Radio – Preparing for the Future Phase 1: Developing a New Framework

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

RAJAR Comparative Report Q3 2003

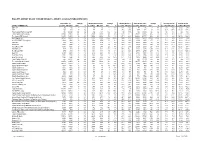

HALLETT ARENDT RAJAR TOPLINE RESULTS - WAVE 3 2003/LAST PUBLISHED DATA Population 15+ Change Weekly Reach 000's Change Weekly Reach % Total Hours 000's Change Average Hours Market Share LOCAL COMMERCIAL Last Pub W3 2003 000's % Last Pub W3 2003 000's % Last Pub W3 2003 Last Pub W3 2003 000's % Last Pub W3 2003 Last Pub W3 2003 Bath FM 82 82 0 0% 16 15 -1 -6% 19% 19% 88 95 7 8% 5.6 6.3 5.5% 5.8% 2BR 203 203 0 0% 77 78 1 1% 38% 38% 799 826 27 3% 10.3 10.6 18.3% 18.8% Total Capital Radio Group UK n/p 48384 n/a n/a n/p 7756 n/a n/a n/p 16% n/p 71888 n/a n/a n/p 9.3 n/p 6.8% Total Capital Radio Group 28097 28081 -16 0% 7600 7630 30 0% 27% 27% 70870 71265 395 1% 9.3 9.3 11.8% 11.9% The Capital FM Network 18951 18951 0 0% 5090 5016 -74 -1% 27% 26% 42282 41373 -909 -2% 8.3 8.2 10.3% 10.2% 95.8 Capital FM 10344 10343 -1 0% 2624 2269 -355 -14% 25% 22% 18991 15613 -3378 -18% 7.2 6.9 8.9% 7.0% 96.4 FM BRMB Birmingham 2004 2004 0 0% 588 555 -33 -6% 29% 28% 4339 4456 117 3% 7.4 8.0 9.8% 10.2% FOX FM 558 559 1 0% 208 214 6 3% 37% 38% 2289 2354 65 3% 11.0 11.0 19.2% 19.5% Invicta FM 1075 1075 0 0% 425 438 13 3% 39% 41% 4634 4984 350 8% 10.9 11.4 17.0% 18.3% 103.2 Power FM 1066 1066 0 0% 299 277 -22 -7% 28% 26% 2624 2326 -298 -11% 8.8 8.4 10.2% 9.7% Southern FM 949 949 0 0% 356 332 -24 -7% 38% 35% 4218 3679 -539 -13% 11.9 11.1 17.4% 16.3% Red Dragon FM 889 889 0 0% 301 311 10 3% 34% 35% 2789 2570 -219 -8% 9.3 8.3 13.3% 12.8% Beat 106 2599 2599 0 0% 415 447 32 8% 16% 17% 2976 3490 514 17% 7.2 7.8 5.8% 7.0% Beat 106 (East) 1101 1101 0 0% 199 198 -1 -1% 18% -

Local Commercial Radio Content

Local commercial radio content Qualitative Research Report Prepared for Ofcom by Kantar Media 1 Contents Contents ................................................................................................................................................. 2 1 Executive summary .................................................................................................................... 5 1.1 Background .............................................................................................................................. 5 1.2 Summary of key findings .......................................................................................................... 5 2 Background and objectives ..................................................................................................... 10 2.1 Background ............................................................................................................................ 10 2.2 Research objectives ............................................................................................................... 10 2.3 Research approach and sample ............................................................................................ 11 2.3.1 Overview ............................................................................................................................. 11 2.3.2 Workshop groups: approach and sample ........................................................................... 11 2.3.3 Research flow summary .................................................................................................... -

Fame Attack : the Inflation of Celebrity and Its Consequences

Rojek, Chris. "The Icarus Complex." Fame Attack: The Inflation of Celebrity and Its Consequences. London: Bloomsbury Academic, 2012. 142–160. Bloomsbury Collections. Web. 1 Oct. 2021. <http://dx.doi.org/10.5040/9781849661386.ch-009>. Downloaded from Bloomsbury Collections, www.bloomsburycollections.com, 1 October 2021, 16:03 UTC. Copyright © Chris Rojek 2012. You may share this work for non-commercial purposes only, provided you give attribution to the copyright holder and the publisher, and provide a link to the Creative Commons licence. 9 The Icarus Complex he myth of Icarus is the most powerful Ancient Greek parable of hubris. In a bid to escape exile in Crete, Icarus uses wings made from wax and feathers made by his father, the Athenian master craftsman Daedalus. But the sin of hubris causes him to pay no heed to his father’s warnings. He fl ies too close to the sun, so burning his wings, and falls into the Tsea and drowns. The parable is often used to highlight the perils of pride and the reckless, impulsive behaviour that it fosters. The frontier nature of celebrity culture perpetuates and enlarges narcissistic characteristics in stars and stargazers. Impulsive behaviour and recklessness are commonplace. They fi gure prominently in the entertainment pages and gossip columns of newspapers and magazines, prompting commentators to conjecture about the contagious effects of celebrity culture upon personal health and the social fabric. Do celebrities sometimes get too big for their boots and get involved in social and political issues that are beyond their competence? Can one posit an Icarus complex in some types of celebrity behaviour? This chapter addresses these questions by examining celanthropy and its discontents (notably Madonna’s controversial adoption of two Malawi children); celebrity health advice (Tom Cruise and Scientology); and celebrity pranks (the Sachsgate phone calls involving Russell Brand and Jonathan Ross). -

Ofcom Content Sanctions Committee

Ofcom Content Sanctions Committee Consideration of Channel TV Ltd (“Channel TV” or the “Licensee”), in sanction against respect of its service the Regional Channel 3 service (“Channel 3”) transmitted across the ITV Network on ITV1. For 1. Early finalising of the vote for the People’s Choice Award in the British Comedy Awards 2004, broadcast on 22 December 2004, Resulting in a breach of the ITC Programme Code 2002 (the “ITC Code”) in force from January 2002 until 24 July 2005 of: Rule 8.2(b) Use of Premium Rate Telephone Services in Programmes: “The licensee must retain control of and responsibility for the service arrangements and the premium line messages (including all matters relating to their content)” 2. Early finalising of the vote for the People’s Choice Award in the British Comedy Awards 2005, broadcast on 14 December 2005, Resulting in a breach of the Ofcom Broadcasting Code of: Rule 2.2: “Factual programmes or items or portrayals of factual matters must not materially mislead the audience” 3. Overriding the viewers’ vote for the People’s Choice Award and substituting a different winner in the British Comedy Awards 2005, broadcast on 14 December 2005 Resulting in a breach of the Code of: Rule 2.2: “Factual programmes or items or portrayals of factual matters must not materially mislead the audience” Decision To impose a financial penalty (payable to HM Paymaster General) of £80,000, which comprises £45,000 in respect of the early finalising of the vote in both programmes (“as live breaches”) and £35,000 in respect of overriding of viewers votes in the BCA 2005 (“the selection breach”). -

10 June 2011 Page 1 of 15

Radio 4 Listings for 4 – 10 June 2011 Page 1 of 15 SATURDAY 04 JUNE 2011 SAT 07:00 Today (b011msk2) Series 74 Morning news and current affairs with John Humphrys and SAT 00:00 Midnight News (b011jx96) Evan Davis. Episode 8 The latest national and international news from BBC Radio 4. 08:10 How effective are plans to curb provocative images seen Followed by Weather. by children? A satirical review of the week's news, chaired by Sandi 08:30 Lord Lamont and Alistair Darling on the economy. Toksvig. With Rory Bremner, Jeremy Hardy, Mark Steel and 08:44 The man who inspired the classic film The Battle of Fred Macaulay. SAT 00:30 Book of the Week (b011mt39) Algiers. Ox Travels 08:49 Does London need its new Playboy club? SAT 12:57 Weather (b011jx9v) The Wrestler The latest weather forecast. SAT 09:00 Saturday Live (b011msk4) Ox Travels features original stories from twenty-five top travel Richard Coles with actor and director Richard Wilson, poet writers; this week we'll be featuring five of these stories. Susan Richardson, a woman who discovered her outwardly SAT 13:00 News (b011jx9x) respectable father was in fact a criminal gangster, and a man The latest national and international news from BBC Radio 4. Each of the stories takes as its theme a meeting life-changing, who kept a lion as a pet. There's an I Was There feature from a affecting, amusing by turn and together they transport readers man who worked on the world's first international satellite TV into a brilliant, vivid atlas of encounters. -

Brits Choose Holiday Partners for Sun, Sand, And… a Laugh Submitted By: Pr-Sending-Enterprises Friday, 15 September 2006

Brits choose holiday partners for sun, sand, and… a laugh Submitted by: pr-sending-enterprises Friday, 15 September 2006 British holidaymakers would pick fun over glamour when it comes to holiday companions according to research by Barclays Insurance (http://www.barclays.co.uk/insurance). Northern comedian Peter Kay has topped the list of celebrities Brits would most like to go on holiday with, relegating homegrown starlet Keira Knightley and Hollywood heart throb George Clooney to second and third places. Elsewhere in the list, Kylie Minogue and Angelina Jolie are the only other non-Brits in a top ten dominated by British personalities. Whilst good looks and the fun factor clearly play an important part when choosing Britain’s favourite holiday companion it seems that most people remain loyal to their local heroes – Scots favoured Sean Connery whilst the North of England was the most supportive of Peter Kay. Unsurprisingly, good-looking and successful members of the opposite sex made up the top ideal holiday companions for both male and female respondents with the exception of all-round favourite Peter Kay who appeared second in the lists for both sexes. However it appears that a large number of male holidaymakers would prefer to take a fellow fella with them on their travels with a total of four males featuring in their top ten whilst the only woman that females would consider holidaying with is Davina McCall. Across the age groups, Big Brother presenter Dermot O’Leary was the most popular companion amongst the under 30s but over 50s would prefer to share a sunlounger with Joanna Lumley. -

X FACTOR JUDGE CHERYL COLE and KYLIE MINOGUE MOST POWERFUL CELEBRITIES in BRITAIN HIGHLIGHTS RESEARCH Submitted By: Eureka Communications Wednesday, 31 March 2010

X FACTOR JUDGE CHERYL COLE AND KYLIE MINOGUE MOST POWERFUL CELEBRITIES IN BRITAIN HIGHLIGHTS RESEARCH Submitted by: Eureka Communications Wednesday, 31 March 2010 31st March 2010, London, UK – Pop star Kylie Minogue and X-Factor judge Cheryl Cole were named the most powerful celebrities in Britain today in Millward Brown’s latest celebrity and brand (Cebra) research . The research, which interviewed 2000 consumers about 100 celebrities and 100 brands, will be used by marketers to identify celebrity and brand partnerships with the greatest marketplace potential. The 10 most powerful UK celebrities were: 1)Kylie Minogue 2)Cheryl Cole 3)David Beckham 4)Ant & Dec 5)Joanna Lumley 6)Terry Wogan 7)Jamie Oliver 8)George Clooney 9)Sean Connery 10)Helen Mirren “Kylie is widely accepted as an adopted Brit. People know her, like her and she is surrounded by positive buzz,” says Mark Husak, Head of Millward Brown’s UK Media Practice. Cheryl’s mix of exciting, endearing and engaging traits seems to be a winning combination.” Cheryl Cole is 2nd in the ranking and has the highest positive Buzz score (80 percent positive) despite the negative media coverage that has surrounded her in the past. Cheryl is seen as very Playful, Sympathetic and Outgoing but least Reserved, Calm and Laid Back. She is well matched to Coca Cola and New Look. Kylie’s personality matches well with L’Oreal, Yahoo, Cadbury and Lucozade. Research highlights: •US star George Clooney (8th in the ranking) is the only other non-Brit to appear in the Top10. Like Kylie, he is well liked with no negative publicity. -

Brand and the BBC – the Full Expletive-Riddled Truth

Brand and the BBC – the full expletive-riddled truth blogs.lse.ac.uk/polis/2008/11/05/brand-and-the-bbc-the-full-expletive-riddled-truth/ 2008-11-5 Was it a storm in a tea-cup or a symbol of a wider malaise at the BBC? Well Polis has got the full, expletive-riddled story from a senior BBC figure. Caroline Thomson is the BBC’s Chief Operating Officer, second only in importance at the corporation to her namesake, Mark. In a speech to Polis she gave a lengthy and carolinethomson.jpg candid narrative of the whole Brand/Ross prank phone call saga. In it she makes a staunch defence of the BBC’s actions and calls on the corporation to continue taking risk. But she recognised in her speech, and the subsequent exchange we had, that it does raise a wider question: Is the BBC too keen to do too much instead of focusing on what it does best. Here is her speech which I think is well worth reading in full – it will also go up on the main Polis website. The BBC: The Challenge to Appeal to All Audiences Caroline Thomson, Chief Operating Officer, BBC POLIS Media Leadership Dialogues London School of Economics, Tuesday 4 November What a week – when I agreed to do this talk I thought I would focus on transforming the BBC – getting it to be a networked organisation, representing the whole of the UK with London as its hub, not its dominant force, with our plans for our new base in the Manchester region as the central theme. -

P R O C E E D I N G S

T Y N W A L D C O U R T O F F I C I A L R E P O R T R E C O R T Y S O I K O I L Q U A I Y L T I N V A A L P R O C E E D I N G S D A A L T Y N HANSARD Douglas, Tuesday, 15th June 2021 All published Official Reports can be found on the Tynwald website: www.tynwald.org.im/business/hansard Supplementary material provided subsequent to a sitting is also published to the website as a Hansard Appendix. Reports, maps and other documents referred to in the course of debates may be consulted on application to the Tynwald Library or the Clerk of Tynwald’s Office. Volume 138, No. 24 ISSN 1742-2256 Published by the Office of the Clerk of Tynwald, Legislative Buildings, Finch Road, Douglas, Isle of Man, IM1 3PW. © High Court of Tynwald, 2021 TYNWALD COURT, TUESDAY, 15th JUNE 2021 Present: The President of Tynwald (Hon. S C Rodan OBE) In the Council: The Lord Bishop of Sodor and Man (The Rt Rev. P A Eagles), The Attorney General (Mr J L M Quinn QC), Mr P Greenhill, Mr R W Henderson, Mrs K A Lord-Brennan, Mrs M M Maska, Mr R J Mercer, Mrs J P Poole-Wilson and Mrs K Sharpe with Mr J D C King, Deputy Clerk of Tynwald. In the Keys: The Speaker (Hon. J P Watterson) (Rushen); The Chief Minister (Hon. -

United Kingdom Distribution Points

United Kingdom Distribution to national, regional and trade media, including national and regional newspapers, radio and television stations, through proprietary and news agency network of The Press Association (PA). In addition, the circuit features the following complimentary added-value services: . Posting to online services and portals with a complimentary ReleaseWatch report. Coverage on PR Newswire for Journalists, PR Newswire's media-only website and custom push email service reaching over 100,000 registered journalists from 140 countries and in 17 different languages. Distribution of listed company news to financial professionals around the world via Thomson Reuters, Bloomberg and proprietary networks. Releases are translated and distributed in English via PA. 3,298 Points Country Media Point Media Type United Adones Blogger Kingdom United Airlines Angel Blogger Kingdom United Alien Prequel News Blog Blogger Kingdom United Beauty & Fashion World Blogger Kingdom United BellaBacchante Blogger Kingdom United Blog Me Beautiful Blogger Kingdom United BrandFixion Blogger Kingdom United Car Design News Blogger Kingdom United Corp Websites Blogger Kingdom United Create MILK Blogger Kingdom United Diamond Lounge Blogger Kingdom United Drink Brands.com Blogger Kingdom United English News Blogger Kingdom United ExchangeWire.com Blogger Kingdom United Finacial Times Blogger Kingdom United gabrielleteare.com/blog Blogger Kingdom United girlsngadgets.com Blogger Kingdom United Gizable Blogger Kingdom United http://clashcityrocker.blogg.no Blogger -

The Bbc Trust Report: On-Screen and On-Air Talent Including an Independent Assessment and Report by Oliver & Ohlbaum Associates

THE BBC TRUST REPORT: ON-SCREEN AND ON-AIR TALENT INCLUDING AN INDEPENDENT ASSESSMENT AND REPORT BY OLIVER & OHLBAUM ASSOCIATES MAY 2008 2 BBC TRUST CONCLUSIONS The issue of talent costs The BBC Trust operates to protect the interests of licence fee payers who pay for and own the BBC. As part of this we seek to ensure quality and value for money for licence fee payers and to challenge BBC management to use everything at their disposal to deliver both. An area where this is particularly complex is the salaries paid to on-screen and on-air talent. During the course of 2006, press reports about presenters’ salaries aroused industry and public concern and led some people to question the BBC’s approach to the talent it employs. This debate was still live when the Trust was established as the BBC’s governing body in January 2007. It was and has remained a topic raised by the public with Trustees during our appearances on radio phone-ins and at public meetings in all parts of the UK. Against this background the Trust commissioned an independent review, conducted by Oliver and Ohlbaum Associates Ltd (O&O), to provide an in depth examination of the BBC’s use of on air and on screen talent. We posed O&O three specific questions: • How do the size and structure of the BBC's reward packages for talent compare with the rest of the market? • What has been the impact of the BBC's policy on the talent market, particularly in relation to cost inflation? • To what extent do the BBC's policy and processes in relation to investment in, and reward of, talent support value for money? We are publishing O&O’s report which seeks to answer these questions, the BBC management’s response to the points it raises and our own judgements informed by this evidence. -

The British Academy Television Awards Sponsored by Pioneer

The British Academy Television Awards sponsored by Pioneer NOMINATIONS ANNOUNCED 11 APRIL 2007 ACTOR Programme Channel Jim Broadbent Longford Channel 4 Andy Serkis Longford Channel 4 Michael Sheen Kenneth Williams: Fantabulosa! BBC4 John Simm Life On Mars BBC1 ACTRESS Programme Channel Anne-Marie Duff The Virgin Queen BBC1 Samantha Morton Longford Channel 4 Ruth Wilson Jane Eyre BBC1 Victoria Wood Housewife 49 ITV1 ENTERTAINMENT PERFORMANCE Programme Channel Ant & Dec Saturday Night Takeaway ITV1 Stephen Fry QI BBC2 Paul Merton Have I Got News For You BBC1 Jonathan Ross Friday Night With Jonathan Ross BBC1 COMEDY PERFORMANCE Programme Channel Dawn French The Vicar of Dibley BBC1 Ricky Gervais Extra’s BBC2 Stephen Merchant Extra’s BBC2 Liz Smith The Royle Family: Queen of Sheba BBC1 SINGLE DRAMA Housewife 49 Victoria Wood, Piers Wenger, Gavin Millar, David Threlfall ITV1/ITV Productions/10.12.06 Kenneth Williams: Fantabulosa! Andy de Emmony, Ben Evans, Martyn Hesford BBC4/BBC Drama/13.03.06 Longford Peter Morgan, Tom Hooper, Helen Flint, Andy Harries C4/A Granada Production for C4 in assoc. with HBO/26.10.06 Road To Guantanamo Michael Winterbottom, Mat Whitecross C4/Revolution Films/09.03.06 DRAMA SERIES Life on Mars Production Team BBC1/Kudos Film & Television/09.01.06 Shameless Production Team C4/Company Pictures/01.01.06 Sugar Rush Production Team C4/Shine Productions/06.07.06 The Street Jimmy McGovern, Sita Williams, David Blair, Ken Horn BBC1/Granada Television Ltd/13.04.06 DRAMA SERIAL Low Winter Sun Greg Brenman, Adrian Shergold,