May 2, 2016 Brent J. Fields Secretary Securities and Exchange

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Our Activities in QATAR TOTAL in QATAR Al Fardan Towers, 61, Al Funduq Street, West Bay

Our activities in QATAR TOTAL IN QATAR Al Fardan Towers, 61, Al Funduq Street, West Bay. P.O. Box 9803, Doha, Qatar [email protected] www.total.qa TotalQatar Total_QA OUR ACTIVITIES IN QATAR 30% SHAREHOLDER SHAREHOLDER 20% SHAREHOLDER IN NORTH OIL IN QATARGAS, IN QAPCO, FORGING A PARTNERSHIP COMPANY, THE OPERATOR THE LARGEST LNG ONE OF THE OF QATAR’S LARGEST PRODUCER WORLD’S LARGEST LDPE OF OVER 80 YEARS OFFSHORE OIL FIELD IN THE WORLD PRODUCTION SITES Qatar plays an important part in Total’s Our sustainability strategy is therefore history and in our future. Our longstanding established through the active involvement presence in this country is testimony to of our stakeholders. the special partnership that we share. Total has been active in all areas of Qatar’s oil We hope to contribute to positive developments and gas sector - from exploration and in the State of Qatar, not only through our production, to refining, petrochemicals, economic activities, but also through initiatives and marketing of lubricants. that focus on the citizens and residents of the country. We work closely with all our stakeholders 2 to ensure that our activities consistently Qatar has one of the highest growth rates deliver economic growth alongside societal in the world, which has given us opportunities and environmental initiatives. We have to create and support ambitious projects, 37 placed corporate social responsibility at and this has enabled us to fulfill the commitment the heart of our business. that Total has made to the society. All our accomplishments have been achieved due to the strong dedication, and team work of our people, who embody our corporate values. -

Qatar Petroleum

Qatar Petroleum 1. Strategy: Strategy is the direction and scope of an organization over the long-term: which achieves advantage for the organization through its configuration of resources within a challenging environment, to meet the needs of markets and to fulfill stakeholder expectations. And Strategic Management can be defined as (1) the art and science of formulating, (2) implementing, and (3) evaluating cross-functional decisions that enable an organization to achieve its objectives. 2. Most Strategic Management Model: 1. PEST analysis 2. STEER Analysis 3. Five Forces Model 4. Strategic Group Map 5. SWOT analysis 6. Blue Ocean Strategies 7. Open innovation 8. seven S model 1) PEST Analysis: PEST analysis stands for "Political, Economic, Social, and Technological analysis" and describes a framework of macro-environmental factors used in the environmental scanning component of strategic management. 2. STEER Analysis: STEER analysis systematically considers Socio-cultural, Technological, Economic, Ecological, and Regulatory factors. Qatar Petroleum | 1 3. Five Forces Model: a) Supplier Power: b) Buyer Power: c) New Market Entrants: d) Product and Technology Development: e) Competitive Rivalry: 4) Strategic Group Map: 1. Extent of product (or service) diversity. 2. Extent of geographic coverage. 3. Number of market segments served. 4. Distribution channels used. 5. Extent of branding. 6. Marketing effort. 7. Product (or service) quality. 8. Pricing policy. 5) SWOT Analysis • Strengths: characteristics of the business or team that give it an advantage over others in the industry. • Weaknesses: are characteristics that place the firm at a disadvantage relative to others. • Opportunities: external chances to make greater sales or profits in the environment. -

Royal Dutch Shell Report on Payments to Governments for the Year 2018

ROYAL DUTCH SHELL REPORT ON PAYMENTS TO GOVERNMENTS FOR THE YEAR 2018 This Report provides a consolidated overview of the payments to governments made by Royal Dutch Shell plc and its subsidiary undertakings (hereinafter refer to as “Shell”) for the year 2018 as required under the UK’s Report on Payments to Governments Regulations 2014 (as amended in December 2015). These UK Regulations enact domestic rules in line with Directive 2013/34/EU (the EU Accounting Directive (2013)) and apply to large UK incorporated companies like Shell that are involved in the exploration, prospection, discovery, development and extraction of minerals, oil, natural gas deposits or other materials. This Report is also filed with the National Storage Mechanism (http://www.morningstar.co.uk/uk/nsm) intended to satisfy the requirements of the Disclosure Guidance and Transparency Rules of the Financial Conduct Authority in the United Kingdom This Report is available for download from www.shell.com/payments BASIS FOR PREPARATION - REPORT ON PAYMENTS TO GOVERNMENTS FOR THE YEAR 2018 Legislation This Report is prepared in accordance with The Reports on Payments to Governments Regulations 2014 as enacted in the UK in December 2014 and as amended in December 2015. Reporting entities This Report includes payments to governments made by Royal Dutch Shell plc and its subsidiary undertakings (Shell). Payments made by entities over which Shell has joint control are excluded from this Report. Activities Payments made by Shell to governments arising from activities involving the exploration, prospection, discovery, development and extraction of minerals, oil and natural gas deposits or other materials (extractive activities) are disclosed in this Report. -

Sustainability Report 2011.Pdf

SUSTAINABILITY report Home / Sustainability Sustainability Sustainability performance for Statoil means helping to meet the world's growing energy needs in economically, environmentally and socially responsible ways. Sustainability is no longer just about doing innovation and business development. One constitutes part of our licence to operate, business responsibly - it is also about of Statoil's strategic beliefs is that being an but also gives us a competitive edge in a seeing social and sustainability challenges industry leader in HSE and carbon resources-constrained world. as opportunities for efficiency not only Home / Sustainability / The context of our reporting The context of our reporting The point of departure in our sustainability reporting is our management approach and our reporting requirements. OUR MANAGEMENT APPROACH At Statoil, the way we deliver is Although we believe impact of our activities and as important as what we deliver. sustainability should be products on the environment This is the first part of company considered in its broadest People and the group - and policy a new employee is likely context, we have grouped our efforts to respect to encounter. It is a belief that is articles into sections in order to individuals, help others to reflected in our performance assist reading. The first section succeed and contribute to a management and risk describes the context of our positive working environment management systems. These reporting and the management policies serve as the framework approach and governance Society - and our efforts to act for the numerous procedures structure that relate to within the law and in and ambitions described environmental and social accordance with our own throughout this report. -

Mexico's Deep Water Success

Energy Alert February 1, 2018 Key Points Round 2.4 exceeded expectations by awarding 18 of 29 (62 percent) of available contract areas Biggest winners were Royal Dutch Shell, with nine contract areas, and PC Carigali, with seven contract areas Investments over $100 billion in Mexico’s energy sector expected in the upcoming years Mexico’s Energy Industry Round 2.4: Mexico’s Deep Water Success On January 31, 2018, the Comisión Nacional de Hidrocarburos (“CNH”) completed the Presentation and Opening of Bid Proposals for the Fourth Tender of Round Two (“Round 2.4”), which was first announced on July 20, 2017. Round 2.4 attracted 29 oil and gas companies from around the world including Royal Dutch Shell, ExxonMobil, Chevron, Pemex, Lukoil, Qatar Petroleum, Mitsui, Repsol, Statoil and Total, among others. Round 2.4 included 60% of all acreage to be offered by Mexico under the current Five Year Plan. Blocks included 29 deep water contract areas (shown in the adjacent map) with an estimated 4.23 billion Barrel of Oil Equivalent (BOE) of crude oil, wet gas and dry gas located in the Perdido Fold Belt Area, Salinas Basin and Mexican Ridges. The blocks were offered under a license contract, similar to the deep water form used by the CNH in Round 1.4. After witnessing the success that companies like ENI, Talos Energy, Inc., Sierra and Premier have had in Mexico over the last several years, Round 2.4 was the biggest opportunity yet for the industry. Some of these deep water contract areas were particularly appealing because they share geological characteristics with some of the projects in the U.S. -

Qatar Fast Facts Occidental Petroleum

Qatar Fast Facts Occidental Petroleum Occidental’s Idd El Shargi North Dome operations, Offshore Qatar. More than Two Decades Partner of Choice® Occidental has worked with Qatar Petroleum since 1994 to Occidental is committed to providing safe, healthy and secure develop and operate offshore oil fields. Occidental also workplaces; protecting the environment; maintaining high participates in Dolphin Energy, the premier transborder natural ethical standards; upholding and promoting human rights; and gas project in the Middle East. respecting cultural norms and values, everywhere we operate. Second-Largest Offshore Oil Producer National Vision 2030 Occidental is the second-largest oil producer offshore, where Occidental is committed to the Government of Qatar’s National the company operates Idd El Shargi North Dome and Idd El Vision 2030, supporting the long-term sustainable development of the country’s economy and citizens. Shargi South Dome. EOR Leader Qatarization Commitment Occidental supports Qatari employees’ growth and Occidental is extending the life of Qatar’s oil fields with development through Qatarization and succession planning largescale waterflooding and other enhanced oil recovery (EOR) projects, combined with state-of-the-art horizontal drilling, programs, with the objective of increasing its Qatari leadership. advanced completion techniques and extensive automated In-Country Value artificial lift systems. Occidental’s In-Country Value (ICV) strategy supports 400% Production Boost employment of Qatari nationals and the development of Qatari Since beginning operations in 1994, Occidental has boosted goods and services, with the goal of strengthening the local production from the Idd El Shargi Fields by more than 400 market. percent. In 2017, Occidental lifted the one billionth barrel of oil SME Development from these fields. -

DMUT LIST ISC 22 AUG 2019.Xlsx

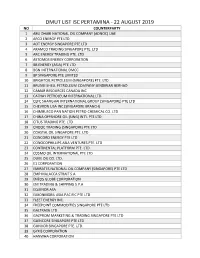

DMUT LIST ISC PERTAMINA - 22 AUGUST 2019 NO COUNTERPARTY 1 ABU DHABI NATIONAL OIL COMPANY (ADNOC) UAE 2 AFCO ENERGY PTE LTD 3 AOT ENERGY SINGAPORE PTE LTD 4 ARAMCO TRADING SINGAPORE PTE. LTD 5 ARC ENERGY TRADING PTE. LTD 6 ASTOMOS ENERGY CORPORATION 7 BB ENERGY (ASIA) PTE LTD 8 BGN INTERNATIONAL DMCC 9 BP SINGAPORE PTE LIMITED 10 BRIGHTOIL PETROLEUM (SINGAPORE) PTE. LTD. 11 BRUNEI SHELL PETROLEUM COMPANY SENDIRIAN BERHAD 12 CAMAR RESOURCES CANADA INC 13 CATHAY PETROLEUM INTERNATIONAL LTD. 14 CEFC SHANGHAI INTERNATIONAL GROUP (SINGAPORE) PTE LTD 15 CHEVRON USA INC (SINGAPORE BRANCH) 16 CHIMBUSCO PAN NATION PETRO-CHEMICAL CO. LTD 17 CHINA OFFSHORE OIL (SING) INT'L PTE LTD 18 CITUS TRADING PTE. LTD 19 CNOOC TRADING (SINGAPORE) PTE LTD 20 COASTAL OIL SINGAPORE PTE. LTD 21 CONCORD ENERGY PTE LTD 22 CONOCOPHILLIPS ASIA VENTURES PTE. LTD 23 CONTINENTAL PLATFORM PTE. LTD. 24 COSMO OIL INTERNATIONAL PTE LTD 25 DUKE OIL CO. LTD. 26 E1 CORPORATION 27 EMIRATES NATIONAL OIL COMPANY (SINGAPORE) PTE LTD 28 EMP MALACCA STRAIT S.A 29 ENEOS GLOBE CORPORATION 30 ENI TRADING & SHIPPING S.P.A 31 EQUINOR ASA 32 EXXONMOBIL ASIA PACIFIC PTE LTD 33 FLEET ENERGY INC. 34 FREEPOINT COMMODITIES SINGAPORE PTE LTD 35 GALTRADE LTD 36 GAZPROM MARKETING & TRADING SINGAPORE PTE LTD 37 GLENCORE SINGAPORE PTE LTD 38 GUNVOR SINGAPORE PTE. LTD. 39 GYXIS CORPORATION 40 HANWHA CORPORATION NO COUNTERPARTY 41 HENGYI INDUSTRIES INTERNATIONAL PTE. LTD 42 HIN LEONG TRADING (PTE) LTD 43 HUAYUE ENERGY (SINGAPORE) PTE. LTD 44 HYPHEN ENERGY PTE. LTD. 45 IDEMITSU INTERNATIONAL (ASIA) PTE LTD 46 INPEX OFFSHORE NORTH MAHAKAM LTD 47 INPEX TRADING, LTD 48 INTERNATIONAL ENERGY GROUP PTE. -

QP Annual Review 2018

2018 ANNUAL REVIEW CONTENTS Message from the President & CEO 5 About QP 7 Company Profile Board of Directors QP’s Executive Leadership Team Corporate Governance, Transparency and Business Ethics Key Figures for 2018 17 Upstream Operations 19 QP-Operated Fields Dukhan Field Maydan Mahzam Field Bul Hanine Field Al Rayyan Field Non-QP-Operated Fields Al Shaheen Field Al Khalij Field Idd El Shargi – North Dome & South Dome Fields Al Karkara & A-Structures El Bunduq Field North Field Downstream Operations 31 QP Refinery Mesaieed Operations Refined Products Supply Chain Project Industrial Cities 35 Mesaieed Industrial City Ras Laffan Industrial City Dukhan Concession Area Major Projects 37 North Field Expansion Project Growing Global Reach 39 International Upstream Investments From Qatar to the World Joint Ventures & Subsidiaries 45 The QP Investment Portfolio The QP People Agenda 49 Qatarization Operating Safely and Responsibly 53 Occupational Health Safety Excellence Corporate Social Responsibility Environmental Stewardship 2018 Highlights 61 Financial Statements 69 Glossary & Acronyms 81 5 QATAR PETROLEUM ANNUAL REVIEW 2018 ANNUAL REVIEW 2018 2 His Highness Sheikh Tamim bin Hamad Al Thani The Amir of the State of Qatar 3 QATAR PETROLEUM His Highness Sheikh Hamad bin Khalifa Al Thani The Father Amir ANNUAL REVIEW 2018 4 His Highness Sheikh Abdullah bin Hamad Al Thani The Deputy Amir of the State of Qatar 5 QATAR PETROLEUM MESSAGE FROM THE PRESIDENT & CEO SAAD SHERIDA AL-KAABI Minister of State for Energy Affairs President & CEO of Qatar Petroleum ANNUAL REVIEW 2018 6 2018 was a robust and dynamic year, which was characterized by steady attention to Qatar Petroleum’s core business, a wider expansion of its international upstream footprint, and a detailed focus on the development of Qatar’s energy resources. -

2007 Annual Report

Qatar Petroleum, Committed to Excellence Qatar Petroleum (QP), formerly Qatar General Petroleum Corporation, is a state-owned corporation established, by Emiri Decree No 10, in 1974 responsible for all phases of the oil and gas industry in Qatar. The principal activities of Qatar Petroleum and its subsidiaries and joint ventures cover exploration, drilling and production operations, transport, storage, marketing and sale of crude oil, natural gas liquids, liqueed natural gas, rened products, petrochemicals and fertilizers, and providing helicopter services. Qatar Petroleum’s strategy of conducting hydrocarbon exploration and new projects is through Exploration and Production Sharing Agreements (EPSA) and Development and Production Sharing Agreements (DPSA) concluded with major international oil and gas companies. The operations and activities of Qatar Petroleum are conducted on various onshore locations, which include Doha, Dukhan, Mesaieed and Ras Laan Industrial Cities, as well as oshore areas including Halul Island, Oshore Production Stations, Drilling Platforms and the North Gas Field. In addition to its operations, QP carries out its activities through the following subsidiaries, joint ventures and other investments. A – Subsidiaries QP Interest Percentage % C- Other Investments % Qatar Petroleum Qatar Gas (3) Ltd. 100.0 Qatar Fuel Co. (WOQOD) 40.0 Gulf Helicopters Co. (Gulf Helicopters) 100.0 Qatar Shipping Co. (Q-SHIP) 18.5 Al Koot Insurance and Reinsurance Co. 100.0 Qatar Metal Coating Co.W.L.L 35.0 Qatar Petroleum Gas Trading (QGII) Ltd. 100.0 Qatar Real Estate Investment Co. 0.7 Qatar Petroleum LNG Services (QGII) Ltd. 100.0 Qatar Plastic Production Co. (QPPC) 26.6 Qatar Terminal Co. Ltd. -

Europe, Middle East and North Africa Total 99 12 646 219

Europe, Middle East Europe,and North Africa Middle East andFact Sheet—March North 2021 Africa Fact Sheet—March 2021 ConocoPhillips has operated in Europe for more than 50 years, with significant developments in the 2020 Production Norwegian sector of the North Sea and in the Norwegian Sea. In Qatar, the company has interests in a producing field as well as liquefied natural gas production and export. The company also has Thousand interests in a concession in Libya. barrels of oil Operated assets in Europe include the Greater Ekofisk Area in Norway. The company also conducts 219 equivalent per day exploration activity in Norway. The company has leveraged its existing operations, infrastructure and basin expertise to create incremental growth projects in recent years, and development 2020 Proved Reserves* opportunities still exist in ConocoPhillips’ legacy areas. In Qatar, the Qatargas 3 joint venture continues providing stable production. Billion barrels of oil In Libya, the company has an interest in the Waha Concession in the Sirte Basin. Production equivalent operations in Libya and related oil exports have been periodically interrupted over the last several 0.6 years due to forced shutdowns of the Es Sider terminal. ConocoPhillips—Average Daily Net Production, 2020 Crude Oil NGL Natural Gas Total Area Interest Operator (MBD) (MBD) (MMCFD) (MBOED) Greater Ekofisk Area 30.7%-35.1% ConocoPhillips 46 2 39 55 Heidrun 24.0% Equinor 12 1 32 18 Aasta Hansteen 10.0% Equinor - - 82 14 Troll 1.6% Equinor 2 - 54 11 Visund 9.1% Equinor 2 1 40 10 Alvheim 20.0% Aker BP 8 - 13 10 Other Various Equinor 8 - 10 9 Norway Total 78 4 270 127 Qatargas 3 30.0% Qatargas Operating Co. -

Qatar: Governance, Security, and U.S. Policy

Qatar: Governance, Security, and U.S. Policy Updated August 27, 2021 Congressional Research Service https://crsreports.congress.gov R44533 SUMMARY R44533 Qatar: Governance, Security, and U.S. Policy August 27, 2021 The State of Qatar, a small Arab Gulf monarchy which has about 300,000 citizens in a total population of about 2.4 million, has employed its ample financial resources to exert Kenneth Katzman regional influence, often independent of the other members of the Gulf Cooperation Specialist in Middle Council (GCC: Saudi Arabia, Kuwait, Qatar, United Arab Emirates (UAE), Bahrain, and Eastern Affairs Oman) alliance. Qatar has fostered a close defense and security alliance with the United States and has maintained ties to a wide range of actors who are often at odds with each other, including Sunni Islamists, Iran and Iran-backed groups, and Israeli officials. Qatar’s support for regional Muslim Brotherhood organizations and its Al Jazeera media network have contributed to a backlash against Qatar led by fellow GCC states Saudi Arabia and the UAE. In June 2017, Saudi Arabia, the UAE, and Bahrain, joined by Egypt and a few other governments, severed relations with Qatar and imposed limits on the entry and transit of Qatari nationals and vessels in their territories, waters, and airspace. The Trump Administration sought a resolution of the dispute, in part because the rift was hindering U.S. efforts to formalize a “Middle East Strategic Alliance” of the United States, the GCC, and other Sunni-led countries in the region to counter Iran. Qatar has countered the Saudi-led pressure with new arms purchases and deepening relations with Turkey and Iran. -

Michiel Kool the Man Behind the Role

WINTER 2015 SHELL ECONOMIC | SOCIAL | ENVIRONMENTAL | HUMAN MICHIEL KOOL Qatar Shell Managing Director and Chairman THE MAN BEHIND THE ROLE ALSO IN THIS ISSUE... FATIMA AHMED AL MULLA Positively Impacting Qatar Discovering ENERGY WORLD QATAR 2015 ROAD SAFETY CAMPAIGN Kicks-Off Winter Tour FOREWORD It is my sincere pleasure to welcome you to 24 Shell World Qatar Magazine and as we 2 head towards the twilight of 2015, I reflect on the 5 months since taking over as Managing Positively Impacting Yvonne Shaw Director and Chairman of Qatar Shell. Managing Editor Qatar [email protected] My first few months have been humbling, A feature on Fatima Ahmed Al Mulla, exciting and intense as we contend with the Reservoir Engineer current low-oil price environment and the challenges that it brings. Our commitment to support Qatar Petroleum and the State of Qatar remains crystal clear. And at the same time we ourselves look to build a dynamic 4 company that is very good at its core business, brings wider benefits to society and Qatar Shell Economist Farah Al-Maadeed retains safety and care for people at the heart Deputy Managing Editor of everything we do. Participates in Dutch [email protected] The cornerstone of our partnership with Visitors Programme Qatar Petroleum is Pearl GTL and despite Interview with Saad Al Matwi challenging oil and gas commodity prices, the plant continues safe and reliable production that generates significant value with its product 2 slate of GTL gasoil, kerosene, baseoil, naptha and normal paraffin. These products provide 8 clear advantages to our customers around the world.