PV up by 63%, Tractor up by 7% and CV up by 166%. • After Tractors, PV for the first time shows strong numbers by clocking 24% growth when compared to pre-covid month of July’19. • FADA has been raising red flag about semi-conductor shortage since quite some time. The situation is now becoming grave with ever-increasing supply-side constraints. • rd The delta variant and a possibility of 3 wave continues to remain a threat for stable Auto Retails. 9th August’21, New Delhi: The Federation of Automobile Dealers Associations (FADA) today released Vehicle Retail Data for July’21. July’21 Retails Commenting on how July’21 performed, FADA President, Mr. Vinkesh Gulati said, “With entire country now open, July continues to see robust recovery in Auto Retails as demand across all categories remain high. The low base effect also continues to play its part. With all categories in green, CV’s continue to see increase in demand specially in M&HCV segment with the Government rolling out infrastructure projects in many parts of the country. -

Innovations 19.3

INNOVATIONS 19.3 1 SOFTWARE INNOVATIONS Manual selection of connection pins This Expert mode function allows the user to configure the connection to a system by manually selecting the communication pins on the OBD or Deutsch 9-pin cable. In this way, this function offers the user an alternative to the connection offered by the software in the most common communication protocols. Only available for V8 and higher devices. Countdown timer During the execution of some functionalities, it is necessary to wait a certain period of time until performing any operation. From this version, in this type of steps, Jaltest offers a countdown timer with the set time. 2 Improvement in the interaction with buttons in action steps Safety considerations in hybrid and electric vehicles (HEV) These instructions appear when selecting a hybrid model, a high voltage element control system and when selecting high voltage components in the wiring diagram configurations. These are very important safety considerations when working in hybrid and electric vehicles. 3 NEW DIAGNOSIS AND SYSTEM FUNCTIONALITIES Take into account that this document is only a summary of the most important information of this new version. For more information, please visit Jaltest Report. TRUCK AND BUS DAF For Euro 6 models, in PCI UDS engine management system, there are new functions such as the performance assessment of the turbo actuator. In the EAS4 Ecofit UL2 exhaust gas treatment system, the diesel particulate filter regeneration and AdBlue/DEF dosing are highlighted. Operation diagrams in the ECS-DC6, EAS3 and EAS4 exhaust gas treatment systems from the brand. 4 IVECO For Euro 6 models, in the EDC 17 CV41 engine management system, the component replacement for new system variants is highlighted. -

SIAM: State of the Indian Automobile Industry

October 2014 Seoul State of the Indian Automobile Industry Latest Performance Review SIAM Society of Indian Automobile Manufacturers Performance & Growth A Presentation SIAM 2 Domestic Sales (number of vehicles) Passenger Vehicles : 2.5 Mn Commercial Vehicles : 0.63 Mn 2 Wheelers : 14.8 Mn 3 Wheelers : 0.48 Mn Industry Estimates Employment (Direct + Indirect) : 2 Mn+27 Mn Contribution to manufacturing GDP : 47.3% Investment from FY 09 - FY 14 : USD 13.5 Bn A SIAM Presentation Source: SIAM, IMACs 3 Segmentation: By Volume Segmentation: By Value Passenger Vehicles Commercial Vehicles (2,503,685) (632,738) 14% 3% 3% Three Wheelers (479,634) 51% 28% 19% 80% 2% Two Wheelers (14,805,481) Passenger Vehicles Commercial Vehicles Three Wheelers Two Wheelers A SIAM4 Presentation Source: SIAM SIAM Hindustan Motor Finance Fiat India Force General Motors India Corporation Volkswagen Automobiles, Motors 2.28 Ashok Leyland Ltd 0.06 India Pvt Ltd 0.42 0.11 0.02 1.62 Ford Hindustan Motors Toyota Kirloskar Motor India, Skoda Auto India 0.01 Tata Motors 5.36 3.29 0.58 5.84 Honda Cars India Renault India 7.04 1.68 Hyundai Motor India Nissan Motor 16.21 India 2.06 Isuzu Motors India 0.01 Mahindra & Mahindra Maruti Suzuki India 8.84 44.58 VECVs – Volvo 0.16 VECVs – Eicher AMW Motors Ashok Leyland 6.01 0.56 13.48 Force Motors 3.50 Isuzu Motors India 0.12 Mahindra & Mahindra 25.72 Tata Motors 47.40 Piaggio Vehicles SML Isuzu 1.03 2.04 Alto Swift Sl. Models Sep No 2014 (Sales Nos) Dzire Wagon R 1 Maruti Suzuki Alto 19,906 2 Maruti Suzuki Swift 17,265 Grand i10 -

Corporate Profile

SML ISUZU LIMITED Company Presentation B&K’s Annual Investor Conference 30th May, 2019 (Mumbai) Safe Harbor • This presentation and the accompanying slides (the “Presentation”), which have been prepared by the Company have been prepared solely for information purposes and do not constitute any offer, recommendation or invitation to purchase or subscribe for any securities, and shall not form the basis or be relied on in connection with any contract or binding commitment what so ever. No offering of securities of the Company will be made except by means of a statutory offering document containing detailed information about the Company. • This Presentation has been prepared by the Company based on information and data which the Company considers reliable, but the Company makes no representation or warranty, express or implied, whatsoever, and no reliance shall be placed on, the truth, accuracy, completeness, fairness and reasonableness of the contents of this Presentation. This Presentation may not be all inclusive and may not contain all of the information that you may consider material. Any liability in respect of the contents of, or any omissionfrom, this Presentation is expressly excluded. • Certain matters discussed in this Presentation may contain statements regarding the Company’s market opportunity and business prospects that are individually and collectively forward-looking statements. Such forward-looking statements are not guarantees of future performance and are subject to known and unknown risks, uncertainties and assumptions -

Investors Presentation AGM 2019

Welcome to Pricol Limited’s 8th Annual General Meeting 29 August 2019 Slide 1 Agenda Financial Performance FY 18‐19 & FY 19‐20 (Q1) New Business Wins Company Outlook FY 19‐20 Key Investments & New Plant Key Partnerships Slide 2 Financial Performance FY 18‐19 & FY 19‐20 (Q1) Slide 3 Standalone Financial Performance FY 18‐19: Operations . Pricol’s standalone revenue from operations grew by 10.30% and stood at INR 1297.90 crores in FY 18‐19 . However, Increase in raw material cost on account of electronics price surge, forex impact due to rupee weakening, fuel price surge and additional cost incurred for stock building for new plants as well as managing labour issues resulted in decrease in profit. Cash generation through operations is INR 73.99 crores in FY 18‐19 as against INR 74.46 crores in FY 17‐18. (In INR crores) Particulars FY 18‐19 FY 17‐18 FY 19‐20 Q1 Revenue from operations 1297.90 1176.71 303.06 (excluding excise duty) Profit / (Loss) before Tax 3.90 74.22 (4.40) (before exceptional item) EBITDA 91.22 107.46 25.16 % of Revenue 7.03% 9.13% 8.30% Slide 4 Standalone Financial Performance FY 18‐19: Total Revenue . Total revenue is INR 1383.91 crores in FY 18‐19, which includes the following: . Sale of land held as stock in trade to the tune of INR 11.84 crores . Sale of traded goods to the tune of INR 67.06 crores . Other income is to the tune of INR 5.93 crores . -

India EV Story Emerging Opportunities

India EV Story Emerging Opportunities India EV Story: EmergingOpportunities Contents Executive Summary 05 Indian Automobile Industry – An Overview 07 Electric Vehicles – Policy Structure 17 EVs in India – Towards Mission 2030 27 EV Chargers in India 39 Overview on EV Battery Segment 57 EV Opportunities for Norway in India 63 Abbreviations 69 Contact Us – Innovation Norway, India 70 About Feedback Consulting 71 Page 3 India EV Story: EmergingOpportunities Executive Summary This report is developed by Innovation Norway, to map the fast growing 'Electric Vehicles' sector in India. Here, we delve into the details of the Indian EV sector nuances and present to you an analysis on how you can ride the EV boom in the country. After interacting with various Norwegian companies and different stakeholders in the Indian EV space, we have put together for you a list of opportunities that can be explored in this high growth market. We hope this will bring you a step closer in realising your India ambition. The Indian Automobile Industry is currently ranked 5th largest in the world and is set to be the 3rd largest by 2030. The requirement of mobility in India is set to change dramatically in the near future to cater to the requirement of 1.30 billion+ population. The past modes of transport and infrastructure will not suffice in coming years. Recognising this aspect, the Government of India, is working towards developing a mobility option which is ‘Shared, Connected and ELectric’. There is an increased need to prepare for a green future for Indian mobility and reduce dependence on imported crude oil. -

To Vigorously Market Custom-Built Terra Vehicles

Contents 26 62 96 Editorial.............................................................................................................................. 8 Cover story Volvo Buses targets 25 per cent annual growth by 2015 ................................................ 10 Volvo focus on raising standard of Indian drivers ............................................................ 18 vehiCle Zone Jayalalithaa inaugurates Daimler’s Chennai plant .......................................................... 26 Shriram Automall contributes to CV fleet management efficiency ................................... 66 Force Motors-HPCL deal for genuine oil supply inked .................................................... 80 FoCus on Components Cummins Group’s 50-year saga of success in India ....................................................... 38 Firestone Industrial opens SBU unit in Gurgaon to expand operations ......................... 42 Omni Matrix servicing growing truck-trailer connector market......................................... 58 RSB Transmissions’ Lucknow plant goes on stream ....................................................... 74 Delphi-TVS consistent growth for over 20 years ............................................................. 78 Partnership with Spal to boost PAEI’s business prospects ............................................. 82 DeFeXpo 2012 Tata Motors’ latest combat vehicles displayed at DEFEXPO .......................................... 44 Ashok Leyland Defence unveils COLT, Stallion range of new vehicles .......................... -

Concentration in the Indian Automobile Industry

Pacific Business Review International Volume 11 Issue 9, March 2019 Concentration in the Indian Automobile Industry Neeraj Kumar Abstract Assistant Professor The Indian automobile industry occupies a prominent place in Indian Dept. of Economics, IBS Hyderabad, economy. It passed from different phases, the emergence of Telangana (India) indigenous automobile manufactures and self reliance before 1983 to Freedom to Grow after 1991 economic reforms. The present paper Pooja Choudhary analyzed the concentration ratio of each segment Indian automobile Independent Economics Researcher industry. It further investigated firm level market shares of each Hyderabad, Telengan (India) individual firm in their respective segment from 1991-92 to 2013-14. The study found that the economic reforms of 1991 dissolved the entry, exit and FDI restrictions which lead entry of foreign players and competition goes on increasing and the concentration ratio starts declining in Indian automobile industry. Keywords: Automobile, Structure, Concentration, Reforms JEL Classification: L620 Introduction Theoretically one can consider perfect competitive market as the ideal market where two pivot assumptions i) large numbers of seller (buyer) and ii) independently acting seller (buyer) prevailed. With the help of these two assumptions there is no possibility of discrepancy among price and marginal receipts to attain profit maximization. But, the markets of the real world differ mostly in the number of firms and their relative size. The public are concerned about industrial concentration, because they are concerned about its economic and political effects. The economist should, therefore, analyze at least the economic effects and assess their importance (Citovsky 1955). The industrial theory assumes that concentration is an important component of the market structure which further determines the conduct and performance of concerned firm or industry. -

![SML Isuzu Limited: Long Term Ratings Downgraded to [ICRA]A+ (Negative); Short Term Ratings Reaffirmed](https://docslib.b-cdn.net/cover/0984/sml-isuzu-limited-long-term-ratings-downgraded-to-icra-a-negative-short-term-ratings-reaffirmed-3420984.webp)

SML Isuzu Limited: Long Term Ratings Downgraded to [ICRA]A+ (Negative); Short Term Ratings Reaffirmed

August 20, 2020 SML Isuzu Limited: Long term ratings downgraded to [ICRA]A+ (Negative); short term ratings reaffirmed Summary of rating action Previous Rated Current Rated Instrument* Rating Action Amount (Rs. crore) Amount (Rs. crore) [ICRA]A+(Negative); Downgraded Cash Credit 18.00 18.00 from [ICRA] AA- (Negative) [ICRA]A+(Negative); Downgraded Long term Fund based Term Loan 40.00 40.00 from [ICRA] AA- (Negative) Short-term Fund-Based Limits 172.00 172.00 [ICRA]A1+; Reaffirmed Short-term Non-fund based limits 30.00 30.00 [ICRA]A1+; Reaffirmed Commercial Paper 50.00 50.00 [ICRA]A1+; Reaffirmed Total 310.00 310.00 *Instrument details are provided in Annexure-1 Rationale The rating downgrade factors in the expected deterioration in the financial risk profile of SML Isuzu Limited (SML) over the medium-term because of the sharp contraction likely in commercial vehicle (CV) sales. The domestic CV industry witnessed several headwinds during FY2020 with a subdued macro-economic environment, surplus capacity in the trucking system, cautious financing environment and regulatory developments related to emission norms. These headwinds were further compounded by the Covid-19 pandemic and its impact on the economy, and consequently demand for CVs. Accordingly, ICRA expects the domestic CV industry sales to contract further in the current fiscal. This would significantly impact earnings of CV OEMs like SML. After a relatively weak performance in FY2020, wherein revenues declined by 18% and OPM contracted to 0.8% (PY: 5.2%), SML is likely to witness further earnings contraction in FY2021, on account of challenges brought about by the pandemic. -

FADA Releases August'21 Vehicle Retail Data

FEDERATION OF AUTOMOBILE DEALERS ASSOCIATIONS 804-805-806, Surya Kiran, 19, K G Marg New Delhi - 110 001 (INDIA) T +91 11 6630 4852, 2332 0095, 4153 1495 E [email protected] CIN U74140DL2004NPL130324 FOR IMMEDIATE RELEASE FADA Releases August’21 Vehicle Retail Data Total vehicle retails for the month of August’21 rises by 14.48% on YoY basis. When compared to August’19 (a regular pre-covid month), retails are still down by -14.75%. On YoY basis, all categories were in green with 2W up by 6.66%, 3W up by 79.70%, PV up by 38.71%, Tractor up by 5.50% and CV up by 97.94%. Both Tractors as well as PVs continues to see robust demand as they grow by 35.98% and 31.67% when compared to August’19, a pre-covid month. FADA first raised demand supply mismatch in Jan’21 due to shortage of semi- conductors in few brands. This has now become a full-blown crisis with no light in sight. FADA warns of a lacklustre festive season specially for PV Dealers as inventory level continues to dip due to non-availability of the fast-moving variants. 7th September’21, New Delhi: The Federation of Automobile Dealers Associations (FADA) today released Vehicle Retail Data for August’21. August’21 Retails Commenting on how August’21 performed, FADA President, Mr. Vinkesh Gulati said, “Auto Dealers are facing the most challenging phase of their business career as Covid-19 after-effect continues to play spoil-sport. While until last year, when demand was a challenge, supply is becoming a bigger problem currently due to shortage of semi-conductors, even though there is high demand for passenger vehicles.