Annual Report 2011 CORPORATE PROFILE

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

China Sunergy Co., Ltd. (CSUN)

China Sunergy Co., Ltd. (CSUN) 20-F Annual and transition report of foreign private issuers pursuant to sections 13 or 15(d) Filed on 06/09/2008 Filed Period 12/31/2007 Table of Contents UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM 20-F (Mark One) ¨ Registration statement pursuant to Section 12(b) or 12(g) of the Securities Exchange Act of 1934 or x Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the fiscal year ended December 31, 2007. or ¨ Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the transition period from to or ¨ Shell company report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 Date of event requiring this shell company report Commission file number: 001-33433 CHINA SUNERGY CO., LTD. (Exact name of Registrant as specified in its charter) N/A (Translation of Registrant's name into English) Cayman Islands (Jurisdiction of incorporation or organization) No. 123 Focheng West Road Jiangning Economic & Technical Development Zone Nanjing, Jiangsu 211100, People's Republic of China (Address of principal executive offices) Ruennsheng Allen Wang, (86 25) 5276 6890, [email protected], No. 123 Focheng West Road Jiangning Economic & Technical Development Zone Nanjing, Jiangsu 211100, People's Republic of China (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of each -

Building for Tomorrow's Communities

Annual Report 2012 BUILDING FOR TOMORROW’S COMMUNITIES Annual Report 2012 Annual Report Commercial growth and corporate social responsibility are equally important imperatives for Henderson Land. With more than three decades of development excellence behind us, we continue to build on our strengths, creating vibrant projects for the communities of tomorrow in partnership with some of the world’s most renowned architects and designers. Contents 2 Corporate Profile 4 Awards & Accolades 6 Group Structure 7 Highlights of 2012 Final Results 21 10 Chairman’s Statement Wong The Review of Operations Chuk Business in Hong Kong Hang Gloucester 38 Land Bank 41 Property Development Road 48 Property Investment 56 Property Related Businesses Business in Mainland China 60 Land Bank 64 Progress of Major Development Projects 75 Major Investment Properties 82 Subsidiary & Associated Companies 94 Business Model and Strategic Direction 96 Financial Review artist’s impression artist’s impression Double Cove 104 Five Year Financial Summary 108 Sustainability and CSR artist’s impression 122 Corporate Governance Report The H Collection 133 Report of the Directors 150 Biographical Details of Directors and Senior Management 158 Report of the Independent Auditor 159 Accounts 254 Corporate Information The Arch of 257 Notice of Annual General Meeting Triumph 260 Financial Calendar Forward-Looking Statements This annual report contains certain statements that are forward- looking or which use certain forward-looking terminologies. Henderson These forward-looking statements are based on the current beliefs, assumptions and expectations of the Board of Directors of the Company regarding the industry and markets in which 688 it operates. These forward-looking statements are subject to The risks, uncertainties and other factors beyond the Company’s control which may cause actual results or performance to differ materially from those expressed or implied in such forward- artist’s impression artist’s impression artist’s impression Reach looking statements. -

5G for Trains

5G for Trains Bharat Bhatia Chair, ITU-R WP5D SWG on PPDR Chair, APT-AWG Task Group on PPDR President, ITU-APT foundation of India Head of International Spectrum, Motorola Solutions Inc. Slide 1 Operations • Train operations, monitoring and control GSM-R • Real-time telemetry • Fleet/track maintenance • Increasing track capacity • Unattended Train Operations • Mobile workforce applications • Sensors – big data analytics • Mass Rescue Operation • Supply chain Safety Customer services GSM-R • Remote diagnostics • Travel information • Remote control in case of • Advertisements emergency • Location based services • Passenger emergency • Infotainment - Multimedia communications Passenger information display • Platform-to-driver video • Personal multimedia • In-train CCTV surveillance - train-to- entertainment station/OCC video • In-train wi-fi – broadband • Security internet access • Video analytics What is GSM-R? GSM-R, Global System for Mobile Communications – Railway or GSM-Railway is an international wireless communications standard for railway communication and applications. A sub-system of European Rail Traffic Management System (ERTMS), it is used for communication between train and railway regulation control centres GSM-R is an adaptation of GSM to provide mission critical features for railway operation and can work at speeds up to 500 km/hour. It is based on EIRENE – MORANE specifications. (EUROPEAN INTEGRATED RAILWAY RADIO ENHANCED NETWORK and Mobile radio for Railway Networks in Europe) GSM-R Stanadardisation UIC the International -

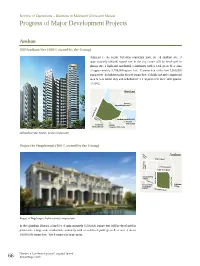

Progress of Major Development Projects

Review of Operations – Business in Mainland China and Macau Progress of Major Development Projects Anshan Old Stadium Site (100% owned by the Group) Adjacent to the scenic Yufoshan municipal park, an old stadium site of approximately 600,000 square feet in the city centre will be developed in phases into a high-end residential community with a total gross floor area of approximately 3,700,000 square feet. Construction of the first 1,200,000 square feet of residences plus 60,000 square feet of clubhouse and commercial area is now under way and scheduled for completion in the fourth quarter of 2013. Anshan Anshan International Hotel YuanlinHuaixiang Road Road Anshan Gateball Field Anshan Yufo Court Anshanshi Anshan Justice Bureau Laoganbu University Old Stadium Site, Anshan (artist’s impression) Project in Yingchengzi (100% owned by the Group) Hunan Street Anshan Yingcui Road Huihuayuan Road Yingcheng Cuijia North Road Gaoguanling Village Anxia Line Cuijia West Road West Cuijia Gaoguanling Cuijiatun Elementary Road Guihua Village School Kuanggong Road Project in Yingchengzi, Anshan (artist’s impression) In the Qianshan District, a land lot of approximately 5,500,000 square feet will be developed in phases into a large scale residential community with a total developable gross floor area of about 14,000,000 square feet. Site formation is in progress. Henderson Land Development Company Limited 66 Annual Report 2011 Review of Operations – Business in Mainland China and Macau • Progress of Major Development Projects Changsha The Arch of Triumph -

Spectator Guideguide

SpectatorSpectator GuideGuide Dear spectators, Welcome to Nanjing 2014 Summer Youth Olympic Games. In hot August, young athletes from around the world gather in the historically and culturally famous city of Nanjing, Jiangsu Province, to fly their dreams and “Share the Games, Share our Dreams”. Here, you can enjoy spectacular competitions, feel the spirit of the Youth Olympic Games and share the joy and passion of youth. Besides, you may participate in colourful CEP events to learn about traditional cultures and customs of Nanjing, its new city look, experience the hospitality of local residents and witness the integration of diverse cultures. This Guide contains event information, ticketing policy, entry rules, venue transport information, spectator services and city information so that you may have a better idea of the Competition and CEP Schedules and plan your schedule accordingly. Nanjing 2014 is a grand gala of youth, culture and sports. May the Games bring you friendship, passion and joy and wish you have a wonderful and memorable YOG journey! Li Xueyong President of Nanjing Youth Olympic Games Organising Committee YOG Spectator Guide Embark on Your YOG Journey Procedure Point for attention Relevant chapter As a key multi-sport event, the YOG have a number of specific requirements for all participants such as spectators and athletes. To make your YOG journey smooth and Please observe spectator rules for the venue order and enjoy the passion of YOG. convenient, please go through relevant information before attending the Games. Watch Information for Competition Please heed the specific requirements Spectators p21 of each event for spectators. Plan Your Visit Check your personal belongings and take everything with you. -

Bvb/06 - 20 Days

Fédération Internationale de Volleyball, Château Les Tourelles, Avenue Edouard Sandoz 2-4 1006 Lausanne, Switzerland Tel: +41 (21) 345 35 35 e-mail: [email protected] BVB/06 - 20 DAYS 2018 FIVB BEACH VOLLEBALL U19 WORLD CHAMPIONSHIPS, IN TANGSHAN, CHINA EVENT’S REGULATIONS This form must be approved by the FIVB 30 days before the start of the event and sent out -20 days by the Organizers to all participating NFs, FIVB Sponsors and FIVB Delegates via e-mail. Promoter Web site link to the event: http://www.fountask.com/ Event Social media accounts: http://weibo.com/u/5669760812 FIVB Web site link to the event: http://worldtour.2018.fivb.com/en/598 Address: Jiangsu Fountask Sports Technology Co. Ltd Contact Person:Guan Jian Mobile Number: +86 19951766114 PROMOTER Emergency mobile number: Email address: [email protected] Company`s Website :http://www.fountask.com/ Address: No.2, Tiyuguan Road, Beijing, 100763, China Contact Person: Xiang Qian Mobile Number: +86 13901314232 NATIONAL FEDERATION Emergency mobile number Email address: [email protected] National Federation Website: http://www.volleychina.org/ Address: Country Garden Phoenix City Hotel Contact Person: Guan Jian Event Office Mobile Number: +86 19951766114 Emergency mobile number: [email protected] Email address: http: [email protected] Contact Person: Li Zibo MAIN CONTACT FOR Mobile Number: +86 13015638358 THE PLAYERS Emergency mobile number Email address: [email protected] 1 ORGANISING COMMITTEE ORGANISING COMMITTEE LAST NAME/FIRST NAME MOBILE EMAIL Tournament -

Development of High-Speed Rail in the People's Republic of China

ADBI Working Paper Series DEVELOPMENT OF HIGH-SPEED RAIL IN THE PEOPLE’S REPUBLIC OF CHINA Pan Haixiao and Gao Ya No. 959 May 2019 Asian Development Bank Institute Pan Haixiao is a professor at the Department of Urban Planning of Tongji University. Gao Ya is a PhD candidate at the Department of Urban Planning of Tongji University. The views expressed in this paper are the views of the author and do not necessarily reflect the views or policies of ADBI, ADB, its Board of Directors, or the governments they represent. ADBI does not guarantee the accuracy of the data included in this paper and accepts no responsibility for any consequences of their use. Terminology used may not necessarily be consistent with ADB official terms. Working papers are subject to formal revision and correction before they are finalized and considered published. The Working Paper series is a continuation of the formerly named Discussion Paper series; the numbering of the papers continued without interruption or change. ADBI’s working papers reflect initial ideas on a topic and are posted online for discussion. Some working papers may develop into other forms of publication. Suggested citation: Haixiao, P. and G. Ya. 2019. Development of High-Speed Rail in the People’s Republic of China. ADBI Working Paper 959. Tokyo: Asian Development Bank Institute. Available: https://www.adb.org/publications/development-high-speed-rail-prc Please contact the authors for information about this paper. Email: [email protected] Asian Development Bank Institute Kasumigaseki Building, 8th Floor 3-2-5 Kasumigaseki, Chiyoda-ku Tokyo 100-6008, Japan Tel: +81-3-3593-5500 Fax: +81-3-3593-5571 URL: www.adbi.org E-mail: [email protected] © 2019 Asian Development Bank Institute ADBI Working Paper 959 Haixiao and Ya Abstract High-speed rail (HSR) construction is continuing at a rapid pace in the People’s Republic of China (PRC) to improve rail’s competitiveness in the passenger market and facilitate inter-city accessibility. -

UNIVERSITY of CALIFORNIA Santa Barbara Scribes in Early Imperial

UNIVERSITY OF CALIFORNIA Santa Barbara Scribes in Early Imperial China A dissertation submitted in partial satisfaction of the requirements for the degree Doctor of Philosophy in History by Tsang Wing Ma Committee in charge: Professor Anthony J. Barbieri-Low, Chair Professor Luke S. Roberts Professor John W. I. Lee September 2017 The dissertation of Tsang Wing Ma is approved. ____________________________________________ Luke S. Roberts ____________________________________________ John W. I. Lee ____________________________________________ Anthony J. Barbieri-Low, Committee Chair July 2017 Scribes in Early Imperial China Copyright © 2017 by Tsang Wing Ma iii ACKNOWLEDGEMENTS I wish to thank Professor Anthony J. Barbieri-Low, my advisor at the University of California, Santa Barbara, for his patience, encouragement, and teaching over the past five years. I also thank my dissertation committees Professors Luke S. Roberts and John W. I. Lee for their comments on my dissertation and their help over the years; Professors Xiaowei Zheng and Xiaobin Ji for their encouragement. In Hong Kong, I thank my former advisor Professor Ming Chiu Lai at The Chinese University of Hong Kong for his continuing support over the past fifteen years; Professor Hung-lam Chu at The Hong Kong Polytechnic University for being a scholar model to me. I am also grateful to Dr. Kwok Fan Chu for his kindness and encouragement. In the United States, at conferences and workshops, I benefited from interacting with scholars in the field of early China. I especially thank Professors Robin D. S. Yates, Enno Giele, and Charles Sanft for their comments on my research. Although pursuing our PhD degree in different universities in the United States, my friends Kwok Leong Tang and Shiuon Chu were always able to provide useful suggestions on various matters. -

Analyzing Influencing Factors of Transfer Passenger Flow of Urban Rail Transit

International Journal of Environmental Research and Public Health Article Analyzing Influencing Factors of Transfer Passenger Flow of Urban Rail Transit: A New Approach Based on Nested Logit Model Considering Transfer Choices Zhenjun Zhu 1, Jun Zeng 2,*, Xiaolin Gong 1, Yudong He 1 and Shucheng Qiu 1 1 College of Automobile and Traffic Engineering, Nanjing Forestry University, No.159 Longpan Road, Nanjing 210037, China; [email protected] (Z.Z.); [email protected] (X.G.); [email protected] (Y.H.); [email protected] (S.Q.) 2 School of Transportation, Southeast University, No.2 Dongnandaxue Road, Nanjing 211189, China * Correspondence: [email protected] Abstract: With the continuous improvement of the operation line network of urban rail transit, analyzing influencing factors of transfer passenger flow of urban rail transit is critical to improve the transfer demand analysis of urban rail transit. Using data collected from questionnaires, transfer passenger flow surveys and smart cards, this study proposes an approach base on nested logit passenger flow assignment model considering transfer choice behaviours of passengers. The transfer passenger flow at seven transfer stations in Nanjing is obtained. Subsequently, this study investigates the potential influencing factors of transfer passenger flow, including the node degree, geographic location (located in the city center, urban fringe, suburbs or suburban fringe), economic location Citation: Zhu, Z.; Zeng, J.; Gong, X.; (distance from the city center) and transportation locations (if it is close to a transportation hub or He, Y.; Qiu, S. Analyzing Influencing in combination with the hub) of rail transit transfer stations. The results indicate that a positive Factors of Transfer Passenger Flow of Urban Rail Transit: A New Approach correlation between the transfer passenger flow and the node degrees of transfer stations. -

Building Deformation Prediction Based on Ground Surface Settlements of Metro-Station Deep Excavation

Hindawi Advances in Civil Engineering Volume 2018, Article ID 6050353, 14 pages https://doi.org/10.1155/2018/6050353 Research Article Building Deformation Prediction Based on Ground Surface Settlements of Metro-Station Deep Excavation Dapeng Li and Changhong Yan School of Earth Sciences and Engineering, Nanjing University, No. 163 Xianlin Road, Qixia District, Nanjing, China Correspondence should be addressed to Dapeng Li; [email protected] Received 1 May 2018; Revised 30 August 2018; Accepted 13 September 2018; Published 10 October 2018 Guest Editor: Zhanguo Ma Copyright © 2018 Dapeng Li and Changhong Yan. *is is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited. Building deformations are not only closely related to the distance from the building to metro-station excavation but also related to the relative positions of the building and metro-station excavation. Building deformations can be predicted using ground surface settlement profiles. Based on typical geological parameters of Nanjing metro-station excavation, ground surface settlements were numerically simulated by auxiliary planes perpendicular and parallel to the excavation and by angled auxiliary planes at the excavation corner. Results show that the ground surface settlement profiles in auxiliary planes are closely related to the relative positions of the auxiliary planes and the metro-station excavation. Partitioning of ground surface settlements was proposed according to the three types of ground surface settlement profiles; furthermore, bending deformation and torsional deformation regularities of surrounding buildings were analyzed, and an estimation method for building settlements was developed. -

The World of Metro Rail in Pictures

THE WORLD OF METRO RAIL IN PICTURES "Dragon Boat Architecture" at Jiantan Metro Station, Taipei, Taiwan By Dr. F.A. Wingler, Germany, July 2020 Dr. Frank August Wingler Doenhoffstrasse 92 D 51373 Leverkusen [email protected] http://www.drwingler.com - b - 21st Century Global Metro Rail in Pictures This is Part II of a Gallery with Pictures of 21st Century Global Metro Rail, with exception of Indian Metro Rail (Part I), elaborated for a book project of the authors M.M. Agarwal, S. Chandra and K.K. Miglani on METRO RAIL IN INDIA . Metros across the World have been in operation since the late 1800s and transport millions of commuters across cities every day. There are now more than 190 Metro Installations globally with an average of about 190 million daily passengers. The first Metro Rail, that went underground, had been in London, England, and opened as an underground steam train for the public on 10st January 1863: llustration of a Train at Praed Street Junction near Paddington, 1863; from: History Today, Volume 63, Issue 1, January, 2013 Vintage London Underground Steam Train; Source “Made up in Britain” 1 Thed worl over, the 21st Century observed the opening of many new Metro Lines, the extension o f existing Metro Systems and the acquisition of modern Rolling Stocks, mostly in Asian Countries. In the last decades Urban Rail Transits in China developed fastest in the world. Urban Rail Transit in the People's Republic of China encompasses a broad range of urban and suburban electric passenger rail mass transit systems including subway, light rail, tram and maglev. -

长江yangtze River 长江长江yangtze River 麒麟有轨电车QILIN TRAM

六合开发区 雄州 方州广场 八百桥 S8 葛塘 LUHE DEVELOPMENT ZONE XIONGZHOU FANGZHOUGUANGCHANG BABAIQIAO GETANG 化工园 龙池 凤凰山公园 沈桥 金牛湖 HUAGONGYUAN LONGCHI FENGHUANGSHANGONGYUAN SHENQIAO JINNIUHU 大厂 DACHANG 卸甲甸 XIEJIADIAN 信息工程大学 NUIST 高新开发区 GAOXIN DEVELOPMENT ZONE 3 星火路 泰冯路 天润城 XINGHUOLU TAIFENGLU TIANRUNCHENG 林场 东大成贤学院 LINCHANG SEU CHENGXIAN COLLEGE 柳洲东路 LIUZHOUDONGLU 长 江 Yangtze River 泰山新村 S8 TAISHANXINCUN 上元门 SHANGYUANMEN 五塘广场 WUTANGGUANGCHANG 1 2 南大仙林校区 仙林湖 羊山公园 NJU XIANLIN CAMPUS 4 XIANLINHU 小市 YANGSHANGONGYUAN XIAOSHI 迈皋桥 MAIGAOQIAO 经天路 JINGTIANLU 红山动物园 HONGSHAN ZOO 仙林中心 XIANLINZHONGXIN 南京站 NANJING RAILWAY STATION 学则路 XUEZELU 西岗桦墅 XIGANGHUASHU 南京林业大学·新庄 王家湾 聚宝山 NFU / XINZHUANG WANGJIAWAN JUBAOSHAN 长 仙鹤门 XIANHEMEN 蒋王庙 JIANGWANGMIAO 新模范马路 XINMOFANMALU 江 玄武湖 徐庄 XUANWU LAKE XUZHUANG 南京工业大学 NANJING TECH UNIVERSITY 龙华路 玄武门 东流 LONGHUALU XUANWUMEN 汇通路 HUITONGLU DONGLIU 孟北 浦口万汇城 MENGBEI PUKOUWANHUICHENG 岗子村 4 云南路 鸡鸣寺 GANGZICUN 金马路 灵山 YUNNANLU JIMINGSI 钟 山 JINMALU LINGSHAN 文德路 ZHONGSHAN MOUNTAIN 10 WENDELU 龙江 草场门 鼓楼 九华山 临江 LONGJIANG CAOCHANGMEN GULOU JIUHUASHAN LINJIANG 雨山路 YUSHANLU 珠江路 浮桥 ZHUJIANGLU FUQIAO 马群 MAQUN 麒麟有轨电车 汉中门 新街口 西安门 QILIN TRAM HANZHONGMEN XINJIEKOU XI`ANMEN 上海路 大行宫 明故宫 苜蓿园 下马坊 孝陵卫 江心洲 SHANGHAILU DAXINGGONG MINGGUGONG MUXUYUAN XIAMAFANG XIAOLINGWEI JIANGXINZHOU 云锦路 YUNJINLU 绿博园 张府园 常府街 LÜBOYUAN 莫愁湖 ZHANGFUYUAN CHANGFUJIE MOCHOUHU 集庆门大街 JIQINGMENDAJIE 梦都大街 三山街 夫子庙 MENGDUDAJIE SANSHANJIE FUZIMIAO 兴隆大街 奥体中心 XINGLONGDAJIE OLYMPIC STADIUM 河西有轨电车 HEXI TRAM 武定门 WUDINGMEN 奥体东站 OLYMPIC STADIUM EAST 中华门 ZHONGHUAMEN 元通 雨花门 YUANTONG YUHUAMEN 中胜 麒麟有轨电车 ZHONGSHENG