Market Summary and Patent Landscape Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Improving the Performance of Solar Thermal Power

The Oil Drum: Australia/New Zealand | Improving the Performance of Solar Therhmtatpl :P/o/wanezr.theoildrum.com/node/6279 Improving the Performance of Solar Thermal Power Posted by Big Gav on March 12, 2010 - 1:23am in The Oil Drum: Australia/New Zealand Topic: Alternative energy Tags: bill gross, concentrating solar power, esolar, solar power, solar thermal power [list all tags] The US Department of Energy granted a US$1.37 billion loan guarantee to Brightsource Energy last week which could help clear the way for over 15 gigawatts of solar thermal power projects in California. Brightsource built a pilot plant in Israel to prove their technology and has tested it over the past 18 months. Their flagship Ivanpah project in California got a big boost when construction giant Bechtel agreed to build the plant. Solar thermal is a way of harnessing the largest source of energy available to us, so in this post I'll have a look at the upswing in interest in the use of this technology for electricity generation in recent years and look at some of the approaches being pursued to make it economically competitive with coal fired power generation. Photo credit: http://www.flickr.com/photos/jurvetson/ The US Department of Energy granted a US$1.37 billion loan guarantee to Brightsource Energy last week which could help clear the way for over 15 gigawatts of solar thermal power projects in California. Brightsource built a pilot plant in Israel to prove their technology and has tested it over the past 18 months. Their flagship Ivanpah project in California got a big boost when construction giant Bechtel agreed to build the plant. -

Town of Amherst Request for Proposals

TOWN OF AMHERST REQUEST FOR PROPOSALS FOR OLD LANDFILL REUSE PROPOSAL Presented by: In partnership with: Letter of Transmittal............................................................................................................... 5 Executive Summary ................................................................................................................ 8 1. Evaluation Criteria ............................................................................................................ 10 1.1. Proposal protects the existing landfill caps. ...............................................................................10 1.2. Proposal protects operation of landfill gas systems...................................................................10 1.3. Experience of team proposing project........................................................................................10 1.4. Risk to human, health and the environment..............................................................................11 1.5. Effect on the environment..........................................................................................................11 1.6. Project compatibility with neighboring properties.....................................................................12 1.7. Noise levels from use of site.......................................................................................................12 1.7. Best compensation to Town of Amherst ....................................................................................13 -

Solar Thermal Energy an Industry Report

Solar Thermal Energy an Industry Report . Solar Thermal Technology on an Industrial Scale The Sun is Our Source Our sun produces 400,000,000,000,000,000,000,000,000 watts of energy every second and the belief is that it will last for another 5 billion years. The United States An eSolar project in California. reached peak oil production in 1970, and there is no telling when global oil production will peak, but it is accepted that when it is gone the party is over. The sun, however, is the most reliable and abundant source of energy. This site will keep an updated log of new improvements to solar thermal and lists of projects currently planned or under construction. Please email us your comments at: [email protected] Abengoa’s PS10 project in Seville, Spain. Companies featured in this report: The Acciona Nevada Solar One plant. Solar Thermal Energy an Industry Report . Solar Thermal vs. Photovoltaic It is important to understand that solar thermal technology is not the same as solar panel, or photovoltaic, technology. Solar thermal electric energy generation concentrates the light from the sun to create heat, and that heat is used to run a heat engine, which turns a generator to make electricity. The working fluid that is heated by the concentrated sunlight can be a liquid or a gas. Different working fluids include water, oil, salts, air, nitrogen, helium, etc. Different engine types include steam engines, gas turbines, Stirling engines, etc. All of these engines can be quite efficient, often between 30% and 40%, and are capable of producing 10’s to 100’s of megawatts of power. -

Energysecurityovervi

energy.sandia.gov EERE Program Overview 26 March 2012 http://energy.sandia.gov Sandia National Laboratories is a multi-program laboratory managed and operated by Sandia Corporation, a wholly owned subsidiary of Lockheed Martin Corporation, for the U.S. Department of Energy’s National Nuclear Security Administration under contract DE-AC04-94AL85000. SAND 2012-3066 P. History of Sandia Energy Programs Energy crisis of the 1970s Combustion Research spawned the beginning of Facility (CRF) & significant energy work Cummins partner on their newest diesel DOE’s Tech engine Strategic Petroleum Transfer Reserve – geological Initiative was characterization of established by Sandia was born as a nuclear salt domes to host oil Congress in weapons engineering laboratory storage caverns 1991 with deep science and Advent Solar engineering competencies Energy Policy Joint BioEnergy Act of 2005 Institute 1950 1960 1970 1980 1990 2000 2007 2010 CRF opens to Vertical axis researchers wind turbine Power grid reliability study Consortium for Advanced NRC cask Simulation of Light Water Sunshine to Reactors (CASL) certification Petrol Pilot Test Our core NW studies & competencies core melt enabled us to take studies on additional large SunCatcher™ Climate study national security Solar Tower partnership with Large-scale pool fire uncertainties to tests of liquefied challenges opens Stirling Energy economies Systems natural gas (LNG) on water Distributed Energy Technology Laboratory (DETL) to integrate Combustion Research emerging energy technologies Computation -

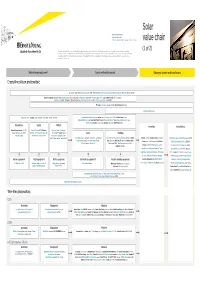

Lsoar Value Chain Value Chain

Solar Private companies in black Public companies in blue Followed by the founding date of companies less than 15 years old value chain (1 of 2) This value chain publication contains information gathered and summarized mainly from Lux Research and a variety of other public sources that we believe to be accurate at the time of ppggyublication. The information is for general guidance only and not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization nor Lux Research can accept responsibility for loss to any person relying on this publication. Materials and equipment Components and products Balance of system and installations Crystalline silicon photovoltaic GCL Silicon, China (2006); LDK Solar, China (2005); MEMC, US; Renewable Energy Corporation ASA, Norway; SolarWorld AG, Germany (1998) Bosch Solar Energy, Germany (2000); Canadian Solar, Canada/China (2001); Jinko Solar, China (2006); Kyocera, Japan; Sanyo, Japan; SCHOTT Solar, Germany (2002); Solarfun, China (2004); Tianwei New Energy Holdings Co., China; Trina Solar, China (1997); Yingli Green Energy, China (1998); BP Solar, US; Conergy, Germany (1998); Eging Photovoltaic, China SOLON, Germany (1997) Daqo Group, China; M. Setek, Japan; ReneSola, China (2003); Wacker, Germany Hyundai Heavy Industries,,; Korea; Isofoton,,p Spain ; JA Solar, China (();2005); LG Solar Power,,; Korea; Mitsubishi Electric, Japan; Moser Baer Photo Voltaic, India (2005); Motech, Taiwan; Samsung -

US Solar Industry Year in Review 2009

US Solar Industry Year in Review 2009 Thursday, April 15, 2010 575 7th Street NW Suite 400 Washington DC 20004 | www.seia.org Executive Summary U.S. Cumulative Solar Capacity Growth Despite the Great Recession of 2009, the U.S. solar energy 2,500 25,000 23,835 industry grew— both in new installations and 2,000 20,000 employment. Total U.S. solar electric capacity from 15,870 2,108 photovoltaic (PV) and concentrating solar power (CSP) 1,500 15,000 technologies climbed past 2,000 MW, enough to serve -th MW more than 350,000 homes. Total U.S. solar thermal 1,000 10,000 MW 1 capacity approached 24,000 MWth. Solar industry 494 revenues also surged despite the economy, climbing 500 5,000 36 percent in 2009. - - A doubling in size of the residential PV market and three new CSP plants helped lift the U.S. solar electric market 37 percent in annual installations over 2008 from 351 MW in 2008 to 481 MW in 2009. Solar water heating (SWH) Electricity Capacity (MW) Thermal Capacity (MW-Th) installations managed 10 percent year-over-year growth, while the solar pool heating (SPH) market suffered along Annual U.S. Solar Energy Capacity Growth with the broader construction industry, dropping 10 1,200 1,099 percent. 1,036 1,000 918 894 928 Another sign of continued optimism in solar energy: 865 -th 725 758 742 venture capitalists invested more in solar technologies than 800 542 any other clean technology in 2009. In total, $1.4 billion in 600 481 2 351 venture capital flowed to solar companies in 2009. -

New Energy Finance

new energy finance GLOBAL TRENDS IN SUS T AINABLE ENER G Y INVES T MEN T 2009 Analysis of Trends and Issues in the Financing of Renewable Energy and Energy Efficiency ROGRAMME P NVIRONMENT E Endorsed by ATIONS N NITED U Copyright © United Nations Environment Programme, 2009 This publication may be reproduced in whole or in part and in any form for educational or non-profit purposes without special permission from the copyright holder, provided acknowledgement of the source is made. UNEP would appreciate receiving a copy of any publication that uses this publication as a source. No use of this publication may be made for resale or for any other commercial purpose whatsoever without prior permission in writing from the United Nations Environment Programme. Disclaimer The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the United Nations Environment Programme concerning the legal status of any country, territory, city or area or of its authorities, or concerning delimitation of its frontiers or boundaries. Moreover, the views UNEP expressed do not necessarily represent the decision or the stated policy of the United Nations promotes environ- Environment Programme, nor does citing of trade mentally sound practices names or commercial processes constitute globally and in its own activities. endorsement. This publication is printed on 100% ISBN 978 92 807 3038 recycled paper, using vegetable -based DTI/1186/PA inks and other eco-friendly practices. -

Alternative Energy Options for Buildings: Distributed Generation— Power Generation at Or Near Buildings

chapter six Alternative Energy Options for Buildings: Distributed Generation— Power Generation At or Near Buildings Frederick R. Fucci With the Assistance of Clara Vondrich and Annette Nichols Introduction The purpose of this chapter is to discuss how sources of electric and thermal energy generation can be placed within or near buildings and thus serve as an alternative to the traditional model of delivering electricity to the customer—the central station model, where large power plants in relatively remote locations generate electricity from fossil fuels (and nuclear fuel and water), and the power they generate is transmitted long distances before being stepped down in voltage for use in local distribution systems. The alternative to this model, where electricity and thermal energy are generated at or near the site where the energy is used, is called distributed generation because the Alternative Energy Options for Buildings 125 generation resources are distributed around the grid. More fundamentally, every com- mercial and residential facility is potentially a small power plant. This is the real alter- native to the central generation model. With existing and readily available technology, every office building, apartment building, hotel, campus, hospital, and factory can generate enough electricity and thermal energy on-site to meet its own basic energy needs and export some to the grid. If configured correctly, these on-site systems can also keep the power on when the grid goes down and provide a much higher level of reliability, efficiency, and even quality than grid power. Distributed Resources Before getting into the considerations involved in actually generating power on-site, this chapter will discuss and consider as alternatives some less complicated measures that reduce the amount of electricity buildings and facilities use. -

Energy at the Crossroads

PREPARED BY The Oregon Center for Non-Partisan Policy Studies A Project of OESTRA: Oregon Energy Systems, Technology, and Research Alliance ENERGY AT THE CROSSROADS New energy economy trends toward a paradigm for renewable energy and associated technologies in coming decades OCTOBER 2012 1 TABLE OF CONTENTS PURPOSE OF THE STUDY 5 ENERGY USE, TECHNOLOGY AND ECONOMIC DEVELOPMENT 6 OVERVIEW 6 A SHORT HISTORY OF ELECTRICITY GENERATION 8 TRENDS IN FUEL SOURCES, USES, AND COSTS 10 FUEL CONSUMPTION 10 SECTOR USES FOR ENERGY 13 FUEL CONSUMPTION FOR ELECTRICITY GENERATION 13 ELECTRICITY SECTOR FUEL COSTS 15 POWER PLANT COSTS 17 CURRENT User COST COMPARISONS FOR FUEL 18 FUEL COST COMPARISON FOR ELECTRIC ENERGY 18 CURRENT ELECTRICITY COSTS BY STATE 19 A NEW PARADIGM FOR ENERGY 21 BACKGROUND 21 CLIMATE CHANGE 22 SCARCITY, NATIONAL SECURITY 23 FOSSIL FUEL CONCERNS 24 PRIVATE SECTOR BEHAVIOR 25 RECENT INVESTMENT TRENDS IN RENEWABLE ENERGY 26 MOMENTUM FOR RENEWABLE ENERGY 26 RECENT DEVELOPMENTS 26 CORPORATE INVESTMENT EXAMPLES 28 VENTURE CAPITAL 28 2 ENERGY AT THE CROSSROADS: RENEWABLE ENERGY SECTOR DIFFICULTIES 30 GOVERNMENT INCENTIVES 31 EMPLOYMENT AND ECONOMIC IMPACTS OF RENEWABLE ENERGY INVESTMENTS 34 JOB GROWTH 34 SKILLS SHORTAGES 34 TRAINING RECOMMENDATIONS 35 APPENDIX - STATUS AND OUTLOOK FOR TRADITIONAL AND EMERGING ENERGY SOURCES 39 OVERVIEW 39 HYBRID POWER GENERATION 39 OUTLOOK FOR ONSHORE WIND 40 OUTLOOK FOR OFFSHORE WIND 41 OUTLOOK FOR SOLAR/PV 41 OUTLOOK FOR CONCENTRATED SOLAR (CSP) 44 OUTLOOK FOR GEOTHERMAL 45 OUTLOOK FOR HYDRO 47 OUTLOOK -

F I L E D 04-23-13 04:20 PM I Have Provided Notification of Filing to the Electronic Mail Addresses on the Attached Service Lists

A.08-03-015 MF1/acr INFORMATION REGARDING SERVICE F I L E D 04-23-13 04:20 PM I have provided notification of filing to the electronic mail addresses on the attached service lists. Upon confirmation of this document’s acceptance for filing, I will cause a Notice of Availability of the filed document to be served upon the service list of Application 08-03-015 and to Rulemaking 08-08-009 by U.S. mail. The service list I will use to serve the Notice of Availability of the filed document is current as of today’s date. Dated April 23, 2012, at San Francisco, California. /s/ ANN CHRISTINA ROTHCHILD Ann Christina Rothchild NOTICE Parties should notify the Process Office, Public Utilities Commission, 505 Van Ness Avenue, Room 2000, San Francisco, CA 94102, of any change of address to ensure that they continue to receive documents. You must indicate the proceeding number on the service list on which your name appears. * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * * The Commission’s policy is to schedule hearings (meetings, workshops, etc.) in locations that are accessible to people with disabilities. To verify that a particular location is accessible, call: Calendar Clerk (415) 703-1203. If specialized accommodations for the disabled are needed, e.g., sign language interpreters, those making the arrangements must call the Public Advisor at (415) 703-2074 or TDD# (415) 703-2032 five working days in advance of the event. ************ SERVICE LIST *********** Last Updated on 22-APR-2013 by: JVG A0803015 LIST ************** PARTIES ************** Michael E. Boyd President Marc D. Joseph CALIFORNIANS FOR RENEWABLE ENERGY, INC. -

Where the Solar and Financial Communities Gather Each Year to Conduct Business Solar Company Solar Project

An Infocast Deal Working Event March 25-27, 2009 | Westin San Diego | San Diego, CA Platinum Sponsors: Where the Solar and Financial Communities Gather Each Year to Conduct Business Gold Sponsors: The Best Solar Deal-Making and Networking Event of the Year Back By Solar Company Popular Finance & Investment Summit Demand March 25, 2009 Innovative solar companies, venture capitalists, private equity, investment bankers, lenders and other financial players join forces to explore the opportunities for solar companies to fund their growth, research and development, and construction of projects. Participants will also explore such developments as going public and mergers and acquisitions. Solar Project Finance & Investment Summit Silver Sponsors: March 26-27, 2009 Leading utility scale and commercial/industrial/government project developers, investors, lenders, solar technology companies and other key industry players will gather to share their perspectives on how to successfully get deals done in 2009 and beyond. Produced by: www.infocastinc.com/solar09 Infocast Deal About the Summit Working Events The Solar Power Finance & Investment Summit has established itself as a major gathering place for the solar power industry’s decision makers—the Infocast Deal Working one deal-making venue where the solar power and financial communities Events facilitate deal- come together year after year to network and conduct business. Previous making by providing Summits have been an enormous success; active with major industry up-to-the-minute market and financial professionals networking and discussing deals. The 2009 Summit is slated for more of the same. This year’s Summit is presented in intelligence and valuable two parts: insight from leading players on conditions Solar Company in the current market. -

Concentrating Solar Power and Water Issues in the U.S. Southwest

Concentrating Solar Power and Water Issues in the U.S. Southwest Nathan Bracken Western States Water Council Jordan Macknick and Angelica Tovar-Hastings National Renewable Energy Laboratory Paul Komor University of Colorado-Boulder Margot Gerritsen and Shweta Mehta Stanford University The Joint Institute for Strategic Energy Analysis is operated by the Alliance for Sustainable Energy, LLC, on behalf of the U.S. Department of Energy’s National Renewable Energy Laboratory, the University of Colorado-Boulder, the Colorado School of Mines, the Colorado State University, the Massachusetts Institute of Technology, and Stanford University. Technical Report NREL/TP-6A50-61376 March 2015 Contract No. DE-AC36-08GO28308 Concentrating Solar Power and Water Issues in the U.S. Southwest Nathan Bracken Western States Water Council Jordan Macknick and Angelica Tovar-Hastings National Renewable Energy Laboratory Paul Komor University of Colorado-Boulder Margot Gerritsen and Shweta Mehta Stanford University Prepared under Task No. 6A50.1010 The Joint Institute for Strategic Energy Analysis is operated by the Alliance for Sustainable Energy, LLC, on behalf of the U.S. Department of Energy’s National Renewable Energy Laboratory, the University of Colorado-Boulder, the Colorado School of Mines, the Colorado State University, the Massachusetts Institute of Technology, and Stanford University. JISEA® and all JISEA-based marks are trademarks or registered trademarks of the Alliance for Sustainable Energy, LLC. The Joint Institute for Technical Report Strategic Energy Analysis NREL/TP-6A50-61376 15013 Denver West Parkway March 2015 Golden, CO 80401 303-275-3000 • www.jisea.org Contract No. DE-AC36-08GO28308 NOTICE This report was prepared as an account of work sponsored by an agency of the United States government.