Korea Music Copyright Association

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Inglish Dikshineri = English

Kriol – Inglish Dikshineri English – Kriol Dictionary Compiled and edited by Yvette Herrera Myrna Manzanares Silvana Woods Cynthia Crosbie Ken Decker Editor-in-Chief Paul Crosbie Belize Kriol Project Cover design: Adapted from Yasser Musa Cover photo: Courtesy Robert Spain at 2008 Crooked Tree Cashew Fest Illustrations in the Introduction are from The Art of Reading, SIL International Literacy Department SIL International provided linguistic consultancy to this publication of the Belize Kriol Project. The Belize Kriol Project is the language development arm of The National Kriol Council. www.sil.org The National Kriol Council House of Culture, Regent Street P.O. Box 2447 Belize City Belize www.kriol.org.bz Belize Kriol Project P.O. Box 2120 Office: 33 Central American Blvd. Belize City, Belize The first printing of this dictionary was in 2007 and was funded by The Ministry of Education and The National Institute of Culture and History House of Culture, Regent Street Belize City, Belize First Edition Copyright © 2007 Belize Kriol Project Second Printing 2009 ISBN # 978-976-95165-1-9 Printed by Print Belize Belmopan, Belize CONTENTS List of Abbreviations .......................................... iv Foreword by Sir Colville Young.............................v Preface ..................................................................... ix Acknowledgements.............................................. xi Introduction.............................................................1 Guide to Using the Dictionary...........................3 The -

The Korean Internet Freak Community and Its Cultural Politics, 2002–2011

The Korean Internet Freak Community and Its Cultural Politics, 2002–2011 by Sunyoung Yang A thesis submitted in conformity with the requirements for the degree of Doctor of Philosophy Graduate Department of Anthropology University of Toronto © Copyright by Sunyoung Yang Year of 2015 The Korean Internet Freak Community and Its Cultural Politics, 2002–2011 Sunyoung Yang Doctor of Philosophy Department of Anthropology University of Toronto 2015 Abstract In this dissertation I will shed light on the interwoven process between Internet development and neoliberalization in South Korea, and I will also examine the formation of new subjectivities of Internet users who are also becoming neoliberal subjects. In particular, I examine the culture of the South Korean Internet freak community of DCinside.com and the phenomenon I have dubbed “loser aesthetics.” Throughout the dissertation, I elaborate on the meaning-making process of self-reflexive mockery including the labels “Internet freak” and “surplus (human)” and gender politics based on sexuality focusing on gender ambiguous characters, called Nunhwa, as a means of collective identity-making, and I explore the exploitation of unpaid immaterial labor through a collective project making a review book of a TV drama Painter of the Wind. The youth of South Korea emerge as the backbone of these creative endeavors as they try to find their place in a precarious labor market that has changed so rapidly since the 1990s that only the very best succeed, leaving a large group of disenfranchised and disillusioned youth. I go on to explore the impact of late industrialization and the Asian financial crisis, and the nationalistic desire not be left behind in the age of informatization, but to be ahead of the curve. -

The Globalization of K-Pop: the Interplay of External and Internal Forces

THE GLOBALIZATION OF K-POP: THE INTERPLAY OF EXTERNAL AND INTERNAL FORCES Master Thesis presented by Hiu Yan Kong Furtwangen University MBA WS14/16 Matriculation Number 249536 May, 2016 Sworn Statement I hereby solemnly declare on my oath that the work presented has been carried out by me alone without any form of illicit assistance. All sources used have been fully quoted. (Signature, Date) Abstract This thesis aims to provide a comprehensive and systematic analysis about the growing popularity of Korean pop music (K-pop) worldwide in recent years. On one hand, the international expansion of K-pop can be understood as a result of the strategic planning and business execution that are created and carried out by the entertainment agencies. On the other hand, external circumstances such as the rise of social media also create a wide array of opportunities for K-pop to broaden its global appeal. The research explores the ways how the interplay between external circumstances and organizational strategies has jointly contributed to the global circulation of K-pop. The research starts with providing a general descriptive overview of K-pop. Following that, quantitative methods are applied to measure and assess the international recognition and global spread of K-pop. Next, a systematic approach is used to identify and analyze factors and forces that have important influences and implications on K-pop’s globalization. The analysis is carried out based on three levels of business environment which are macro, operating, and internal level. PEST analysis is applied to identify critical macro-environmental factors including political, economic, socio-cultural, and technological. -

The K-Pop Wave: an Economic Analysis

The K-pop Wave: An Economic Analysis Patrick A. Messerlin1 Wonkyu Shin2 (new revision October 6, 2013) ABSTRACT This paper first shows the key role of the Korean entertainment firms in the K-pop wave: they have found the right niche in which to operate— the ‘dance-intensive’ segment—and worked out a very innovative mix of old and new technologies for developing the Korean comparative advantages in this segment. Secondly, the paper focuses on the most significant features of the Korean market which have contributed to the K-pop success in the world: the relative smallness of this market, its high level of competition, its lower prices than in any other large developed country, and its innovative ways to cope with intellectual property rights issues. Thirdly, the paper discusses the many ways the K-pop wave could ensure its sustainability, in particular by developing and channeling the huge pool of skills and resources of the current K- pop stars to new entertainment and art activities. Last but not least, the paper addresses the key issue of the ‘Koreanness’ of the K-pop wave: does K-pop send some deep messages from and about Korea to the world? It argues that it does. Keywords: Entertainment; Comparative advantages; Services; Trade in services; Internet; Digital music; Technologies; Intellectual Property Rights; Culture; Koreanness. JEL classification: L82, O33, O34, Z1 Acknowledgements: We thank Dukgeun Ahn, Jinwoo Choi, Keun Lee, Walter G. Park and the participants to the seminars at the Graduate School of International Studies of Seoul National University, Hanyang University and STEPI (Science and Technology Policy Institute). -

アーティスト 商品名 品番 ジャンル名 定価 URL 100% (Korea) RE

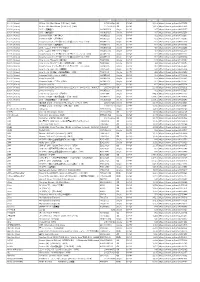

アーティスト 商品名 品番 ジャンル名 定価 URL 100% (Korea) RE:tro: 6th Mini Album (HIP Ver.)(KOR) 1072528598 K-POP 2,290 https://tower.jp/item/4875651 100% (Korea) RE:tro: 6th Mini Album (NEW Ver.)(KOR) 1072528759 K-POP 2,290 https://tower.jp/item/4875653 100% (Korea) 28℃ <通常盤C> OKCK05028 K-POP 1,296 https://tower.jp/item/4825257 100% (Korea) 28℃ <通常盤B> OKCK05027 K-POP 1,296 https://tower.jp/item/4825256 100% (Korea) 28℃ <ユニット別ジャケット盤B> OKCK05030 K-POP 648 https://tower.jp/item/4825260 100% (Korea) 28℃ <ユニット別ジャケット盤A> OKCK05029 K-POP 648 https://tower.jp/item/4825259 100% (Korea) How to cry (Type-A) <通常盤> TS1P5002 K-POP 1,204 https://tower.jp/item/4415939 100% (Korea) How to cry (Type-B) <通常盤> TS1P5003 K-POP 1,204 https://tower.jp/item/4415954 100% (Korea) How to cry (ミヌ盤) <初回限定盤>(LTD) TS1P5005 K-POP 602 https://tower.jp/item/4415958 100% (Korea) How to cry (ロクヒョン盤) <初回限定盤>(LTD) TS1P5006 K-POP 602 https://tower.jp/item/4415970 100% (Korea) How to cry (ジョンファン盤) <初回限定盤>(LTD) TS1P5007 K-POP 602 https://tower.jp/item/4415972 100% (Korea) How to cry (チャンヨン盤) <初回限定盤>(LTD) TS1P5008 K-POP 602 https://tower.jp/item/4415974 100% (Korea) How to cry (ヒョクジン盤) <初回限定盤>(LTD) TS1P5009 K-POP 602 https://tower.jp/item/4415976 100% (Korea) Song for you (A) OKCK5011 K-POP 1,204 https://tower.jp/item/4655024 100% (Korea) Song for you (B) OKCK5012 K-POP 1,204 https://tower.jp/item/4655026 100% (Korea) Song for you (C) OKCK5013 K-POP 1,204 https://tower.jp/item/4655027 100% (Korea) Song for you メンバー別ジャケット盤 (ロクヒョン)(LTD) OKCK5015 K-POP 602 https://tower.jp/item/4655029 100% (Korea) -

JEWELS of the EDWARDIANS by Elise B

JEWELS OF THE EDWARDIANS By Elise B. Misiorowski and Nancy K. Hays Although the reign of King Edward VII of ver the last decade, interest in antique and period jew- Great Britain was relatively short (1902- elry has grown dramatically. Not only have auction 1910), the age that bears his name produced 0 houses seen a tremendous surge in both volume of goods distinctive jewelry and ushered in several sold and prices paid, but antique dealers and jewelry retail- new designs and manufacturing techniques. ers alikereportthat sales inthis area of the industry are During this period, women from the upper- excellent and should continue to be strong (Harlaess et al., most echelons of society wore a profusion of 1992). As a result, it has become even more important for extravagant jewelry as a way of demon- strating their wealth and rank. The almost- jewelers and independent appraisers to understand-and exclusive use of platinum, the greater use of know how to differentiate between-the many styles of pearls, and the sleady supply of South period jewelry on the market. African diamonds created a combination Although a number of excellent books have been writ- that will forever characterize Edwardian ten recently on various aspects of period jewelry, there are jewels. The Edwardian age, truly the last so many that the search for information is daunting. The era of the ruling classes, ended dramatically purpose of this article is to provide an overview of one type with the onset of World War I. of period jewelry, that of the Edwardian era, an age of pros- perity for the power elite at the turn of the 19th century. -

Conceptually Androgynous

Umeå Center for Gender Studies Conceptually androgynous The production and commodification of gender in Korean pop music Petter Almqvist-Ingersoll Master Thesis in Gender Studies Spring 2019 Thesis supervisor: Johanna Overud, Ph. D. ABSTRACT Stemming from a recent surge in articles related to Korean masculinities, and based in a feminist and queer Marxist theoretical framework, this paper asks how gender, with a specific focus on what is referred to as soft masculinity, is constructed through K-pop performances, as well as what power structures are in play. By reading studies on pan-Asian masculinities and gender performativity - taking into account such factors as talnori and kkonminam, and investigating conceptual terms flower boy, aegyo, and girl crush - it forms a baseline for a qualitative research project. By conducting qualitative interviews with Swedish K-pop fans and performing semiotic analysis of K-pop music videos, the thesis finds that although K-pop masculinities are perceived as feminine to a foreign audience, they are still heavily rooted in a heteronormative framework. Furthermore, in investigating the production of gender performativity in K-pop, it finds that neoliberal commercialism holds an assertive grip over these productions and are thus able to dictate ‘conceptualizations’ of gender and project identities that are specifically tailored to attract certain audiences. Lastly, the study shows that these practices are sold under an umbrella of ‘loyalty’ in which fans are incentivized to consume in order to show support for their idols – in which the concept of desire plays a significant role. Keywords: Gender, masculinity, commercialism, queer, Marxism Contents Acknowledgments ................................................................................................................................... 1 INTRODUCTION ................................................................................................................................. -

A Thesis Presented to the Faculty of Divinity of the University of Edinburgh for the Degree of Ph.D

THE RELATION OF ST. PAUL'S ETHICS TO HIS DOCTRINE OF SALVATION BY H. W. KSRLEY, B.A., B.D. A THESIS PRESENTED TO THE FACULTY OF DIVINITY OF THE UNIVERSITY OF EDINBURGH FOR THE DEGREE OF PH.D. THE RELATION OF ST. PAUL'S ETHICS TO HIS DOCTRINE OF SALVATION CONTENTS Page CHAPTER ONE INTRODUCTION................................ 1 CHAPTER TWO CONVERSION AND BACKGROUND................... 10 CHAPTER THREE THE DOCTRINE OF "IN CHRIST1"................. 60 CHAPTER FOUR THE NATURE OF: REDEMPTION.................... 106 CHAPTER FIVE THE NATURE OF JUSTIFICATION................. 145 CHAPTER SIX THE NATURE OF RECONCILIATION................ 182 CHAPTER SEVEN THE LIFE OF HOLINESS........................ £14 CHAPTER EIGHT ETHICAL PRESUPPOSITIONS..................... 248 CHAPTER ONE INTRODUCTION In the epistles of St. Paul we find a remarkably well- developed theology. Ethical teaching is, however, by no means lacking. A brief survey is sufficient to show that a large proportion of his extant writings is devoted to practical advice and exhortation. Frequently the main body of ethical teaching follows the section in which his theology is developed and explained. Sometimes, as in the epistle to the Romans, the transition seems to be abrupt and the connection obscure. Possibly it is for this reason that there has been, at times, a tendency either to emphasize the doctrine or the ethic to the exclusion of the other, or to give more or less equal weight to both, and thus to emphasize the disconnection between the two. Some ages have taken St. Paul's doctrine without his ethic. Our own seems to be more concerned with ethics than with theology, and the attempt is made to establish morality without a doctrinal basis. -

YG Entertainment Buy (122870 KQ ) (Maintain)

[Korea] Entertainment May 13, 2021 YG Entertainment Buy (122870 KQ ) (Maintain) Increasing content leverage TP: W56,000 Upside: 25.8% Mirae Asset Securities Co., Ltd. Jeong -yeob Park [email protected] 1Q21 review : Big earnings beat Consolidated revenue of W97bn (+83.9% YoY), OP of W9.5bn (turn to profit YoY) In 1Q21, YG Entertainment proved its enhanced fundamentals by overcoming the absence of offline performances/activities with the release of new content (Rosé and Treasure). Revenue from albums/digital content/goods was up 170.6% YoY, driven by strong sales of albums (980,000 copies; helped by new releases) and goods. Digital content revenue surged 125.6% YoY, boosted by BLACKPINK’s online concert (280,000 paid views and net revenue of around W8bn). Revenue from Google came in strong at W4.5bn (excluding BLACKPINK concert; vs. W2.5bn in 1Q20) on the back of new releases and subscriber growth. Despite constraints on artist activities, management revenue expanded 44.7% YoY, fueled by luxury advertisers’ (Dior, Saint Laurent and Tiffany & Co.) strong preference for YG artists. Elsewhere, the company recorded W15.6bn from TV production (YG Studioplex’s Mr. Queen ) and a valuation gain of roughly W5bn related to Tencent Music Entertainment. Expectations on 2H21 artist Artist activities to gather steam; IP monetization to strengthen on Weverse incl usion activities and Weverse 1) Earnings: During the 2018-20 absence of its main artist group, YG Entertainment built a robust lineup that includes BLACKPINK, Treasure, and iKON. We expect robust ad and appearance income to continue, supported by the growing international profile of the company’s artists. -

URL 100% (Korea)

アーティスト 商品名 オーダー品番 フォーマッ ジャンル名 定価(税抜) URL 100% (Korea) RE:tro: 6th Mini Album (HIP Ver.)(KOR) 1072528598 CD K-POP 1,603 https://tower.jp/item/4875651 100% (Korea) RE:tro: 6th Mini Album (NEW Ver.)(KOR) 1072528759 CD K-POP 1,603 https://tower.jp/item/4875653 100% (Korea) 28℃ <通常盤C> OKCK05028 Single K-POP 907 https://tower.jp/item/4825257 100% (Korea) 28℃ <通常盤B> OKCK05027 Single K-POP 907 https://tower.jp/item/4825256 100% (Korea) Summer Night <通常盤C> OKCK5022 Single K-POP 602 https://tower.jp/item/4732096 100% (Korea) Summer Night <通常盤B> OKCK5021 Single K-POP 602 https://tower.jp/item/4732095 100% (Korea) Song for you メンバー別ジャケット盤 (チャンヨン)(LTD) OKCK5017 Single K-POP 301 https://tower.jp/item/4655033 100% (Korea) Summer Night <通常盤A> OKCK5020 Single K-POP 602 https://tower.jp/item/4732093 100% (Korea) 28℃ <ユニット別ジャケット盤A> OKCK05029 Single K-POP 454 https://tower.jp/item/4825259 100% (Korea) 28℃ <ユニット別ジャケット盤B> OKCK05030 Single K-POP 454 https://tower.jp/item/4825260 100% (Korea) Song for you メンバー別ジャケット盤 (ジョンファン)(LTD) OKCK5016 Single K-POP 301 https://tower.jp/item/4655032 100% (Korea) Song for you メンバー別ジャケット盤 (ヒョクジン)(LTD) OKCK5018 Single K-POP 301 https://tower.jp/item/4655034 100% (Korea) How to cry (Type-A) <通常盤> TS1P5002 Single K-POP 843 https://tower.jp/item/4415939 100% (Korea) How to cry (ヒョクジン盤) <初回限定盤>(LTD) TS1P5009 Single K-POP 421 https://tower.jp/item/4415976 100% (Korea) Song for you メンバー別ジャケット盤 (ロクヒョン)(LTD) OKCK5015 Single K-POP 301 https://tower.jp/item/4655029 100% (Korea) How to cry (Type-B) <通常盤> TS1P5003 Single K-POP 843 https://tower.jp/item/4415954 -

Publications Contents Digest January/2020

IEEE Communications Society Publications Contents Digest January/2020 Direct links to magazine and journal s and full paper pdfs via IEEE Xplore ComSoc Vice President – Publications – Robert Schober Director – Journals – Michele Zorzi Director – Magazines – Ekram Hossain Magazine Editors EIC, IEEE Communications Magazine – Tarek El-Bawab AEIC, IEEE Communications Magazine – Antonio Sanchez-Esquavillas EIC, IEEE Network Magazine – Mohsen Guizani AEIC, IEEE Network Magazine – David Soldani EIC, IEEE Wireless Communications Magazine – Yi Qian AEIC, IEEE Wireless Communications Magazine – Nirwan Ansari EIC, IEEE Communications Standards Magazine – Glenn Parsons AEIC, IEEE Communications Standards Magazine – Zander Lei EIC, IEEE Internet of Things Magazine — Keith Gremban EIC, China Communications – Zhongcheng Hou Journal Editors EIC, IEEE Transactions on Communications –Tolga M. Duman EIC, IEEE Journal on Selected Areas In Communications (J-SAC) –Raouf Boutaba EIC, IEEE Communications Letters – Marco Di Renzo EIC, IEEE Communications Surveys & Tutorials – Ying-Dar Lin EIC, IEEE Transactions on Network & Service Management (TNSM) – Filip De Turck EIC, IEEE Wireless Communications Letters – Kai Kit Wong EIC, IEEE Transactions on Wireless Communications – Junshan Zhang EIC, IEEE Transactions on Mobile Communications – Marwan Krunz EIC, IEEE/ACM Transactions on Networking – Eytan Modiano EIC, IEEE/OSA Journal of Optical Communications & Networking (JOCN) – Jane M. Simmons EIC, IEEE/OSA Journal of Lightwave Technology – Gabriella Bosco Co-EICs, -

Teaser Memorandum

Teaser Memorandum The First Half of 2017 Investment Opportunities In Korea Table of Contents Important Notice ………………………………… 1 Key Summary ………………………………… 2 Expected Method of Investment Promotion …………………………… 3 Business Plan ………………………………… 4 Business Introduct ………………………………… 5 License ………………………………… 11 Capacity ………………………………… 12 Market ………………………………… 13 Financial Figures ………………………………… 14 Key Summary Private & Confidential Investment Highlights RBW is a K-POP (Hallyu) contents production company founded by producer/songwriter Kim Do Hoon, Kim Jin Woo, and Hwang Sung Jin, who have produced numerous K-POP artists such as CNBLUE, Whee-sung, Park Shin Hye, GEEKS, 4MINUTE etc. Based on the “RBW Artist Incubating System’, the company researches and provides various K-POP related products such as OEM Artist & Music Production (Domestic/Overseas), Exclusive Artist Production (MAMAMOO, Basick, Yangpa etc.), Overseas Broadcasting Program Planning & Production (New concept music game show/Format name: RE:BIRTH), and K-POP Educational Training Program. With its business ability, RBW is currently making a collaboration with various domestic and overseas companies, including POSCO, NHN, Human Resources Development Service of Korea, Ministry of Labor & Employment, and KOTRA. • Business with RBW’s Unique Artist Incubating •Affiliation Relationship with International Key Factors System Companies Description • With analyzing the artists’ potentials and market trend, every stage for training and debuting artists (casting, training, producing, and album production) is efficiently processed under this system. Pictures Company Profiles Category Description Establishment Date 2013. 8. 26 Revenue 12 Billion Won (12 Million $) (2016) Website www.rbbridge.com Current Shareholder C.E.O. Kim Jin Woo 29.2%, C.E.O. Kim Do Hoon 29.2%, Institutional Investment 31.7%, Executives and Staff Composition 5.6%, Etc.