Appendix 9A. the 100 Largest Arms-Producing Companies, 2003

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annu Al Repor T and Sus Tainabilit Y

SUSTAINABILITY REPORT ANNUAL REPORT AND 2014 “Overall, KONGSBERG had a good year in 2014, with good earnings and cash flows, growth in revenues, and record-high orders” 1 Introduction 8 Directors’ Report and Financial Statements 86 Corporate Governance 100 Shareholder’s information 104 Sustainability Report 149 Financial calendar and contact information CONTENT – ANNUAL REPORT AND SUSTAINABILITY REPORT 2014 Cover Key figures 2014 8 Directors’ Report and 86 Corporate Governance 104 Sustainability Report Financial Statements 87 The Board’s Report on 104 Content 1 Introduction 9 Short summary Business Corporate Governance 106 Introduction 2 Extreme Areas 88 Policy – Kongsberg Gruppen 118 Sustainable innovation performance for 10 Directors’ Report 2014 89 Articles of Association 123 What have we achieved? extreme conditions 25 Financial statements, – Kongsberg Gruppen 131 Systems of governance 4 President and CEO contents 90 The Board’s Report on The and key figures Walter Qvam 26 Consolidated financial Norwegian Code of Practice 6 This is KONGSBERG statements 149 Financial calendar and 73 Financial statements 100 Shareholder’s information contact information – Kongsberg Gruppen ASA 101 Shares and shareholders 83 Statement from the Board of Directors 84 Auditor’s Report KONGSBERG • Annual Report and Sustainability Report 2014 1 Introduction 8 Directors’ Report and Financial Statements 86 Corporate Governance 100 Shareholder’s information 104 Sustainability Report 149 Financial calendar and contact information KEY FIGURES 2014 2013 2012 2011 -

Kongsberg Gruppen ASA - Climate Change 2020

Kongsberg Gruppen ASA - Climate Change 2020 C0. Introduction C0.1 (C0.1) Give a general description and introduction to your organization. Kongsberg Gruppen (KONGSBERG) is an international technology group that delivers advanced and reliable solutions that improve safety, security and performance in complex operations and under extreme conditions. KONGSBERG works with demanding customers in the global defence, maritime, oil and gas, fisheries and aerospace sectors. The Group is divided into three business areas. Our headquarters is in Norway, and we have operations in more than 40 countries. Per 31. December 2019 we had almost 11 thousand employees, and total revenue was MNOK 24.081 (about 2.738 billion USD). Kongsberg Gruppen ASA is listed on the Oslo Stock Exchange and is subject to Norwegian securities legislation and stock exchange regulations. The Norwegian state owns 50.001 per cent of the shares in the company. KONGSBERG’s deliveries are often of strategic importance for our customers, and contribute to the satisfaction of important societal needs and development trends within sectors such as safety, energy, transport and climate. It is important for KONGSBERG to hold technological and product positions where we are either world-leading or have the potential to become world-leading in the long term. KONGSBERG’s strategic goal is to utilise our technologies to develop sustainable solutions for today’s societal challenges. Our deliveries are facilitating a green switch in shipping, optimal management of the ocean’s resources, monitoring of the condition of the oceans using data and information from satellites, as well as greater security for society. This is positioning KONGSBERG as a highly attractive employer for the recruitment of new talent for value creation and growth going forward. -

2017-2018 Annual Investment Report Retirement System Investment Commission Table of Contents Chair Report

South Carolina Retirement System Investment Commission 2017-2018 Annual Investment Report South Carolina Retirement System Investment Commission Annual Investment Report Fiscal Year Ended June 30, 2018 Capitol Center 1201 Main Street, Suite 1510 Columbia, SC 29201 Rebecca Gunnlaugsson, Ph.D. Chair for the period July 1, 2016 - June 30, 2018 Ronald Wilder, Ph.D. Chair for the period July 1, 2018 - Present 2017-2018 ANNUAL INVESTMENT REPORT RETIREMENT SYSTEM INVESTMENT COMMISSION TABLE OF CONTENTS CHAIR REPORT Chair Report ............................................................................................................................... 1 Consultant Letter ........................................................................................................................ 3 Overview ................................................................................................................................... 7 Commission ............................................................................................................................... 9 Policy Allocation ........................................................................................................................13 Manager Returns (Net of Fees) ..................................................................................................14 Securities Lending .....................................................................................................................18 Expenses ...................................................................................................................................19 -

Vanguard Total World Stock Index Fund Annual Report October 31, 2020

Annual Report | October 31, 2020 Vanguard Total World Stock Index Fund See the inside front cover for important information about access to your fund’s annual and semiannual shareholder reports. Important information about access to shareholder reports Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of your fund’s annual and semiannual shareholder reports will no longer be sent to you by mail, unless you specifically request them. Instead, you will be notified by mail each time a report is posted on the website and will be provided with a link to access the report. If you have already elected to receive shareholder reports electronically, you will not be affected by this change and do not need to take any action. You may elect to receive shareholder reports and other communications from the fund electronically by contacting your financial intermediary (such as a broker-dealer or bank) or, if you invest directly with the fund, by calling Vanguard at one of the phone numbers on the back cover of this report or by logging on to vanguard.com. You may elect to receive paper copies of all future shareholder reports free of charge. If you invest through a financial intermediary, you can contact the intermediary to request that you continue to receive paper copies. If you invest directly with the fund, you can call Vanguard at one of the phone numbers on the back cover of this report or log on to vanguard.com. Your election to receive paper copies will apply to all the funds you hold through an intermediary or directly with Vanguard. -

ANNUAL REPORT and SUSTAIN ABILITY REPORT 2018 01 Year 2018 02 About 03 Sustainability 04 Corporate 05 Directors’ Report and KONGSBERG Governance Financial Statements

ANNUAL REPORT AND SUSTAIN ABILITY REPORT 2018 01 Year 2018 02 About 03 Sustainability 04 Corporate 05 Directors’ Report and KONGSBERG Governance Financial Statements 01 02 3 YEAR 2018 11 ABOUT KONGSBERG 4 Key Figures 2018 12 This is KONGSBERG 7 Important milestones 2018 14 Strategy and ambitions 8 President and CEO Geir Håøy 15 Vision 16 Our values 17 Corporate Executive Management 18 Business areas 28 The world of KONGSBERG 03 04 34 SUSTAINABILITY 75 CORPORATE GOVERNANCE 35 About the Sustainability Report 76 The Board’s Report on Corporate 36 Framework for the preparation of Governance Sustainability Report 77 Policy 37 Responsible Business Conduct 78 Articles of Association 38 Responsible Tax – our Tax Policy 79 Board of Directors 40 Organisation and Management Systems 80 The Board’s Report relating to “The 41 Focus areas 2018–2019 Norwegian Code of Practice for Corporate 67 Climate Statement and Key Figures Governance” 74 Auditor’s Report, Sustainability Interactive PDF with bookmarks Navigate in Contents and hyperlinked text (hyperlinks are underlined). You can 05 browse one page back or forward by using the arrows in the top right-hand corner. Use the menu button on the far left to go back to the table of contents. The chapters are also bookmarked, and you can find short cuts to these in the 92 DIRECTORS’ REPORT AND left-hand menu of the PDF Reader. FINANCIAL STATEMENTS 93 Directors’ Report 2018 111 Financial Statements and Notes 182 Statement from the Board 183 Auditor’s report 2018 187 Financial calendar 187 Contact KONGSBERG Annual -

Shipshaped Kongsberg Industry and Innovations in Deepwater

Shipshaped Kongsberg industry and innovations in deepwater technology, 1975-2007 by Stein Bjørnstad A dissertation submitted to BI Norwegian School of Management for the degree of PhD Series of Dissertations 7/2009 BI Norwegian School of Management Department of Innovation and Economic Organisation Stein Bjørnstad Shipshaped: Kongsberg industry and innovations in deepwater technology, 1975-2007 © Stein Bjørnstad 2009 Series of Dissertations 7/2009 ISBN: 978 82 7042 951 6 ISSN: 1502-2099 BI Norwegian School of Management N-0442 Oslo Phone: +47 4641 0000 www.bi.no Printing: Nordberg The dissertation may be ordered from our website www.bi.no (Research – Research Publications) 2 Abstract Shipshaped is a thesis on the emergence of an innovative offshore supplier industry. Multiple influences combined to the success of various techniques to extract oil and gas without fixed platforms; this thesis put particular emphasis on the relaxation of hierarchies in fostering innovation. Such disintegration occurred within firms in which empowered employees took on larger responsibilities and between firms. The pace of innovation accelerated where people were allowed to sort out things themselves rather than conforming to directions from above. Initially these conditions were more evident in offshore support services serviced by shipping companies, but practices pioneered in shipping eventually spread to the proper offshore oil industry. Two business units at Kongsberg, Albatross and Kongsberg Offshore, serves as a vantage point for this thesis. Kongsberg Offshore pioneered production systems that help oil companies control the flow of petroleum from a valve tree on the seabed rather than on fixed platforms. Albatross pioneered dynamic positioning, a technique that helps shipping companies maintain their position using propellers rather than mooring lines and anchors. -

KOG †Rsrapport 99 Orig

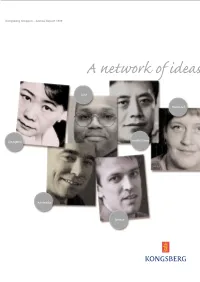

Kongsberg Gruppen – Annual Report 1999 Kongsberg Gruppen A network of ideas USA Kongsberg Gruppen ASA P.O. Box 1000 Denmark N-3601 KONGSBERG Annual Report 1999 Telephone: + 47 32 28 82 00 Fax: +47 32 28 82 01 www.kongsberg.com [email protected] Singapore South Korea Australia Greece Contents: Our international presence . 3 This is Kongsberg Gruppen . 5 Key Figures . 6 Highlights . 8 Directors’ Report . 10 Consolidated Accounts for Kongsberg Gruppen (The Group) . 17 Parent Company Accounts for Kongsberg Gruppen ASA . 30 Auditor’s Report . 32 Shares and shareholder relations . 34 Analytical Data . 36 Kongsberg Maritime . 40 Kongsberg Defence & Aerospace . 48 Business Development . 54 Property . 56 Addresses . 57 Financial calendar . 61 On the cover With their diversity, knowledge and enthusiasm, 3 400 employees in 20 countries work to generate added value for Kongsberg Gruppen, its shareholders and society-at-large. From top left: Lona Chang (46) – Finance Manager, Kongsberg Simrad Pte. Ltd. – Singapore Michael Santos Boyd (39) – Customer Support, Simrad Inc. – Seattle, Washington, USA Hwang-Yong Park (40) – Service Manager, Kongsberg Norcontrol Ltd. – Pusan, South Korea Maiken Thomassen (23) – Export Assistant, Simrad Shipmate AS - Støvring, Denmark Helge Morsund (47) – Program Manager Australia, Kongsberg Defence & Aerospace – Kongsberg, Norway Eirik Lie (33) – Project Manager Air Defence, Kongsberg Defence & Aerospace – Kongsberg, Norway 1 KOG Årsrapport 99 orig Eng 12.04.2000 09:49 Side 3 Our international presence Jan Erik Korssjøen We are proud to present the annual As a knowledge based corporation, it is CEO report for 1999. The year was charac- only natural that we pay close attention terised by strong performance in most to the development of high-technology of the Corporation's business areas, as based products. -

Kongsberg Gruppen – Powerpoint

Satellite Technology in Arctic governance Gunnar Pedersen and Richard Hall Kongsberg Satellite Services WORLD CLASS – through people, technology and dedication KSAT owner structure Kongsberg 50 % 50 % Norwegian Defense and Aerospace (KDA) Space Center (NCS) Kongsberg Satellite Services Tromsø Station SvalSat (Svalbard) Grimstad Station TrollSat (Antarctica) Business Segments Ground Station Services Earth Observation / 2 / 22-Oct-09 What does KSAT do? • Provide communications link for satellite owners • Uplink and downlink • Satellite commands go up • Data comes down • Exploit data received in real-time • Deliver the images anywhere in the world in real-time / 3 / 22-Oct-09 KSAT in the polar regions Trollsat 72° South Svalsat 78° North Tromsø 69° North / 4 / 22-Oct-09 Arctic Shipping and related Challenges • Safety, security and environment • Ice and icing • Metocean • Navigation in ice/ice infested waters • Knowledge about ships, their identity and position • Illegal pollution • Information access • Arctic area – large oceans - very few observation sites • Darkness and weather limit operations and information access • Communication and information distribution Satellite based monitoring - SAR ¾ Large area surveillance ¾ Independent of weather and light conditions ¾ Frequent overpassess in the high North (and South) ¾ Marine application: • Oil on sea • Vessels • Ice location • Ice condition Radarsat-2 • Wind • Waves / 6 / 22-Oct-09 Oil Service chain – main elements Sea state AIS for source identification Advanced processing Oil rigs, equipment installations, wrecks….. Know how , trained and experienced operators Auxiliary data / 7 / 22-Oct-09 Key users Coastal state authorities responsible for maritime surveillance Oil companies and oil industry associations / 8 / 22-Oct-09 Combining satellite images with AIS, (Automatic Identificaton System) -a powerful combination Oil spill outside the Norwegian coast, ships Combined with AIS, tracked back, one of the ship in the area. -

Defense News Top 100

Defense News Top 100 % of Last 2005 2005 2004 Revenue Rank Company Leadership Country Year’s Defense Total Defense from Rank Revenue* Revenue* Revenue** Defense Robert Stevens, President and 1 Lockheed Martin U.S. 1 36,465.0 37,213.0 98.0 34,050.0 CEO James McNerney, Chairman, 2 Boeing U.S. 2 30,791.0 54,845.0 56.1 30,464.0 President and CEO Ronald Sugar, Chairman and 3 Northrop Grumman U.S. 3 23,332.0 30,700.0 76.0 22,126.0 CEO 4 BAE Systems Mike Turner, CEO U.K. 4 20,935.2 26,500.2 79.0 20,344.0 William Swanson, Chairman 5 Raytheon U.S. 5 18,200.0 21,900.0 83.1 18,771.0 and CEO Nicholas Chabraja, Chairman 6 General Dynamics U.S. 6 16,570.0 21,244.0 78.0 15,000.0 and CEO Thomas Enders and Noël 7 EADS Netherlands 7 9,120.3 40,508.2 22.5 10,505.9 Forgeard, co-CEOs Michael Strianese, interim 8 L-3 Communications U.S. 13 8,549.2 9,444.7 90.5 6,133.8 CEO Denis Ranque, Chairman and 9 Thales France 9 8,523.3 12,176.1 70.0 8,868.6 CEO David Lesar, Chairman, 10 Halliburton 1 U.S. 10 7,552.0 20,994.0 36.0 8,000.0 President and CEO Pier Francesco Guarguaglini, 11 Finmeccanica Italy 11 7,125.7 12,728.1 56.0 7,670.6 Chairman and CEO George David, Chairman and 12 United Techologies U.S. -

Annual Report and Sustainability Report 2016 01 02 03 04 INTRODUCTION DIRECTORS’ REPORT & FINANCIAL STATEMENTS CORPORATE GOVERNANCE SUSTAINABILITY

01 02 03 04 INTRODUCTION DIRECTORS’ REPORT & FINANCIAL STATEMENTS CORPORATE GOVERNANCE SUSTAINABILITY ANNUAL REPORT & SUSTAINABILITY REPORT 2016 1 KONGSBERG • Annual Report and Sustainability Report 2016 01 02 03 04 INTRODUCTION DIRECTORS’ REPORT & FINANCIAL STATEMENTS CORPORATE GOVERNANCE SUSTAINABILITY • KONGSBERG • Vision, ambitions and values • Key figures • CEO Geir Håøy CONTENTS 01 02 INTRODUCTION 3 DIRECTORS’ REPORT & FINANCIAL STATEMENTS 14 KONGSBERG 3 Directors’ Report 2016 15 Vision, ambitions and values 5 Financial Statements and Notes 30 Key Figures 7 Statement from the Board 95 President and CEO Geir Håøy 10 Auditor’s Report 96 03 04 CORPORATE GOVERNANCE 100 SUSTAINABILITY 114 The Board’s report About the Sustainability Report 115 on Corporate Governance 101 Sustainable innovation 131 Policy 102 What have we achieved? 137 Articles of association 103 Climate and the environment 148 The Board’s report on the Norwegian Goals and reporting 152 Code of Practice for Corporate Governance 104 GRI 161 Auditor’s Report 166 This is an interactive PDF with bookmarks Navigate in Contents and hyperlinked text (hyperlinks are underlined by a dashed line). You can browse one page back or forward by using the arrows in the top left-hand corner. Use the menu button on the far left to go back to the table of contents. The chapters are also bookmarked, and you can find short cuts to these in the left-hand menu of the PDF Reader. 2 KONGSBERG • Annual Report and Sustainability Report 2016 01 02 03 04 INTRODUCTION DIRECTORS’ REPORT & FINANCIAL STATEMENTS CORPORATE GOVERNANCE SUSTAINABILITY • KONGSBERG • Vision, ambitions and values • Key figures • CEO Geir Håøy KONGSBERG Kongsberg Gruppen (KONGSBERG) is an international technology group that delivers advanced and reliable solutions improving safety, security and performance in complex operations and under extreme conditions. -

Financial Statements and Notes Statement from the Board Auditor’S Report

01 Year 2020 02 About 03 Sustainability 04 Corporate 05 Directors’ Report and KONGSBERG Governance Financial Statements Directors’ Report 2020 Financial Statements and Notes Statement from the Board Auditor’s Report Financial Statements and Notes Page Page KONGSBERG (GROUP) 135 Financial Statements and Notes 187 24 Cash and cash equivalents 136 Consolidated statement of income 188 25 Share capital 137 Consolidated statement of comprehensive income 189 26 Provisions 138 Consolidated statement of financial position 190 27 Other current liabilities as of 31 December 191 28 Assets pledged as collateral and guarantees 139 Consolidated statement of changes in equity 191 29 Statement on remuneration of the Group CEO 140 Consolidated statement of cash flow and Executive Management 141 Notes 194 30 Remuneration for Executive Management 141 1 General information and the Board 141 2 Basis for the preparation of the consolidated 197 31 Auditor’s fees financial statements 197 32 List of Group companies 142 3 Summary of significant accounting policies 199 33 Transactions with related parties 150 4 Fair value 200 34 Definitions and abbreviations 151 5 Management of capital and financial risks 201 35 Events after balance date 153 6 Discontinued operations 155 7 Acquisitions 158 8 Operating segments 161 9 Revenue recognition customer contracts KONGSBERG GRUPPEN ASA 165 10 Shares in joint arrangements and associated companies 202 Statement of income 166 11 Inventories 203 Statement of financial position as of 31 December 166 12 Personnel expenses 204 Statement -

Annual Report 2000

Kongsberg Gruppen – Annual Report 2000 Technology: (from the Greek teknologia) the science that refers to the various practices, methods and means used to convert ideas or raw materials into us- able products. Technology inspired by nature Our reasons for existence and profit- ability are contingent upon our ability to discover and develop useful applications for sophisticated technology products. Accordingly, technology is the main theme of this year's annual report. Cybernetics Software Signal processing Contents Technology . 1 Key figures . 2 Systems integration Key figures, by segment . 3 This is Kongsberg Gruppen . 4 World-class technology . 6 Vision, paramount objective and strategy . 7 Highlights . 9 Annual Report . 12 Annotated accounts for Kongsberg Gruppen (The Group) . 20 Annotated accounts for Kongsberg Gruppen ASA (The Parent Company) . 34 Auditor's report . .36 Shares and shareholder relations . .37 Analytical data . 40 Kongsberg Maritime . 46 Kongsberg Defence & Aerospace . 56 Business Development . .62 Property . 64 Addresses . 65 4 Ellen K. Ohren (25) – Graduate engineer, Kongsberg Defence & Aerospace AS Technology - products We earn our living by accepting challenges - thinking along new lines, moving beyond the ordinary to the realm of the extraordinary and thus remaining in the vanguard. We have learned to be humble in the face of the multitude of amazing solutions we see in nature, perceiving them as role models which inspire us not to give up until we achieve optimal results. Technology - markets Gunnar Thorsen (45) - Sales and Marketing Manager, We endeavour to serve the best interests of society and to Kongsberg Simrad AS pave the way for growth and prosperity among our customers.