Challenges for European Aerospace Suppliers Contents Introduction 3

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Thanks a Million, Tornado

Aug 11 Issue 39 desthe magazine for defenceider equipment and support Thanks a million, Tornado Fast jets in focus − Typhoon and Tornado impress See inside Welcome Warrior Goliath’s The future Warfare goes Voyager returns to war giant task is now on screen lockheedmartin.com/f35 NOT JUSTAN AIRCRAFT, THE UK’SAIRCRAFT The F-35 Lightning II isn’t just a cutting-edge aircraft. It also demonstrates the power of collaboration. Today, a host of UK companies are playing their part in developing and building this next-generation F-35 fi ghter. The F-35 programme is creating thousands of jobs throughout the country, as well as contributing LIGHTNINGLIGHTNING IIII to UK industrial and economic development. It’s enhancing the UK’s ability to compete in the global technology marketplace. F-35 Lightning II. Delivering prosperity and security. UNITED KINGDOM THE F-35 LIGHTNING II TEAM NORTHROP GRUMMAN BAE SYSTEMS PRATT & WHITNEY LOCKHEED MARTIN 301-61505_NotJust_Desider.indd 1 7/14/11 2:12 PM FRONTISPIECE 3 lockheedmartin.com/f35 Jackal helps keep the peace JACKAL CUTS a dash on Highway 1 between Kabul and Kandahar, one of the most important routes in Afghanistan. Soldiers from the 9th/12th Royal Lancers have been helping to keep open a section of the road which locals use to transport anything from camels to cars. The men from the Lancers have the tough task of keeping the highway open along with members of 2 Kandak of the Afghan National Army, who man checkpoints along the road. NOT JUSTAN AIRCRAFT, Picture: Sergeant Alison Baskerville, Royal Logistic Corps THE UK’SAIRCRAFT The F-35 Lightning II isn’t just a cutting-edge aircraft. -

Coproduce Or Codevelop Military Aircraft? Analysis of Models Applicable to USAN* Brazilian Political Science Review, Vol

Brazilian Political Science Review ISSN: 1981-3821 Associação Brasileira de Ciência Política Svartman, Eduardo Munhoz; Teixeira, Anderson Matos Coproduce or Codevelop Military Aircraft? Analysis of Models Applicable to USAN* Brazilian Political Science Review, vol. 12, no. 1, e0005, 2018 Associação Brasileira de Ciência Política DOI: 10.1590/1981-3821201800010005 Available in: http://www.redalyc.org/articulo.oa?id=394357143004 How to cite Complete issue Scientific Information System Redalyc More information about this article Network of Scientific Journals from Latin America and the Caribbean, Spain and Journal's webpage in redalyc.org Portugal Project academic non-profit, developed under the open access initiative Coproduce or Codevelop Military Aircraft? Analysis of Models Applicable to USAN* Eduardo Munhoz Svartman Universidade Federal do Rio Grande do Sul, Porto Alegre, Rio Grande do Sul, Brazil Anderson Matos Teixeira Universidade Federal do Rio Grande do Sul, Porto Alegre, Rio Grande do Sul, Brazil The creation of the Union of South American Nations (USAN) aroused expectations about joint development and production of military aircraft in South America. However, political divergences, technological asymmetries and budgetary problems made projects canceled. Faced with the impasse, this article approaches features of two military aircraft development experiences and their links with the regionalization processes to extract elements that help to account for the problems faced by USAN. The processes of adoption of the F-104 and the Tornado in the 1950s and 1970s by countries that later joined the European Union are analyzed in a comparative perspective. The two projects are compared about the political and diplomatic implications (mutual trust, military capabilities and regionalization) and the economic implications (scale of production, value chains and industrial parks). -

EFC JIP CBRN Workshop

EFC JIP CBRN Workshop Finmeccanica areas of interest Michele Genisio Brussels - September 15, 2011 Contents Contents 1. Finmeccanica key data 2010 2. Proposed areas of investigation Commercial in Confidence 1 - Finmeccanica Key Data 2010 FY2010 FY2009 Net Profit 557 M€ 718 M€ Revenues € 18.695 m Order Intake 22,5 B€ 21,1 B€ Employees 75,197 73,056 R & D 2.0 B€ 1.98 B€ DEFENSE AND DEFENSE AERONAUTICS HELICOPTERS TRANSPORT ENERGY SPACE SECURITY SYSTEMS ELECTRONICS 2.809 M€ 3.644 M€ 1.962 M€ 7.137 M€ 1.210 M€ 1.413 M€ 925 M€ . Alenia Aeronautica . AgustaWestland . AnsaldoBreda . DRS Technologies . Oto Melara . Ansaldo Energia . Telespazio . Alenia Aermacchi . BAAC . Ansaldo STS . ElsagDatamat . WASS . Ansaldo Fuel Cells . Thales Alenia Space . SuperJet . BredaMenarini . Selex . MBDA . Ansaldo Nucleare Communications International bus . Selex Galileo . ATR . Selex Sistemi . Eurofighter GmbH Integrati 100% owned by Finmeccanica . Selex Service Management JVs Finmeccanica view Emerging requirements in the CBRN area: C and B detectors • Wide threat range • Speed of Response • Low Detection Levels • Threat Identification M&S of CBRN architectures • representing the whole process, from threat to recovery • enabling military-civil interaction • multi-threat scenarios. M&S of CBRN Architectures OBJECTIVES Modelling & Simulation of a CBRN Architecture representing: - Environment: both predictable (terrain characteristics, urban context, road network, etc) and unpredictable (crowd behaviour, humand behaviour, weather etc ) aspects - Responders: -

Airbus Use of Nadcap EASA Workshop – May 10, 2011

Commodity – Siglum - Reference Date Airbus Use of Nadcap EASA Workshop – May 10, 2011 Presented by Pascal Blondet - PDQC Use menu "View - Header & Footer" for Presentation title - Siglum - Reference month 200X Summary 1. What is Nadcap? 2. How Airbus is controlling Nadcap? Page 2 © AIRBUS S.A.S. All rights reserved. Confidential and proprietary document. Use menu "View - Header & Footer" for Presentation title - Siglum - Reference month 200X Summary 1. What is Nadcap? 2. How Airbus is controlling Nadcap? Page 3 © AIRBUS S.A.S. All rights reserved. Confidential and proprietary document. Use menu "View - Header & Footer" for Presentation title - Siglum - Reference month 200X What is Nadcap? The leading, worldwide cooperative program of major companies designed to manage a cost effective consensus approach to special processes and products and provide continual improvement within the aerospace industry by • Promoting and supporting common standards worldwide • Implementing common auditing and accreditation process More than 60 Subscribing Primes (50% Americas, 50% Europe) More than 4 000 Audits conducted per year More than 4200 active supplier/process accreditations About 80 Auditors (FTE) Page 4 © AIRBUS S.A.S. All rights reserved. Confidential and proprietary document. Use menu "View - Header & Footer" for Presentation title - Siglum - Reference month 200X Nadcap Commodities Special Processes • Nondestructive Testing (NDT) • Metallic Material Testing Laboratories (MTL) • Non Metallic Material Testing Laboratories (NMMT) • Heat Treating (HT) • Coatings (CT) • Chemical Processing (CP) • Welding (WLD) • Nonconventional Machining & Surface Enhancement (NMSE) Systems & Products including Special Processes • Sealants (SLT) • Distributors (DIST) • Aerospace Quality Management Systems (AQS) • Fluid Distribution Standards (FLU) • Elastomer Seals (SEALS) • Composites (COMP) Already mandated by Airbus • Electronics (ETG) Airbus engagement in Nadcap TGs but not yet mandated No Airbus engagement to date Page 5 © AIRBUS S.A.S. -

ATR Appoints New Head of Communications

Toulouse, 7th May 2015 ATR appoints new Head of Communications Palmira Rotolo has been appointed as new Head of Communications of world’s leading turboprop manufacturer ATR. In her new position, she will be in charge of coordinating activities in the fields of Events, Brand Image, and both Internal and External Communications. Mrs.Rotolo has held a number of successive different positions within Alenia Aermacchi (previously Alenia Aeronautica), Superjet International, Finmeccanica and ATR. Since 2014, she was Head of Marketing Communication at Alenia Aermacchi. Previously, she had took the position of Head of Communication and Image (2012-2014), Deputy Head of Human Resources International (2010- 2012) and Head of International Communication (2007-2010), all of them also at Alenia Aermacchi. Before this, among other positions, she had been CEO Public Relations assistant while making part of the Task Force Team for the launch of SuperJet International (2006-2007), and she had managed Events at Finmeccanica (2004-2005). Mrs.Rotolo has an extensive knowledge of ATR, where she had already worked between 1992 and 2003, being successively in charge of External Relations, Public Relations and Exhibitions. She helds a Degree in Social Science from LUMSA University in Rome, Italy, and a Degree in Trainee Officer for mercantile shipping. About ATR: ATR is the world leader on the market for regional aircraft. Known for its exemplary eco-responsibility, ATR is a role model for airlines, not only in terms of its performance and reliability, but also in terms of profitability on short-haul air routes. ATR is ISO 14001 certified. Its aircraft are currently operated by more than 180 airlines in over 90 countries. -

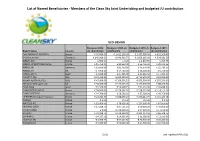

List of Named Beneficiaries - Members of the Clean Sky Joint Undertaking and Budgeted JU Contribution

List of Named Beneficiaries - Members of the Clean Sky Joint Undertaking and budgeted JU contribution ECO-DESIGN Budgeted 2008- Budgeted 2009-JU Budgeted 2010-JU Budgeted 2011- Beneficiaries Country JU contribution contribution contribution JU contribution DAV DASSAULT AVIATION France € 95,000.00 € 1,411,100.00 € 1,305,000.00 € 652,500.00 FhG Fraunhofer Germany € 145,900.00 € 943,593.75 € 1,069,165.00 € 534,582.50 AIRBUS SAS France € 500.00 € 0.00 € 1,833.50 € 916.75 AIRBUS OPERATIONS France France € 15,750.00 € 82,550.00 € 56,426.50 € 28,213.25 AIRBUS DE Germany € 15,650.00 € 81,450.00 € 43,578.00 € 21,789.00 AIRBUS UK UK € 7,350.00 € 24,700.00 € 13,500.00 € 6,750.00 AIRBUS SPAIN Spain € 2,900.00 € 47,305.00 € 34,644.50 € 17,322.25 AGUSTA Spa Italy € 22,185.00 € 102,350.00 € 124,400.00 € 62,200.00 ALENIA AERONAUTICA Italy € 47,000.00 € 310,036.25 € 595,500.00 € 297,750.00 Westland Helicopter Ltd UK € 50,000.00 € 127,655.00 € 177,000.00 € 88,500.00 EADS CASA Spain € 5,500.00 € 59,998.75 € 91,676.00 € 45,838.00 EUROCOPTER SAS FR France € 58,950.00 € 229,202.50 € 228,225.00 € 114,112.50 EUROCOPTER DE Germany € 14,700.00 € 58,500.00 € 87,500.00 € 43,750.00 LIEBHERR Aerospace Toulouse France € 22,782.50 € 108,076.25 € 270,212.75 € 135,106.38 SAFRAN France € 0.00 € 0.00 € 0.00 € 0.00 AIRCELLE ACL France € 10,000.00 € 78,000.00 € 134,000.00 € 67,000.00 HISPANO SUIZA France € 17,208.75 € 67,791.25 € 90,000.00 € 45,000.00 MICROTURBO France € 0.00 € 170,000.00 € 34,020.00 € 17,010.00 SNECMA France € 32,208.75 € 173,000.00 € 132,217.50 € 66,108.75 -

Two Recent Developments in Italy Illustrate How Boeing Is Working

n FEATURE STORY Two recent developments in Italy illustrate how Boeing is working with top technology providers around the world—and helping strengthen a nation’s aerospace industry in support of Boeing’s cross-enterprise efforts OTO.COM H ISTOCKP Magnifico! 38 December 2007/January 2008 BOEING FRONTIERS n FEATURE STORY BY MAUREEN JENKINS Inside or Boeing, doing business in Italy is about more than Advanced research activities: Boeing and Alenia Aeronautica merely selling commercial airplanes or military aircraft. It’s recently signed a memorandum of understanding that calls for the Falso about leveraging the country’s high-tech and aerospace companies to jointly develop research activities in advanced materials infrastructure—and that includes its scientists and engineers— and integrated fuselage aircraft structures. Page 39 so that Italian companies can better compete in the global market- Educational collaboration: Through its connections and support, place. And with Italian corporations of all sizes partnering on key Boeing is helping strengthen the high-tech skill base of southern Italy Boeing programs, it’s critical that they be involved in the creation by facilitating a partnership between a university in the United States and development of advanced technologies. and one in Italy. Page 40 The next step in the frequent collaboration between Alenia Aeronautica and Boeing is a newly signed memorandum of un- derstanding, one where they’ll jointly develop research activities in advanced materials and integrated fuselage aircraft structures. The agreement also provides for the opening of a small Boeing Italian Research Office in the southern region of Campania, an area where government officials are keen on strengthening the high-tech skill base and creating jobs. -

Mp-Msg-045-05

Modeling & Simulation for Experimentation, Test & Evaluation and Training: Alenia Aeronautica Experiences and Perspectives Mrs. Marcella Guido Alenia Aeronautica Simulation & System’s Operability C.so Marche 41, 10146 Torino Italy [email protected] Mr. Cristiano Montrucchio Alenia Aeronautica Simulation & System’s Operability Manager C.so Marche, 41, 10146 Torino Italy [email protected] ABSTRACT The use of Modeling & Simulation to support aircraft development is nowadays common practice within any modern aeronautical industry, and a long term key capability of Alenia Aeronautica. Starting from such crucial role, M&S utilization has progressively expanded to effectively support the aeronautical system’s early stages – feasibility and definition, and later stages – in service support and pilots training, becoming an essential element during the entire system’s life cycle. The main tool to implement and sustain such capability is the Synthetic Environment, which relies on the following elements: • Flight Simulators with engineering and training potential • Simulators networking at both LAN and WAN (Local and Wide Area Network) levels • Tactical scenarios • Image generation • Virtual reality The paper will focus on the latest major experiences of Alenia Aeronautica with the AMX ACOL, Eurofighter, C-27J and Sky-X UAV Programs, from systems concept, through development and experimentation, to pilots training and mission rehearsal. Moreover, Alenia Aeronautica’s approach and perspectives in the field of the simulation of Network Centric Operations will be described: the Network Centric Simulation Environment 1.0 INTRODUCTION The use of Modeling & Simulation (M&S) in aerospace engineering is nowadays common practice within any modern aeronautical firm and a long term key capability of Alenia Aeronautica. -

ATR Appoints New Head of Quality

Toulouse, 6th May 2015 ATR appoints new Head of Quality World’s leading turboprop manufacturer ATR is pleased to announce Roberto Del Pezzo as new Head of Quality. ATR has created this new direction in the aim of further developing and strengthening all activities related to quality, a core part of its business. Mr. Del Pezzo will be in charge of implementing the Quality policy with respect to the ATR objectives. Among his new responsibilities, he will be in charge of providing quality methodological support across the different directions of ATR, managing customer’s satisfaction measurement, interfacing with the certification agencies and managing the entire quality process associated to the ATR program. He will directly report to ATR’s Chief Executive Officer, Patrick de Castelbajac. Mr. Del Pezzo started its aeronautical career at Aeritalia (today Alenia Aermacchi) in 1983, holding various positions with the Product Support Directorate. In 1994 he joined the Quality Directorate of Alenia Aeronautica (today Alenia Aermacchi) as Quality Control manager first, and then he took this same position specifically for the ATR aircraft. In 1997 he was appointed as Head of the production plant of Alenia at Nola (Italy), and two years later he became Head of American programs at the plant of Pomigliano (Italy), including the manufacturing activities of Alenia for the Boeing 717s, 767s, and 777s. He moved back to the Quality Directorate in 2004, holding different positions including Senior Vice-President (SVP) Quality, SVP Quality assurance & Certification Deputy and Head of Program & Product Quality. He holds a full-honors Degree in Mechanical Engineering from Federico II University, in Naples. -

EASA-TCDS-A.407 Alenia C--27J

TCDS No.: EASA.A.407 C-27J Page 1/14 Issue: 05 Date: 19/12/2016 European Aviation Safety Agency EASA TYPE-CERTIFICATE DATA SHEET No. EASA.A.407 for C-27J Type Certificate Holder: Leonardo S.p.A. – Divisione Velivoli Piazza Monte Grappa, 4 00195 Rome ITALY Airworthiness Category: Large Aeroplanes For Models: C-27J TCDS No.: EASA.A.407 C-27J Page 2/14 Issue: 05 Date: 19/12/2016 Intentionally left blank TCDS No.: EASA.A.407 C-27J Page 3/14 Issue: 05 Date: 19/12/2016 TABLE OF CONTENT SECTION 1: C-27J 4 I. General 4 II. Certification Basis 4 III. Technical Characteristics and Operational Limitations 6 IV. Operating and Service Instructions 10 V. Notes 11 SECTION: ADMINISTRATIVE 13 I. Acronyms and Abbreviations 13 II. Type Certificate Holder Record 13 III. Change Record 14 TCDS No.: EASA.A.407 C-27J Page 4/14 Issue: 05 Date: 19/12/2016 SECTION 1: C-27J I. General 1. Type/ Model/ Variant: Alenia C-27J 2. Performance Class: A 3. Certifying Authority: EASA 4. Manufacturer: Leonardo S.p.A. – Divisione Velivoli Piazza Monte Grappa, 4 00195 Rome ITALY 5. EASA Validation Application Date: 02 October 1996 6. EASA Type Validation Date: 18 June 2001 (original issue by ENAC Italy) 06 December 2002 (amended issue by ENAC Italy) 25 September 2008 (original issue by EASA) 24 April 2012 (amended issue by EASA) 19 December 2016 (amended issue by EASA) II. Certification Basis 1. Reference Date for determining the applicable requirements 02 October 1996 2. EASA Airworthiness Requirements JAR 25, Large Aeroplanes, Change 14, Amendment 25/96/1 dated 19 April 1996 JAR 1, Definitions, Change 5 dated 15 July 1996 JAR AWO Change 2, effective 01 August 1996 Reversions to FAR 25 amdt 35 paragraphs are applicable to C-27J: 25.783 Doors 25.805 Flight crew emergency exits 25.809 Emergency exit arrangement 25.811 Emergency exit marking 25.812 Emergency lighting 25.813 Emergency exit access. -

The Role of Italian Fighter Aircraft in Crisis Management Operations: Trends and Needs V

ISSN 2239-2122 16 IAI Research Papers T HE N. 1 European Security and the Future of Transatlantic Relations, edited by Italian combat aircraft have played an increasing important role in the R OLE The IAI Research Papers are brief monographs written by one or Riccardo Alcaro and Erik Jones, 2011 international missions in which Italy has participated in the post-Cold War era OF more authors (IAI or external experts) on current problems of inter- – from the First Gulf War to Libya, including Bosnia-Herzegovina, Kosovo and N. 2 Democracy in the EU after the Lisbon Treaty, edited by Raaello Matarazzo, I TALIAN THE ROLE OF ITALIAN 2011 Afghanistan. This participation has been a signicant tool of Italy's defense national politics and international relations. The aim is to promote greater and more up to date knowledge of emerging issues and policy, and therefore of its foreign policy towards crisis areas relevant to its N. 3 The Challenges of State Sustainability in the Mediterranean, edited by F Silvia Colombo and Nathalie Tocci, 2011 national interests (from the Western Balkans to the Mediterranean), as well as IGHTER FIGHTER AIRCRAFT IN trends and help prompt public debate. towards its most important allies within NATO and the EU. This IAI publication N. 4 Re-thinking Western Policies in Light of the Arab Uprisings, edited by A Riccardo Alcaro and Miguel Haubrich-Seco, 2012 analyses the role of these military capabilities in recent operations and their IRCRAFT prospects for the future. In fact, a number of trends can be inferred from the CRISIS MANAGEMENT A non-prot organization, IAI was founded in 1965 by Altiero Spinelli, N. -

The Market for Military Transport Aircraft

The Market for Military Transport Aircraft Product Code #F616 A Special Focused Market Segment Analysis by: Military Aircraft Forecast Analysis 2 The Market for Military Transport Aircraft 2010-2019 Table of Contents Executive Summary .................................................................................................................................................2 Introduction................................................................................................................................................................2 Trends..........................................................................................................................................................................3 Competitive Environment.....................................................................................................................................13 Market Statistics .....................................................................................................................................................13 Table 1 - The Market for Military Transport Aircraft Unit Production by Headquarters/Company/Program 2010 - 2019......................................................16 Table 2 - The Market for Military Transport Aircraft Value Statistics by Headquarters/Company/Program 2010 - 2019 ......................................................19 Figure 1 - The Market for Military Transport Aircraft Unit Production 2010-2019 (Bar Graph).....................................................................................22