Coca-Cola Decision

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Coca Cola Was the Purchase of Parley Brands

SWAMI VIVEKANAND UNIVERSITY A PROJECT REPORT ON MARKETING STRATGIES OF TOP BRANDS OF COLD DRINKS Submitted in partial fulfilment for the Award of degree of Master in Management Studies UNDER THE GUIDANCE OF SUBMITTED BY Prof.SHWETA RAJPUT HEMANT SONI CERTIFICATE Certified that the dissertation title MARKETING STRATEGIES OF TOP BRANDS OF COLD DRINKS IN SAGAR is a bonafide work done Mr. HEMANI SONI under my guidance in partial fulfilment of Master in Management Studies programme . The views expressed in this dissertation is only of that of the researcher and the need not be those of this institute. This project work has been corrected by me. PROJECT GUIDE SWETA RAJPUT DATE:: PLACE: STUDENT’S DECLARATION I hereby declare that the Project Report conducted on MARKETING STRATEGIES OF TOP BRANDS OF COLD DRINKS Under the guidance of Ms. SHWETA RAJPUT Submitted in Partial fulfillment of the requirements for the Degree of MASTER OF BUSINESS ADMINISTRATION TO SVN COLLAGE Is my original work and the same has not been submitted for the award of any other Degree/diploma/fellowship or other similar titles or prizes. Place: SAGAR HEMANT SONI Date: ACKNOWLEDGEMENT It is indeed a pleasure doing a project on “MARKETING STRATEGIES OF TOP BRANDS OF COLD DRINKS”. I am grateful to sir Parmesh goutam (hod) for providing me this opportunity. I owe my indebtedness to My Project Guide Ms. Shweta rajput, for her keen interest, encouragement and constructive support and under whose able guidance I have completed out my project. She not only helped me in my project but also gave me an overall exposure to other issues related to retailing and answered all my queries calmly and patiently. -

Coca Cola India: Little Drops of Joy,” September 8, 2007

oikos Global Case Writing Competition 2009 Corporate Sustainability Track Finalist Coca-Cola India’s Corporate Social Responsibility Strategy Hadiya Faheem, ICMR Center for Management Research, Hyderabad, India This is an Online Inspection Copy. Protected under Copyright Law. Reproduction Forbidden unless Authorized. Copyright © 2009 by the Author. All rights reserved. This case was prepared by Hadiya Faheem as a basis for class discussion rather than to illustrate the effective or ineffective handling of an administrative situation. No part of this publication may be reproduced, stored in a retrieval system, used in a spreadsheet, or transmitted in any form by any means without permission. To order copies, call 0091-40-2343-0462/63 or write to ICMR, Plot # 49, Nagarjuna Hills, Hyderabad 500 082, India or email [email protected] oikos sustainability case collection http://www.oikos-international.org/projects/cwc oikos Global Case Writing Competition 2009 Finalist “Coca-Cola India undertakes a diverse range of activities for the benefit of the community across the country. As part of our CSR strategy, sustainable water management remains our top priority.” 1 Deepak Kaul, Regional Vice-President, South, The Hindustan Coca-Cola Beverages Pvt. Ltd., in 2007. “It is in India where the company’s abuse of water resources have been challenged vociferously, and communities across India living around Coca-Cola’s bottling plants have organized in large numbers to demand an end to the mismanagement of water…. In response to the growing Indian campaigns against Coca-Cola, the company has decided to promote rainwater harvesting — a traditional Indian practice — in and around its bottling plants in India. -

Coca-Cola La Historia Negra De Las Aguas Negras

Coca-Cola La historia negra de las aguas negras Gustavo Castro Soto CIEPAC COCA-COLA LA HISTORIA NEGRA DE LAS AGUAS NEGRAS (Primera Parte) La Compañía Coca-Cola y algunos de sus directivos, desde tiempo atrás, han sido acusados de estar involucrados en evasión de impuestos, fraudes, asesinatos, torturas, amenazas y chantajes a trabajadores, sindicalistas, gobiernos y empresas. Se les ha acusado también de aliarse incluso con ejércitos y grupos paramilitares en Sudamérica. Amnistía Internacional y otras organizaciones de Derechos Humanos a nivel mundial han seguido de cerca estos casos. Desde hace más de 100 años la Compañía Coca-Cola incide sobre la realidad de los campesinos e indígenas cañeros ya sea comprando o dejando de comprar azúcar de caña con el fin de sustituir el dulce por alta fructuosa proveniente del maíz transgénico de los Estados Unidos. Sí, los refrescos de la marca Coca-Cola son transgénicos así como cualquier industria que usa alta fructuosa. ¿Se ha fijado usted en los ingredientes que se especifican en los empaques de los productos industrializados? La Coca-Cola también ha incidido en la vida de los productores de coca; es responsable también de la falta de agua en algunos lugares o de los cambios en las políticas públicas para privatizar el vital líquido o quedarse con los mantos freáticos. Incide en la economía de muchos países; en la industria del vidrio y del plástico y en otros componentes de su fórmula. Además de la economía y la política, ha incidido directamente en trastocar las culturas, desde Chamula en Chiapas hasta Japón o China, pasando por Rusia. -

Coca-Cola FEMSA, S.A.B. De C.V

As filed with the Securities and Exchange Commission on June 25, 2007 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F ANNUAL REPORT PURSUANT TO SECTION 13 OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2006 Commission file number 1-12260 Coca-Cola FEMSA, S.A.B. de C.V. (Exact name of registrant as specified in its charter) Not Applicable (Translation of registrant’s name into English) United Mexican States (Jurisdiction of incorporation or organization) Guillermo González Camarena No. 600 Centro de Ciudad Santa Fé 01210 México, D.F., México (Address of principal executive offices) Securities registered or to be registered pursuant to Section 12(b) of the Act: Title of Each Class Name of Each Exchange on Which Registered American Depositary Shares, each representing 10 Series L Shares, without par value ................................................. New York Stock Exchange, Inc. Series L Shares, without par value............................................................. New York Stock Exchange, Inc. (not for trading, for listing purposes only) Securities registered or to be registered pursuant to Section 12(g) of the Act: None Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None The number of outstanding shares of each class of capital or common stock as of December 31, 2006 was: 992,078,519 Series A Shares, without par value 583,545,678 Series D Shares, without par value 270,906,004 Series L Shares, without par value Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. -

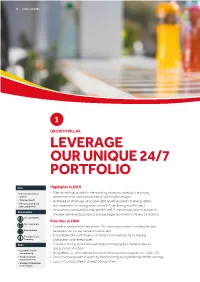

Leverage Our Unique 24/7 Portfolio

26 COCA-COLA HBC 1 GROWTH PILLAR LEVERAGE OUR UNIQUE 24/7 PORTFOLIO KPIs Highlights in 2019 • FX-neutral revenue • Maintained high growth in the sparkling category, aided by the strong growth performance of sophisticated adult sparkling beverages • Volume growth • Achieved another year of double-digit revenue growth in energy drinks • FX-neutral revenue per case growth and expanded the energy portfolio with Coke Energy and Predator • Innovations supported overall growth, with 4.2pp of total volume growth in Stakeholders the year delivered by products and packages launched in the last 12 months Our consumers Priorities in 2020 Our customers • Continue expanding to become a 24/7 beverage partner, creating shared Shareholders value with our consumers and customers The Coca-Cola • Consolidate the performance of product innovations by increasing Company distribution and repeat sales Risks • Continue driving growth in sparkling by leveraging light variants, flavour and pack architecture • Consumer health and wellbeing • Bring ready-to-drink tea back to growth through a strong plan for FUZETEA • Geopolitical and • Drive revenue growth in water by implementing our hydration portfolio strategy macroeconomic • Launch Costa Coffee in at least 10 countries • Strategic stakeholder relationships INTEGRATED ANNUAL REPORT 2019 27 SR CG FS SSR SI Introduction As lifestyles and consumer habits change, Percentage the motivations and occasions driving of Coca-Cola beverage consumption are also evolving. HBC revenue Our category strategy We are unlocking growth potential in segments beyond our core sparkling portfolio, offering a wider choice of drinks to meet consumer needs at any time of the day. In line with growing societal concerns around environmental issues, consumers are looking for sustainably-sourced ingredients and responsible packaging. -

Featured Cocktail OLD BAKERY Kind of Blueberry $3.5 $6 Kolsch with Blueberries

LeMoNAdE Beer glass: $9, pitcher: $32 9 oz 16oz 2ND SHIFT Hibiscus Wit $3.5 $6 Lavendula Cucumber Hazy Belgian witbier with a touch of tart hibiscus Gin, lavender honey, Gin, cucumber liqueur, 2ND SHIFT Little Big Hop $3.5 $6 lemonade fresh mint, lemonade New England Session IPA with 5 different hops. Stupid good! 4HANDS Chocolate Milk Stout $3.5 $6 Rosemary Peach El Diablo Dark chocolate nibs and roasted chocolate malt. Great dessert beer. Purus Organic Vodka, Milagro Tequila, creme 4HANDS City Museum Pils $3.5 $6 American Pilsner with tangerine and ginger. For one of the fav spots rosemary, peach, lemonade de cassis, ginger beer, 4HANDS Contact High: Juiced $3.5 $6 lemonade Pale Wheat Ale with tangerine juice and zest Cherry Limeade BROADWAY Bonne Femme $3.5 $6 Purus Organic Vodka, Strawberry American Pale Wheat brewed with gallons of local Missouri honey. cherry, lemonade, lime, Basil CIVIL LIFE Angel & Sword $3 $5 lemon-lime soda Purus Organic Vodka, fresh Amber/ESB with a worldly array of hops and malt. Extra special. basil, strawberry, lemonade CRANE Trailsmith $3.5 $6 Crisp, refreshing Farmhouse Saison bursting with citrus Hawaiian Breeze DESTIHL Extended Jam $3.5 $6 Coconut rum, peach nectar, Bourbon Basil Deadhead Hazy IPA with wailing aromas and groovy tropical hops lemonade, cranberry juice Old Forester, basil, iced tea, DESTIHL Flanders Red $3.5 $6 lemonade Wild sour with tart cherry and sour candy notes. Dry wine finish Limoncello DESTIHL Piña Colada Gose $3.5 $6 Purus Organic Vodka, fresh Ginger Peach Super fun and complex sour with pineapple and coconut. -

The Story of Coca-Cola

The Story of Coca-Cola Atlanta Beginnings 1886-1892 It was 1886, and in New York Harbor, workers were constructing the Statue of Liberty. Eight hundred miles away another great American symbol was about to be unveiled. Like many people who change history, John Pemberton, a Civil War veteran and Atlanta pharmacist, was inspired by simple curiosity. He loved tinkering with medicinal formulas, and one afternoon, searching for a quick cure for headaches, he stirred up a fragrant, caramel-colored liquid in a three-legged pot. When it was done, he carried it a few doors down to Jacobs’ Pharmacy. Here, the mixture was combined with carbonated water and sampled by customers who all agreed – this new drink was something special. So Jacobs’ Pharmacy put it on sale for five cents a glass. Pemberton's bookkeeper Frank Robinson named the mixture â Coca-Cola , and wrote it out in his distinct script. To this day, Coca-Cola is written the same way. In its first year, the Company sold about 9 glasses of Coca-Cola a day. A century later, The Coca-Cola Company has produced over 10 billion gallons of syrup. Unfortunately for Pemberton, he was more of an inventor than a businessman, and had no idea that he had invented one of the greatest products in the world. Over the course of three years, 1888-1891, Pemberton sold the Company to Atlanta businessman Asa Griggs Candler for a total of about $2300. Candler would become the Company's first president, and the first to bring real vision to the business and the brand. -

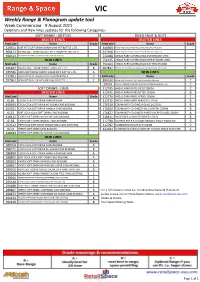

Weekly Range & Planogram Update Tool

VIC Weekly Range & Planogram update tool Week Commencing - 9 August 2021 Deletions and New lines updates for the following Categories - SOFT DRINKS - BOTTLES DRIED FRUIT & NUTS DELETED LINES DELETED LINES MetCode Name Grade MetCode Name Grade 329551 DIET RITE SOFT DRINK LEMON LIME PET BOTTLE 1.25L 346969 ANGAS PARK DRIED CRANBERRIES CRANBERRIES SNACK PACKS 6PK 968143 NEXBA SOFT DRINK SUGAR FREE LEMON PET BOTTLE 1L 347698 ANGAS PARK DRIED FRUIT C/BERRIES RAISINS B/BERRIES SNACK 6PK 948313 SCHWEPPES SOFT DRINK LEMONADE ZERO SUGAR PET BOTTLE 2L 751088 ANGAS PARK SUPERBLENDS ANTIOXIDANT 170G NEW LINES 751135 ANGAS PARK SUPERBLENDS ENERGY BOOST 200G MetCode Name Grade 751164 ANGAS PARK SUPERBLENDS GUT HEALTH 200G 636267 BISLERI SOFT DRINK CHINOTTO BOTTLE 1.25L B 907817 MURRAY RIVER SUN MUSCAT RAISINS AUSTRALIAN ORGANIC BAG 325GM 289586 KIRKS SOFT DRINK PASITO SUGAR FREE BOTTLE 1.25L A NEW LINES 313961 NEXBA SOFT DRINK CREAMING SODA SUGAR FREE BOTTLE 1L C MetCode Name Grade 297961 NEXBA SOFT DRINK LEMON SQUASH SUGAR FREE BOTTLE 1L C 894140 ANGAS PARK DRIED FRUIT FRUIT SALAD RESEALABLE BAG 500G C 50704 ANGAS PARK DRIED PRUNES AUSTRALIAN RESEALABLE BAG 1KG C SOFT DRINKS - CANS 312745 ANGUS PARK DATES DICED 200GM C DELETED LINES 313741 ANGUS PARK DATES PITTED 125GM B MetCode Name Grade 312774 ANGUS PARK DRIED APPLES 100GM C 6116 COCA-COLA SOFT DRINK CANS 8X200ML 313725 ANGUS PARK DRIED APRICOTS 125GM B 848649 COCA-COLA SOFT DRINK NO SUGAR CANS 8X200ML 176518 COMMUNITY CO GINGER GLACED 125GM B 650931 COCA-COLA SOFT DRINK VANILLA CANS 8X200ML 176699 -

Setting New Trends

Setting New Trends 2005 Annual Report FESMA INSIDE FRONT COVER Total Revenues Operating Income millions of 2005 pesos millions of 2005 pesos 6 105,582 2 3 6 15,587 3,526 5,864 6,660 7,689 8,572 9,490 82,496 96,833 59,99 36,500 40,939 47,082 49,435 54,526 56,188 13,07 14,23 120000 120,000 16,000 10,54 16000 100000 100,000 12,000 12000 80000 80,000 60000 60,000 8,000 8000 40000 40,000 4,000 4000 20000 20,000 0 0 0 0 a96 a97 a98 a99 a00 a01 a02 a03 a04 a05 ’96 ’97 ’98 ’99 ’00 ’01 ’02 ’03 ’04 ’05 ’96 ’97 ’98 ’99 ’00 ’01 ’02 ’03 ’04 ’05 a96 a97 a98 a99 a00 a01 a02 a03 a04 a05 % Annual % Annual Growth 12.2 15.0 5.0 10.3 3.0 6.8 37.5 17.4 9.0 Growth 66.3 13.6 15.5 11.5 10.7 11.1 24.0 8.9 9.5 % Operating Margin 9.7 14.3 14.1 15.6 15.7 16.9 17.6 15.8 14.7 14.8 ROIC* Total Assets millions of 2005 pesos 3 2 8 1 6 2 3 9.4 9.8 5.1 7.5 8.7 9.8 9.9 9.9 125,998 13.3 12.1 50,39 52,87 53,02 52,46 56,31 67,06 47,58 15 15% 140,000 115,692 125,075 140000 120,000 120000 12 12% 100,000 100000 9 9% 80,000 80000 60,000 60000 6 6% 40,000 40000 3 3% 20,000 20000 0 0% 0 0 a96 a97 a98 a99 a00 a01 a02 a03 a04 a05 ’96 ’97 ’98 ’99 ’00 ’01 ’02 ’03 ’04 ’05 ’96 ’97 ’98 ’99 ’00 ’01 ’02 ’03 ’04 ’05 a96 a97 a98 a99 a00 a01 a02 a03 a04 a05 *Based on EVA® methodology as per Stern, Stewart & Co. -

View Annual Report

2019 ANNUAL REPORT BUSINESS OUR COVID-19 & OUR 2019 REPORT AN IMPORTANT MESSAGE WE CREATE THE VALUE OUR BUSINESS PERFORMANCE & OUTLOOK READING THIS REPORT IN THE CONTEXT OF COVID-19 01 COVID-19 & Our 2019 Report 40 Group Performance As you will see, we have adopted a new approach to We will continue to align with advice from the World 02 Who We Are 46 Australian Beverages Amatil’s 2019 Annual Report. We have combined our Health Organisation and the relevant Government 04 Where We Operate 50 New Zealand & Fiji Annual and Sustainability Reports for the first time, Authorities in our countries of operation. PERFORMANCE building on our commitment to move towards integrated OUTLOOK& 06 2019 Highlights 52 Alcohol & Coffee Given the significant uncertainty around the duration reporting, and to showcase the year that was for our 08 Chairman’s Review 54 Indonesia & Papua New Guinea and impacts of the COVID-19 pandemic, on 17 March 2020 company, our people and all of our stakeholders. 10 Group Managing Director’s Review 57 Corporate & Services Amatil withdrew the earnings guidance, which was 1 At the time of publication of this 2019 Annual Report previously issued to the market on 20 February 2020. (“Report”), the world is responding to the COVID-19 This Report reflects our results and achievements for THE VALUE WE CREATE BEING A SUSTAINABLE BUSINESS pandemic and the duration, impacts and severity are 2019. The strategies, priorities, shareholder value continuing, with many unknowns. 12 Strategy and Long-term Value Creation 58 Sustainability Strategy proposition and outlook statements were relevant and 14 Our Shareholder Value Proposition 61 Sustainability Goals and Progress At Coca-Cola Amatil, protecting the health and safety appropriate at the time of being issued within the 2019 16 Thriving Customers of our people and those we work with will always be our Financial and Statutory Reports, but COVID-19 will BEING A SUSTAINABLE 20 Committed Partners overriding priority. -

1. Acknowledgement 5 2. Preface 6 3. Introduction 7 (A) History of Coca-Cola (B) Around the World (C) Various Brands of Coca-Col

CONTENTS 1. Acknowledgement 55 2. Preface 66 3. Introduction 77 (a) History of Coca-Cola (b) Around the world (c) Various brands of Coca-Cola Company (d) Products and packaging MYTHS and RUMORS (e) Mission Coca Cola India (f) Faboulas facts about Coca-Cola (g) Slogan (h) Going Global Coca-Cola dominated, 4. A Brief profile of Flavoured & Pack. 53 5. Objective 57 6. Research Methodology 58 (a) Method of marking research (b) Research decision (c) Method of data collection (d) Sampling plan 7. Limitations 68 8. Analysis & Design 69 9. Finding 83 10. Conclusion 84 11. Bibliography 91 11 PREFACE The present is an era of cut throat competition after liberalization policy of Indian Govt. plethora of MNC enters in India. As a result today every business hold a view of of globalization. The new products are launching and the old and absolute product are being obliterating from the market every second. There is no monopoly played by an enterprise in every one. There is an existence of rival enterprise the rivals are strong enough to vanguisth each other sort of dard erstine struggle has taken its break though in the corporate and business world. The same is befalling between Coca-Cola and Pepsi. Some times one Coca Cola over powered the Pepsi and some time vice versa has taken place regarding the market share and scaled volume though the rivalry contrive rood the year but it is at zenith in summer. 22 INTRODUCTION HISTORY OF COCA-COLA BBIRTH OF A REFRESHING IIDEA John Stryth pemberton first introduced the refreshing coke taste of Coca cola in Atlanta Georgia. -

Coca-Cola, Globalization, and the Cultural Politics of Branding in the Twentieth Century

The Company that Taught the World to Sing: Coca-Cola, Globalization, and the Cultural Politics of Branding in the Twentieth Century by Laura A. Hymson A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy (American Culture) in The University of Michigan 2011 Doctoral Committee: Associate Professor, James W. Cook, Chair Professor Philip J. Deloria Professor Susan J. Douglass Professor Penny Von Eschen © Laura A. Hymson 2011 Acknowledgements I owe an extraordinary debt to the people and institutions that helped and supported me as I worked to complete this dissertation. While working on this project, I spent time in several cities, including: Ann Arbor, New York, Atlanta, Urbana- Champagne, Alexandria, Washington, D.C, Newark, and Hartford. In all of these places where I have lived, researched, or taught, I have been shown incredible kindness and I am grateful for everyone who has helped me along the way. Thanks first to the chair of my dissertation committee, Jay Cook, who has been exceptionally generous with his time. Without his insightful feedback, invaluable advice, and thoughtful comments this dissertation would not have been possible. I can only hope to be as effective and compassionate as a teacher and mentor as he has been to me. My entire dissertation committee was composed of scholars whose work I truly admire and I am grateful for the time they devoted to my ideas and my work. Penny Von Eschen and Phil Deloria provided important feedback on drafts, and made suggestions for research and writing that helped advance my thinking on a number key issues at the heart of this project.