Mexico's Deep Water Success

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Oil Refining in Mexico and Prospects for the Energy Reform

Articles Oil refining in Mexico and prospects for the Energy Reform Daniel Romo1 1National Polytechnic Institute, Mexico. E-mail address: [email protected] Abstract: This paper analyzes the conditions facing the oil refining industry in Mexico and the factors that shaped its overhaul in the context of the 2013 Energy Reform. To do so, the paper examines the main challenges that refining companies must tackle to stay in the market, evaluating the specific cases of the United States and Canada. Similarly, it offers a diagnosis of refining in Mexico, identifying its principal determinants in order to, finally, analyze its prospects, considering the role of private initiatives in the open market, as well as Petróleos Mexicanos (Pemex), as a placeholder in those areas where private enterprises do not participate. Key Words: Oil, refining, Energy Reform, global market, energy consumption, investment Date received: February 26, 2016 Date accepted: July 11, 2016 INTRODUCTION At the end of 2013, the refining market was one of stark contrasts. On the one hand, the supply of heavy products in the domestic market proved adequate, with excessive volumes of fuel oil. On the other, the gas and diesel oil demand could not be met with production by Petróleos Mexicanos (Pemex). The possibility to expand the infrastructure was jeopardized, as the new refinery project in Tula, Hidalgo was put on hold and the plan was made to retrofit the units in Tula, Salamanca, and Salina Cruz. This situation constrained Pemex's supply capacity in subsequent years and made the country reliant on imports to supply the domestic market. -

Climate and Energy Benchmark in Oil and Gas Insights Report

Climate and Energy Benchmark in Oil and Gas Insights Report Partners XxxxContents Introduction 3 Five key findings 5 Key finding 1: Staying within 1.5°C means companies must 6 keep oil and gas in the ground Key finding 2: Smoke and mirrors: companies are deflecting 8 attention from their inaction and ineffective climate strategies Key finding 3: Greatest contributors to climate change show 11 limited recognition of emissions responsibility through targets and planning Key finding 4: Empty promises: companies’ capital 12 expenditure in low-carbon technologies not nearly enough Key finding 5:National oil companies: big emissions, 16 little transparency, virtually no accountability Ranking 19 Module Summaries 25 Module 1: Targets 25 Module 2: Material Investment 28 Module 3: Intangible Investment 31 Module 4: Sold Products 32 Module 5: Management 34 Module 6: Supplier Engagement 37 Module 7: Client Engagement 39 Module 8: Policy Engagement 41 Module 9: Business Model 43 CLIMATE AND ENERGY BENCHMARK IN OIL AND GAS - INSIGHTS REPORT 2 Introduction Our world needs a major decarbonisation and energy transformation to WBA’s Climate and Energy Benchmark measures and ranks the world’s prevent the climate crisis we’re facing and meet the Paris Agreement goal 100 most influential oil and gas companies on their low-carbon transition. of limiting global warming to 1.5°C. Without urgent climate action, we will The Oil and Gas Benchmark is the first comprehensive assessment experience more extreme weather events, rising sea levels and immense of companies in the oil and gas sector using the International Energy negative impacts on ecosystems. -

Integrating Into Our Strategy

INTEGRATING CLIMATE INTO OUR STRATEGY • 03 MAY 2017 Integrating Climate Into Our Strategy INTEGRATING CLIMATE INTO OUR STRATEGY • 03 CONTENTS Foreword by Patrick Pouyanné, Chairman and Chief Executive Officer, Total 05 Three Questions for Patricia Barbizet, Lead Independent Director of Total 09 _____________ SHAPING TOMORROW’S ENERGY Interview with Fatih Birol, Executive Director of the International Energy Agency 11 The 2°C Objective: Challenges Ahead for Every Form of Energy 12 Carbon Pricing, the Key to Achieving the 2°C Scenario 14 Interview with Erik Solheim, Executive Director of UN Environment 15 Oil and Gas Companies Join Forces 16 Interview with Bill Gates, Breakthrough Energy Ventures 18 _____________ TAKING ACTION TODAY Integrating Climate into Our Strategy 20 An Ambition Consistent with the 2°C Scenario 22 Greenhouse Gas Emissions Down 23% Since 2010 23 Natural Gas, the Key Energy Resource for Fast Climate Action 24 Switching to Natural Gas from Coal for Power Generation 26 Investigating and Strictly Limiting Methane Emissions 27 Providing Affordable Natural Gas 28 CCUS, Critical to Carbon Neutrality 29 A Resilient Portfolio 30 Low-Carbon Businesses to Become the Responsible Energy Major 32 Acquisitions That Exemplify Our Low-Carbon Strategy 33 Accelerating the Solar Energy Transition 34 Affordable, Reliable and Clean Energy 35 Saft, Offering Industrial Solutions to the Climate Change Challenge 36 The La Mède Biorefinery, a Responsible Transformation 37 Energy Efficiency: Optimizing Energy Consumption 38 _____________ FOCUS ON TRANSPORTATION Offering a Balanced Response to New Challenges 40 Our Initiatives 42 ______________ OUR FIGURES 45 04 • INTEGRATING CLIMATE INTO OUR STRATEGY Total at a Glance More than 98,109 4 million employees customers served in our at January 31, 2017 service stations each day after the sale of Atotech A Global Energy Leader No. -

Future Supply of Oil and Gas from the Gulf of Mexico

Future Supply of Oil and Gas From the Gulf of Mexico U.S. GEOLOGICAL SUltyEY PROFESSIONAL PAPER 1294 Future Supply of Oil and Gas From the Gulf of Mexico By E. D. Attanasi and]. L. Haynes U.S. GEOLOGICAL SURVEY PROFESSIONAL PAPER 1294 An engineering-economic costing algorithm combined with a discovery process model to forecast long-run incremental costs of undiscovered oil and gas UNITED STATES GOVERNMENT PRINTING OFFICE, WASHINGTON : 1983 UNITED STATES DEPARTMENT OF THE INTERIOR JAMES G. WATT, Secretary GEOLOGICAL SURVEY Dallas L. Peck, Director Library of Congress Cataloging in Publication Data Attanasi, E. D. Future supply of oil and gas from the Gulf of Mexico. (U.S. Geological Survey professional paper ; 1294) Bibliography: p. 1. Petroleum in submerged lands Mexico, Gulf of. 2. Gas, Natural, in submerged lands Mexico, Gulf of. I. Haynes, J. (John), 1954- . II. Title. III. Series: Geological Survey professional paper ; 1294. TN872.A5A87 1983 553.2'8'0916364 83-600030 ____ ____________ For sale by the Superintendent of Documents, U.S. Government Printing Office Washington, D.C. 20402 CONTENTS Page Abstract 1 Introduction 1 Engineering-economic model 3 Methodology 3 Engineering data and assumptions 5 Field classification 5 Field design 6 Production schedules of oil and nonassociated gas wells 7 Economic assumptions and variables 8 Field development costs 8 Production costs and production related taxes 9 Assumptions for after-tax net present value calculations 10 Exploration costs 10 Industry behavior and market conditions 10 Forecasting future discoveries 11 Discovery process model 11 Estimated marginal cost functions for undiscovered recoverable oil and gas resources in the Gulf of Mexico 12 Conclusions and implications 16 References cited 16 Appendix A 17 Appendix B 20 ILLUSTRATIONS FIGURE 1. -

Shell QRA Q2 2021

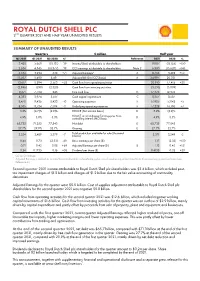

ROYAL DUTCH SHELL PLC 2ND QUARTER 2021 AND HALF YEAR UNAUDITED RESULTS SUMMARY OF UNAUDITED RESULTS Quarters $ million Half year Q2 2021 Q1 2021 Q2 2020 %¹ Reference 2021 2020 % 3,428 5,660 (18,131) -39 Income/(loss) attributable to shareholders 9,087 (18,155) +150 2,634 4,345 (18,377) -39 CCS earnings attributable to shareholders Note 2 6,980 (15,620) +145 5,534 3,234 638 +71 Adjusted Earnings² A 8,768 3,498 +151 13,507 11,490 8,491 Adjusted EBITDA (CCS basis) A 24,997 20,031 12,617 8,294 2,563 +52 Cash flow from operating activities 20,910 17,415 +20 (2,946) (590) (2,320) Cash flow from investing activities (3,535) (5,039) 9,671 7,704 243 Free cash flow G 17,375 12,376 4,383 3,974 3,617 Cash capital expenditure C 8,357 8,587 8,470 9,436 8,423 -10 Operating expenses F 17,905 17,042 +5 8,505 8,724 7,504 -3 Underlying operating expenses F 17,228 16,105 +7 3.2% (4.7)% (2.9)% ROACE (Net income basis) D 3.2% (2.9)% ROACE on an Adjusted Earnings plus Non- 4.9% 3.0% 5.3% controlling interest (NCI) basis D 4.9% 5.3% 65,735 71,252 77,843 Net debt E 65,735 77,843 27.7% 29.9% 32.7% Gearing E 27.7% 32.7% Total production available for sale (thousand 3,254 3,489 3,379 -7 boe/d) 3,371 3,549 -5 0.44 0.73 (2.33) -40 Basic earnings per share ($) 1.17 (2.33) +150 0.71 0.42 0.08 +69 Adjusted Earnings per share ($) B 1.13 0.45 +151 0.24 0.1735 0.16 +38 Dividend per share ($) 0.4135 0.32 +29 1. -

The Economic Impacts of the Gulf of Mexico Oil and Natural Gas Industry

The Economic Impacts of the Gulf of Mexico Oil and Natural Gas Industry Prepared For Prepared By Executive Summary Introduction Despite the current difficulties facing the global economy as a whole and the oil and natural gas industry specifically, the Gulf of Mexico oil and natural gas industry will likely continue to be a major source of energy production, employment, gross domestic product, and government revenues for the United States. Several proposals have been advanced recently which would have a major impact on the industry’s activity levels, and the economic activity supported by the Gulf of Mexico offshore oil and natural gas industry. The proposals vary widely, but for the purpose of this report three scenarios were developed, a scenario based on a continuation of current policies and regulations, a scenario examining the potential impacts of a ban on new offshore leases, and a scenario examining the potential impacts of a ban on new drilling permits approvals in the Gulf of Mexico. Energy and Industrial Advisory Partners (EIAP) was commissioned by the National Ocean Industry Association (NOIA) to develop a report forecasting activity levels, spending, oil and natural gas production, supported employment, GDP, and Government Revenues in these scenarios. The scenarios developed in this report are based solely upon government and other publicly available data and EIAP’s own expertise and analysis. The study also included profiles of NOIA members to demonstrate the diverse group of companies which make up the offshore Gulf of Mexico oil and natural gas industry as well as a list of over 2,400 suppliers to the industry representing all 50 states. -

Our Activities in QATAR TOTAL in QATAR Al Fardan Towers, 61, Al Funduq Street, West Bay

Our activities in QATAR TOTAL IN QATAR Al Fardan Towers, 61, Al Funduq Street, West Bay. P.O. Box 9803, Doha, Qatar [email protected] www.total.qa TotalQatar Total_QA OUR ACTIVITIES IN QATAR 30% SHAREHOLDER SHAREHOLDER 20% SHAREHOLDER IN NORTH OIL IN QATARGAS, IN QAPCO, FORGING A PARTNERSHIP COMPANY, THE OPERATOR THE LARGEST LNG ONE OF THE OF QATAR’S LARGEST PRODUCER WORLD’S LARGEST LDPE OF OVER 80 YEARS OFFSHORE OIL FIELD IN THE WORLD PRODUCTION SITES Qatar plays an important part in Total’s Our sustainability strategy is therefore history and in our future. Our longstanding established through the active involvement presence in this country is testimony to of our stakeholders. the special partnership that we share. Total has been active in all areas of Qatar’s oil We hope to contribute to positive developments and gas sector - from exploration and in the State of Qatar, not only through our production, to refining, petrochemicals, economic activities, but also through initiatives and marketing of lubricants. that focus on the citizens and residents of the country. We work closely with all our stakeholders 2 to ensure that our activities consistently Qatar has one of the highest growth rates deliver economic growth alongside societal in the world, which has given us opportunities and environmental initiatives. We have to create and support ambitious projects, 37 placed corporate social responsibility at and this has enabled us to fulfill the commitment the heart of our business. that Total has made to the society. All our accomplishments have been achieved due to the strong dedication, and team work of our people, who embody our corporate values. -

US Sanctions on Russia

U.S. Sanctions on Russia Updated January 17, 2020 Congressional Research Service https://crsreports.congress.gov R45415 SUMMARY R45415 U.S. Sanctions on Russia January 17, 2020 Sanctions are a central element of U.S. policy to counter and deter malign Russian behavior. The United States has imposed sanctions on Russia mainly in response to Russia’s 2014 invasion of Cory Welt, Coordinator Ukraine, to reverse and deter further Russian aggression in Ukraine, and to deter Russian Specialist in European aggression against other countries. The United States also has imposed sanctions on Russia in Affairs response to (and to deter) election interference and other malicious cyber-enabled activities, human rights abuses, the use of a chemical weapon, weapons proliferation, illicit trade with North Korea, and support to Syria and Venezuela. Most Members of Congress support a robust Kristin Archick Specialist in European use of sanctions amid concerns about Russia’s international behavior and geostrategic intentions. Affairs Sanctions related to Russia’s invasion of Ukraine are based mainly on four executive orders (EOs) that President Obama issued in 2014. That year, Congress also passed and President Rebecca M. Nelson Obama signed into law two acts establishing sanctions in response to Russia’s invasion of Specialist in International Ukraine: the Support for the Sovereignty, Integrity, Democracy, and Economic Stability of Trade and Finance Ukraine Act of 2014 (SSIDES; P.L. 113-95/H.R. 4152) and the Ukraine Freedom Support Act of 2014 (UFSA; P.L. 113-272/H.R. 5859). Dianne E. Rennack Specialist in Foreign Policy In 2017, Congress passed and President Trump signed into law the Countering Russian Influence Legislation in Europe and Eurasia Act of 2017 (CRIEEA; P.L. -

2020 Annual Report

Online Annual Report Gazprom Neft Performance review Sustainable 2020 at a glance 62 Resource base and production development CONTENTS 81 Refining and manufacturing 4 Geographical footprint 94 Sales of oil and petroleum products 230 Sustainable development 6 Gazprom Neft at a glance 114 Financial performance 234 Health, safety and environment (HSE) 8 Gazprom Neft’s investment case 241 Environmental safety 10 2020 highlights 250 HR Management 12 Letter from the Chairman of the Board of Directors 254 Social policy Technological Strategic report development Appendices 264 Consolidated financial statements as at and for the year ended 31 December 2020, with the 16 Letter from the Chairman of the Management Board 122 Innovation management independent auditor’s report About the Report 18 Market overview 131 2020 highlights and key projects 355 Company history This Report by Public Joint Stock Company Gazprom Neft (“Gazprom 28 2020 challenges 135 Import substitution 367 Structure of the Gazprom Neft Group Neft PJSC”, the “company”) for 2020 includes the results of operational activities of Gazprom Neft PJSC and its subsidiaries, 34 2030 Strategy 370 Information on energy consumption at Gazprom collectively referred to as the Gazprom Neft Group (the “Group”). 38 Business model Neft Gazprom Neft PJSC is the parent company of the Group and provides consolidated information on the operational and financial 42 Company transformation 371 Excerpts from management’s discussion and performance of the Group’s key assets for this Annual Report. The analysis of financial condition and results of list of subsidiaries covered in this Report and Gazprom Neft PJSC’s 44 Digital transformation operations interest in their capital are disclosed in notes to the consolidated Governance system IFRS financial statements for 2020. -

Qatar Petroleum

Qatar Petroleum 1. Strategy: Strategy is the direction and scope of an organization over the long-term: which achieves advantage for the organization through its configuration of resources within a challenging environment, to meet the needs of markets and to fulfill stakeholder expectations. And Strategic Management can be defined as (1) the art and science of formulating, (2) implementing, and (3) evaluating cross-functional decisions that enable an organization to achieve its objectives. 2. Most Strategic Management Model: 1. PEST analysis 2. STEER Analysis 3. Five Forces Model 4. Strategic Group Map 5. SWOT analysis 6. Blue Ocean Strategies 7. Open innovation 8. seven S model 1) PEST Analysis: PEST analysis stands for "Political, Economic, Social, and Technological analysis" and describes a framework of macro-environmental factors used in the environmental scanning component of strategic management. 2. STEER Analysis: STEER analysis systematically considers Socio-cultural, Technological, Economic, Ecological, and Regulatory factors. Qatar Petroleum | 1 3. Five Forces Model: a) Supplier Power: b) Buyer Power: c) New Market Entrants: d) Product and Technology Development: e) Competitive Rivalry: 4) Strategic Group Map: 1. Extent of product (or service) diversity. 2. Extent of geographic coverage. 3. Number of market segments served. 4. Distribution channels used. 5. Extent of branding. 6. Marketing effort. 7. Product (or service) quality. 8. Pricing policy. 5) SWOT Analysis • Strengths: characteristics of the business or team that give it an advantage over others in the industry. • Weaknesses: are characteristics that place the firm at a disadvantage relative to others. • Opportunities: external chances to make greater sales or profits in the environment. -

LUKOIL's Market Strategy in Central and Eastern Europe 105 O Increasing the Number of Filling Stations for Petroleum Products in Russia and Other Countries

Petroleum-Gas University of Ploiesti Vol. LXII Economic Sciences 103-110 BULLETIN No. 4/2010 Series LUKOIL’s Market Strategy in Central and Eastern Europe Mihaela Oprea Ciopi Petroleum-Gas University of Ploieşti, Bd. Bucureşti 39, Ploieşti, Romania e-mail: [email protected] Abstract The economic environment has undergone significant development over the past 20 years marked, in particular, by the globalization of the economy and increased competitiveness. The large oil corporations significantly influence national economies and the global economy in general, as a result of their huge financial power and their profit-oriented corporate management, by identifying the most appropriate strategies and the most effective methods of business management . Currently, oil market in Central and Eastern Europe is controlled by three major players: the Austrian OMV, Hungarian MOL company and the Russian company LUKOIL, whose investment strategies and policies contributed to a decisive extent to the development and consolidation of oil industry in the countries in this area, thus in Romania too. In this context, the paper aims to analyze the strategy of developing and consolidating LUKOIL’s position on this market. Key words: strategic alliance, a global energy player, offensive strategy, territorial expansion JEL Classification: M10 Introduction The greatest oil corporations significantly influence national economies and the global economy in general, the effect of their huge financial power and corporate management oriented to increase profit by identifying the most appropriate strategies and the most effective methods of business management. These elements underpin the development of management as a science and was later taken over and adapted by national companies. -

Royal Dutch Shell Report on Payments to Governments for the Year 2018

ROYAL DUTCH SHELL REPORT ON PAYMENTS TO GOVERNMENTS FOR THE YEAR 2018 This Report provides a consolidated overview of the payments to governments made by Royal Dutch Shell plc and its subsidiary undertakings (hereinafter refer to as “Shell”) for the year 2018 as required under the UK’s Report on Payments to Governments Regulations 2014 (as amended in December 2015). These UK Regulations enact domestic rules in line with Directive 2013/34/EU (the EU Accounting Directive (2013)) and apply to large UK incorporated companies like Shell that are involved in the exploration, prospection, discovery, development and extraction of minerals, oil, natural gas deposits or other materials. This Report is also filed with the National Storage Mechanism (http://www.morningstar.co.uk/uk/nsm) intended to satisfy the requirements of the Disclosure Guidance and Transparency Rules of the Financial Conduct Authority in the United Kingdom This Report is available for download from www.shell.com/payments BASIS FOR PREPARATION - REPORT ON PAYMENTS TO GOVERNMENTS FOR THE YEAR 2018 Legislation This Report is prepared in accordance with The Reports on Payments to Governments Regulations 2014 as enacted in the UK in December 2014 and as amended in December 2015. Reporting entities This Report includes payments to governments made by Royal Dutch Shell plc and its subsidiary undertakings (Shell). Payments made by entities over which Shell has joint control are excluded from this Report. Activities Payments made by Shell to governments arising from activities involving the exploration, prospection, discovery, development and extraction of minerals, oil and natural gas deposits or other materials (extractive activities) are disclosed in this Report.