Integrating Into Our Strategy

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Oil Refining in Mexico and Prospects for the Energy Reform

Articles Oil refining in Mexico and prospects for the Energy Reform Daniel Romo1 1National Polytechnic Institute, Mexico. E-mail address: [email protected] Abstract: This paper analyzes the conditions facing the oil refining industry in Mexico and the factors that shaped its overhaul in the context of the 2013 Energy Reform. To do so, the paper examines the main challenges that refining companies must tackle to stay in the market, evaluating the specific cases of the United States and Canada. Similarly, it offers a diagnosis of refining in Mexico, identifying its principal determinants in order to, finally, analyze its prospects, considering the role of private initiatives in the open market, as well as Petróleos Mexicanos (Pemex), as a placeholder in those areas where private enterprises do not participate. Key Words: Oil, refining, Energy Reform, global market, energy consumption, investment Date received: February 26, 2016 Date accepted: July 11, 2016 INTRODUCTION At the end of 2013, the refining market was one of stark contrasts. On the one hand, the supply of heavy products in the domestic market proved adequate, with excessive volumes of fuel oil. On the other, the gas and diesel oil demand could not be met with production by Petróleos Mexicanos (Pemex). The possibility to expand the infrastructure was jeopardized, as the new refinery project in Tula, Hidalgo was put on hold and the plan was made to retrofit the units in Tula, Salamanca, and Salina Cruz. This situation constrained Pemex's supply capacity in subsequent years and made the country reliant on imports to supply the domestic market. -

Climate and Energy Benchmark in Oil and Gas Insights Report

Climate and Energy Benchmark in Oil and Gas Insights Report Partners XxxxContents Introduction 3 Five key findings 5 Key finding 1: Staying within 1.5°C means companies must 6 keep oil and gas in the ground Key finding 2: Smoke and mirrors: companies are deflecting 8 attention from their inaction and ineffective climate strategies Key finding 3: Greatest contributors to climate change show 11 limited recognition of emissions responsibility through targets and planning Key finding 4: Empty promises: companies’ capital 12 expenditure in low-carbon technologies not nearly enough Key finding 5:National oil companies: big emissions, 16 little transparency, virtually no accountability Ranking 19 Module Summaries 25 Module 1: Targets 25 Module 2: Material Investment 28 Module 3: Intangible Investment 31 Module 4: Sold Products 32 Module 5: Management 34 Module 6: Supplier Engagement 37 Module 7: Client Engagement 39 Module 8: Policy Engagement 41 Module 9: Business Model 43 CLIMATE AND ENERGY BENCHMARK IN OIL AND GAS - INSIGHTS REPORT 2 Introduction Our world needs a major decarbonisation and energy transformation to WBA’s Climate and Energy Benchmark measures and ranks the world’s prevent the climate crisis we’re facing and meet the Paris Agreement goal 100 most influential oil and gas companies on their low-carbon transition. of limiting global warming to 1.5°C. Without urgent climate action, we will The Oil and Gas Benchmark is the first comprehensive assessment experience more extreme weather events, rising sea levels and immense of companies in the oil and gas sector using the International Energy negative impacts on ecosystems. -

Innovation Insights Brief 2019

Innovation Insights Brief 2019 NEW HYDROGEN ECONOMY - HOPE OR HYPE? ABOUT THE WORLD ENERGY COUNCIL ABOUT THIS INNOVATION INSIGHTS BRIEF The World Energy Council is the principal impartial This Innovation Insights brief on hydrogen is part of network of energy leaders and practitioners promoting a series of publications by the World Energy Council an affordable, stable and environmentally sensitive focused on Innovation. In a fast-paced era of disruptive energy system for the greatest benefit of all. changes, this brief aims at facilitating strategic sharing of knowledge between the Council’s members and the Formed in 1923, the Council is the UN-accredited global other energy stakeholders and policy shapers. energy body, representing the entire energy spectrum, with over 3,000 member organisations in over 90 countries, drawn from governments, private and state corporations, academia, NGOs and energy stakeholders. We inform global, regional and national energy strategies by hosting high-level events including the World Energy Congress and publishing authoritative studies, and work through our extensive member network to facilitate the world’s energy policy dialogue. Further details at www.worldenergy.org and @WECouncil Published by the World Energy Council 2019 Copyright © 2019 World Energy Council. All rights reserved. All or part of this publication may be used or reproduced as long as the following citation is included on each copy or transmission: ‘Used by permission of the World Energy Council’ World Energy Council Registered in England -

Hydrogen and Fuel Cells in Japan

HYDROGEN AND FUEL CELLS IN JAPAN JONATHAN ARIAS Tokyo, October 2019 EU-Japan Centre for Industrial Cooperation ABOUT THE AUTHOR Jonathan Arias is a Mining Engineer (Energy and Combustibles) with an Executive Master in Renewable Energies and a Master in Occupational Health and Safety Management. He has fourteen years of international work experience in the energy field, with several publications, and more than a year working in Japan as an energy consultant. He is passionate about renewable energies, energy transition technologies, electric and fuel cell vehicles, and sustainability. He also published a report about “Solar Energy, Energy Storage and Virtual Power Plants in Japan” that can be considered the first part of this document and is available in https://lnkd.in/ff8Fc3S. He can be reached on LinkedIn and at [email protected]. ABOUT THE EU-JAPAN CENTRE FOR INDUSTRIAL COOPERATION The EU-Japan Centre for Industrial Cooperation (http://www.eu-japan.eu/) is a unique venture between the European Commission and the Japanese Government. It is a non-profit organisation established as an affiliate of the Institute of International Studies and Training (https://www.iist.or.jp/en/). It aims at promoting all forms of industrial, trade and investment cooperation between the EU and Japan and at improving EU and Japanese companies’ competitiveness and cooperation by facilitating exchanges of experience and know-how between EU and Japanese businesses. (c) Iwatani Corporation kindly allowed the use of the image on the title page in this document. Table of Contents Table of Contents ......................................................................................................................... I List of Figures ............................................................................................................................ III List of Tables .............................................................................................................................. -

Quarterly Analyst Themes of Oil and Gas Earnings

Quarterly analyst themes of oil and gas earnings Q2 2021 ey.com/oilandgas Overview The recovery of oil and gas commodity markets and underleveraged and begin to return even more improved company performance continued in the cash to shareholders. As companies grapple with second quarter of 2021 with oil demand and OPEC+ low unlevered returns on renewable energy discipline resulting in a steady reduction in investments relative to oil and gas projects, the inventories and an increase in crude oil prices. matter of gearing is likely to re-emerge. Brent crude averaged US$69/bbl in the second On capital spending, analysts were interested in quarter, up 13% from the previous quarter and companies’ response to the improving macro- twice the average a year ago. Henry Hub averaged environment, specifically whether the companies US$2.95/mmBtu, down from US$3.50/mmBtu in were considering mobilizing additional upstream the first quarter as prices normalized after the investment with commodity prices returning to pre- extreme cold, but were up 50% from the beginning COVID-19 levels. Supply chain interruptions, labor to the end of the quarter, a trend that has market shortages and inflation concerns have continued into Q3. International gas markets begun to take center stage in economic news, and strengthened with northern Asia LNG prices oil and gas industry analysts checked for signs of averaging nearly US$10/mmbtu in 2Q21, driven by pricing pressure in the market for materials and strong growth in Chinese power demand, European services upstream and indications of how inventory rebuild and reduced hydroelectric output companies plan to offset the impact. -

Oil and Gas News Briefs, July 26, 2021

Oil and Gas News Briefs Compiled by Larry Persily July 26, 2021 Saudis want to be ‘last man standing’ as oil demand declines (Bloomberg; July 21) – Saudi Energy Minister Prince Abdulaziz bin Salman’s decisions after flying home from a tumultuous OPEC meeting in Vienna in March 2020 exposed a new Saudi policy — bolder, defiant of a growing global consensus on climate change, and more controlled by the royal family. They also reflected what Abdulaziz sees as his destiny: To ensure that the last barrel of oil on Earth comes from a Saudi well. As he said at a private event in June, according to a source, “We are still going to be the last man standing, and every molecule of hydrocarbon will come out.” All of this has huge implications for world energy markets. Abdulaziz, the first member of the royal family to be the kingdom’s energy minister, is the most important person in the oil market today. But a rancorous OPEC+ meeting in July showed just how difficult it’s going to be for him to consistently get his way in an era when oil-producing nations — their self-interests often in conflict — are contemplating a future of declining oil demand. Saudi Arabia’s power is under threat as the world seeks to move away from oil and other fossil fuels. Beneath the kingdom’s desert there are about 265 billion barrels of oil, worth almost $20 trillion at current prices. It’s a massive prize, but one that may be worthless someday if the global economy figures out how to keep churning without oil. -

Shell QRA Q2 2021

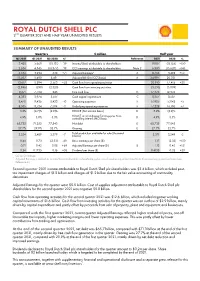

ROYAL DUTCH SHELL PLC 2ND QUARTER 2021 AND HALF YEAR UNAUDITED RESULTS SUMMARY OF UNAUDITED RESULTS Quarters $ million Half year Q2 2021 Q1 2021 Q2 2020 %¹ Reference 2021 2020 % 3,428 5,660 (18,131) -39 Income/(loss) attributable to shareholders 9,087 (18,155) +150 2,634 4,345 (18,377) -39 CCS earnings attributable to shareholders Note 2 6,980 (15,620) +145 5,534 3,234 638 +71 Adjusted Earnings² A 8,768 3,498 +151 13,507 11,490 8,491 Adjusted EBITDA (CCS basis) A 24,997 20,031 12,617 8,294 2,563 +52 Cash flow from operating activities 20,910 17,415 +20 (2,946) (590) (2,320) Cash flow from investing activities (3,535) (5,039) 9,671 7,704 243 Free cash flow G 17,375 12,376 4,383 3,974 3,617 Cash capital expenditure C 8,357 8,587 8,470 9,436 8,423 -10 Operating expenses F 17,905 17,042 +5 8,505 8,724 7,504 -3 Underlying operating expenses F 17,228 16,105 +7 3.2% (4.7)% (2.9)% ROACE (Net income basis) D 3.2% (2.9)% ROACE on an Adjusted Earnings plus Non- 4.9% 3.0% 5.3% controlling interest (NCI) basis D 4.9% 5.3% 65,735 71,252 77,843 Net debt E 65,735 77,843 27.7% 29.9% 32.7% Gearing E 27.7% 32.7% Total production available for sale (thousand 3,254 3,489 3,379 -7 boe/d) 3,371 3,549 -5 0.44 0.73 (2.33) -40 Basic earnings per share ($) 1.17 (2.33) +150 0.71 0.42 0.08 +69 Adjusted Earnings per share ($) B 1.13 0.45 +151 0.24 0.1735 0.16 +38 Dividend per share ($) 0.4135 0.32 +29 1. -

Sustainable Energy Transition: Opportunities Abound

1 PERSPECTI VE Sustainable energy transition: opportunities abound July 2021 For investment professionals only 2 On 18 May 2021, the International Energy Agency THE UTILITIES SECTOR IS ON THE RIGHT TRACK (IEA) published its report “Net Zero by 2050. A Utility companies are setting themselves apart from oil and Roadmap for the Global Energy Sector”. The IEA was gas companies in a positive sense. This is partly due to market established in 1974 as the oil sector watchdog of differences, other shareholders and more stringent Western countries. Over the past 47 years, this regulations. agency has mainly been considered a strong The table below shows that this does not necessarily affect supporter of fossil fuels. This is precisely why its returns. The table shows returns versus the capital employed. report came as a big surprise to the oil sector, While this is only one variable and the companies shown differ politicians, climate activists and investors alike. The in size, financial strategy, activities, etc., it does show that report outlines how carbon emissions could be there are opportunities to maintain returns on investments in sustainable activities. reduced to zero by 2050. That goal can be seen as a 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 GEM necessary condition for complying with the Paris O&G Royal Dutch Climate Agreement, which aims to limit global -6.87 6.68 9.13 5.50 2.58 1.73 6.81 7.65 12.95 15.68 11.46 8.02 6.78 Shell PLC o TotalEnergies warming to 1.5 C (above pre-industrial levels). -

Developing Hydrogen Fueling Infrastructure for Fuel Cell Vehicles: a Status Update

www.theicct.org BRIEFING OCTOBER 2017 Developing hydrogen fueling infrastructure for fuel cell vehicles: A status update This briefing provides a synthesis of information regarding the global development of hydrogen fueling infrastructure to power fuel cell vehicles. The compilation includes research on hydrogen infrastructure deployment, fuel pathways, and planning based on developments in the prominent fuel cell vehicle growth markets around the world. INTRODUCTION Governments around the world continue to seek the right mix of future vehicle technologies that will enable expanded personal mobility and freight transport with near-zero emissions. This move toward zero emissions is motivated by the simultaneous drivers of improving local air quality, protecting against increased climate change impacts, and shifting to local renewable fuel sources. Electricity-powered plug-in vehicles and hydrogen-powered fuel cell electric vehicles offer great potential to displace the inherently high emissions associated with the combustion of petroleum- based gasoline and diesel fuels. Hydrogen fuel cell electric vehicles offer a unique combination of features as a zero-emission alternative to conventional vehicles. Fuel cell powertrains, converting hydrogen to electric power to propel the vehicle, tend to be about twice as efficient as those on conventional vehicles. Hydrogen fuel cell vehicles are typically capable of long trips (i.e., over 500 kilometers or 300 miles) and a short refueling time that is comparable to conventional vehicles. Furthermore, fuel cell vehicles are expected to be less expensive than conventional vehicles in the long run. The Prepared by: Aaron Isenstadt and Nic Lutsey. BEIJING | BERLIN | BRUSSELS | SAN FRANCISCO | WASHINGTON ICCT BRIEFING diversity of fuel pathways to produce hydrogen allows for the use of lower-carbon, renewable, and nonimported sources. -

Low-Carbon Hydrogen: Sensing the Path Towards Large-Scale Deployment

Thematic Research Infrastructure | Green & Sustainable 15.12.2020 Low-carbon hydrogen: sensing the path towards large-scale deployment WRITTEN BY Ivan Pavlovic [email protected] research.natixis.com Marketing communication: This document is a marketing presentation. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research; and it is not subject to any prohibition on dealing ahead of the dissemination of investment research. RESEARCH Based around the world, Natixis CIB Research provides original, fundamental insights and analysis to inform clients’ investment and hedging decisions across all asset classes and produce marketing Asia is now theresearch new frontier with an integratedfor infrastructure view of markets to investing. Over betterthe last understand 12 months economic we’ve trends. seen many funds deploying teams in the region and there is clear investorGREEN appetite SUSTAINABLE with capital HUB raised for dedicated Asia focused funds. “The Green & Sustainable Hub is the cross- asset and operational team working alongside Corporate Investment Bank (CIB) Law Kwong-Wingbusiness lines. It co-originates and structures Head of Infrastructuregreen Finance & sustainable Asia Pacific, financing solutions Natixis (through bonds, credit or securitizations), engineers and develops investment products & solutions and provides clients advisory services”. gsh.cib.natixis.com research.natixis.com C2 - Internal Natixis Executive summary (1/5) Long presented as the ”energy carrier of the future” due to its abundance and absence of CO2 emissions upon combustion, hydrogen has apparently entered another era. While support plans have been multiplying across OECD countries to promote hydrogen-centric mobility, the molecule and its uses has been identified in Europe as a pillar for reviving the economy after the Covid-19 pandemic and achieving neutrality carbon by 2050, an essential condition for the achievement of the Paris Climate Agreement signed in December 2015. -

10.30% Pa JB Callable Multi Barrier

INDICATIVE KEY INFORMATION – 26 JULY 2021 1/10 10.30% P.A. JB CALLABLE MULTI BARRIER REVERSE CONVERTIBLE (65%) ON REPSOL SA, TOTALENERGIES SE, ROYAL DUTCH SHELL PLC (the "Products") SSPA SWISS DERIVATIVE MAP© / EUSIPA DERIVATIVE MAP© BARRIER REVERSE CONVERTIBLE (1230) CONTINUOUS BARRIER OBSERVATION – CASH SETTLEMENT – EUR – QUARTERLY CALLABLE This document is for information purposes only and until the Initial Fixing Date the terms are indicative and may be amended. A Product does not constitute a collective investment scheme within the meaning of the Swiss Federal Act on Collective Investment Schemes. Therefore, it is not subject to authorisation by the Swiss Financial Market Supervisory Authority FINMA ("FINMA") and potential investors do not benefit from the specific investor protection provided under the CISA and are exposed to the credit risk of the Issuer. I. Product Description Terms Swiss Security 112475275 Coupon 10.30% p.a. Number (Valor) Initial Fixing Date: 29 July 2021, being the date on which the ISIN CH1124752754 Initial Level and the Strike and the Barrier are fixed. Symbol MEQVJB Issue Date/Payment Date: 05 August 2021, being the date on which the Products are issued and the Issue Price is paid. Issue Size up to EUR 20,000,000 (may be increased/ decreased at any time) Final Fixing Date: 29 July 2022, being the date on which the Final Level will be fixed. Subscription Period 26 July 2021 – 29 July 2021, 16:00 CET Last Trading Date: 29 July 2022, until the official close on the SIX Swiss Exchange, being the last date on which the Products Issue Currency EUR may be traded. -

Statoil Business Update

Statoil US Onshore Jefferies Global Energy Conference, November 2014 Torstein Hole, Senior Vice President US Onshore competitively positioned 2013 Eagle Ford Operator 2012 Marcellus Operator Williston Bakken 2011 Stamford Bakken Operator Marcellus 2010 Eagle Ford Austin Eagle Ford Houston 2008 Marcellus 1987 Oil trading, New York Statoil Office Statoil Asset 2 Premium portfolio in core plays Bakken • ~ 275 000 net acres, Light tight oil • Concentrated liquids drilling • Production ~ 55 kboepd Eagle Ford • ~ 60 000 net acres, Liquids rich • Liquids ramp-up • Production ~34 koepd Marcellus • ~ 600 000 net acres, Gas • Production ~130 kboepd 3 Shale revolution: just the end of the beginning • Entering mature phase – companies with sustainable, responsible development approach will be the winners • Statoil is taking long term view. Portfolio robust under current and forecast price assumptions. • Continuous, purposeful improvement is key − Technology/engineering − Constant attention to costs 4 Statoil taking operations to the next level • Ensuring our operating model is fit for Onshore Operations • Doing our part to maintain the company’s capex commitments • Leading the way to reduce flaring in Bakken • Not just reducing costs – increasing free cash flow 5 The application of technology Continuous focus on cost, Fast-track identification, Prioritised development of efficiency and optimisation of development & implementation of potential game-changing operations short-term technology upsides technologies SHORT TERM – MEDIUM – LONG TERM • Stage