New Energy Finance

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Improving the Performance of Solar Thermal Power

The Oil Drum: Australia/New Zealand | Improving the Performance of Solar Therhmtatpl :P/o/wanezr.theoildrum.com/node/6279 Improving the Performance of Solar Thermal Power Posted by Big Gav on March 12, 2010 - 1:23am in The Oil Drum: Australia/New Zealand Topic: Alternative energy Tags: bill gross, concentrating solar power, esolar, solar power, solar thermal power [list all tags] The US Department of Energy granted a US$1.37 billion loan guarantee to Brightsource Energy last week which could help clear the way for over 15 gigawatts of solar thermal power projects in California. Brightsource built a pilot plant in Israel to prove their technology and has tested it over the past 18 months. Their flagship Ivanpah project in California got a big boost when construction giant Bechtel agreed to build the plant. Solar thermal is a way of harnessing the largest source of energy available to us, so in this post I'll have a look at the upswing in interest in the use of this technology for electricity generation in recent years and look at some of the approaches being pursued to make it economically competitive with coal fired power generation. Photo credit: http://www.flickr.com/photos/jurvetson/ The US Department of Energy granted a US$1.37 billion loan guarantee to Brightsource Energy last week which could help clear the way for over 15 gigawatts of solar thermal power projects in California. Brightsource built a pilot plant in Israel to prove their technology and has tested it over the past 18 months. Their flagship Ivanpah project in California got a big boost when construction giant Bechtel agreed to build the plant. -

Town of Amherst Request for Proposals

TOWN OF AMHERST REQUEST FOR PROPOSALS FOR OLD LANDFILL REUSE PROPOSAL Presented by: In partnership with: Letter of Transmittal............................................................................................................... 5 Executive Summary ................................................................................................................ 8 1. Evaluation Criteria ............................................................................................................ 10 1.1. Proposal protects the existing landfill caps. ...............................................................................10 1.2. Proposal protects operation of landfill gas systems...................................................................10 1.3. Experience of team proposing project........................................................................................10 1.4. Risk to human, health and the environment..............................................................................11 1.5. Effect on the environment..........................................................................................................11 1.6. Project compatibility with neighboring properties.....................................................................12 1.7. Noise levels from use of site.......................................................................................................12 1.7. Best compensation to Town of Amherst ....................................................................................13 -

Solar Thermal Energy an Industry Report

Solar Thermal Energy an Industry Report . Solar Thermal Technology on an Industrial Scale The Sun is Our Source Our sun produces 400,000,000,000,000,000,000,000,000 watts of energy every second and the belief is that it will last for another 5 billion years. The United States An eSolar project in California. reached peak oil production in 1970, and there is no telling when global oil production will peak, but it is accepted that when it is gone the party is over. The sun, however, is the most reliable and abundant source of energy. This site will keep an updated log of new improvements to solar thermal and lists of projects currently planned or under construction. Please email us your comments at: [email protected] Abengoa’s PS10 project in Seville, Spain. Companies featured in this report: The Acciona Nevada Solar One plant. Solar Thermal Energy an Industry Report . Solar Thermal vs. Photovoltaic It is important to understand that solar thermal technology is not the same as solar panel, or photovoltaic, technology. Solar thermal electric energy generation concentrates the light from the sun to create heat, and that heat is used to run a heat engine, which turns a generator to make electricity. The working fluid that is heated by the concentrated sunlight can be a liquid or a gas. Different working fluids include water, oil, salts, air, nitrogen, helium, etc. Different engine types include steam engines, gas turbines, Stirling engines, etc. All of these engines can be quite efficient, often between 30% and 40%, and are capable of producing 10’s to 100’s of megawatts of power. -

Water Scenarios Modelling for Renewable Energy Development in Southern Morocco

ISSN 1848-9257 Journal of Sustainable Development Journal of Sustainable Development of Energy, Water of Energy, Water and Environment Systems and Environment Systems http://www.sdewes.org/jsdewes http://www.s!ewes or"/js!ewes Year 2021, Volume 9, Issue 1, 1080335 Water Scenarios Modelling for Renewable Energy Development in Southern Morocco Sibel R. Ersoy*1, Julia Terrapon-Pfaff 2, Lars Ribbe3, Ahmed Alami Merrouni4 1Division Future Energy and Industry Systems, Wuppertal Institute for Climate, Environment and Energy, Döppersberg 19, 42103 Wuppertal, Germany e-mail: [email protected] 2Division Future Energy and Industry Systems, Wuppertal Institute for Climate, Environment and Energy, Döppersberg 19, 42103 Wuppertal, Germany e-mail: [email protected] 3Institute for Technology and Resources Management, Technical University of Cologne, Betzdorferstraße 2, 50679 Köln, Germany e-mail: [email protected] 4Materials Science, New Energies & Applications Research Group, Department of Physics, University Mohammed First, Mohammed V Avenue, P.O. Box 524, 6000 Oujda, Morocco Institut de Recherche en Energie Solaire et Energies Nouvelles – IRESEN, Green Energy Park, Km 2 Route Régionale R206, Benguerir, Morocco e-mail: [email protected] Cite as: Ersoy, S. R., Terrapon-Pfaff, J., Ribbe, L., Alami Merrouni, A., Water Scenarios Modelling for Renewable Energy Development in Southern Morocco, J. sustain. dev. energy water environ. syst., 9(1), 1080335, 2021, DOI: https://doi.org/10.13044/j.sdewes.d8.0335 ABSTRACT Water and energy are two pivotal areas for future sustainable development, with complex linkages existing between the two sectors. These linkages require special attention in the context of the energy transition. -

PDF-Download

Michaël Tanchum FOKUS | 8/2020 Morocco‘s Africa-to-Europe Commercial Corridor: Gatekeeper of an emerging trans-regional strategic architecture Morocco’s West-Africa-to-Western-Europe framework of this emerging trans-regional emerging West-Africa-to-Western-Europe commercial transportation corridor is commercial architecture for years to come. commercial corridor. The November 15, redefining the geopolitical parameters of 2018 inauguration of the first segment of the global scramble for Africa and, with Morocco’s Construction of an Africa-to- the landmark high-speed line was presi- it, the strategic architecture of the Medi- Europe Corridor ded over by King Mohammed VI himself, in terranean basin. By massively expanding conjunction with French President Emma- the port capacity on its Mediterranean Situated in the northwest corner of Africa, nuel Macron.2 Seven years in construction, coast, Morocco has surpassed Spain and is fronting the Atlantic Ocean on its western the $2.3 billion line was built as a joint poised to become the dominant maritime coast and the Mediterranean Sea on its venture between France’s national railway hub in the western Mediterranean. Having northern coast, the Kingdom of Morocco company Société Nationale des Chemins constructed Africa’s first high-speed rail line, historically has been a geographical pivot de Fer Français (SNCF) and its Moroccan Morocco’s extension of the line to the Mau- for interchange between Europe, Africa, state counterpart Office National des Che- ritanian border, will transform Morocco into and the Middle East. In recent years, the mins de Fer (ONCF). Outfitted with Avelia the preeminent connectivity node in the semi-constitutional monarchy has adroitly Euroduplex high-speed trains produced nexus of commercial routes that connect combined the soft power resources of by French manufacturer Alstom, the initial West Africa to Europe and the Middle East. -

Energysecurityovervi

energy.sandia.gov EERE Program Overview 26 March 2012 http://energy.sandia.gov Sandia National Laboratories is a multi-program laboratory managed and operated by Sandia Corporation, a wholly owned subsidiary of Lockheed Martin Corporation, for the U.S. Department of Energy’s National Nuclear Security Administration under contract DE-AC04-94AL85000. SAND 2012-3066 P. History of Sandia Energy Programs Energy crisis of the 1970s Combustion Research spawned the beginning of Facility (CRF) & significant energy work Cummins partner on their newest diesel DOE’s Tech engine Strategic Petroleum Transfer Reserve – geological Initiative was characterization of established by Sandia was born as a nuclear salt domes to host oil Congress in weapons engineering laboratory storage caverns 1991 with deep science and Advent Solar engineering competencies Energy Policy Joint BioEnergy Act of 2005 Institute 1950 1960 1970 1980 1990 2000 2007 2010 CRF opens to Vertical axis researchers wind turbine Power grid reliability study Consortium for Advanced NRC cask Simulation of Light Water Sunshine to Reactors (CASL) certification Petrol Pilot Test Our core NW studies & competencies core melt enabled us to take studies on additional large SunCatcher™ Climate study national security Solar Tower partnership with Large-scale pool fire uncertainties to tests of liquefied challenges opens Stirling Energy economies Systems natural gas (LNG) on water Distributed Energy Technology Laboratory (DETL) to integrate Combustion Research emerging energy technologies Computation -

How to Create Efficient, Reliable and Clean Electricity Markets: a Regulatory Design for Mongolia and Northeast Asia

MASTER’S THESIS HOW TO CREATE EFFICIENT, RELIABLE AND CLEAN ELECTRICITY MARKETS: A REGULATORY DESIGN FOR MONGOLIA AND NORTHEAST ASIA Working title: Beyond Mining: Barriers to Renewable Energy Investments in Mongolia Paul Maidowski International Relations (B.A.) University of Dresden, 2010 Thesis Advisor: Professor William Moomaw SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE: MASTER OF ARTS IN LAW AND DIPLOMACY THE FLETCHER SCHOOL OF LAW AND DIPLOMACY SEPTEMBER 13, 2012 Version history V 1. Original: September 13, 2012 V 2. Updated: December 7, 2012 V 2.1. Slightly edited: December 8, 2012 Abstract This paper develops a comprehensive proposal for how Mongolia’s domestic power sector could be made more efficient, reliable and sustainable. The analysis is based on inter- views in Ulaanbaatar. It reviews the literature on power sector reforms in small developing countries and regional electricity markets. In a second step, a framework is proposed for a re- gional electricity market between Mongolia, Russia and China. In principle, this framework is applicable also to South Korea and Japan. The findings include that inadequate regulation has contributed to performance prob- lems in every aspect of Mongolia’s power sector, which remains a horizontally integrated monopoly. A lack of generation capacity was ignored for decades; as a result, supply is ex- pected to fall critically short of demand for the coming 3 to 5 years. Mongolia possesses rich coal resources, but water scarcity, harmful emissions, high vulnerability to the effects of cli- mate change, social constraints and the need for economic diversification will limit the future role of conventional technologies. -

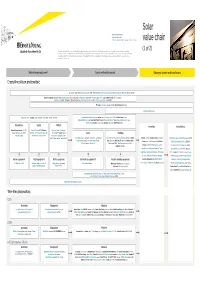

Lsoar Value Chain Value Chain

Solar Private companies in black Public companies in blue Followed by the founding date of companies less than 15 years old value chain (1 of 2) This value chain publication contains information gathered and summarized mainly from Lux Research and a variety of other public sources that we believe to be accurate at the time of ppggyublication. The information is for general guidance only and not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization nor Lux Research can accept responsibility for loss to any person relying on this publication. Materials and equipment Components and products Balance of system and installations Crystalline silicon photovoltaic GCL Silicon, China (2006); LDK Solar, China (2005); MEMC, US; Renewable Energy Corporation ASA, Norway; SolarWorld AG, Germany (1998) Bosch Solar Energy, Germany (2000); Canadian Solar, Canada/China (2001); Jinko Solar, China (2006); Kyocera, Japan; Sanyo, Japan; SCHOTT Solar, Germany (2002); Solarfun, China (2004); Tianwei New Energy Holdings Co., China; Trina Solar, China (1997); Yingli Green Energy, China (1998); BP Solar, US; Conergy, Germany (1998); Eging Photovoltaic, China SOLON, Germany (1997) Daqo Group, China; M. Setek, Japan; ReneSola, China (2003); Wacker, Germany Hyundai Heavy Industries,,; Korea; Isofoton,,p Spain ; JA Solar, China (();2005); LG Solar Power,,; Korea; Mitsubishi Electric, Japan; Moser Baer Photo Voltaic, India (2005); Motech, Taiwan; Samsung -

US Solar Industry Year in Review 2009

US Solar Industry Year in Review 2009 Thursday, April 15, 2010 575 7th Street NW Suite 400 Washington DC 20004 | www.seia.org Executive Summary U.S. Cumulative Solar Capacity Growth Despite the Great Recession of 2009, the U.S. solar energy 2,500 25,000 23,835 industry grew— both in new installations and 2,000 20,000 employment. Total U.S. solar electric capacity from 15,870 2,108 photovoltaic (PV) and concentrating solar power (CSP) 1,500 15,000 technologies climbed past 2,000 MW, enough to serve -th MW more than 350,000 homes. Total U.S. solar thermal 1,000 10,000 MW 1 capacity approached 24,000 MWth. Solar industry 494 revenues also surged despite the economy, climbing 500 5,000 36 percent in 2009. - - A doubling in size of the residential PV market and three new CSP plants helped lift the U.S. solar electric market 37 percent in annual installations over 2008 from 351 MW in 2008 to 481 MW in 2009. Solar water heating (SWH) Electricity Capacity (MW) Thermal Capacity (MW-Th) installations managed 10 percent year-over-year growth, while the solar pool heating (SPH) market suffered along Annual U.S. Solar Energy Capacity Growth with the broader construction industry, dropping 10 1,200 1,099 percent. 1,036 1,000 918 894 928 Another sign of continued optimism in solar energy: 865 -th 725 758 742 venture capitalists invested more in solar technologies than 800 542 any other clean technology in 2009. In total, $1.4 billion in 600 481 2 351 venture capital flowed to solar companies in 2009. -

Alternative Energy Options for Buildings: Distributed Generation— Power Generation at Or Near Buildings

chapter six Alternative Energy Options for Buildings: Distributed Generation— Power Generation At or Near Buildings Frederick R. Fucci With the Assistance of Clara Vondrich and Annette Nichols Introduction The purpose of this chapter is to discuss how sources of electric and thermal energy generation can be placed within or near buildings and thus serve as an alternative to the traditional model of delivering electricity to the customer—the central station model, where large power plants in relatively remote locations generate electricity from fossil fuels (and nuclear fuel and water), and the power they generate is transmitted long distances before being stepped down in voltage for use in local distribution systems. The alternative to this model, where electricity and thermal energy are generated at or near the site where the energy is used, is called distributed generation because the Alternative Energy Options for Buildings 125 generation resources are distributed around the grid. More fundamentally, every com- mercial and residential facility is potentially a small power plant. This is the real alter- native to the central generation model. With existing and readily available technology, every office building, apartment building, hotel, campus, hospital, and factory can generate enough electricity and thermal energy on-site to meet its own basic energy needs and export some to the grid. If configured correctly, these on-site systems can also keep the power on when the grid goes down and provide a much higher level of reliability, efficiency, and even quality than grid power. Distributed Resources Before getting into the considerations involved in actually generating power on-site, this chapter will discuss and consider as alternatives some less complicated measures that reduce the amount of electricity buildings and facilities use. -

Planning for the Energy Transition: Solar Photovoltaics in Arizona By

Planning for the Energy Transition: Solar Photovoltaics in Arizona by Debaleena Majumdar A Dissertation Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy Approved November 2018 by the Graduate Supervisory Committee: Martin J. Pasqualetti, Chair David Pijawka Randall Cerveny Meagan Ehlenz ARIZONA STATE UNIVERSITY December 2018 ABSTRACT Arizona’s population has been increasing quickly in recent decades and is expected to rise an additional 40%-80% by 2050. In response, the total annual energy demand would increase by an additional 30-60 TWh (terawatt-hours). Development of solar photovoltaic (PV) can sustainably contribute to meet this growing energy demand. This dissertation focuses on solar PV development at three different spatial planning levels: the state level (state of Arizona); the metropolitan level (Phoenix Metropolitan Statistical Area); and the city level. At the State level, this thesis answers how much suitable land is available for utility-scale PV development and how future land cover changes may affect the availability of this land. Less than two percent of Arizona's land is considered Excellent for PV development, most of which is private or state trust land. If this suitable land is not set-aside, Arizona would then have to depend on less suitable lands, look for multi-purpose land use options and distributed PV deployments to meet its future energy need. At the Metropolitan Level, ‘agrivoltaic’ system development is proposed within Phoenix Metropolitan Statistical Area. The study finds that private agricultural lands in the APS (Arizona Public Service) service territory can generate 3.4 times the current total energy requirements of the MSA. -

DIRTY ENERGY in AFRICA November 2016 Introduction

DIRTY ENERGY IN AFRICA November 2016 Introduction Dirty energy not only fuels dangerous climate change but also to afford the cost of unsubsidised electricity are left to struggle causes immense harm to people, communities, workers and the on, cooking indoors with coal or biomass year in, year out, while environment, all around the world. Dirty and harmful energy lies their health degenerates. This is part of an on-going colonial and at the heart of a broken energy system that is unjust and post-colonial pattern of natural resource exports leaving Africa’s unsustainable and destroying people and the planet. ports for richer northern countries and other wealthy elites including in southern countries. Friends of the Earth International takes a holistic approach to fighting dirty energy—we include coal, oil, gas, nuclear power, In the longer term Africa is currently on a lose-lose dirty energy industrial agrofuels and biomass, mega hydroelectric dams, and trajectory. waste-to-energy incineration in our definition of dirty energy. These destructive energy sources and technologies are driving Ambitions to keep average global temperature increase below climate change and have a deplorable track record, ranging from 1.5 oC compared to pre-industrial levels mean that carbon air and water pollution causing serious health impacts, through reductions must be very steep indeed. Developed countries must to massive land grabbing for new dirty energy mines, plants and act first and cut the most drastically, and they must contribute infrastructure. their fair share of the climate debt to ensure that Africa can shift towards sustainable socially-controlled renewable energy.