HATS Regional Freight Plan Update Followed the Following Primary Tasks

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

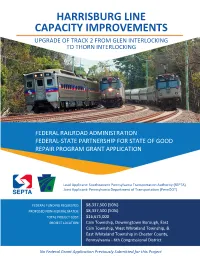

Harrisburg Line Capacity Improvements Upgrade of Track 2 from Glen Interlocking to Thorn Interlocking

HARRISBURG LINE CAPACITY IMPROVEMENTS UPGRADE OF TRACK 2 FROM GLEN INTERLOCKING TO THORN INTERLOCKING FEDERAL RAILROAD ADMINISTRATION FEDERAL-STATE PARTNERSHIP FOR STATE OF GOOD REPAIR PROGRAM GRANT APPLICATION Lead Applicant: Southeastern Pennsylvania Transportation Authority (SEPTA) Joint Applicant: Pennsylvania Department of Transportation (PennDOT) FEDERAL FUNDING REQUESTED: $8,337,500 (50%) PROPOSED NON-FEDERAL MATCH: $8,337,500 (50%) TOTAL PROJECT COST: $16,675,000 PROJECT LOCATION: Caln Township, Downingtown Borough, East Caln Township, West Whiteland Township, & East Whiteland Township in Chester County, Pennsylvania - 6th Congressional District No Federal Grant Application Previously Submitted for this Project Table of Contents I. Project Summary .................................................................................................................................. 1 II. Project Funding ..................................................................................................................................... 2 III. Applicant Eligibility ............................................................................................................................... 3 IV. NEC Project Eligibility ........................................................................................................................... 3 V. Detailed Project Description ................................................................................................................ 5 VI. Project Location ................................................................................................................................. -

Freight Rail B

FREIGHT RAIL B Pennsylvania has 57 freight railroads covering 5127 miles across the state, ranking it 4th largest rail network by mileage in the U.S. By 2035, 246 million tons of freight is expected to pass through the Commonwealth of Pennsylvania, an increase of 22 percent over 2007 levels. Pennsylvania’s railroad freight demand continues to exceed current infrastructure. Railroad traffic is steadily returning to near- World War II levels, before highways were built to facilitate widespread movement of goods by truck. Rail projects that could be undertaken to address the Commonwealth’s infrastructure needs total more than $280 million. Annual state-of-good-repair track and bridge expenditures for all railroad classes within the Commonwealth are projected to be approximately $560 million. Class I railroads which are the largest railroad companies are poised to cover their own financial needs, while smaller railroads are not affluent enough and some need assistance to continue service to rural areas of the state. BACKGROUND A number of benefits result from using rail freight to move goods throughout the U.S. particularly on longer routes: congestion mitigation, air quality improvement, enhancement of transportation safety, reduction of truck traffic on highways, and economic development. Railroads also remain the safest and most cost efficient mode for transporting hazardous materials, coal, industrial raw materials, and large quantities of goods. Since the mid-1800s, rail transportation has been the centerpiece of industrial production and energy movement. Specifically, in light of the events of September 11, 2001 and from a national security point of view, railroads are one of the best ways to produce a more secure system for transportation of dangerous or hazardous products. -

South Central Regional ITS Architecture Final Report

Regional ITS Architecture PennDOT South Central ITS Architecture Region TABLE OF CONTENTS 1 INTRODUCTION .................................................................................. 1 1.1 ARCHITECTURE PROCESS .....................................................................................2 1.2 USING THIS DOCUMENT........................................................................................3 1.3 UTILITY OF THE ARCHITECTURE .............................................................................7 1.4 ITS STANDARDS...................................................................................................8 1.5 MAINTAINING THE ARCHITECTURE .......................................................................10 1.6 MOVING FORWARD/INSTITUTIONALIZING ITS........................................................16 2 ARCHITECTURE SCOPE ................................................................... 23 2.1 SCOPE OF SERVICES ..........................................................................................23 2.2 CONFORMITY MATRIX.........................................................................................23 2.3 DESCRIPTION OF THE REGION .............................................................................26 2.4 REGIONAL STAKEHOLDERS .................................................................................30 2.5 REGIONAL ITS PROJECTS ...................................................................................34 3 REGIONAL SYSTEMS INVENTORY, NEEDS, AND SERVICES ......... -

Harrisburg Division

HARRISBURG DIVISION NORTHERN REGION TIMETABLE NUMBER 1 EFFECTIVE SEPTEMBER 19, 2015 COMMITTED TO SAFETY DOUBLE ZEROS ZERO INJURIES ZERO INCIDENTS HARRISBURG DIVISION TIMETABLE TABLE OF CONTENTS I. Timetable General Information..................................................5 a. Train Dispatcher Contact Information…………………….4 b. Station Page........................................................................5 c. Explanation of Characters.................................................5 d. Diesel Unit Groups.............................................................6 e. Main Track Control.............................................................6 f. Division Special Instructions.............................................6 II. Harrisburg Division Station Pages.....................................7-263 III. Harrisburg Division Special Instructions......................265-269 NORFOLK SOUTHERN DIVISION HEADQUARTERS Train Dispatching Office 4600 Deer Path Road Harrisburg, PA 17110 Assistant Superintendent – Microwave 541-2146 Bell 717-541-2146 Dispatch Chief Dispatcher Microwave 541-2158 Bell 717-541-2158 Harrisburg East Dispatcher Microwave 541-2136 Bell 717-541-2136 Harrisburg Terminal Dispatcher Microwave 541-2138 Bell 717-541-2138 Lehigh Line Dispatcher Microwave 541-2139 Bell 717-541-2139 Southern Tier Dispatcher Microwave 541-2144 Bell 717-541-2144 Mainline Dispatcher Microwave 541-2142 Bell 717-541-2142 D&H Dispatcher Microwave 541-2143 Bell 717-541-2143 EMERGENCY 911 HARRISBURG DIVISION TIMETABLE GENERAL INFORMATION A. -

Planning Context

1. Preface This plan serves as the update to Chapter 12, the transportation plan element, of the 2003 Cumberland County Comprehensive Plan. Background information and specific statistics on the modes of transportation in the county can be found in Chapter 11 of the comprehensive plan and in the Harrisburg Area Transportation Study (HATS) Long Range Transportation Plan1. 2. Introduction Cumberland County is home to a variety of transportation resources ranging from interstate highways to sidewalks in local neighborhoods. The transportation infrastructure found in the county supports the national, state and local economies and the high quality of life in our communities, alike. The value of our transportation system warrants the county’s involvement in its planning, design, construction and maintenance. Cumberland County’s transportation planning authority emanates from Article III of the Pennsylvania Municipalities Planning Code (MPC), Act 247 of 1968. The MPC requires county comprehensive plans to include a plan for the “movement of people and goods” that includes all modes of transportation. Under this planning authorization the county’s actual role in planning and implementing improvements for all modes of transportation must be carefully managed. This plan identifies the salient transportation issues and needs facing the county and recommends a series of county-based strategies and action steps aimed at addressing the identified needs and issues. 3. Highways and Bridges Issues and Needs Cumberland County has an extensively developed highway network that provides for local, regional, and national transportation. All roads in the county are owned and maintained by municipalities, the state, or the federal government. The rich hydrologic resources of Cumberland County are spanned by 438 bridges that are over 20’ in length2. -

RAIL (FREIGHT) B 2006 Report Card for Pennsylvania’S Infrastructure

RAIL (FREIGHT) B 2006 Report Card for Pennsylvania’s Infrastructure In 1998, 919 million tons of freight passed through the Commonwealth. In 2020, that value is expected to be 1,397 million tons. Railroad freight demand is growing at a much faster rate than the general population, and railroad traffic is steadily approaching World War II levels. Projects that could be undertaken to address the Commonwealth’s infrastructure needs total some $280 million. Annual state of good repair track and bridge expenditures for all railroad classes within the state are projected to be approximately $560 million. Class I and larger railroads are more poised to cover their own financial needs. Smaller railroads are not as fortunate and need the most assistance to remain competitive. BACKGROUND A number of benefits result from supporting rail freight: congestion mitigation, air quality improvement, improving transportation safety, curtailing truck traffic growth on highways, job growth and economic development. Railroads also remain the safest and most viable mode for transporting hazardous materials, coal, industrial raw materials and large quantities of goods. Since the mid-1800’s, rail transportation has been the centerpiece of industrial production and energy generation. Specifically, in light of September 11th and from a national security point of view, railroads are one of most secure options for transporting dangerous or hazardous products. In fact, the majority of spent nuclear fuel rods will likely be sent via rail to the newly established federal depository. Surely, many of these shipments will pass through the Keystone State. By further improving the rail infrastructure, railroad operation can become even safer and more difficult to disrupt by any terrorist group. -

Elegant Report

Pennsylvania State Transportation Advisory Committee PENNSYLVANIA STATEWIDE PASSENGER RAIL NEEDS ASSESSMENT TECHNICAL REPORT TRANSPORTATION ADVISORY COMMITTEE DECEMBER 2001 Pennsylvania State Transportation Advisory Committee TABLE OF CONTENTS Acknowledgements...................................................................................................................................................4 1.0 INTRODUCTION .........................................................................................................................5 1.1 Study Background........................................................................................................................................5 1.2 Study Purpose...............................................................................................................................................5 1.3 Corridors Identified .....................................................................................................................................6 2.0 STUDY METHODOLOGY ...........................................................................................................7 3.0 BACKGROUND RESEARCH ON CANDIDATE CORRIDORS .................................................14 3.1 Existing Intercity Rail Service...................................................................................................................14 3.1.1 Keystone Corridor ................................................................................................................................14 -

South Central Pennsylvania Regional Goods Movement Study

South Central Pennsylvania Regional Goods Movement Study final report prepared for Harrisburg Area Transportation Study South Central Pennsylvania Regional Goods Movement Steering Committee prepared by Cambridge Systematics, Inc. with Global Insight PB Farradyne A. Strauss-Wieder, Inc. November 2006 www.camsys.com final report South Central Pennsylvania Regional Goods Movement Study prepared for Harrisburg Area Transportation Study South Central Pennsylvania Regional Goods Movement Steering Committee prepared by Cambridge Systematics, Inc. 4800 Hampden Lane, Suite 800 Chevy Chase, Maryland 20814 with Global Insight PB Farradyne A. Strauss-Wieder, Inc. date November 2006 South Central Pennsylvania Regional Goods Movement Study: Steering Committee Membership Mr. Eulois Cleckley – FHWA-HQ Mr. Richard Schmoyer – Adams County Mr. Matthew Smoker – FHWA – PA Mr. Kirk Stoner – CCPC Mr. Carmine Fiscina FHWA-Philadelphia Mr. Phil Tarquino – FCPC Mr. John Bork – FHWA Mr. Christopher Neumann – LCPC Mr. Dennis McGee FMCSA-PA Mr. Glenn Taggart – LCPC – PROJECT FACILITATOR Mr. Patrick Quigley FMCSA-PA Mr. David Royer – LCPC Mr. Paul Lang FHWA-DE Division Mr. Jonathan Fitzkee – Lebanon County Ms. Tameka Macon FHWA – NJ Ms. Felicia Dell – YCPC Mr. Robert Hannigan – PennDOT Central Mr. Donald Bubb – YCPC Mr. Brian Wall – PennDOT Central Mr. Jeph Rebert – YCPC Mr. Dan Walston – PennDOT Central Mr. Rick Crawford – Norfolk Southern Corporation Mr. Walt Panko – PennDOT Central Mr. William Shafer – Norfolk Southern Corporation Mr. Jeff Reed – PennDOT Central Mr. James Runk – PAMTA Mr. Terry Adams – PennDOT 8-0 Mr. Donald Siekerman – PAMTA Mr. Greg Vaughn – PennDOT 8-0 Mr. Craig Zumbrun – South Central Assembly Mr. Dennis Sloand – PennDOT 8-0 Ms. Megan Ardary – South Central Assembly Deputy Secretary Sharon Daboin – PennDOT BRFP &W Mr. -

Pennsylvania Comprehensive Freight Movement Plan

Draft Final PENNSYLVANIA COMPREHENSIVE FREIGHT MOVEMENT PLAN Prepared for: Pennsylvania Department of Transportation Prepared by: June 3, 2015 PA On Track Freight Planning: A Multi-state and Multi-modal Approach Supply chains and freight flows vary by commodity, industry, supply and demand, and origins and destinations and are rarely limited to a single jurisdiction. Transportation freight plans are best approached by a multi-faceted perspective of trade lanes, key commodities, or key industries in the U.S. and neighboring trade partners, such as Latin America and Canada, rather than simply from a state’s geography. PennDOT, for example, is a critical component of the freight movement system in the I- 95 Corridor – a region of 16 States (from Maine to Florida) generating 41% of the Nation’s Gross Domestic Product and representing 40% of the Nation’s population. Within this essential region are: • 41 Ports, and Coastal Shipping Lanes in the Atlantic, and the Intercostal and Inland Waterways • 106+ Airports • 907,000 miles of Highway • 30,495 miles of Freight Railroad Track, with 1,111 heavy-rail directional route miles (70% of the national total) As international markets continue to emerge for imports and exports, and with expansions of the Panama and Suez Canals, the port-airport-rail-highway system in the I- 95 Corridor will remain one of the most critical components of the United States’ freight network. Comprehensive freight planning must address the systems within individual political jurisdictions or state boundaries while recognizing the multi-state economic corridor that comprises the trip of a particular mode. Assistance for addressing the growing needs of the industry will come from the USDOT national freight strategic plan guidance, with its national freight framework built upon multistate corridors. -

Congressional Record—House H1272

H1272 CONGRESSIONAL RECORD — HOUSE March 10, 2005 could be money going to education, For instance, Colgate-Palmolive said until the Bush administration takes its going to health care, going to address that while the corporate tax bill will privatization plan off the table, we can- the infrastructure of our Nation. allow it to repatriate half a billion dol- not work together to address Social Se- So the President’s plan clearly needs lars in profits, the company will actu- curity solvency. help. And his failure to provide a clear ally shut down a third of its factories Even one of our Republican col- and honest accounting of the difficult and lay off 4,400 employees. leagues, Senator LINDSEY GRAHAM, has tradeoffs between increases in debt, Sun Microsystems, $1 billion in new admitted that privatization is not a benefits cuts and tax increases shows a profits during the so-called corporate plan that will fix Social Security. On failure in leadership. tax ‘‘holiday,’’ will be repatriated, but Tuesday he said, ‘‘We now have this f plans to lay off 3,600 employees. huge fight over a sideshow. It has al- DuPont Photomasks is repatriating ways been a sideshow, but we sold it as b 1100 $24 million, but laying off 100 employ- the main event.’’ That is a Republican DENOUNCING VIOLENCE AGAINST ees, while expanding its Singapore fac- Senator calling the President’s plan a WOMEN AND SUPPORTING VITAL tory at the same time. sideshow. SOCIAL SECURITY BENEFITS While the corporate suites enjoy the Mr. Speaker, it is a sideshow because FOR WOMEN fruits of this tax cut, Americans are it does nothing to strengthen Social Security. -

To Download Our Comprehensive Plan in PDF

CONEWAGO TOWNSHIP COMPREHENSIVE PLAN South Londonderry Township BE AVER N B E Lebanon County U Derry Township P A S C U R H H M E O R A A W N H E V L S I E L H L O A D IT E N O E H T P C S IN E R H A E D M E L C O C K N Y YE E E H L S I Z EL R UR A G LA W P E B A R H E T O E I T O M D S H D R L T B O O O W I S N W I E T E H D N M C E D O E H R O W R U S G N R H W C T E O Y H H O E D L T P A D N N DTO C N E A OU H R R E Iro B S n Run T R N E U D T AB743 R B O A O B S A K K L O E RO R B LE CO RHO AD S H ON o BB f R I f E e LU r B C r e e k RIDGE K I R B Y M E A D O W E R I A L L AB341 E COL B EBR OOK E T A PIKE D TU RN VANIA O NNSYL E PE PENNSYLVANIA TURNPIKE D 76 §¨¦ H E R S H n E u Y R s l l i r B OLL OAK KN L P O L E DA R N E PL O D MA O S P N E C T K Y M E O I L S L L E L A V R PA AB283 283 O AB283 L M P D L A E 28 H 3 go C reek E Con ewa R S H E Y L L I M L L I L E H BEAG Londonderry Township Mount Joy Township Lancaster County k e R re E C F o F g a O w e H n o C Elizabethtown Borough Adopted October 14, 2009 CONEWAGO TOWNSHIP COMPREHENSIVE PLAN Adopted October 14, 2009 Prepared for the Conewago Township Board of Supervisors John D. -

I-95 Corridor Coalition

I-95 Corridor Coalition Southeast Rail Operations Study, Phase II Tasks 1 and 2: Strategic Corridor Identification and Mapping FINAL REPORT June 2011 Tasks 1 and 2: Strategic Corridor Identification and Mapping Southeast Rail Operations Study, Phase II Tasks 1 and 2: Strategic Corridor Identification and Mapping Prepared for: I-95 Corridor Coalition Sponsored by: I-95 Corridor Coalition Prepared by: Cambridge Systematics FINAL REPORT June 2011 This report was produced by the I-95 Corridor Coalition. The I-95 Corridor Coalition is a partnership of state departments of transportation, regional and local transportation agencies, toll authorities, and related organizations, including law enforcement, port, transit, and rail organizations, from Maine to Florida, with affiliate members in Canada. Additional information on the Coalition, including other project reports, can be found on the Coalition’s web site at http://www.i95coalition.org. Tasks 1 and 2: Strategic Corridor Identification and Mapping Table of Contents Executive Summary ............................................................................................. ES-1 Passenger Rail Initiatives ........................................................................... ES-1 Freight Rail Initiatives ................................................................................ ES-5 Next Steps ..................................................................................................... ES-9 1.0 Objective .....................................................................................................