Annual Report 1 FINANCIAL HIGHLIGHTS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Fidelity® Emerging Markets Index Fund

Quarterly Holdings Report for Fidelity® Emerging Markets Index Fund January 31, 2021 EMX-QTLY-0321 1.929351.109 Schedule of Investments January 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 92.5% Shares Value Shares Value Argentina – 0.0% Lojas Americanas SA rights 2/4/21 (b) 4,427 $ 3,722 Telecom Argentina SA Class B sponsored ADR (a) 48,935 $ 317,099 Lojas Renner SA 444,459 3,368,738 YPF SA Class D sponsored ADR (b) 99,119 361,784 Magazine Luiza SA 1,634,124 7,547,303 Multiplan Empreendimentos Imobiliarios SA 156,958 608,164 TOTAL ARGENTINA 678,883 Natura & Co. Holding SA 499,390 4,477,844 Notre Dame Intermedica Participacoes SA 289,718 5,003,902 Bailiwick of Jersey – 0.1% Petrobras Distribuidora SA 421,700 1,792,730 Polymetal International PLC 131,532 2,850,845 Petroleo Brasileiro SA ‑ Petrobras (ON) 2,103,697 10,508,104 Raia Drogasil SA 602,000 2,741,865 Bermuda – 0.7% Rumo SA (b) 724,700 2,688,783 Alibaba Health Information Technology Ltd. (b) 2,256,000 7,070,686 Sul America SA unit 165,877 1,209,956 Alibaba Pictures Group Ltd. (b) 6,760,000 854,455 Suzano Papel e Celulose SA (b) 418,317 4,744,045 Beijing Enterprises Water Group Ltd. 2,816,000 1,147,720 Telefonica Brasil SA 250,600 2,070,242 Brilliance China Automotive Holdings Ltd. 1,692,000 1,331,209 TIM SA 475,200 1,155,127 China Gas Holdings Ltd. 1,461,000 5,163,177 Totvs SA 274,600 1,425,346 China Resource Gas Group Ltd. -

The Annual Report on the Most Valuable and Strongest Real Estate Brands June 2020 Contents

Real Estate 25 2020The annual report on the most valuable and strongest real estate brands June 2020 Contents. About Brand Finance 4 Get in Touch 4 Brandirectory.com 6 Brand Finance Group 6 Foreword 8 Executive Summary 10 Brand Finance Real Estate 25 (USD m) 13 Sector Reputation Analysis 14 COVID-19 Global Impact Analysis 16 Definitions 20 Brand Valuation Methodology 22 Market Research Methodology 23 Stakeholder Equity Measures 23 Consulting Services 24 Brand Evaluation Services 25 Communications Services 26 Brand Finance Network 28 © 2020 All rights reserved. Brand Finance Plc, UK. Brand Finance Real Estate 25 June 2020 3 About Brand Finance. Brand Finance is the world's leading independent brand valuation consultancy. Request your own We bridge the gap between marketing and finance Brand Value Report Brand Finance was set up in 1996 with the aim of 'bridging the gap between marketing and finance'. For more than 20 A Brand Value Report provides a years, we have helped companies and organisations of all types to connect their brands to the bottom line. complete breakdown of the assumptions, data sources, and calculations used We quantify the financial value of brands We put 5,000 of the world’s biggest brands to the test to arrive at your brand’s value. every year. Ranking brands across all sectors and countries, we publish nearly 100 reports annually. Each report includes expert recommendations for growing brand We offer a unique combination of expertise Insight Our teams have experience across a wide range of value to drive business performance disciplines from marketing and market research, to and offers a cost-effective way to brand strategy and visual identity, to tax and accounting. -

AGILE GROUP HOLDINGS LIMITED (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 3383)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. This announcement does not constitute an offer to sell or the solicitation of an offer to buy any securities in the United States or any other jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. The securities referred to herein will not be registered under the United States Securities Act of 1933, as amended (the “Securities Act”), and may not be offered or sold in the United States except pursuant to an exemption from, or a transaction not subject to, the registration requirements of the Securities Act. Any public offering of securities to be made in the United States will be made by means of a prospectus. Such prospectus will contain detailed information about the company making the offer and its management and financial statements. The Company does not intend to make any public offering of securities in the United States. AGILE GROUP HOLDINGS LIMITED (Incorporated in the Cayman Islands with limited liability) (Stock Code: 3383) OVERSEAS REGULATORY ANNOUNCEMENT This overseas regulatory announcement is issued pursuant to Rule 13.10B of the Rules Governing the Listing of Securities (the “Listing Rules”) on The Stock Exchange of Hong Kong Limited (the “Stock Exchange”). -

Spatiotemporal Analysis of the Dengue Outbreak in Guangdong Province, China Guanghu Zhu1,2,3†, Jianpeng Xiao2†,Taoliu2, Bing Zhang2, Yuantao Hao3 and Wenjun Ma2*

Zhu et al. BMC Infectious Diseases (2019) 19:493 https://doi.org/10.1186/s12879-019-4015-2 RESEARCH ARTICLE Open Access Spatiotemporal analysis of the dengue outbreak in Guangdong Province, China Guanghu Zhu1,2,3†, Jianpeng Xiao2†,TaoLiu2, Bing Zhang2, Yuantao Hao3 and Wenjun Ma2* Abstract Background: Dengue is becoming a major public health concern in Guangdong (GD) Province of China. The problem was highlighted in 2014 by an unprecedented explosive outbreak, where the number of cases was larger than the total cases in previous 30 years. The present study aimed to clarify the spatial and temporal patterns of this dengue outbreak. Methods: Based on the district/county-level epidemiological, demographic and geographic data, we first used Moran’s I statistics and Spatial scan method to uncover spatial autocorrelation and clustering of dengue incidence, and then estimated the spatial distributions of mosquito ovitrap index (MOI) by using inverse distance weighting. We finally employed a multivariate time series model to quantitatively decompose dengue cases into endemic, autoregressive and spatiotemporal components. Results: The results indicated that dengue incidence was highly spatial-autocorrelated with the inclination of clustering and nonuniformity. About 12 dengue clusters were discovered around Guangzhou and Foshan with significant differences by district/county, where the most likely cluster with the largest relative risk located in central Guangzhou in October. Three significant high-MOI areas were observed around Shaoguan, Qingyuan, Shanwei and Guangzhou. It was further found the districts in Guagnzhou and Foshan were prone to local autoregressive transmission, and most region in southern and central GD exhibited higher endemic components. -

AGILE PROPERTY HOLDINGS LIMITED (Incorporated in the Cayman Islands with Limited Liability) Stock Code: 3383

雅居樂地產控股有限公司 AGILE PROPERTY HOLDINGS LIMITED (Incorporated in the Cayman Islands with limited liability) Stock code: 3383 Annual Report 2009 2009 Projects on Sale Corporate Profile The Group is one of leading property developers in China. It is principally engaged in the development of large-scale comprehensive property projects. The Group currently owns a diversified portfolio of 66 projects in various stages of development (including 5 developed and sold projects) in 22 different cities and districts such as Guangzhou, Zhongshan, Foshan, Heyuan, Huizhou, Shanghai, Changzhou, Nanjing, Chengdu, Xi’an, Chongqing, Shenyang and Hainan. As of 15 April 2010, the Group has a land bank with total GFA of approximately 32.15 million sq. m. (including both lands with titles and contractual interests). The shares of Agile have been listed on the Main Board of The Stock Exchange of Hong Kong Limited since 15 December 2005 under (Stock code: 3383). They are included as constituent stocks in Morgan Stanley Capital International China Index, the Hang Seng Composite Index and the Hang Seng Freefloat Composite Index. Contents 2 Financial Highlights 84 Senior Management’s Profi le 4 Business Structure 86 Corporate Governance Report 6 Milestone 2009 94 Report of the Directors 8 Honours and Awards 108 Independent Auditor’s Report 10 Chairman’s Statement 110 Consolidated Balance Sheet 18 Management Discussion and Analysis 112 Balance Sheet 26 Property Development 113 Consolidated Income Statement Land Bank of the Group 114 Consolidated Statement of Comprehensive -

CHINA VANKE CO., LTD.* 萬科企業股份有限公司 (A Joint Stock Company Incorporated in the People’S Republic of China with Limited Liability) (Stock Code: 2202)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. CHINA VANKE CO., LTD.* 萬科企業股份有限公司 (A joint stock company incorporated in the People’s Republic of China with limited liability) (Stock Code: 2202) 2019 ANNUAL RESULTS ANNOUNCEMENT The board of directors (the “Board”) of China Vanke Co., Ltd.* (the “Company”) is pleased to announce the audited results of the Company and its subsidiaries for the year ended 31 December 2019. This announcement, containing the full text of the 2019 Annual Report of the Company, complies with the relevant requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited in relation to information to accompany preliminary announcement of annual results. Printed version of the Company’s 2019 Annual Report will be delivered to the H-Share Holders of the Company and available for viewing on the websites of The Stock Exchange of Hong Kong Limited (www.hkexnews.hk) and of the Company (www.vanke.com) in April 2020. Both the Chinese and English versions of this results announcement are available on the websites of the Company (www.vanke.com) and The Stock Exchange of Hong Kong Limited (www.hkexnews.hk). In the event of any discrepancies in interpretations between the English version and Chinese version, the Chinese version shall prevail, except for the financial report prepared in accordance with International Financial Reporting Standards, of which the English version shall prevail. -

Agile Property (3383 HK) Neutral (Maintained) Property - Real Estate Target Price: HKD6.30 Market Cap: USD3,051M Price: HKD6.04

Company Update, 5 June 2015 Agile Property (3383 HK) Neutral (Maintained) Property - Real Estate Target Price: HKD6.30 Market Cap: USD3,051m Price: HKD6.04 Macro Risks 2 Key Takeaways From Zhongshan Visit Growth . 2 0 Value . 01 0 . 02 0 We recently visited Agile’s four major projects in Zhongshan (tier-3 . Agile Property Holdings (3383 HK) 0 Price Close Relative to Hang Seng Index (RHS) city). Reiterate NEUTRAL with a higher HKD6.30 TP (4% upside), 0 7.4 110 following the sector valuation upgrade. Key takeaways: i) a preliminary 0 6.9 104 recovery in sales volume, driven by end-users and loosening mortgage approvals, and ii) ASP tends to stabilise, but upside is limited. We 6.4 98 remain concerned on Agile’s low-tier cities exposure (75% of its 5.9 91 landbank) and profit margin erosion. 5.4 85 Zhongshan the home base. Agile Property (Agile) was founded in 4.9 79 Zhongshan in 1992. It had been headquartered in the city since its establishment, until the headquarters was moved to Guangzhou in 2012. 4.4 73 Zhongshan is the highest contributing city, generating 13.7% and 18.4% 3.9 66 of landbank and contracted sales revenue, respectively, as of end-FY14. In turn, Agile is the market leader in Zhongshan, given that it achieved 3.4 60 250 the highest sales revenue among its peers in 2014. 200 150 Desirable sell-through, but likely an isolated case for Zhongshan. Benefitting from its brand reputation and track record in Zhongshan, 100 Agile’s projects are supported by end-user demand and loosening 50 mortgage approvals from banks. -

(852) 2861-9299

Network Hospital List For assistance or for updated hospital information, you may call the 24-hour IPA Service Hotline. IPA reserves the final right to amend this list of hospitals at any time without prior notice. : (852) 2861-9299 Province/City Hospital Name Address 111 Guangzhou Military Hospital No. 111 Liuhua Road, Guangzhou, Guangdong 48 Guangzhou Huadu District People's No. 48 Xinhua Road, Xinhuazhen, Huadu, Guangzhou Hospital 1838 Southern Hospital No.1838 Dadao North, Guangzhou 253 The First Military Medical University No. 253 Gongyeda Road, Guangzhou Zhujiang Hospital 111 Guangdong Provincial Chinese Medicine No. 111 Dade Road, Guangzhou, Guangdong Hospital 167 Guangzhou Sailor Hospital No. 167 Xingang West Road, Guangzhou, Guangdong 196 Hospital of Guangzhou Economic & No.196 Youyi Road, Guangzhou Economic Technical Development Area Technological Development District Guangdong 1 Guangzhou No.12 People's Hospital No. 1 Xitianqiang Road, Huangpu Road, Guangzhou 65 Guangzhou Panyu Qu Chinese Hospital No. 65 Qiaodong Road, Shiqiao Street, Panyu, Guangzhou Guangdong 19 Eur Am Int l Medical Center No. 19 Huali Road, Zhujiangxincheng, Guangzhou 368 Can Am Medical Center Huayuan Plaza No. 368, Huanshi East Road, Guangzhou Shanwei People's Hospital Lane 2 Min Zhu Plaza, Sanwei, Guangdong Chaoyang People's Hospital Xishuang, Chaoyang, Guangdong 24 Yangchun People's Hospital No. 24 Huangsheng South Road, Chunschengzhen, Yangchun, Guangdong Yangjiang Chinese Medicine Hospital Moyang Street, Jiangcheng District, Yangjiang, Guangdong 2 Yangchun -

AGILE GROUP HOLDINGS LIMITED (Incorporated with Limited Liability Under the Laws of the Cayman Islands)

香 港 交 易 及 結 算 所 有 限 公 司 及 香 港 聯 合 交 易 所 有 限 公 司 對 本 公 告 的 內 容 概 不 負 責 , 對 其 準 確 性 或 完 整 性 亦 不 發 表 任 何 聲 明 , 並 明 確 表 示 概 不 就 因 本 公 告 全 部 或 任 何 部 分 內 容 而 產 生 或 因 倚 賴 該 等 內 容 而 引 致 的 任 何 損 失 承 擔 任 何 責 任 。 本 公 告 僅 供 參 考 , 並 不 構 成 收 購 、 購 買 或 認 購 證 券 的 邀 請 或 遊 說 要 約 , 或 邀 請 訂 立 協 議 進 行 上 述 任 何 事 宜 , 亦 無 意 招 攬 任 何 要 約 以 收 購 、 購 買 或 認 購 任 何 證 券 。 本 公 告 並 非 供 於 美 國 或 美 國 境 內 直 接 或 間 接 派 發 。 本 公 告 及 其 所 載 資 料 並 不 構 成 或 組 成 在 美 國 購 買 、 認 購 或 出 售 證 券 的 部 分 要 約 。 除 非 根 據 1933 年 美 國 證 券 法 ( 經 修 訂 ()「 證 券 法 」)登 記 或 獲 適 用 豁 免 登 記 規 定 , 否 則 證 券 不 得 在 美 國 提 呈 發 售 或 出 售 。 在 美 國 公 開 發 售 任 何 證 券 將 通 過 載 有 與 本 公 司 及 管 理 層 有 關 的 詳 細 資 料 以 及 財 務 報 表 的 招 股 章 程 的 方 式 進 行 。 本 公 告 所 述 證 券 並 無 及 將 不 會 根 據 證 券 法 登 記 , 且 不 會 在 美 國 公 開 發 售 任 何 證 券 。 本 公 告 所 述 證 券 將 根 據 所 有 適 用 法 律 法 規 出 售 。 本 公 告 或 其 所 載 資 料 並 非 用 以 招 攬 金 錢 、 證 券 或 其 他 代 價 , 而 倘 為 回 應 本 公 告 或 其 所 載 資 料 而 寄 出 金 錢 、 證 券 或 其 他 代 價 , 則 不 會 獲 接 納 。 本 公 告 並 非 歐 洲 經 濟 區(「 歐 洲 經 濟 區 」)成 員 國 所 實 施 歐 盟 指 令 2003 / 71 / EC( 及 其 任 何 修 訂 )所 界 定 之 招 股 章 程 。 無 PRIIPs 重 要 資 訊 文 件 - 由 於 不 可 於 歐 洲 經 濟 區 進 行 零 售 , 故 並 無 編 製 PRIIPs 重 要 資 訊 文 件 。 本 公 告 及 有 關 據 此 提 呈 發 行 證 券 之 任 何 其 他 文 件 或 資 料 並 非 由 英 國《 2000 年 金 融 服 務 與 市 場 法 》( 經 修 訂 )第 21 條 所 界 定 之 認 可 人 士 發 佈 , 而 有 關 文 件 及 ╱ 或 資 料 亦 未 經 其 批 准 。 因 此 , 有 關 文 件 及 ╱ 或 資 料 並 不 會 向 英 國 公 眾 人 士 派 發 , 亦 不 得 向 英 國 公 眾 人 士 傳 遞 。 有 關 文 件 及 ╱ 或 資 料 僅 作 為 財 務 推 廣 向 在 英 國 擁 有 相 關 專 業 投 資 經 驗 及 屬 於《 2000 年 金 融 服 務 與 市 場 法 》2005 年( 財 務 推 廣 )命 令( 經 修 訂 ) (「 財 務 推 廣 命 令 」)第 19 (5) 條 所 界 定 之 投 資 專 業 人 士 , 或 屬 於 財 務 推 廣 命 令 第 49 (2) (a) 至 (d) 條 範 圍 之 人 士 , 或 根 據 財 務 推 廣 命 令 可 以 其 他 方 式 -

Clarks Tannery List

LEATHER SUPPLIERS (TANNERIES) SS21 COUNTRY SUPPLIER GROUP FACTORY NAME ADDRESS Argentina Hispano S.A. La Hispano Argentina Curtiembre y charoleria WORKERS <500 Av. Juan B Alberdi 5045/49 FEMALE MALE Buenos Aires OAR ID AR2020028Y07RTR Argentina GEOLOCATION C1440AAB -34.6458547 -58.4964907 Argentina Sadesa Sadesa S.A. WORKERS 501 - 1,000 DE LA RIBERA SUR 664 FEMALE <25% MALE >75% LOMAS DE ZAMORA OAR ID AR20200284WGEGF PCIA DE BS.AIRES REP. ARGENTINA GEOLOCATION -34.7081658 -58.4536824 Brazil CBC Couros e acabamentos Ltda. WORKERS <500 Estrada Leopoldo Petry FEMALE MALE 255 OAR ID BR2020028AGT1C3 Novo Hamburgo RS. Brazil GEOLOCATION -29.716984 -51.1090575 China Nedlink Resources Ltd WORKERS <500 Fu Ze 2nd Street, Fu Ze Road FEMALE <25% MALE >75% Gao Ping Industrial Zone OAR ID CN2020028QXMCE1 San Jiao Zhongshan GEOLOCATION Guangdong, China 528445 22.677198 113.46188 Page 1 of 14 LEATHER SUPPLIERS (TANNERIES) SS21 COUNTRY SUPPLIER GROUP FACTORY NAME ADDRESS China DongGuan JingHong Shoe Material CO.LTD WORKERS <500 South Industrial Zone FEMALE >25% MALE >50% LiuChongWei OAR ID CN20200282REYPV WanJiang District DongGuan City GEOLOCATION GuangDong province 23.047104 113.738543 China Heng Tong Guangzhou Xuna Leather Co.,Ltd. WORKERS <500 2/F,B/D 4 Yili Industrial Park FEMALE >50% MALE >25% Longtang OAR ID CN2020028VNGX95 Qingcheng District Qingyuan GEOLOCATION Guangdong 23.471394 113.0038866 China Heng Tong Anhui Hengtong Leather Co., Ltd. WORKERS <500 Linjiang Industrial Park FEMALE >50% MALE >25% Fuxing Town OAR ID CN2020028TZ7TPF Susong County Anqing GEOLOCATION Anhui 41.811979 126.918087 China Hispano Huizhou Modapelle Leathers Ltd. WORKERS <500 Shang Sha Road, Sha Tou Industrial District, FEMALE >50% MALE >25% Yuan Zhou Town OAR ID CN2020028R1GM62 Boluo County Huizhou GEOLOCATION Guangdong, PRC 23.075215 114.100057 Page 2 of 14 LEATHER SUPPLIERS (TANNERIES) SS21 COUNTRY SUPPLIER GROUP FACTORY NAME ADDRESS China ISA ISA Heshan Trading Limited WORKERS <500 No. -

China Property Sector

China / Hong Kong Industry Focus China Property Sector Refer to important disclosures at the end of this report DBS Group Research . Equity 19 Apr 2021 Spotlight on future land supply • Solid sales growth momentum sustained with strong HSI: 28,970 potential to ink another year of record-high sales • Developers poised to meet their 2021 targets ANALYST Jason LAM +852 3668 4179 [email protected] • Future land supply and new starts as keys to watch for Danielle WANG CFA, +852 3668 4176 [email protected] • Sector top picks: Vanke, COLI, CIFI and Logan Ken HE CFA, +86 21 3896 8221 [email protected] Solid performance in 1Q21; strong potential for another year of Ben Wong [email protected] record-high residential sales. Residential sales in Mar rose 63% y-o-y (or 44% vs Mar-19) on the back of a 38% (or 19% vs Mar- Recommendation & valuation 19) increment in residential GFA sold and 19% (or 21% vs Mar- 19) rise in residential ASP, marking another solid month of FY22F physical market performance. We believe the market is well- Target Price Price Rec Mkt Cap PE poised to post another record-high sales value this year – as it HK$ HK$ US$bn x will likely attain 2020’s level even if the market records a 12.5% y- o-y decline for the remaining nine months. China Overseas Developers well on track to achieve their 2021 targets. Presales 20.15 25.70 BUY 28.4 4.0 (688 HK) growth of 30 listed developers we track on a weighted-average China Vanke 'H' 28.25 45.56 BUY 49.9 5.3 basis remained strong at 47% y-o-y (or +33% vs Mar 2019) in (2202 HK) Mar (Feb-21: 144%), as compared to their c.10% weighted Logan Property 12.50 16.44 BUY 8.9 3.5 average presales target for 2021. -

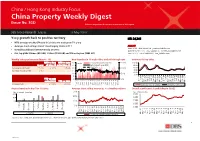

China Property Weekly Digest (Issue No

China / Hong Kong Industry Focus China Property Weekly Digest (Issue No. 302) Refer to important disclosures at the end of this report DBS Group Research . Equity 13 May 2020 Y-o-y growth back to positive territory HSI: 24,246 • MTD average weekly GFA sold in 29 cities we track grew 7% y-o-y • Average short-selling interest stood largely stable at 11% ANALYST Jason LAM +852 36684179 [email protected] • Overall southbound interest steady at 5.65% Danielle WANG CFA, +852 36684176 [email protected] • Our top picks: Shimao (813 HK), Yuzhou (1628 HK) and China Aoyuan (3883 HK) Ken HE CFA, +86 2138968221 [email protected] Weekly sales performance (May 4 – 10) New launches in 10 major cities and sell-through rate Inventory in key cities MTD vs Avg MTD vs same 30 k units Total units launched (LHS) 150% 100.0 w-o-w of May -19 period May-19 25 Sell-through rate (RHS) 80.0 Avg weekly GFA sold ↑ 1.4% ↓ 1.1% ↑ 7.0% 20 26w avg 100% 60.0 Inventory (no. of weeks) ↑ 3.7 15 40.0 20.0 10 50% 0.0 5 YTD vs same 0 0% Jul-13 Jul-18 Jan-11 Jan-16 Jun-11 Jun-16 Feb-13 Oct-14 Feb-18 Oct-19 Apr-12 Sep-12 Apr-17 Sep-17 Dec-13 Dec-18 Nov-11 Nov-16 Mar-15 Mar-20 Aug-15 May-14 period 2019 YTD vs 2019 May-19 7W17 2W18 1W19 YTD GFA sold ↓ 21.3% ↓ 35.0% 9W19 51W16 15W17 23W17 31W17 39W17 47W17 12W18 20W18 28W18 36W18 45W18 17W19 25W19 33W19 41W19 49W19 12W20 Inventory (no.