The Prospects for Russian Oil and Gas

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

The Killing of William Browder

THE KILLING OF WILLIAM BROWDER THE KILLING OF WILLIAM BROWDER Bill Browder, the fa lse crusader for justice and human rights and the self - styled No. 1 enemy of Vladimir Putin has perpetrated a brazen and dangerous deception upon the Weste rn world. This book traces the anatomy of this deception, unmasking the powerful forces that are pushing the West ern world toward yet another great war with Russia. ALEX KRAINER EQUILIBRIUM MONACO First published in Monaco in 20 17 Copyright © 201 7 by Alex Krainer ISBN 978 - 2 - 9556923 - 2 - 5 Material contained in this book may be reproduced with permission from its author and/or publisher, except for attributed brief quotations Cover page design, content editing a nd copy editing by Alex Krainer. Set in Times New Roman, book title in Imprint MT shadow To the people of Russia and the United States wh o together, hold the keys to the future of humanity. Enlighten the people generally, and tyranny and oppressions of body and mind will vanish like the evil spirits at the dawn of day. Thomas Jefferson Table of Contents 1. Bill Browder and I ................................ ................................ ............... 1 Browder’s 2005 presentation in Monaco ................................ .............. 2 Harvard club presentation in 2010 ................................ ........................ 3 Ru ssophobia and Putin - bashing in the West ................................ ......... 4 Red notice ................................ ................................ ............................ 6 Reading -

The Russia You Never Met

The Russia You Never Met MATT BIVENS AND JONAS BERNSTEIN fter staggering to reelection in summer 1996, President Boris Yeltsin A announced what had long been obvious: that he had a bad heart and needed surgery. Then he disappeared from view, leaving his prime minister, Viktor Cher- nomyrdin, and his chief of staff, Anatoly Chubais, to mind the Kremlin. For the next few months, Russians would tune in the morning news to learn if the presi- dent was still alive. Evenings they would tune in Chubais and Chernomyrdin to hear about a national emergency—no one was paying their taxes. Summer turned to autumn, but as Yeltsin’s by-pass operation approached, strange things began to happen. Chubais and Chernomyrdin suddenly announced the creation of a new body, the Cheka, to help the government collect taxes. In Lenin’s day, the Cheka was the secret police force—the forerunner of the KGB— that, among other things, forcibly wrested food and money from the peasantry and drove some of them into collective farms or concentration camps. Chubais made no apologies, saying that he had chosen such a historically weighted name to communicate the seriousness of the tax emergency.1 Western governments nod- ded their collective heads in solemn agreement. The International Monetary Fund and the World Bank both confirmed that Russia was experiencing a tax collec- tion emergency and insisted that serious steps be taken.2 Never mind that the Russian government had been granting enormous tax breaks to the politically connected, including billions to Chernomyrdin’s favorite, Gazprom, the natural gas monopoly,3 and around $1 billion to Chubais’s favorite, Uneximbank,4 never mind the horrendous corruption that had been bleeding the treasury dry for years, or the nihilistic and pointless (and expensive) destruction of Chechnya. -

Zbwleibniz-Informationszentrum

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Ahmadi, Maryam; Manera, Matteo Working Paper Oil Price Shocks and Economic Growth in Oil- Exporting Countries Working Paper, No. 013.2021 Provided in Cooperation with: Fondazione Eni Enrico Mattei (FEEM) Suggested Citation: Ahmadi, Maryam; Manera, Matteo (2021) : Oil Price Shocks and Economic Growth in Oil-Exporting Countries, Working Paper, No. 013.2021, Fondazione Eni Enrico Mattei (FEEM), Milano This Version is available at: http://hdl.handle.net/10419/237738 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten -

Privatization in Russia: Catalyst for the Elite

PRIVATIZATION IN RUSSIA: CATALYST FOR THE ELITE VIRGINIE COULLOUDON During the fall of 1997, the Russian press exposed a corruption scandal in- volving First Deputy Prime Minister Anatoli Chubais, and several other high- ranking officials of the Russian government.' In a familiar scenario, news organizations run by several bankers involved in the privatization process published compromising material that prompted the dismissal of the politi- 2 cians on bribery charges. The main significance of the so-called "Chubais affair" is not that it pro- vides further evidence of corruption in Russia. Rather, it underscores the im- portance of the scandal's timing in light of the prevailing economic environment and privatization policy. It shows how deliberate this political campaign was in removing a rival on the eve of the privatization of Rosneft, Russia's only remaining state-owned oil and gas company. The history of privatization in Russia is riddled with scandals, revealing the critical nature of the struggle for state funding in Russia today. At stake is influence over defining the rules of the political game. The aim of this article is to demonstrate how privatization in Russia gave birth to an oligarchic re- gime and how, paradoxically, it would eventually destroy that very oligar- chy. This article intends to study how privatization influenced the creation of the present elite structure and how it may further transform Russian decision making in the foreseeable future. Privatization is generally seen as a prerequisite to a market economy, which in turn is considered a sine qua non to establishing a democratic regime. But some Russian analysts and political leaders disagree with this approach. -

A Three-Way Analysis of the Relationship Between the USD Value and the Prices of Oil and Gold: a Wavelet Analysis

AIMS Energy, 6(3): 487–504. DOI: 10.3934/energy.2018.3.487 Received: 18 April 2018 Accepted: 30 May 2018 Published: 08 June 2018 http://www.aimspress.com/journal/energy Research article A three-way analysis of the relationship between the USD value and the prices of oil and gold: A wavelet analysis Basheer H. M. Altarturi1, Ahmad Alrazni Alshammari1, Buerhan Saiti2,*, and Turan Erol2 1 Institute of Islamic Banking and Finance, International Islamic University Malaysia, Kuala Lumpur, Malaysia 2 Istanbul Sabahattin Zaim University, Istanbul, Turkey * Correspondence: Email: [email protected]. Abstract: This study examines the relationships among oil prices, gold prices, and the USD real exchange rate. It adopts the wavelet approach as a nonlinear causality technique to decompose the data into various scales over time. Higher-order coherence and partial coherence were used to identify the lead-lag effect and mutual coherence function among the variables. The results show that changes in the USD exchange rate influence the prices of oil and gold negatively in the short- and medium-term. While in the long-term, the oil price has a negative impact on the value of the USD. Oil and gold are significantly linked and correlated because their prices are determined in USD. The findings of this paper have significant implications, particularly for risk management. Keywords: wavelet; partial wavelet coherence; U.S. dollar value; oil prices; gold prices 1. Introduction Examining the nexus between oil and gold is an established practice among researchers in the field of economics due to the importance of these variables. Oil is considered the primary driver of the economy. -

Overlap Issues Consent Order

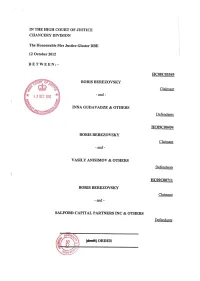

IN THE HIGH COURT OF JUSTICE CHANCERY DIVISION The Honourable Mrs Justice Gloster DBE 12 October 2012 BETWEEN:- HCO8C03549 BORIS BEREZOVSICY Claimant - and - INNA GUDAVADZE & OTHERS Defendants HCO9C00494 BORIS BEREZOVSKY Claimant - and - VASILY ANISIMOV & OTHERS Defendants HCO9C00711 BORIS BEREZOVSICY Claimant - and - SALFORD CAPITAL PARTNERS INC & OTHERS Defendants 1),D 1147 (f) MEEK ORDER UPON the Order of Mr Justice Mann and Mrs Justice Gloster DBE dated 16 August 2010, ordering the trial of the issues set out in paragraph 1 of that Order (the Overlap Issues) as preliminary issues in proceedings number HC08C03549 (the Main Action), HC09C00494 (the Metalloinvest Action) and HCO9C00711 (the Salford Action); AND UPON the trial of the Overlap Issues (as amended by subsequent Orders) together with the trial of the Claimant's claims in Commercial Court proceedings number 2007 Folio 942 (the Joint Trial); AND UPON the Court having heard oral evidence and having read the written evidence filed; AND UPON hearing Leading Counsel for the Claimant, Counsel for the Second to Fifth Defendants in the Main Action (the Family Defendants), Leading Counsel for the Third to Fifth and Tenth Defendants in the Metalloinvest Action (the Anisimov Defendants), and Counsel for the Fourth to Ninth and Eleventh Defendants in the Salford Action (the Salford Defendants); AND UPON the Court having given judgment on the Overlap Issues on 31 August 2012; AND UPON the parties having agreed the orders as to costs set out in paragraphs 2 to 5 of this Order below; IT IS ORDERED THAT:- Determination of the Overlap Issues 1. The Overlap Issues are determined as follows:- (1) The Claimant did not acquire any interest in any Russian aluminium industry assets prior to the alleged meeting at the Dorchester Hotel in March 2000 (other than as a result of the alleged overarching joint venture agreement alleged by the Claimant in the Main Action, in relation to which no findings are made). -

Mr. Chairman, I Welcome the Opportunity to Appear Before The

Mr. Chairman, I welcome the opportunity to appear before the Helsinki Commission to discuss the current situation in Russia and the concerns of all of us about the Putin government and the future of Russia. First, I wish to emphasize the value of the Commission’s mandate and stated criteria to promote compliance with the fundamental standards of civil society in Russia and the other former Soviet republics. Second, those of us who have witnessed first-hand the travesty of justice in Russia much appreciate the concerns expressed by the co-chairmen about the improper handling of the Yukos trial and the sentencing of Mikhail Khodorkovsky and his colleagues by Russian authorities. Your formal statement to the world’s press that the “case appears to the world to be justice directed by politics” and that the “selective prosecution such as appears to be the case here will wreak havoc on Russia’s legal system” reflects that the chairmen of this commission have an accurate view of the Khodorkovsky trial and the weakened state of the legal system in Russia. Third, it is vitally important that the Helsinki Commission continue monitoring the implementation of the provisions of the 1975 Helsinki Accords as they relate to Russia and report its findings to the public. While the U.S. Administration and Congressional leaders must necessarily balance many variables in the bilateral relationship, the Helsinki Commission has a clear mandate to insure that human rights and basic freedoms are maintained in the countries under its jurisdiction. Mr. Chairman, it is my opinion that the rule of law is the cornerstone of civil society because it serves to protect the rights and freedoms of all citizens. -

Oil, Foreign Exchange Swaps and Interest Rates in the GCC Countries Nawaf Almaskati1

Oil, foreign exchange swaps and interest rates in the GCC countries Nawaf Almaskati1 Abstract We examine the relationship between oil prices, FX swaps and local interbank offered rates in the six GCC countries. We also investigate the potential hedging and diversification benefits from adding oil positions to portfolios containing GCC FX swaps or interest rates positions. Our findings confirm that oil predicts, and in some cases cause, movements in the various GCC FX swaps and interbank offered rates. We also find that the Saudi FX swap market has the highest volatility spillover from the oil market compared to other markets in the region. Furthermore, our analysis shows a significant change in liquidity conditions in the GCC FX swap markets following a sudden shift in oil prices. Lastly, we document the presence of significant risk reduction benefits from adding oil exposure to portfolios of GCC FX swaps or interest rates with risk going down by at least half in the case of the GCC FX swaps. Key Words: GCC markets; Oil; FX swaps; Hedging; Interest rates; Volatility spillover. JEL classification: G11; G12; G15 1 University of Waikato 1 1. Introduction Oil plays a major role in the economies of the members of the Gulf Cooperation Council (GCC). Oil and oil-related exports account for more than two thirds of the GCC total exports and are considered as the main sources of USD liquidity in the region. On top of that, income from oil represents the most important source of government funding and is a main driver of major projects and development initiatives. -

A Comparative History of Oil and Gas Markets and Prices: Is 2020 Just an Extreme Cyclical Event Or an Acceleration of the Energy Transition?

April 2020 A Comparative History of Oil and Gas Markets and Prices: is 2020 just an extreme cyclical event or an acceleration of the energy transition? Introduction Natural gas markets have gone through an unprecedented transformation. Demand growth for this relatively clean, plentiful, versatile and now relatively cheap fuel has been increasing faster than for other fossil fuels.1 Historically a `poor relation’ of oil, gas is now taking centre stage. New markets, pricing mechanisms and benchmarks are being developed, and it is only natural to be curious about the direction these developments are taking. The oil industry has had a particularly rich and well recorded history, making it potentially useful for comparison. However, oil and gas are very different fuels and compete in different markets. Their paths of evolution will very much depend on what happens in the markets for energy sources with which they compete. Their history is rich with dominant companies, government intervention and cycles of boom and bust. A common denominator of virtually all energy industries is a tendency towards natural monopoly because they have characteristics that make such monopolies common. 2 Energy projects tend to require multibillion – often tens of billions of - investments with long gestation periods, with assets that can only be used for very specific purposes and usually, for very long-time periods. Natural monopolies are generally resolved either by new entrants breaking their integrated market structures or by government regulation. Historically, both have occurred in oil and gas markets.3 As we shall show, new entrants into the oil market in the 1960s led to increased supply at lower prices, and higher royalties, resulting in the collapse of control by the major oil companies. -

Treisman Silovarchs 9 10 06

Putin’s Silovarchs Daniel Treisman October 2006, Forthcoming in Orbis, Winter 2007 In the late 1990s, many Russians believed their government had been captured by a small group of business magnates known as “the oligarchs”. The most flamboyant, Boris Berezovsky, claimed in 1996 that seven bankers controlled fifty percent of the Russian economy. Having acquired massive oil and metals enterprises in rigged privatizations, these tycoons exploited Yeltsin’s ill-health to meddle in politics and lobby their interests. Two served briefly in government. Another, Mikhail Khodorkovsky, summed up the conventional wisdom of the time in a 1997 interview: “Politics is the most lucrative field of business in Russia. And it will be that way forever.”1 A decade later, most of the original oligarchs have been tripping over each other in their haste to leave the political stage, jettisoning properties as they go. From exile in London, Berezovsky announced in February he was liquidating his last Russian assets. A 1 Quoted in Andrei Piontkovsky, “Modern-Day Rasputin,” The Moscow Times, 12 November, 1997. fellow media magnate, Vladimir Gusinsky, long ago surrendered his television station to the state-controlled gas company Gazprom and now divides his time between Israel and the US. Khodorkovsky is in a Siberian jail, serving an eight-year sentence for fraud and tax evasion. Roman Abramovich, Berezovsky’s former partner, spends much of his time in London, where he bought the Chelsea soccer club in 2003. Rather than exile him to Siberia, the Kremlin merely insists he serve as governor of the depressed Arctic outpost of Chukotka—a sign Russia’s leaders have a sense of humor, albeit of a dark kind. -

RUSSIA INTELLIGENCE Politics & Government

N°66 - November 22 2007 Published every two weeks / International Edition CONTENTS KREMLIN P. 1-4 Politics & Government c KREMLIN The highly-orchestrated launching into orbit cThe highly-orchestrated launching into orbit of of the «national leader» the «national leader» Only a few days away from the legislative elections, the political climate in Russia grew particu- STORCHAK AFFAIR larly heavy with the announcement of the arrest of the assistant to the Finance minister Alexey Ku- c Kudrin in the line of fire of drin (read page 2). Sergey Storchak is accused of attempting to divert several dozen million dol- the Patrushev-Sechin clan lars in connection with the settlement of the Algerian debt to Russia. The clan wars in the close DUMA guard of Vladimir Putin which confront the Igor Sechin/Nikolay Patrushev duo against a compet- cUnited Russia, electoral ing «Petersburg» group based around Viktor Cherkesov, overflows the limits of the «power struc- home for Russia’s big ture» where it was contained up until now to affect the entire Russian political power complex. business WAR OF THE SERVICES The electoral campaign itself is unfolding without too much tension, involving men, parties, fac- cThe KGB old guard appeals for calm tions that support President Putin. They are no longer legislative elections but a sort of plebicite campaign, to which the Russian president lends himself without excessive good humour. The objec- PROFILE cValentina Matvienko, the tive is not even to know if the presidential party United Russia will be victorious, but if the final score “czarina” of Saint Petersburg passes the 60% threshhold. -

Alfa Annual Report

ALFA GROUP CONSOLIDATED FINANCIAL STATEMENTS AND REPORT OF THE AUDITORS FOR THE YEAR ENDED 31 DECEMBER 2001 STATEMENT OF MANAGEMENT’S RESPONSIBILITIES TO THE SHAREHOLDERS OF ALFA GROUP . International convention requires that Management prepare consolidated financial statements which give a true and fair view of the state of affairs of Alfa Group (“the Group”) at the end of each financial period and of the results, cash flows and changes in shareholders’ equity for each period. Management are responsible for ensuring that the Group keeps accounting records which disclose, with reasonable accuracy, the financial position of each entity and which enable it to ensure that the consoli- dated financial statements comply with International Accounting Standards and that their statutory accounting reports comply with the applicable country’s laws and regulations. Furthermore, appropriate adjustments were made to such statutory accounts to present the accompanying consolidated financial statements in accordance with International Accounting Standards. Management also have a general responsibility for taking such steps as are reasonably possible to safeguard the assets of the Group and to prevent and detect fraud and other irregularities. Management considers that, in preparing the consolidated financial statements set out on pages to , the Group has used appropriate and consistently applied accounting policies, which are supported by reasonable and prudent judgments and estimates and that appropriate International Accounting Standards have been followed. For and on behalf of Management Nigel J. Robinson October ZAO PricewaterhouseCoopers Audit Kosmodamianskaya Nab. 52, Bld. 5 115054 Moscow Russia Telephone +7 (095) 967 6000 Facsimile +7 (095) 967 6001 REPORT OF THE AUDITORS TO THE SHAREHOLDERS OF ALFA GROUP .