1 a Tale of Two Jurisdictions

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Inverell Shire Council Report 2008 Local Government Elections

Inverell Shire Council Report 2008 Local Government Elections REPORT ON THE 2008 LOCAL GOVERNMENT ELECTIONS INVERELL SHIRE COUNCIL General Manager Inverell Shire Council PO Box 138 Inverell NSW 2360 Dear General Manager I am pleased to present to you a report on the conduct and administration of the 2008 Local Government Elections held for Inverell Shire Council. Yours sincerely Colin Barry Electoral Commissioner 31 August 2009 REPORT ON THE 2008 LOCAL GOVERNMENT ELECTIONS INVERELL SHIRE COUNCIL 2 Contents LIST OF TABLES ...................................................................................................................... 4 LIST OF GRAPHS.................................................................................................................... 5 THE 2008 LOCAL GOVERNMENT ELECTIONS ....................................................................... 8 2008 INVERELL SHIRE COUNCIL ELECTIONS ...................................................................... 15 ELECTION PREPARATION.................................................................................................... 19 CONDUCT OF THE ELECTIONS ........................................................................................... 38 ELECTION CONCLUSION.................................................................................................... 67 FUTURE DIRECTION ............................................................................................................. 80 APPENDICES...................................................................................................................... -

Tweed Shire Council Report 2008 Local Government Elections

Tweed Shire Council Report 2008 Local Government Elections REPORT ON THE 2008 LOCAL GOVERNMENT ELECTIONS TWEED SHIRE COUNCIL General Manager Tweed Shire Council PO Box 816 Murwillumbah NSW 2484 Dear General Manager I am pleased to present to you a report on the conduct and administration of the 2008 Local Government Elections held for Tweed Shire Council. Yours sincerely Colin Barry Electoral Commissioner 31 August 2009 REPORT ON THE 2008 LOCAL GOVERNMENT ELECTIONS TWEED SHIRE COUNCIL 2 Contents LIST OF TABLES ...................................................................................................................... 4 LIST OF GRAPHS.................................................................................................................... 5 THE 2008 LOCAL GOVERNMENT ELECTIONS ....................................................................... 8 2008 TWEED SHIRE COUNCIL ELECTIONS .......................................................................... 15 ELECTION PREPARATION.................................................................................................... 18 CONDUCT OF THE ELECTIONS ........................................................................................... 37 ELECTION CONCLUSION.................................................................................................... 66 FUTURE DIRECTION ............................................................................................................. 79 APPENDICES...................................................................................................................... -

Local Plumbing Regulators in NSW On-Site Plumbing and Drainage Compliance and Inspections

Local plumbing regulators in NSW On-site plumbing and drainage compliance and inspections This document outlines who performs the functions of the plumbing regulator in NSW. Under the Plumbing and Drainage Act 2011 NSW Fair Trading is the plumbing regulator in New South Wales. The Plumbing Code of Australia is the technical standard for compliance throughout NSW. It is the responsibility of the plumbing regulator in each area to set requirements for inspections of on-site plumbing and drainage. Fair Trading’s area of operation includes all areas in which properties are provided with services (either drinking water, recycled water or a sewerage service) by Sydney Water Corporation or Hunter Water Corporation. This area of operation stretches from Gerringong in the south (the Illawarra), to Newcastle, Port Stephens and Dungog in the north (the Hunter), and west to Mount Victoria (Blue Mountains). The function of the plumbing regulator has been delegated by Fair Trading to local councils, county councils, or other qualified bodies. The delegation of the function has been accepted by local and county councils across NSW, with a small number of exceptions where the council declined the delegation. Below are two tables identifying the local authority for plumbing regulator functions, including conducting inspections, throughout NSW by local government area. Please Note: Onsite plumbing and drainage work does not include stormwater, fire suppression; work on network utility assets or roof plumbing. If you are a plumber or drainer in regional -

Councils and Utilities

Page 1 Councils and Utilities Local Government Authorities Albury City Council: www.alburycity.nsw.gov.au Armidale Regional Council: www.armidaleregional.nsw.gov.au Ballina Shire Council: www.ballina.nsw.gov.au Balranald Shire Council: www.balranald.nsw.gov.au Bathurst Regional Council: www.bathurst.nsw.gov.au Bayside Council: www.bayside.nsw.gov.au Bega Valley Shire Council: www.begavalley.nsw.gov.au Bellingen Shire Council: www.bellingen.nsw.gov.au Berrigan Shire Council: www.berriganshire.nsw.gov.au Blacktown City Council: www.blacktown.nsw.gov.au Bland Shire Council: www.blandshire.nsw.gov.au Blayney Shire Council: www.blayney.nsw.gov.au Blue Mountains City Council: www.bmcc.nsw.gov.au Bogan Shire Council: www.bogan.nsw.gov.au Bourke, the Council of the Shire: www.bourke.nsw.gov.au Brewarrina Shire Council: www.brewarrina.nsw.gov.au Broken Hill City Council: www.brokenhill.nsw.gov.au Burwood Council: www.burwood.nsw.gov.au Law Diary Councils and Utilities Directory | 2021 Page 2 Byron Shire Council: www.byron.nsw.gov.au Cabonne Council: www.cabonne.nsw.gov.au Camden Council: www.camden.nsw.gov.au Campbelltown City Council: www.campbelltown.nsw.gov.au Canada Bay Council, City of: www.canadabay.nsw.gov.au Canterbury-Bankstown City Council: www.cbcity.nsw.gov.au Carrathool Shire Council: www.carrathool.nsw.gov.au Central Coast Council: www.centralcoast.nsw.gov.au Central Darling Shire Council: www.centraldarling.nsw.gov.au Cessnock City Council: www.cessnock.nsw.gov.au Clarence Valley Council: www.clarence.nsw.gov.au Cobar Shire Council: -

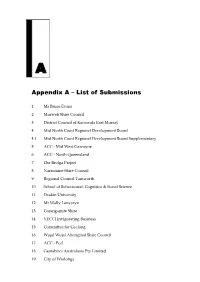

Appendix a – List of Submissions

A Appendix A – List of Submissions 1 Mr Bruce Evans 2 Murweh Shire Council 3 District Council of Karoonda East Murray 4 Mid North Coast Regional Development Board 4.1 Mid North Coast Regional Development Board Supplementary 5 ACC - Mid West Gascoyne 6 ACC - North Queensland 7 The Brolga Project 8 Narromine Shire Council 9 Regional Council Tamworth 10 School of Behavioural, Cognitive & Social Science 11 Deakin University 12 Mr Wally Lenyszyn 13 Corangamite Shire 14 VECCI Invigorating Business 15 Committee for Geelong 16 Wujal Wujal Aboriginal Shire Council 17 ACC - Peel 18 Geofabrics Australasia Pty Limited 19 City of Wodonga 90 THE GLOBAL FINANCIAL CRISIS AND REGIONAL AUSTRALIA 20 Horsham Rural City Council 21 Hughenden Chamber of Commerce Inc. 22 Central Darling Shire 23 Rural City of Wangaratta 24 Southern Cross University 25 Department of Broadband, Communications & the Digital Economy 26 Municipal Association of Victoria 27 Australian Bankers' Association Inc. 28 Southern Cross University 29 Growcom 30 Southern Councils Group 31 Southern Mallee District Council 32 Manningham City Council 33 G21 - Geelong Region Alliance 34 ACC - Illawarra 35 Department of Resources, Energy & Tourism 36 Peel Development Commission 37 Latrobe City Council 38 Shire of Yilgarn 39 City of Albany 40 Glenelg Shire Council 41 National Farmers' Federation 42 RMIT University 43 National Sea Change Taskforce 44 Shire of Strathbogie 45 ACC - Mackay Region 46 Hurstville City Council 47 Qantas Airways Limited APPENDIX A – LIST OF SUBMISSIONS 91 48 Albury City 49 -

Local Council Earthworks Compliance Regulation

1 LOCAL COUNCIL EARTHWORKS COMPLIANCE REGULATION TOP 10 Council Area Form Name Lithgow RSS-PF-001A Mudgee RSS-PF-001A Oberon RSS-PF-001A Baulkham Hills RSS-PF-001A Blayney RSS-PF-001A Orange RSS-PF-001A Dubbo RSS-PF-001A Bathurst RSS-PF-001A Hawkesbury RSS-PF-001Ah Blue Mountains RSS-PF-001Abl Council Area Form Name Albury City Council RSS-PF-001A Armidale Regional Council RSS-PF-001A Ballina Shire Council RSS-PF-001A Balranald Shire Council RSS-PF-001A Bathurst Regional Council RSS-PF-001A Bayside Council RSS-PF-001A Bega Valley Shire Council RSS-PF-001A Bellingen Shire Council RSS-PF-001A Berrigan Shire Council RSS-PF-001A Blacktown City Council RSS-PF-001A Bland Shire Council RSS-PF-001A Blayney Shire Council RSS-PF-001A Blue Mountains City Council RSS-PF-001A Bogan Shire Council RSS-PF-001A Bourke Shire Council RSS-PF-001A Brewarrina Shire Council RSS-PF-001A Broken Hill City Council RSS-PF-001A Burwood Council RSS-PF-001A Byron Shire Council RSS-PF-001A Cabonne Council RSS-PF-001A Camden Council RSS-PF-001A Campbelltown City Council RSS-PF-001A Canterbury-Bankstown Council RSS-PF-001A Carrathool Shire Council RSS-PF-001A Central Coast Council RSS-PF-001A Central Darling Shire Council RSS-PF-001A Cessnock City Council RSS-PF-001A City of Canada Bay Council RSS-PF-001A City of Parramatta Council RSS-PF-001A 2 City of Ryde Council RSS-PF-001A City of Sydney Council RSS-PF-001A Clarence Valley Council RSS-PF-001A Cobar Shire Council RSS-PF-001A Coffs Harbour City Council RSS-PF-001A Coolamon Shire Council RSS-PF-001A Coonamble Shire -

Glen Innes Severn Council Report 2008 Local Government Elections

Glen Innes Severn Council Report 2008 Local Government Elections REPORT ON THE 2008 LOCAL GOVERNMENT ELECTIONS GLEN INNES SEVERN COUNCIL General Manager Glen Innes Severn Council PO Box 61 Glen Innes NSW 2370 Dear General Manager I am pleased to present to you a report on the conduct and administration of the 2008 Local Government Elections held for Glen Innes Severn Council. Yours sincerely Colin Barry Electoral Commissioner 31 August 2009 REPORT ON THE 2008 LOCAL GOVERNMENT ELECTIONS GLEN INNES SEVERN COUNCIL 2 Contents LIST OF TABLES ...................................................................................................................... 4 LIST OF GRAPHS.................................................................................................................... 5 THE 2008 LOCAL GOVERNMENT ELECTIONS ....................................................................... 8 2008 GLEN INNES SEVERN COUNCIL ELECTIONS.............................................................. 15 ELECTION PREPARATION.................................................................................................... 18 CONDUCT OF THE ELECTIONS ........................................................................................... 37 ELECTION CONCLUSION.................................................................................................... 66 FUTURE DIRECTION ............................................................................................................. 79 APPENDICES...................................................................................................................... -

DISABILITY INCLUSION ACTION PLANS Progress Reports NSW Local Councils 2019-2020

DISABILITY INCLUSION ACTION PLANS Progress Reports NSW Local Councils 2019-2020 1 [ Page left intentionally blank ] 2 Contents AlburyCity Council 7 Armidale Regional Council 7 Ballina Shire Council 8 Balranald Shire Council 9 Bathurst Regional Council 9 Bayside Council 10 Bega Valley Shire Council 11 Bellingen Shire Council 15 Berrigan Shire Council 17 Blacktown City Council 18 Bland Shire Council 21 Blayney Shire Council 23 Blue Mountains City Council 24 Bogan Shire Council 27 Bourke Shire Council 27 Brewarrina Shire Council 28 Broken Hill Council 29 Burwood Council 31 Byron Shire Council 31 Cabonne Council 32 Camden Council 32 Campbelltown City Council 33 Canterbury Bankstown Council 37 Carrathool Shire Council 38 Central Coast Council 39 Central Darling Shire Council 41 Cessnock City Council 41 City of Canada Bay 43 City of Newcastle Council 44 City of Parramatta Council 47 City of Ryde Council 48 City of Sydney Council 51 Clarence Valley Council 67 Cobar Shire Council 68 Council progress updates have been Coffs Harbour City Council 69 extracted from Council Annual Re- ports, either in the body of the Annual Coolamon Shire Council 71 Report or from the attached DIAP, Coonamble Shire Council 72 or from progress updates provided Cootamundra Gundagai Regional Council 71 directly via the Communities and Cowra Shire Council 73 Justice Disability Inclusion Planning Cumberland City Council 73 mailboxes. Dubbo Regional Council 78 Dungog Shire Council 82 3 Edward River Council 83 Narrabri Shire Council 147 Eurobodalla Shire Council 83 Narrandera -

Local Council and Road Authority Contact Numbers Australian Capital Territory

5 April 2019 Local council and road authority contact numbers Australian Capital Territory Code Council Name Generic Contact Number Section (if listed) Territory and Municipal Services RMACT1 13 22 81 Directorate l New South Wales Code Council Name Generic Contact Number Section (if listed) NSW171 Albury City Council (02) 6023 8111 NSW324 Armidale Council 1300 136 833 NSW187 Ballina Shire Council 1300 864 444 or (02) 6686 1209 Works Supervisor NSW278 Balranald Shire Council (03) 5020 1300 (still NSW Council) NSW235 Bathurst City Council (02) 6333 6111 NSW335 Bayside Council 1300 581 299 NSW228 Bega Valley Shire Council (02) 6499 2222 NSW160 Bellingen Shire Council (02) 6655 7300 NSW170 Berrigan Shire Council (03) 5888 5100 (still NSW Council) NSW283 Blacktown City Council (02) 9839 6000 NSW256 Bland Shire Council (02) 6972 2266 NSW173 Blayney Shire Council (02) 6368 2104 Engineering/Roads NSW248 Blue Mountains City Council (02) 4723 5000 or (02) 4780 5000 Road work and NSW291 Bogan Shire Council (02) 6835 9000 Maintenance NSW165 Bourke Shire Council (02) 6830 8000 NSW302 Brewarrina Shire Council (02) 6830 5100 NSW231 Broken Hill City Council (08) 8080 3300 (still NSW Council) NSW268 Burwood Council (02) 9911 9911 NSW194 Byron Shire Council (02) 6626 7000 or 1300 811 942 NSW239 Cabonne Shire Council (02) 6392 3200 NSW264 Camden Council (02) 4654 7777 NSW272 Campbelltown City Council (02) 4645 4000 NSW282 Canada Bay Council (02) 9911 6555 www.nhvr.gov.au 1 of 16 Local council and road authority contact numbers Code Council Name Generic -

Central Darling Shire Is Particularly Interested in Providing Input to Your Inquiry, Given That the GFC Is Beginning to Impact Significantly on Our Economy

Central SUBMISSION 22 Darling Shire Vast lands. Rich heritage. Diverse culture. 23rd March 2009 House Standing Committee on Infrastructure, Transport, Regional Development and Local Government House of Representatives Parliament House CANBERRA ACT 2600 Dear Committee members, Inquiry into the impact of the global financial crisis on regional Australia Central Darling Shire is particularly interested in providing input to your inquiry, given that the GFC is beginning to impact significantly on our economy. Our discussions with local councils in other remote regions suggest we are not alone. We would like to highlight some of the steps we are taking to advance our economic and social standing, and how the Commonwealth Government might improve our efforts to respond to the GFC and other economic and social shocks in the future. We also wish to invite your Committee to visit us, so that you can understand the issues first- hand. Background The Central Darling Shire is located in the Far West of NSW. The shire is the largest in the state, but with a population of only 2,000 or thereabouts, of which 50 per cent are Indigenous. Its distinguishing features are the Darling River and the Menindee Lakes, and four towns that are the quintessential Outback. Most Australians can relate to these places even if they haven't visited - Wilcannia (administrative centre), Menindee (horticultural crops), White Cliffs (opal mining) and Ivanhoe (Indian Pacific rail stop and rural service centre). Economic, social and environmental hardship is not new to us - the shire has been drought declared for over 8 years, river flows are irregular, the population is ageing, job creation is minimal and there is chronic unemployment, especially among the Indigenous population. -

BF Lead Agencies by Area Covered and LGA September 2017 Docx

Brighter Futures funded services: Lead agencies by areas covered and local government areas Service Provider Areas covered Local Government Areas (LGA) SDN CHILD AND FAMILY Ashfield, Botany, Burwood, Canada Bay, Canterbury, City of Sydney, Woollahra Council, City of Botany Bay, City of SERVICES INC Hurstville, Kogarah, Leichhardt, Marrickville, Randwick, Randwick, Inner West Council, Waverley Council, Rockdale, Strathfield, Sutherland, Sydney, Waverley, Burwood Council, Strathfield Council, Canada Bay Council, Woollahra Inner West Council, Canterbury-Bankstown Council, Sutherland Shire, City of Hurstville, Bayside Council, Georges River Council THE BENEVOLENT Hornsby, Hunters Hill, Ku-ring-gai, Lane Cove, Manly, Hornsby Shire, Hunters Hill Council, Ku-ring-gai Council, Lane SOCIETY Mosman, North Sydney, Pittwater, Ryde, Warringah, Cove Council, Northern Beaches Council, Mosman Council, Willoughby North Sydney Council, City of Ryde, City of Willoughby South West Sydney THARAWAL ABORIGINAL Campbelltown, Camden, Wingecarribee, Wollondilly City of Campbelltown, Camden Council, Wollondilly Shire, CORPORATION Wingecarribee Shire THE BENEVOLENT Bankstown, Fairfield, Liverpool City of Liverpool , City of Fairfield , Canterbury-Bankstown SOCIETY Council UNITING Campbelltown, Camden, Wingecarribee, Wollondilly City of Campbelltown, Camden Council, Wollondilly Shire, Wingecarribee Shire KARI ABORIGINAL Liverpool, Fairfield and Bankstown City of Liverpool , City of Fairfield , Canterbury-Bankstown RESOURCES INC Council METRO MIGRANT Bankstown, Fairfield -

Pollution Incident Response Management Plan – (Pirmp)

Version: January 2021 POLLUTION INCIDENT RESPONSE MANAGEMENT PLAN – (PIRMP) Cleanaway Daniels NSW Pty Ltd (Formerly Sterihealth NSW Pty Ltd) Waste Transporter EPA LICENCE NO. 6156 Industry is now required to report pollution incidents immediately to ALL regulatory bodies listed below. Call 000 if the incident presents an immediate threat or potential immediate threat to human health, the environment or property. If the incident does not require an initial combat agency, or once the 000 call has been made, notify the Branch Manager / Operation Manager / Operations Coordinator / Transport Supervisor relevant to your site (see Section 4.1-4.4) who shall then contact the remaining authorities: Environment Protection Authority 131 555 Safe Work NSW 13 10 50 Comcare 1300 366 979 For list of Local Councils see Appendix Local Council A For list of Public Health Units see The NSW Ministry of Health Appendix B Fire and Rescue 000 Fire and Rescue without immediate 1300 729 579 threat Also call CWY Spill response 1800 SPILLS (1800 774 557), if appropriate / assistance is required. Page 1 of 17 Uncontrolled document when printed Version: January 2021 Revision Status: Date Issue By Checked Approved 0 Previous Versions 14/10/2020 A Haydn Rossback Bart Downe - 11/01/2021 1 - CWD Business CWD Business Page 2 of 17 Uncontrolled document when printed Version: January 2021 1.0 INTRODUCTION The Pollution Incident Response Management Plan (PIRMP) has been developed to assist with the management of pollution incidents which may occur during the transportation of waste by Cleanaway Daniels NSW (Silverwater) and may impact the environment, personnel, or the community in which we operate.