Turkish Outbound M&A Review 2014-2015

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Günlük Bülten 12 Ağustos 2021 Piyasalarda Son Görünüm* USD/TL EUR/TRY EUR/USD BIST-100 Gram Altın Gösterge Tahvil 8,6314 10,1510 1,1744 1.411 485,9 18,27

Günlük Bülten 12 Ağustos 2021 Piyasalarda Son Görünüm* USD/TL EUR/TRY EUR/USD BIST-100 Gram Altın Gösterge Tahvil 8,6314 10,1510 1,1744 1.411 485,9 18,27 Yurt içinde bugün TCMB faiz kararı takip edilecek Haftalık Getiriler (%) 1,5 1,2 ● TCMB’nin politika faizini sabit tutması bekleniyor 1,0 0,7 0,4 ● ABD’de yıllık enflasyon, %5,4 düzeyinde yatay seyretti 0,5 ● ABD Senatosu, 3,5 trilyon $’lık harcama paketini onayladı 0,0 -0,5 Küresel çapta, ABD'de tüketici fiyatları temmuz ayında aylık bazda -1,0 %0,5 artış gösterdi. Haziran ayında aylık enflasyon %0,9 -1,5 -1,5 düzeyinde gerçekleşmiş idi. Bu temmuz ayı gerçekleşmesi ile, yıllık -2,0 -1,7 enflasyon da %5,4 düzeyinde yatay seyretti. Yıllık çekirdek enflasyon Dolar/TL Euro/TL Gram Altın BIST-100 Gösterge Tahvil ise, %4,5'ten %4,3'e geriledi. ABD‘de özellikle enflasyon ve işgücü piyasasına yönelik veriler, Fed'in varlık alımlarında azaltıma Veriler (Bugün) Önceki Beklenti başlayabileceği tarih açısından kritik öneme sahip. TCMB Faiz Kararı (%) 19,0 19,0 Euro Bölgesi Sanayi Bölgesi ABD Senatosu, Başkan Biden'ın ekonomik reform takviminde -1,0 0,2 (Haziran, aylık % değişim, m.a.) bulunan 3,5 trilyon $ tutarındaki bütçe taslağına 50'ye karşı 49 oy ile onay verdi. Tasarının, ABD hükümetinin sosyal ve çevresel konulara yönelik daha fazla harcama yapmasına imkan tanıyacağı Yatırımcı Takvimi için tıklayınız belirtiliyor. Küresel çapta günlük vaka sayıları 7 günlük ortalamalar Devlet Tahvili Getirileri bazında artış eğilimini sürdürürken, ABD'de ve Avrupa'da, aşı (%) 11/08 10/08 2020 olmayanlara yönelik kısmi zorlayıcı tedbirler yürürlüğe giriyor. -

PRE-MARKET REPORT 8 June 2021

PRE-MARKET REPORT 8 June 2021 HEADLINES MARKET INDICATORS GCC CORPORATE NEWS, ANNOUNCEMENTS & DISCLOSURES • Creditors agree to restructure NMC Healthcare; DOCA plan urges lenders to bring down debt to USD 2.25bn from USD 7bn • FAB Properties partners with Emirates International Gas for gas supply • Air Arabia launches region's first service to Thailand's Phuket • MIS signs deal with Saudi Fransi Capital to set up fund to develop, operate data centres • Basic Chemical Industries Co. Announces an update on Commencement of work for Jubail project as well as a change in project costs from SAR 685mn to SAR 750mn • CMA approves Fitaihi’s request to cut capital to SAR 275mn • FIPCO renews SAR 73.7mn Islamic facility with Riyad Bank • Zahrat Al Waha Trading Company announces the repayment of a long-term loan from Alinma Bank • Barwa’s Dara in Lusail City offers additional apartments • CMA approves Kuwait Finance House USD 1bn Sukuk Issuance • ALBA shows resilience amid Covid, outlines 5-year strategic initiatives ECONOMIC, GENERAL & COMMODITIES NEWS • Mideast Stocks: Emaar lifts Dubai • China’s Alibaba to invest in cloud computing centre in Oman • Oman-India JV launches engineered quartz stone project in Sohar FZ • Total Fixed Internet Subscribers Rise 13.5 Percent till April 2021 • UAE central bank sets up 'whistleblowing' portal for misconduct, unethical practices • Saudi’s PIF, early Alibaba investor back Jordanian startup OpenSooq • CBK issues more debt instruments worth KWD 280m • Asia stocks open higher on record for MSCI's All-Country -

Investor Book (PDF)

INVESTOR BOOK EDITION OCTOBER 2016 Table of Contents Program 3 Venture Capital 10 Growth 94 Buyout 116 Debt 119 10 -11 November 2016 Old Billingsgate PROGRAM Strategic Partners Premium Partners MAIN STAGE - Day 1 10 November 2016 SESSION TITLE COMPANY TIME SPEAKER POSITION COMPANY Breakfast 08:00 - 10:00 CP 9:00 - 9:15 Dr. Klaus Hommels Founder & CEO Lakestar CP 9:15 - 9:30 Fabrice Grinda Co-Founder FJ Labs 9:35 - 9:50 Dr. Klaus Hommels Founder & CEO Lakestar Fabrice Grinda Co-Founder FJ Labs Panel Marco Rodzynek Founder & CEO NOAH Advisors 9:50 - 10:00 Chris Öhlund Group CEO Verivox 10:00 - 10:10 Hervé Hatt CEO Meilleurtaux CP Lead 10:10 - 10:20 Martin Coriat CEO Confused.com Generation 10:20 - 10:30 Andy Hancock Managing Director MoneySavingExpert K 10:30 - 10:45 Carsten Kengeter CEO Deutsche Börse Group 10:45 - 10:55 Carsten Kengeter CEO Deutsche Börse Group FC Marco Rodzynek Founder & CEO NOAH Advisors CP 10:55 - 11:10 Nick Williams Head of EMEA Global Market Solutions Credit Suisse 11:10 - 11:20 Talent 3.0: Science meets Arts CP Karim Jalbout Head of the European Digital Practice Egon Zehnder K 11:20 - 11:50 Surprise Guest of Honour 11:50 - 12:10 Yaron Valler General Partner Target Global Mike Lobanov General Partner Target Global Alexander Frolov General Partner Target Global Panel Shmuel Chafets General Partner Target Global Marco Rodzynek Founder & CEO NOAH Advisors 12:10 - 12:20 Mirko Caspar Managing Director Mister Spex 12:20 - 12:30 Philip Rooke CEO Spreadshirt CP 12:30 - 12:40 Dr. -

Deloitte Art and Finance Report 2014

Art & Finance Report 2014. 2 Art & Finance Report 2014 5 Art & Finance Report 2014 7 8 Table of contents Foreword 10 Deloitte US launches an Art & Finance practice 11 Introduction 12 Key findings 14 Priorities 20 Section 1: The art market 24 - Interview: Hala Khayat–An informed view from the Middle East 52 Section 2: Art and wealth management survey 54 - General motivation and perception among wealth managers, art professionals and collectors 60 - Interview: Georgina Hepbourne-Scott–The role of art management in a family office 68 - Interview: Paul Aitken–Recent developments at Borro® 76 - Interview: Harco Van Den Oever–Why using an art advisor 82 - Freeports for valuable tangible assets 86 - Article: Jean-Philippe Drescher–Freeport and art secured lending in Luxembourg 88 Section 3: Art as an investment 90 Section 4: The online art industry 100 - Q&A with investors: Dr. Christian G. Nagel–Earlybird Venture Capital & the art market 112 - Q&A with investors: Christian Leybold–e.ventures & the art market 114 Section 5: Legal Trends 119 - Interview: Steven Schindler–Most significant recent legal developments in the art world 120 - Article: Karen Sanig–Attribution and authenticity - the quagmire 124 - Article: Pierre Valentin–Art finance - can the borrower keep possession of the art collateral? 128 - Article: Catherine Cathiard–The evolution of French regulations on investments in art and collectors’ items 132 Art & Finance Report 2014 9 Foreword Deloitte Luxembourg and ArtTactic are pleased to present the 3rd edition of the Art & Finance Report. The two first editions of the Art & Finance Report (2011 and 2013) helped us to establish a forum and platform for monitoring emerging trends and attitudes around important issues related to the Art & Finance industry. -

En-Isbank2009.Pdf

Contents Presentation 1 İşbank at the onset of 2010 2 Turkey’s Bank 4 İşbank since 1924 5 İşbank’s Vision, Objectives, and Strategy 6 Pioneering Activities 7 İşbank’s Financial Indicators and Shareholder Structure 8 Chairman’s Message 12 CEO’s Message 18 İşbank’s transformation journey: Customer Centric Transformation (MOD) 20 The Economic Outlook in 2009 26 İşbank in 2009 49 Subsidiaries 54 Corporate Social Responsibility at İşbank 60 Annual Report Compliance Opinion Management and Corporate Governance at İşbank 62 Board of Directors & Auditors 64 Executive Committee 66 Organization Chart 68 Managers of Internal Systems 68 Information About the Meetings of the Board of Directors 69 İşbank Committees 71 Human Resources Functions at İşbank 72 Information on the Transactions Carried out with İşbank’s Risk Group 72 Activities for which Support Services are Received in Accordance with the Regulation on Procurement of Support Services for Banks and Authorization of Organizations Providing this Service 73 İşbank’s Dividend Distribution Policy 74 Agenda of the Annual General Meeting 75 Report of the Board of Directors 76 Auditors’ Report 77 Dividend Distribution Proposal 78 Corporate Governance Principles Compliance Report Financial Information and Assessment on Risk Management 89 Audit Committee’s Assessments on the Operation of Internal Control, Internal Audit and Risk Management Systems, and Their Activities in the Reported Period 91 Independent Auditors’ Report 92 Unconsolidated Financial Statements 102 Financial Highlights and Key Ratios -

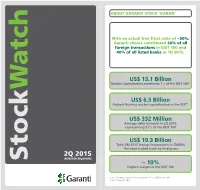

2Q 2015, Representing 21% of the BIST 100

ABOUT GARANTI STOCK ‘GARAN’ With an actual free float ratio of ~50%, Garanti shares constituted 20% of all foreign transactions in BIST 100 and 40% of all listed banks in 1H 2015. US$ 13.1 Billion Market Capitalization constitutes 7% of the BIST 100* Watch US$ 6.5 Billion Highest floating market capitalization in the BIST* US$ 332 Million Average daily turnover in 2Q 2015, representing 21% of the BIST 100 US$ 19.3 Billion Total 6M 2015 foreign transactions in GARAN The most traded stock by foreigners 2Q 2015 INVESTOR RELATIONS Stock ~ 10% Highest weight in the BIST 100 Note: Currency conversion is based on US$/TL CBRT ask rate. * As of June 30, 2015 GARANTI FINANCIAL HIGHLIGHTS Garanti Market Shares* Jun-15 QoQ ∆ In the first half of 2015, Garanti Total Performing Loans 11.8% reached consolidated total TL Loans 10.8% asset of US$ 99.9 billion and FC Loans 14.1% Credit Cards - Issuing (Cumulative) 19.1% consolidated net profit of Credit Cards - Acquiring (Cumulative) 20.4% US$ 777.7 million. Consumer Loans** 14.0% Total Customer Deposits 11.4% TL Customer Deposits 9.3% FC Customer Deposits 14.1% SELECTED FINANCIALS* Customer Demand Deposits 13.5% Mutual Funds 11.0% Total Assets Total Performing Loans * Figures are based on bank-only financials for fair comparison with sector. Sector US$ 99.9 Billion US$ 60.0 Billion figures are based on BRSA weekly data for commercial banks only. ** Including consumer credit cards and other Total Deposits Shareholders’ Equity Garanti with Numbers* US$ 54.7 Billion US$ 10.5 Billion Dec-14 Mar-15 Jun-15 -

Mergers and Acquisitions Report Turkey 2013

Mergers and Acquisitions Report Turkey 2013 January 2014 Foreword In 2013, many countries continued to be impacted by the global economic crisis and political and economic troubles still dominated agendas. Yet, Turkey, with its economy still growing, albeit to a lesser extent than in previous years, continued to distinguish itself as a successful, important and attractive country to invest in, not only in its region but in the world. In a year when global mergers and acquisitions volume slowed down, Turkey also experienced a slight decrease in transaction volume but reached a record high in terms of the number of deals. After such a year, we are delighted to share the twelfth “EY Mergers and Acquisitions Report”, a widely respected and much used reference material by all market players. The EY Mergers and Acquisitions Report 2013 is a thorough compilation of the facts and trends in mergers and acquisitions that were realized in Turkey in 2013, including comparisons with previous years. The Report also presents the results of our traditional “Mergers and Acquisitions in Turkey Survey” whose participants comprised shareholders and upper management of prominent public companies and private sector establishments in Turkey. We thank the survey participants for their contributions and support, as well as the EY Corporate Finance Team who prepared the EY Mergers and Acquisitions Report 2013. Mustafa Çamlıca Müşfik Cantekinler EY Turkey EY Turkey Country Leader Head of Corporate Finance Services 15 January 2014 Content General evaluation 5 Investor profile 8 Sectoral breakdown 12 Public sector deals 14 Transaction volumes 15 2014 overview 16 The overlook of the Turkish Business World towards the M&A Market 18 List of M&A transactions in 2013 25 Basis of preparation of the study 32 Mergers and Acquisitions Report Turkey 2013 General evaluation In a year when developed countries, many of them European, achieved limited growth, Turkey stood out by meeting growth expectations and exceeding the previous year’s growth rate. -

Istanbul Jewelry School Spreads to the World Behold the Jewels, from the Ancient Lands, Where Civilisations Flourished, Gifts Crafted by the Artisanship of Ages

YOUR COMPLIMENTARY COPY BRIEFING Turkey aims to export $190B in 2020 INDEPT Turkish Jewelry all over the Word INTERVIEW Deva CEO TheTurkish Philipp Haas PerspectiveFEBRUARY 2020 ISSUE 79 ECONOMY I BUSINESS I FOREIGN TRADE I ANALYSIS Istanbul Jewelry School Spreads to the World Behold the jewels, from the ancient lands, where civilisations flourished, gifts crafted by the artisanship of ages. It is the historical and cultural heritage that these rare accesories bear, that makes you feel special when you touch, put them on or wear them, rather than their monetary value. The Turkish Perspective TheTurkish Perspective Contents FEBRUARY 2020 ISSUE 79 Snow Globe of the World: 42Turkey Mckinsey: Artificial Intelligence The Power Symbol Turkey’s innovation ecosystem 14 to create 3.1 million jobs in 28 of Turkey: Jewelry 46 grows above the EU average Turkey 2019 exports reach to record Kamar: Our exports totaled 7.2 16 level of 180.5 billion dollars 30 billion dollars in 2019 THY awarded as Turkey’s A Master of Murassa: 20 top service exporter 35 Hrac Aslanyan Franchise sector to create an FDI Spotlight in Turkey Turkey’s Car Introduced 48 ecosystem of 50 billion dollars 22 38 in 2020 Foreign investors generated 64 Turkey eyes 120 billion USD Gastronomical reflection of 26 percent of Turkish M&A market 40 from tourism 54 Turkish Culture deal volume Mediterranean Cuisine FEBRUARY 2020 ISSUE 79 3 TheTurkish Perspective FEBRUARY 2020 ISSUE 79 THE TURKISH PERSPECTIVE RENEWED Management Publisher On Behalf Of Turkish Exporters Assembly Chairman Of The Turkish Exporters Assembly The Turkish Perspective continues publishing İsmail GÜLLE Strategic Partner with its renewed content in 2020. -

The Mineral Industry of Turkey in 2016

2016 Minerals Yearbook TURKEY [ADVANCE RELEASE] U.S. Department of the Interior January 2020 U.S. Geological Survey The Mineral Industry of Turkey By Sinan Hastorun Turkey’s mineral industry produced primarily metals and decreases for illite, 72%; refined copper (secondary) and nickel industrial minerals; mineral fuel production consisted mainly (mine production, Ni content), 50% each; bentonite, 44%; of coal and refined petroleum products. In 2016, Turkey was refined copper (primary), 36%; manganese (mine production, the world’s leading producer of boron, accounting for 74% Mn content), 35%; kaolin and nitrogen, 32% each; diatomite, of world production (excluding that of the United States), 29%; bituminous coal and crushed stone, 28% each; chromite pumice and pumicite (39%), and feldspar (23%). It was also the (mine production), 27%; dolomite, 18%; leonardite, 16%; salt, 2d-ranked producer of magnesium compounds (10% excluding 15%; gold (mine production, Au content), 14%; silica, 13%; and U.S. production), 3d-ranked producer of perlite (19%) and lead (mine production, Pb content) and talc, 12% each (table 1; bentonite (17%), 4th-ranked producer of chromite ore (9%), Maden İşleri Genel Müdürlüğü, 2018b). 5th-ranked producer of antimony (3%) and cement (2%), 7th-ranked producer of kaolin (5%), 8th-ranked producer of raw Structure of the Mineral Industry steel (2%), and 10th-ranked producer of barite (2%) (table 1; Turkey’s industrial minerals and metals production was World Steel Association, 2017, p. 9; Bennett, 2018; Bray, 2018; undertaken mainly by privately owned companies. The Crangle, 2018a, b; Fenton, 2018; Klochko, 2018; McRae, 2018; Government’s involvement in the mineral industry was Singerling, 2018; Tanner, 2018; van Oss, 2018; West, 2018). -

SW2 – Sample E-Commerce Site

SW2 – Sample E-Commerce Site 1. NAME/ LOGO 2. DESCRIPTION OLX is an Argentinian global online marketplace, operating in 45 countries, and is the largest online classified ads company in India, Brazil, Pakistan, Poland[1], Portugal and Ukraine . It was founded by Fabrice Grinda in 2006. Fabrice Grinda and Alec Oxenford founded the company as a Craigslist alternative for the world outside of the United States.[1] South African media group Naspers, acquired a majority of OLX in 2010 and 95% of the company in 2014. Mariel R. Ologar Page 1 of 4 November 21, 2017 PRODUCTS AND SERVICES : CATEGORIES OF OLX: B2C (BUSINESS-TO-CONSUMER) C2C (CONSUMER-TO-CONSUMER) Mariel R. Ologar Page 2 of 4 November 21, 2017 3. SWOT ANALYSIS STRENGHT 1. It is present in over 100+ countries, and thus have great learning curve. 2. It receives around 1.5 billion page views in a month, which gives a hint of its brand visibility in India. 3. Strong backing by Naspers which has experience in working with ecommerce giants 1.Funding of competitors 1. Diversification of its like Quickr by investors. portfolio to include various 2. Offline stores like Big SWOT other subcategories. Bazaar coming up with 2. Setting up of marketing campaigns to ANALYSIS offline/kiosks to increase its provided discounts on old brand awareness as well to goods. acquire new customers. THREATS OPPURTUNITIES 1. Lack of strong features to convert non-internet users as potential clients. 2. Intense competition means limited ROI considering huge investments in marketing WEAKNESSES Bibliography (n.d.). contributors, W. (2001). -

Speaker Book

SPEAKER BOOK Version as of 8 NOVEMBER 2016 Strategic Partners Premium Partners Table of Contents Program 4 Presenting Companies 7 Speakers 16 PROGRAM Porsche recommends and In the past no one understood what electricity could add to the guitar. The new Panamera 4 E-Hybrid. Imagine electriFying perFormance thanks to a race-proven hybrid concept. 700 Nm oF torque giving blistering acceleration while active all-wheel drive and e-boost Function inject more adrenaline into your everyday liFe. It’s time to plug yourself in: www.porsche.com/panamera Fuel consumption (in l/100 km) combined 2.5; CO2 emissions combined 56 g/km; electricity consumption (combined in kWh/100 km) 15.9 MAIN STAGE - Day 1 10 November 2016 SESSION TITLE COMPANY TIME SPEAKER POSITION COMPANY Breakfast 8:00 - 10:00 CP 9:00 - 9:15 Dr. Klaus Hommels Founder & CEO Lakestar CP 9:15 - 9:30 Fabrice Grinda Co-Founder FJ Labs 9:30 - 9:50 Dr. Klaus Hommels Founder & CEO Lakestar Fabrice Grinda Co-Founder FJ Labs Panel Marco Rodzynek Founder & CEO NOAH Advisors 9:50 - 10:00 Chris Öhlund Group CEO Verivox 10:00 - 10:10 Hervé Hatt CEO Meilleurtaux CP Lead 10:10 - 10:20 Martin Coriat CEO Confused.com 10:20 - 10:30 Andy Hancock Managing Director MoneySavingExpert Generation K 10:30 - 10:45 Carsten Kengeter CEO Deutsche Börse Group 10:45 - 10:55 Carsten Kengeter CEO Deutsche Börse Group FC Marco Rodzynek Founder & CEO NOAH Advisors CP 10:55 - 11:10 Nick Williams Head of EMEA ECM, Co-Head of CMSG Credit Suisse 11:10 - 11:20 Talent 3.0: Science meets Arts CP Karim Jalbout Head of the European -

Political Economy of Conflict: Evidence from Turkey

Markets, Conflict, and Incumbent Tenure: Evidence From Turkey's Kurdish Insurgency Emine Deniz ∗ February 3, 2020 ∗Harris School of Publicy Policy, The University of Chicago ([email protected]). I am grateful to Shanker Satyanath for his unwavering support throughout this project. I would like to thank Micha¨elAklin, Eric Arias, Antonella Bandiera, Kara Ross Camarena, Maria Carreri, Oeindrila Dube, Anna Getmansky, Michael Gilligan, Luis Martinez, Erzen Oncel,¨ Pablo Querebin, Cyrus Sami, Edoardo Teso, and Austin Wright for helpful discussions and insightful comments. The author thanks the discussants and seminar participants at the Workshop on the Political Economy of Turkey at LSE, Ozye˘ginUniversity,¨ Sabancı University and Bo˘gazi¸ciUniversity. Finally, Deniz Akku¸sand the analysts at the Kare Investment and Securities, Inc., were very generous with their time and resources providing the financial markets data. Alyssa Eldridge provided incredible editorial assistance.All errors belong to the author. Abstract Unexpected outbreaks of civil conflict may either strengthen or weaken the like- lihood of an incumbent remaining in office. In the absence of an actual turnover in office, or immediate public opinion surveys, scholars of conflict are at a loss to tell whether such episodes of conflict strengthen or weaken an incumbent's hold on power. In this paper, I address this question with a novel approach: studying the stock market performances of the firms inside and outside of the incumbent's network to infer the effect of an exogenous conflict episode on the incumbent's survival probability. I hypothesize that the abnormal returns of firms connected with the incumbent provide valuable information about the incumbent's hold on power: positive abnormal returns indicate stronger incumbent power, while neg- ative abnormal returns indicate weaker incumbent power.