Agile Property Holdings (3383.HK) Above Expectations: Steady Growth

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

* This Document Is Important and Requires Your

THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in doubt as to any aspect of this document, you should consult your licensed securities dealer, bank manager, Sch I front page solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Henderson China Holdings Limited, you should at once hand this document and the accompanying forms of proxy to the purchaser or transferee or to the bank, licensed securities dealer or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. The Stock Exchange of Hong Kong Limited takes no responsibility for the contents of this document, makes no representation as to its accuracy or completeness and expressly disclaims any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this document. * (Stock Code: 0246) PROPOSED PRIVATISATION BY BY WAY OF A SCHEME OF ARRANGEMENT (UNDER SECTION 99 OF THE COMPANIES ACT 1981 OF BERMUDA) INVOLVING THE CANCELLATION OF ALL THE ISSUED SHARES OF HK$1.00 EACH IN HENDERSON CHINA HOLDINGS LIMITED HELD BY THE SCHEME SHAREHOLDERS (AS DEFINED HEREIN) Financial Adviser to Henderson Land Development Company Limited Sch I Para 1 Independent financial adviser to the Independent Board Committee (as defined herein) of Henderson China Holdings Limited A letter from the board of directors of Henderson China Holdings Limited is set out on pages 8 to 17 of this document. An explanatory statement regarding the Proposal (as defined herein) is set out on pages 46 to 63 of this document. -

ANNUAL REPORT ADDITIONAL INFORMATION All Figures in This Document Are Expressed in Canadian Dollars, Unless Otherwise Indicated

2009 ANNUAL REPORT ADDITIONAL INFORMATION All figures in this document are expressed in Canadian dollars, unless otherwise indicated. This publication, as well as the 2009 Annual Report, are available at www.lacaisse.com. Information: 514 842-3261 [email protected] Ce document, de même que le Rapport annuel 2009, sont disponibles en français sur www.lacaisse.com. Legal Deposit – Bibliothèque et Archives nationales du Québec, 2010 50% Annual Report 2009 – Additional Information I. Tables of returns 1. Auditors’ Report ................................................................................................. 1 2. General Notes .................................................................................................... 2 3. Short Term Investments ....................................................................................... 4 4. Real Return Bonds ............................................................................................... 6 5. Long Term Bonds ................................................................................................. 8 6. Bonds .............................................................................................................. 10 7. Bonds - Fixed Income .......................................................................................... 12 8. Canadian Equity ................................................................................................ 14 9. Publicly Traded Canadian Equity Markets ............................................................. -

Fidelity® Emerging Markets Index Fund

Quarterly Holdings Report for Fidelity® Emerging Markets Index Fund January 31, 2021 EMX-QTLY-0321 1.929351.109 Schedule of Investments January 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks – 92.5% Shares Value Shares Value Argentina – 0.0% Lojas Americanas SA rights 2/4/21 (b) 4,427 $ 3,722 Telecom Argentina SA Class B sponsored ADR (a) 48,935 $ 317,099 Lojas Renner SA 444,459 3,368,738 YPF SA Class D sponsored ADR (b) 99,119 361,784 Magazine Luiza SA 1,634,124 7,547,303 Multiplan Empreendimentos Imobiliarios SA 156,958 608,164 TOTAL ARGENTINA 678,883 Natura & Co. Holding SA 499,390 4,477,844 Notre Dame Intermedica Participacoes SA 289,718 5,003,902 Bailiwick of Jersey – 0.1% Petrobras Distribuidora SA 421,700 1,792,730 Polymetal International PLC 131,532 2,850,845 Petroleo Brasileiro SA ‑ Petrobras (ON) 2,103,697 10,508,104 Raia Drogasil SA 602,000 2,741,865 Bermuda – 0.7% Rumo SA (b) 724,700 2,688,783 Alibaba Health Information Technology Ltd. (b) 2,256,000 7,070,686 Sul America SA unit 165,877 1,209,956 Alibaba Pictures Group Ltd. (b) 6,760,000 854,455 Suzano Papel e Celulose SA (b) 418,317 4,744,045 Beijing Enterprises Water Group Ltd. 2,816,000 1,147,720 Telefonica Brasil SA 250,600 2,070,242 Brilliance China Automotive Holdings Ltd. 1,692,000 1,331,209 TIM SA 475,200 1,155,127 China Gas Holdings Ltd. 1,461,000 5,163,177 Totvs SA 274,600 1,425,346 China Resource Gas Group Ltd. -

The Annual Report on the Most Valuable and Strongest Real Estate Brands June 2020 Contents

Real Estate 25 2020The annual report on the most valuable and strongest real estate brands June 2020 Contents. About Brand Finance 4 Get in Touch 4 Brandirectory.com 6 Brand Finance Group 6 Foreword 8 Executive Summary 10 Brand Finance Real Estate 25 (USD m) 13 Sector Reputation Analysis 14 COVID-19 Global Impact Analysis 16 Definitions 20 Brand Valuation Methodology 22 Market Research Methodology 23 Stakeholder Equity Measures 23 Consulting Services 24 Brand Evaluation Services 25 Communications Services 26 Brand Finance Network 28 © 2020 All rights reserved. Brand Finance Plc, UK. Brand Finance Real Estate 25 June 2020 3 About Brand Finance. Brand Finance is the world's leading independent brand valuation consultancy. Request your own We bridge the gap between marketing and finance Brand Value Report Brand Finance was set up in 1996 with the aim of 'bridging the gap between marketing and finance'. For more than 20 A Brand Value Report provides a years, we have helped companies and organisations of all types to connect their brands to the bottom line. complete breakdown of the assumptions, data sources, and calculations used We quantify the financial value of brands We put 5,000 of the world’s biggest brands to the test to arrive at your brand’s value. every year. Ranking brands across all sectors and countries, we publish nearly 100 reports annually. Each report includes expert recommendations for growing brand We offer a unique combination of expertise Insight Our teams have experience across a wide range of value to drive business performance disciplines from marketing and market research, to and offers a cost-effective way to brand strategy and visual identity, to tax and accounting. -

For Personal Use Only Use Personal For

13 November 2014 Norton Rose Fulbright Australia ABN 32 720 868 049 Level 15, RACV Tower 485 Bourke Street MELBOURNE VIC 3000 AUSTRALIA Tel +61 3 8686 6000 Company Announcements Fax +61 3 8686 6505 Australian Securities Exchange GPO Box 4592, Melbourne VIC 3001 Level 2 120 King Street DX 445 Melbourne MELBOURNE VIC 3000 nortonrosefulbright.com Direct line +61 3 8686 6710 Email [email protected] Our reference: 2813782 Dear Sir/Madam Takeover bid by Transcendent Resources Limited for Roc Oil Company Limited (ROC) – interests of substantial holder We act for Transcendent Resources Limited ( Fosun ) and its associated companies and controllers, which includes Fosun International Limited ( Fosun Parties ) in relation to Fosun’s off-market takeover bid for all of the ordinary shares in Roc Oil Company Limited ( ROC ). On behalf of the Fosun Parties and in accordance with section 671B of the Corporations Act 2001 (Cth), we enclose a notice of change of interests of substantial holder in respect of ROC ( Form 604 ). This notice will be provided to ROC today. Yours faithfully James Stewart Partner Norton Rose Fulbright Australia Encl. For personal use only APAC-#24924633-v1 Norton Rose Fulbright Australia is a law firm as defined in the Legal Profession Acts of the Australian states and territory in which it practises. Norton Rose Fulbright Australia, Norton Rose Fulbright LLP, Norton Rose Fulbright Canada LLP, Norton Rose Fulbright South Africa (incorporated as Deneys Reitz Inc) and Fulbright & Jaworski LLP, each of which is a separate legal entity, are members of Norton Rose Fulbright Verein, a Swiss Verein. -

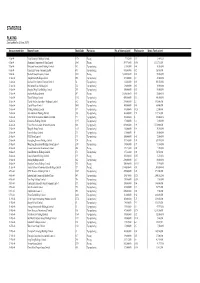

PLACING (Last Updated on 22 June 2007)

STATISTICS PLACING (Last updated on 22 June 2007) Announcement date Name of issuer Stock Code Particulars No. of shares placed Placing price Gross Funds raised (HK$) 5-Jan-04 Vitop Bioenergy Holdings Limited 1178 Placing 7,752,000 0.31 2,403,120 6-Jan-04 Aluminum Corporation of China Limited 2600 Placing 549,976,000 5.658 3,111,764,208 7-Jan-04 Perfectech International Holdings Limited 765 Top-up placing 21,000,000 0.68 14,280,000 8-Jan-04 China Eagle Group Company Limited 493 Top-up placing 473,000,000 0.12 56,760,000 9-Jan-04 Medtech Group Company Limited 1031 Placing 5,000,000,000 0.01 50,000,000 12-Jan-04 Tongda Group Holdings Limited 698 Top-up placing 227,500,000 0.2 45,500,000 13-Jan-04 Kowloon Development Company Limited 34 Top-up placing 83,000,000 6.85 568,550,000 13-Jan-04 Millennium Sense Holdings Ltd 724 Top-up placing 30,000,000 0.63 18,900,000 13-Jan-04 Shanghai Ming Yuan Holdings Limited 233 Top-up placing 100,000,000 0.55 55,000,000 13-Jan-04 Starbow Holdings Limited 397 Placing 2,000,000,000 0.01 20,000,000 13-Jan-04 Titan (Holdings) Limited 1192 Top-up placing 450,000,000 0.92 414,000,000 15-Jan-04 Chaoda Modern Agriculture (Holdings) Limited 682 Top-up placing 280,000,000 2.5 683,000,000 15-Jan-04 Capital Prosper Limited 1003 Top-up placing 140,000,000 0.05 68,000,000 15-Jan-04 Paliburg Holdings Limited 617 Top-up placing 180,000,000 0.128 22,500,000 15-Jan-04 Asia Aluminum Holdings Limited 930 Top-up placing 332,000,000 1.56 517,920,000 15-Jan-04 Silver Grant International Industries Limited 171 Top-up placing 165,000,000 -

Shanghai Forte Land Co., Ltd.*

14.63(2)(c) THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt about this circular or as to the action to be taken, you should consult your stockbroker, bank manager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Shanghai Forte Land Co., Ltd.*, you should at once hand this circular to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. Hong Kong Exchange and Clearing Limited and The Stock Exchange of Hong Kong Limited take no 14.58(1) responsibility for the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. App1B1 SHANGHAI FORTE LAND CO., LTD.* (a sino-foreign joint stock company incorporated in the People’s Republic of China with limited liability) 13.51A (Stock Code: 02337) MAJOR TRANSACTION ACQUISITION OF THE ENTIRE ISSUED QUOTAS IN THE CAPITAL OF GARDEN PLAZA CAPITAL SRL A letter from the Board is set out on pages 5 to 10 of this circular. * For identification purpose only 25 June 2010 CONTENTS pages Definitions ............................................................... 1 Letter from the Board ..................................................... 5 Appendix I — Financial Information of the Group .......................... I-1 Appendix II — Financial information of the Target Group .................... II-1 Appendix III — Unaudited pro forma financial information of the Enlarged Group ...................................III-1 Appendix IV — Valuation Report .........................................IV-1 Appendix V — General Information ..................................... -

AGILE GROUP HOLDINGS LIMITED (Incorporated in the Cayman Islands with Limited Liability) (Stock Code: 3383)

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. This announcement does not constitute an offer to sell or the solicitation of an offer to buy any securities in the United States or any other jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. The securities referred to herein will not be registered under the United States Securities Act of 1933, as amended (the “Securities Act”), and may not be offered or sold in the United States except pursuant to an exemption from, or a transaction not subject to, the registration requirements of the Securities Act. Any public offering of securities to be made in the United States will be made by means of a prospectus. Such prospectus will contain detailed information about the company making the offer and its management and financial statements. The Company does not intend to make any public offering of securities in the United States. AGILE GROUP HOLDINGS LIMITED (Incorporated in the Cayman Islands with limited liability) (Stock Code: 3383) OVERSEAS REGULATORY ANNOUNCEMENT This overseas regulatory announcement is issued pursuant to Rule 13.10B of the Rules Governing the Listing of Securities (the “Listing Rules”) on The Stock Exchange of Hong Kong Limited (the “Stock Exchange”). -

Shanghai Forte Land Co., Ltd.*

14.63(2)(b) THIS CIRCULAR IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION 14A.58(3)(b) If you are in any doubt about this circular or as to the action to be taken, you should consult your stockbroker, 14.63(2)(b) bankmanager, solicitor, professional accountant or other professional adviser. If you have sold or transferred all your shares in Shanghai Forte Land Co., Ltd.*, you should at once hand this circular 14A.58(3)(b) to the purchaser or transferee or to the bank, stockbroker or other agent through whom the sale or transfer was effected for transmission to the purchaser or transferee. Hong Kong Exchange and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for 14.58(1) the contents of this circular, make no representation as to its accuracy or completeness and expressly disclaim any 14A.59(1) liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this circular. App1B1 SHANGHAI FORTE LAND CO., LTD.* (a sino-foreign joint stock company incorporated in the People’s Republic of China with limited liability) 13.51A (Stock Code: 02337) MAJOR AND CONNECTED TRANSACTION TRANSFER OF A 30% EQUITY INTEREST IN JV COMPANY AND CONNECTED TRANSACTION DOMESTIC SHARE ISSUE Independent Financial Adviser to the Independent Board Committee and the Independent Shareholders of the Company SOMERLEY LIMITED A letter from the Board is set out on pages 1 to 10 of this circular. A letter from the Independent Board Committee which contains recommendations to the Independent Shareholders in respect of the Equity Transfer Agreement and the Capital Injection Agreement is set out on page 11 of this circular. -

Evergrande Real Estate Group (3333.HK) Scalability Potential Not

October 9, 2009 Evergrande Real Estate Group Limited March 1, 2010 ACTION Buy Evergrande Real Estate Group (3333.HK) Return Potential: 29% Scalability potential not priced in; initiate with a Buy rating Source of opportunity Investment Profile We believe that Evergrande’s current valuation does not price in the scalability Low High potential of the company on the back of its: (1) strong balance sheet with optimal Growth Growth Returns * Returns * debt structure post its recent IPO and overseas note issuance; (2) attractive land Multiple Multiple bank portfolio located in 17 key municipalities and provincial capitals throughout Volatility Volatility China, with an average land cost of only 9% of 2009 ASP; (3) a standardized Percentile 20th 40th 60th 80th 100th Evergrande Real Estate Group (3333.HK) operation and product line that helps reduce execution risks during times of rapid Asia Pacific Property Peer Group Average scale expansion; and (4) a seasoned management team that is highly motivated * Returns = Return on Capital For a complete description of the investment profile measures please refer to to achieve its growth targets. We initiate coverage on Evergrande with a Buy the disclosure section of this document. rating and a 12-month NAV-based TP of HK$4.15. Catalyst Key data Current Price (HK$) 3.21 (1) We expect stronger-than-peers property sales performance to be achieved by 12 month price target (HK$) 4.15 Market cap (HK$ mn / US$ mn) 48,150.0 / 6,202.2 Evergrande through: (a) providing affordable, quality-competitive, mid-end Foreign ownership (%) -- properties to capitalize on the fast growing housing upgrade needs of less developed provincial capitals in China, and (b) setting asset turnover rather than 12/08 12/09E 12/10E 12/11E EPS (Rmb) 0.21 0.07 0.52 0.59 margin expansion as the business objective in a policy tightening environment, EPS growth (%) (53.9) (65.8) 630.7 13.9 which we think is practical. -

Fosun International Limited Shanghai Forte Land Co., Ltd.*

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no 14.58(1) Note 5 to responsibility for the contents of this announcement, make no representation as to its accuracy or completeness 13.52 and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. FOSUN INTERNATIONAL LIMITED (Incorporated in Hong Kong with limited liability SHANGHAI FORTE LAND CO., LTD.* (a sino-foreign joint stock limited company incorporated in the under the Companies Ordinance) People’s Republic of China with limited liability) (Stock Code: 00656) (Stock Code: 02337) 13.51A JOINT ANNOUNCEMENT TRANSFER OF A 30% EQUITY INTEREST IN JV COMPANY MAJOR AND CONNECTED TRANSACTIONS Independent Financial Adviser to the Independent Board Committee and the Independent Shareholders of Forte SOMERLEY LIMITED EQUITY INTEREST IN JV COMPANY Forte Investment, a subsidiary of Forte, and Zhejiang Fosun, a subsidiary of Fosun, entered into the Equity Transfer Agreement on 28 June 2010, whereby Zhejiang Fosun has agreed to acquire the Investment (comprising of a capital contribution in the amount of RMB300,000,000 (equivalent to approximately HK$343,697,729) and the Shareholder Loan in the amount of RMB1,300,000,000 (equivalent to approximately HK$1,489,356,827)) and take up all the rights and obligations of Forte Investment under the Joint Investment Agreement (including the Outstanding Financial Commitment) for a consideration of RMB1,600,000,000 (equivalent to approximately HK$1,833,054,556). As all of the applicable percentage ratios (as defined under Rule 14.04(9) of the Hong Kong Listing Rules) in relation to the Transfer are below 5%, the Transfer does not constitute a discloseable transaction of Fosun under Chapter 14 of the Hong Kong Listing Rules. -

International Cross-Listing Information for Chinese Firms

Appendix APPENDIX 1: INTERNATIONAL CROSS-LISTING INFORMATION FOR CHINESE FIRMS Table 1.1. Chinese firms listed on Hong Kong Stock Exchange Mainboard (Sources: Hong Kong Stock Exchange website, by December 31st, 2012) Company Listing Date Stock Code Industry Advanced Semiconductor April 7, 2006 3355 Semiconductors Manufacturing Corporation Ltd Agricultural Bank of China Ltd July 16, 2010 1288 Banks Air China Ltd December 15, 2004 753 Travel & Leisure Industrial Metals & Aluminum Corporation of China Ltd December 12, 2001 2600 Mining Industrial Metals & Angang Steel Co Ltd July 24, 1997 347 Mining Construction and Anhui Conch Cement Co Ltd October 21, 1997 914 Material Industrial Anhui Expressway Co Ltd November 13, 1996 995 Transportation Anhui Tianda Oil Pipe Co Ltd December 1, 2002 839 Industrial Supplier AviChina Industry & Technology October 30, 2003 2357 Industrial Engineering Co Ltd Bank of China Ltd June 1, 2006 3988 Banks Bank of Communications Co, Ltd June 23, 2005 3328 Banks Baoye Group Co Ltd June 30, 2003 2355 Industrial Construction BBMG Corporation July 29, 2009 2009 Industrial Metals Beijing Capital International Airport February 1, 2000 694 Travel and Leisure Co Ltd Real Estate Investment Beijing Capital Land Ltd June 19, 2003 2868 & Service Beijing Jingkelong Co Ltd February 26, 2008 814 Personal Goods Beijing Jingneng Clean Energy Co December 22, 2011 579 Electricity Ltd Beijing Media Corporation Ltd December 22, 2004 1000 Media Real Estate Investment Beijing North Star Co Ltd May 14, 1997 588 & Service Beiren Printing Machinery Holdings August 6, 1993 187 Industrial Engineering Ltd BYD Co Ltd July 31, 2002 1211 Industrial Products Software and Computer Capinfo Co Ltd December 21, 2001 1075 Services continued on following page 242 Appendix Table 1.1.