Turkish OFDI Continues to Grow Report Dated March 24, 2014

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Turkey Market Scoping Report

IFC MOBILE MONEY SCOPING COUNTRY REPORT: TURKEY By Andrew Lake and Minakshi Ramji TURKEY SUMMARY- PAGE 1 OVERALL READINESS RANKING The Turkish financial sector is highly advanced. However, stakeholders appear less driven to promote access to financial services other than payment services. CURRENT MOBILE MONEY SOLUTION Currently all major banks and 2 of 3 biggest telecom providers offer mobile money solutions. POPULATION 80.17 million (2014) MOBILE PENETRATION 92.96% (high) (2013) BANKED POPULATION 57% through banks (2014) Mobile Money Readiness PERCENT UNDER POVERTY LINE 16.9% (2010) ECONOMICALLY ACTIVE POPULATION Workforce: 27.56 million (2014) Regulation 3 ADULT LITERACY 95%, age 15yrs+ can read and write (2014) Financial Sector 4 MOBILE NETWORK OPERATORS Turkcell, Vodafone, Avea Telecom Sector 3 MAIN BANKS Türkiye İş Bankası, Ziraat Bankası, Garanti Bank, Akbank, Yapı ve Kredi Bankası Distribution Channel 2 REGULATION Recent regulation on payments which Market Demand 3 clarifies which institutions may offer digital payments and which may issue e-money. Only banks may offer financial services such as deposits and loans. However, banks may not operate via agents other than the postal system. Sources: CIA World Fact book, ITU World Telecommunications statistics, World Bank Financial Inclusion Database TURKEY SUMMARY - PAGE 2 . OVERALL MOBILE MONEY IMPLEMENTATIONS Over three fourths of all transactions in banks currently happen over alternate delivery channels (ADCs) which includes ATMs, call center, internet, and mobile banking. Thus, banks view ADCs as being integral to their value proposition to clients. All leading banks offer mobile and internet banking services to clients. Till recently, 2 (Turkcell, Vodafone) of the three major MNOs offer mobile money solutions. -

Sayı 103 – Sermaye Piyasasında Gündem Mart 2011

sermaye piyasasında GüNDeM SAYI 103 MART 2011 ISSN 1304-8155 Endonezya Sermaye Piyasası (sayfa 7) Yabancı Piyasalarda Menkul Kıymet Kotasyonu ve Depo Sertifikaları (sayfa 16) TSPAKB TSPAKB Adına İmtiyaz Sahibi E. Nevzat Öztangut Başkan Genel Yayın Yönetmeni İlkay Arıkan Genel Sekreter Sorumlu Yazı İşleri Müdürü Alparslan Budak Genel Sekreter Yardımcısı Editör Ekin Fıkırkoca Müdür/Araştırma ve İstatistik Türkiye Sermaye Piyasası Aracı Kuruluşları Birliği Tasarım (TSPAKB), aracı kuruluşların üye olduğu, kamu Cennet Türker tüzel kişiliğini haiz özdüzenleyici bir meslek ku- Kıdemli Uzman/Eğitim ve Tanıtım ruluşudur. Efsun Ayça Değertekin Uzman/Araştırma ve İstatistik Birliğin 103 aracı kurum, 1 vadeli işlemler aracı- lık şirketi ve 41 banka olmak üzere toplam 145 Kapak Tasarımı ve Mizanpaj üyesi vardır. Cennet Türker Kıdemli Uzman/Eğitim ve Tanıtım Yayın Türü: Yaygın, süreli Sermaye piyasasında GüNDeM, TSPAKB’nin aylık iletişim organıdır. Para ile satılmaz. TSPAKB Büyükdere Caddesi No:173 1. Levent Plaza Kat:4 1. Levent 34394 İstanbul Tel:212-280 85 67 Faks:212-280 85 89 www.tspakb.org.tr [email protected] Basım Printcenter Bu rapora www.tspakb.org.tr adresinden ulaşabilirsiniz. Sermaye piyasasında GüNDeM, Türkiye Sermaye Piyasası Aracı Kuruluşları Birliği (TSPAKB) tarafından bilgilendirme ama- cıyla hazırlanmıştır. Bu raporda yer alan her türlü bilgi, değerlendirme, yorum ve istatistiki değerler, hazırlandığı tarih itibariyle güvenilirliğine inanılan kaynaklardan elde edilerek derlenmiştir. Bilgilerin hata ve eksikliğinden ve ticari amaçla kullanılmasından doğabilecek zararlardan TSPAKB hiçbir şekilde sorumluluk kabul etmemektedir. Raporda yer alan bilgi- ler kaynak gösterilmek şartıyla izinsiz yayınlanabilir. TSPAKB Sunuş KOBİ’lerin gelişmesi ve rekabet gücünün artması için alternatif fon kaynaklarına erişim, ekonomik kalkın- manın en önemli anahtarlarından birini oluşturuyor. -

Günlük Bülten 12 Ağustos 2021 Piyasalarda Son Görünüm* USD/TL EUR/TRY EUR/USD BIST-100 Gram Altın Gösterge Tahvil 8,6314 10,1510 1,1744 1.411 485,9 18,27

Günlük Bülten 12 Ağustos 2021 Piyasalarda Son Görünüm* USD/TL EUR/TRY EUR/USD BIST-100 Gram Altın Gösterge Tahvil 8,6314 10,1510 1,1744 1.411 485,9 18,27 Yurt içinde bugün TCMB faiz kararı takip edilecek Haftalık Getiriler (%) 1,5 1,2 ● TCMB’nin politika faizini sabit tutması bekleniyor 1,0 0,7 0,4 ● ABD’de yıllık enflasyon, %5,4 düzeyinde yatay seyretti 0,5 ● ABD Senatosu, 3,5 trilyon $’lık harcama paketini onayladı 0,0 -0,5 Küresel çapta, ABD'de tüketici fiyatları temmuz ayında aylık bazda -1,0 %0,5 artış gösterdi. Haziran ayında aylık enflasyon %0,9 -1,5 -1,5 düzeyinde gerçekleşmiş idi. Bu temmuz ayı gerçekleşmesi ile, yıllık -2,0 -1,7 enflasyon da %5,4 düzeyinde yatay seyretti. Yıllık çekirdek enflasyon Dolar/TL Euro/TL Gram Altın BIST-100 Gösterge Tahvil ise, %4,5'ten %4,3'e geriledi. ABD‘de özellikle enflasyon ve işgücü piyasasına yönelik veriler, Fed'in varlık alımlarında azaltıma Veriler (Bugün) Önceki Beklenti başlayabileceği tarih açısından kritik öneme sahip. TCMB Faiz Kararı (%) 19,0 19,0 Euro Bölgesi Sanayi Bölgesi ABD Senatosu, Başkan Biden'ın ekonomik reform takviminde -1,0 0,2 (Haziran, aylık % değişim, m.a.) bulunan 3,5 trilyon $ tutarındaki bütçe taslağına 50'ye karşı 49 oy ile onay verdi. Tasarının, ABD hükümetinin sosyal ve çevresel konulara yönelik daha fazla harcama yapmasına imkan tanıyacağı Yatırımcı Takvimi için tıklayınız belirtiliyor. Küresel çapta günlük vaka sayıları 7 günlük ortalamalar Devlet Tahvili Getirileri bazında artış eğilimini sürdürürken, ABD'de ve Avrupa'da, aşı (%) 11/08 10/08 2020 olmayanlara yönelik kısmi zorlayıcı tedbirler yürürlüğe giriyor. -

Assessment of Trade and Investment Potential Between Turkey and EU's

European Commission Assessment of trade and investment potential between Turkey and EU’s crsis- struck economies, the neighbouring Member States and Croatia Final Report Project No. 2013/318629 This project is funded by A project implemented by The European Commission HTSPE Limited Areas of expertise Monitoring and Evaluation Monitoring is a continuous process that is integrated into every stage of management within our large programmes such as those in Nigeria, Malawi, Nepal and Kenya. Monitoring is a key management tool that allows us as project managers to manage risk, evaluate achievements, build capacity, deliver lasting results, and maximise Value for Money. Evaluation is about using the data available to make judgements about a programme, its successes and identifying where changes are needed. We have undertaken many successful evaluations, including programmes in Pakistan, Bangladesh, Afghanistan, Nigeria and Liberia. Governance and Democracy Accountability, transparency and fair treatment of all stakeholders help to ensure the sustainability of change initiatives. We build and work with multi-disciplinary teams from the state, civil society, media and private sector agencies to develop integrated solutions to governance issues. We have wide geographical experience of governance and democracy programmes, including those in post-conflict and fragile states. We have worked in countries as varied as Afghanistan, Nigeria, Kyrgyzstan, Tanzania, South Africa, Guyana, Nepal, Moldova, Jamaica and Vietnam. Institutional Reform and Organisational Change These often go hand-in-hand with Governance. We help manage change at every step of the way; from initial policy analysis and public consultation, to building an agreed programme for reform, and then managing adjustments. -

En-Isbank2009.Pdf

Contents Presentation 1 İşbank at the onset of 2010 2 Turkey’s Bank 4 İşbank since 1924 5 İşbank’s Vision, Objectives, and Strategy 6 Pioneering Activities 7 İşbank’s Financial Indicators and Shareholder Structure 8 Chairman’s Message 12 CEO’s Message 18 İşbank’s transformation journey: Customer Centric Transformation (MOD) 20 The Economic Outlook in 2009 26 İşbank in 2009 49 Subsidiaries 54 Corporate Social Responsibility at İşbank 60 Annual Report Compliance Opinion Management and Corporate Governance at İşbank 62 Board of Directors & Auditors 64 Executive Committee 66 Organization Chart 68 Managers of Internal Systems 68 Information About the Meetings of the Board of Directors 69 İşbank Committees 71 Human Resources Functions at İşbank 72 Information on the Transactions Carried out with İşbank’s Risk Group 72 Activities for which Support Services are Received in Accordance with the Regulation on Procurement of Support Services for Banks and Authorization of Organizations Providing this Service 73 İşbank’s Dividend Distribution Policy 74 Agenda of the Annual General Meeting 75 Report of the Board of Directors 76 Auditors’ Report 77 Dividend Distribution Proposal 78 Corporate Governance Principles Compliance Report Financial Information and Assessment on Risk Management 89 Audit Committee’s Assessments on the Operation of Internal Control, Internal Audit and Risk Management Systems, and Their Activities in the Reported Period 91 Independent Auditors’ Report 92 Unconsolidated Financial Statements 102 Financial Highlights and Key Ratios -

Sami Can Besceli

Sami Can Besceli 24 Adelaide Rd, Leyton [email protected] E10 5NN, London, UK www.intg-strategies.com Phone: +44 7516 797009 Portfolio: https://bit.ly/2Uvt6vE Objective A position in the marketing, strategic planning and/or research department utilizing my experience and education. Work INTG.Strategies London, United Kingdom Experience Founder/Director 2019 - Present • Providing strategic consultancy services based on integrated advertising (conventional, digital, shopper), CX and app growth (mobile) to various stakeholders e.g. creative agencies, consultancy firms, start-ups, universities and so on in the UK and across the world. Self-Employed Istanbul, Turkey Freelance Strategist 2013 - 2017 • Provided strategic communication services across multi-, cross- and omni-channels for local or global creative, digital and media agencies based in Istanbul/Turkey as well as in different markets such as Dublin/Ireland, Warsaw/Poland, Dubai/United Arab Emirates. (Ask for references.) FCB Artgroup / FCB Red Istanbul, Turkey Senior Strategic Planner January 2016 - December 2016 • Responsible for the whole strategic planning process of both creative and shopper agency’s clients along with new business ventures. Brands: Nivea, Nivea Men, Faber-Castell, Adel, Adeland, Dyo, Feast, Mesa, Eyüp Sabri Tuncer, Demirören Holding, Milliyet, Total, Lenovo, Arçelik, Migros Cheil Worldwide Istanbul, Turkey Strategic Planner February 2015 - December 2015 • Worked on the strategic planning process of the main account Samsung and existing clients along with new business ventures. • Led Cheil WW Turkey’s strategic planning services and its positive development for the creative, retail and event teams. • Involved in global pitches and various projects (e.g. regional trend reports, competitive analyses) of Cheil WW network. -

Turkcell Annual Report 2010

TURKCELL ANNUAL REPORT 2010 GET MoRE oUT of LIfE WITh TURKCELL CoNTENTS PAGE our Vision / our Values / our Strategic Priorities 4 Turkcell Group in Numbers 6 Turkcell: Leading Communication and Technology Company 8 Letter from the Chairman 10 Board Members 12 Letter from the CEo 14 Executive officers 16 Superior Technologies 22 More Advantages 32 Best Quality Service 40 More Social Responsibility 46 Awards 53 Managers of Turkcell Affiliates 54 Subsidiaries 56 human Resources 62 Mobile Telecommunication Sector 66 International Ratings 72 Investor Relations 74 Corporate Governance 78 Turkcell offices 95 Consolidated financial Statement and Independent Audit Report 96 Dematerialization of The Share Certificates of The Companies That Are Traded on The Stock Exchange 204 The Board’s Dividend Distribution Proposal 205 2 3 oUR VISIoN oUR STRATEGIC PRIoRITIES To ease and enrich the lives of our customers with communication and As a Leading Communication and Technology Company, technology solutions. • to grow in our core mobile communication business through increased use of voice and data, • to grow our existing international subsidiaries with a focus on profitability, oUR VALUES • to grow in the fixed broadband business by creating synergy among Turkcell Group companies through our fiber optic infrastructure, • We believe that customers come first • to grow in the area of mobility, internet and convergence through new • We are an agile team business opportunities, • We promote open communication • to grow in domestic and international markets through communications, • We are passionate about making a difference technology and new business opportunities, • We value people • to develop new service platforms that will enrich our relationship with our customers through our technical capabilities. -

Market Watch Monday, March 01, 2021 Agenda

Market Watch Monday, March 01, 2021 www.sekeryatirim.com.tr Agenda 01 M onday 02 Tuesday 03 Wednesday 04 Thursday 05 Friday Turkstat, 4Q20 GDP Growth Germany, January TurkStat, February inflation CBRT, February Germany, Janu- retail sales inflation assess- ary factory orders China, February Caixin non-mfg. China, February Caixin mfg. PMI ment Germany, February PMI U.S., February Germany and Eurozone, Febru- unemployment data U.S., jobless non-farm payrolls ary Markit mfg. PMI Germany and Eurozone, Febru- ary Markit non-mfg. PMI claims and unemploy- Eurozone, February ment rate Germany, February CPI CPI Eurozone, February PPI U.S., January factory orders U.S., February U.S., February Markit mfg. PMI U.S., February ADP employment average hourly change earnings U.S., February ISM manufactur- ing index U.S., February Markit non-mfg. PMI U.S., January construction U.S., February ISM non- spending manufacturing index Outlook Major global stock markets closed lower on Friday, amid the rise in US Treasury yields, which has increased concerns over rising inflation and the Fed derailing its currently accommodative policy. Global risk appetite has Volume (mn TRY) BIST 100 relatively weakened, despite Fed Chair Powell’s statements suggesting that inflation was likely to remain below the targeted value, and that the 1.551 major central bank would maintain its current policy. Having moved in 1.518 1.488 parallel to the course of major international stock markets, the BIST100 48.000 1.483 1.471 1.600 also shed 1.13% to close at 1,471.39 on Friday, after a volatile day in 40.000 1.500 trading. -

Market Watch Tuesday, August 08, 2017 Agenda

Market Watch Tuesday, August 08, 2017 www.sekeryatirim.com.tr Agenda 07 Monday 08 Tuesday 09 Wednesday 10 Thursday 11 Friday Germany, June industrial TurkStat, June industrial U.S., June wholesale U.S., jobless claims CBRT, June balance of production production inventories U.S., July PPI payments U.S., July CPI Outlook: Major stock markets have advanced to new highs, and the BIST100 has Volume (mn TRY) BIST 100 also tested new record-highs, closing up 1.1% at 109,781 on Monday. Total trading volume in the market was at TRY 6.6bn. Today, market participants 109.781 will follow TurkStat’s June industrial production release; there are no other 10.000 110.000 108.545 major data announcements. Asian markets have seen mixed trading this 8.000 morning, and the European stock markets are expected to open slightly 107.154 108.000 106.525 down. We expect the BIST to maintain its uptrend in parallel to rising global 6.000 106.147 risk appetite, although we caution that the likelihood of profit taking rises 106.000 after swift upsurges. We expect the BIST to open positively today, refresh- 4.000 4.912 4.958 ing its new record highs. RESISTANCE: 110,000 /111,200 SUP- 5.418 104.000 4.667 2.000 4.667 PORT: 109,100/108,600. 0 102.000 1-Aug 2-Aug 3-Aug 4-Aug 7-Aug Money Market: The Lira was positive yesterday, gaining 0.14% against the USD to close at 3.5295. Additionally, the currency depreciated by 0.07% against the basket composed of $0.50 and €0.50. -

Premailer Middle East 2021

Bonds, Loans Shangri-La Bosphorus, Istanbul & Sukuk Turkey 2021 Turkey’s largest capital markets event www.bondsloansturkey.com 93% 50+ 20% 250+ DIRECTOR LEVEL OR ABOVE REGIONAL & INTERNATIONAL SOVEREIGN, CORPORATE & INDUSTRY EXPERT SPEAKERS BANKS ATTENDED FI BORROWERS Bonds, Loans & Sukuk Turkey has become the meeting point of all important players in finance through the correct mix of its participants, and its reliability with continuity of successful organisations in the last consecutive years Selahattin BİLGEN, IGA Airport PLATINUM SPONSOR GOLD SPONSOR BRONZE SPONSORS WELCOME TO THE ANNUAL MEETING PLACE FOR TURKEY’S FINANCE PROFESSIONALS Bonds, Loans & Sukuk Turkey is the country’s largest capital markets event. It is the only event to combine discussions across the Bond, Loans and Sukuk markets, making it a “must attend” event for the country’s leading CEOs, CFOs and Treasurers. With over 65% of the audience representing issuers and borrowers and over 93% being director level or above, it is the place where live deals are discussed and mandates are won each year. As a speaker, I had a dynamic discussion which was a great experience. Overall, the organisation was great and attracted an invaluable list of attendees. Orhan Kaya, ICBC Turkey SAVE YOURSELF SHOWCASE YOUR INCREASE TIME AND MONEY EXPERTISE IN THE REGION AWARENESS get the attendee list 2 weeks by presenting a case study by taking an exhibition space before the event so you can to a room full of potential and demonstrating your pre-arrange meetings. clients. products and services. WIN MORE INCREASE YOUR BUSINESS BRANDS PRESENCE packages include a number through the numerous of staff passes so you can branding opportunities cover more clients. -

2018/1 08/01/2018

SERMAYE PİYASASI KURULU BÜLTENİ 2018/1 08/01/2018 A. İZAHNAME / İHRAÇ BELGESİ ONAYLANAN SERMAYE PİYASASI ARAÇLARI 1. Borçlanma Araçları Nominal İhraççı Türü Satış Türü İhraç Tavanı Halka Arz/Tahsisli/Nitelikli Şeker Faktoring A.Ş. Tahvil/Finansman Bonosu 130.000.000 Yatırımcı Vakıf Faktoring A.Ş. Tahvil/Finansman Bonosu 400.000.000 Nitelikli yatırımcı Zorlu Enerji Elektrik Üretim A.Ş. Tahvil/Finansman Bonosu 300.000.000 Nitelikli Yatırımcı Tahvil/Finansman Bonosu/Sermaye 5.000.000.000 Türkiye Vakıflar Bankası T.A.O. Yurtdışı Benzeri Borçlanma Aracı ABD Doları 2. Diğer Sermaye Piyasası Araçları Kira Sertifikası ve VİDMK İhraçlarında Sermaye Piyasası Aracı Nominal İhraççı Satış Türü Türü İhraç Tavanı Kurucu Kaynak Kuruluş/Fon Kullanıcı Aktif Aktif Yatırım Bankası Turkcell Varlığa Dayalı Nitelikli Yatırım A.Ş. (3) No’lu Turkcell 100.000.000 Finansman Menkul Kıymet Yatırımcı Bankası Varlık Finansmanı Fonu A.Ş. A.Ş. B. YENİ FAALİYET İZİNLERİ 1. Vera TYT Gayrimenkul Portföy Yönetimi A.Ş.’nin faaliyet izni ile portföy yöneticiliği yetki belgesi verilmesi talebinin olumlu karşılanmasına karar verilmiştir. 2. KT Portföy Yönetimi A.Ş. KOBİ Girişim Sermayesi Yatırım Fonu’nun kuruluşuna izin verilmesi talebinin olumlu karşılanmasına karar verilmiştir. 3. A1 Capital Yatırım Menkul Değerler A.Ş.’nin yurt dışında paylar, diğer menkul kıymetler ve türev araçlar üzerinde işlem aracılığı faaliyeti yürütmek üzere yaptığı başvurunun olumlu karşılanmasına karar verilmiştir. NOT : Aksi belirtilmedikçe tüm parasal tutarlar TL cinsindendir. 1 ________________________________________________________________________________________________________________________________________________________________________ MERKEZ Eskişehir Yolu 8.Km No:156 06530 ANKARA Tel: (312) 292 90 90 Faks:(312) 292 90 00 www.spk.gov.tr İSTANBUL TEMSİLCİLİĞİ Harbiye Mah. Askerocağı Cad. No:15 34367 Şişli İSTANBUL Tel: (212) 334 55 00 Faks: (212) 334 56 00 C. -

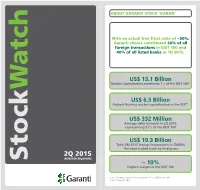

2Q 2015, Representing 21% of the BIST 100

ABOUT GARANTI STOCK ‘GARAN’ With an actual free float ratio of ~50%, Garanti shares constituted 20% of all foreign transactions in BIST 100 and 40% of all listed banks in 1H 2015. US$ 13.1 Billion Market Capitalization constitutes 7% of the BIST 100* Watch US$ 6.5 Billion Highest floating market capitalization in the BIST* US$ 332 Million Average daily turnover in 2Q 2015, representing 21% of the BIST 100 US$ 19.3 Billion Total 6M 2015 foreign transactions in GARAN The most traded stock by foreigners 2Q 2015 INVESTOR RELATIONS Stock ~ 10% Highest weight in the BIST 100 Note: Currency conversion is based on US$/TL CBRT ask rate. * As of June 30, 2015 GARANTI FINANCIAL HIGHLIGHTS Garanti Market Shares* Jun-15 QoQ ∆ In the first half of 2015, Garanti Total Performing Loans 11.8% reached consolidated total TL Loans 10.8% asset of US$ 99.9 billion and FC Loans 14.1% Credit Cards - Issuing (Cumulative) 19.1% consolidated net profit of Credit Cards - Acquiring (Cumulative) 20.4% US$ 777.7 million. Consumer Loans** 14.0% Total Customer Deposits 11.4% TL Customer Deposits 9.3% FC Customer Deposits 14.1% SELECTED FINANCIALS* Customer Demand Deposits 13.5% Mutual Funds 11.0% Total Assets Total Performing Loans * Figures are based on bank-only financials for fair comparison with sector. Sector US$ 99.9 Billion US$ 60.0 Billion figures are based on BRSA weekly data for commercial banks only. ** Including consumer credit cards and other Total Deposits Shareholders’ Equity Garanti with Numbers* US$ 54.7 Billion US$ 10.5 Billion Dec-14 Mar-15 Jun-15