Concept Eindverslag 10-04-2006

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

C ANGELL, Glandwr Street, Gl

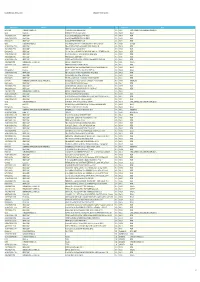

No Redg Chassis Chasstype Body Seats Orig Redg Date Status Operator Livery Location CSANGABER "C ANGELL, Glandwr Street, Glandwr Industrial Estate, Aberbeeg, Blaenau Gwent (0,5,0) FN: C & R Transport PG7402/I G200 RRN Vo B10M-60 020302 VH 13917 C49F G501 CJT Feb-08 J222 CNR Vo B10M-60028692 Pn 9112VCP0492 C48FT J701 CWT Sep-07 H 11 CNR MB 811D 670303-2P-082331 RB C33F 18471 J764 ONK Jun-06 M111 CNR MB 711D WDB6693632N030899 Onyx C24F M 20 TGC N111 CNR MB 814D 670313-2N-027798 Pn C33F 958.5MMY3616 N 98 BHL Aug-05 N125 FFV Fd Tt SFAEXXBDVESS30782 Fd M8 Mar-03 N213 TAX Fd Tt P111 CNR MB 711D R111 CNR Fd Tt WF0EXXGBFE2B39351 Ford M16 WN52 XTO Jun-06 T726 SCN Fd Tt Y162 GBO Fd Tt CSBENGRIF JSB & KE BENNING, 13 East View, GRIFFITHSTOWN, NP4 5DW PG6666/N (0,2,2) FN: B's Travel OC: Unit 18, The Old Cold Stores, Court Road Industrial Estate, Cwmbran, Torfaen, NP44 H315 TWE Mercedes 811D WDB6703032P020867 Ce C16.108 B32F Mar-07 sale 2/08 R222 BST LDV Cy X222 BST MB 311D BU56 AZW Ibs 45C14 ZCFC45A100D315479 Excel 664 M16 Oct-06 CSBOYDNEW "MB CHICK, ISCA Works, Mill Parade, NEWPORT, NP20 2JQ" (0,8,12) FN: Croydon Minibus Hire PG6750/N DXI 84 Scania K113T Irizar C FT P 26 RGO Feb-05 JUI 1716 Vo B10M-53 16728 VH C49FT 13500 (E280HRY) Sep-00 TIL 7205 Kassbohrer S215HD WKK17900001035026 Setra C49FT APA 672Y Jan-07 YAZ 6392 MB 811D 670303-20-815779 Oe C29F 311 (E872EHK/MXX481/E872EHK)Apr-06 A 7 FRX Sca K93CRB 1818346 Pn C53F 9012SFA2221 (H524DVM) Mar-06 sale 4/07 A 8 FRX Sca K93CRB 1818350 Pn 9012SFA2225 C53F (H528DVM) Mar-06 w G 57 KTG Oe MR09 VN2020 -

ANNUAL REPORT 2019 Contents

ANNUAL REPORT 2019 Contents 1. Message from the General Director 2. 2019: A Record Year 3. A Year of Celebrations and Important Milestones 4. At the forefront of technology 5. Irizar Group Sustainability Message from the General Director In March, when the global pandemic was declared, an enormous health crisis of unknown dimensions was confirmed and that lead to an unprecedented economic crisis. We have been working on staying close to our customers these months and ensuring that the people in the Group can keep doing their jobs safely and maintain their delicate work life balance. Likewise, we have given some social support, in accordance with our principles and mission. I am very proud of the behaviour of every person in the Group and the attitude of union and solidarity with which we are facing these difficult times. However, this annual report for 2019 should let us recognise the goal we are aspiring to. 2019 was the year we celebrated the 130th anniversary of Irizar. It has also been ten years since we had our own stand at the Busworld fair for the first time. And we are celebrating the 20th anniversary of Irizar Mexico, the 10th anniversary of Datik and it has been ten years since we became a manufacturer of integral coaches. The Group currently has 13 production plants, 8 brands of its own, an R&D centre and 8 distribution and Without a doubt, the success of the Group is an outcome of the strategy based on brand, technology and after-sales companies. We have activities in six different sectors, including passenger transport, electro-mo- sustainability. -

Winter 2021 Plus

WINTER 2021 PLUS. PLUS Winter 2021 1 Front Cover: TasPort’s new D9T Dozer at WELCOME the Burnie chip export terminal Welcome to the Winter 2021 edition of PLUS magazine. investment in our Clayton head office (just as we’ve finished technology group within William Adams is helping VICTORIA TASMANIA one upgrade, we’re planning the next…). Plans are afoot to customers take advantage of everything that Cat machines After last year’s lockdowns, I’m relieved to be writing add new workshop facilities, including both a Component have got on board. Among the biggest technological this letter from our head office in Clayton, which is now Rebuild Centre (CRC) and a new Central Distribution Centre developments are the new machines’ 3D capabilities, which CLAYTON HORSHAM BENDIGO GEELONG LAUNCESTON 81-83 Dimboola Road 11A Trantara Court Cnr Fyans & Crown Street 308 George Town Road operating at 100 percent capacity – and it’s great to be (CDC), for our parts operation. allow operators to dig accurately to their designs, allowing (HEAD OFFICE) Horsham VIC 3400 East Bendigo VIC 3550 Geelong South VIC 3220 Rocherlea TAS 7248 back. Our William Adams team adapted quickly and for greater safety and productivity. 17-55 Nantilla Road (03) 5362 4100 (03) 5434 2140 (03) 5223 5200 (03) 6325 0900 successfully to remote working last year, but nothing beats The CRC will be a state-of-the-art facility where we can Clayton VIC 3168 the ability to meet face-to-face with colleagues and, of centralise the rebuilding of machine components like If you’re keen to know more about Cat’s industry-leading (03) 9566 0666 course, being able to welcome our valued customers back engines, transmissions, power trains and final drives, and tech, we’ll be holding our William Adams Cat Live festival HOBART on site. -

Truck 45.0.0

IDC5 software update TRUCK 45.0.0 TEXA S.p.A. Via 1 Maggio, 9 31050 Monastier di Treviso Treviso - ITALY Tel. +39 0422 791311 Fax +39 0422 791300 www.texa.com - [email protected] IDC5 TRUCK software update 45.0.0 The new diagnostic features included in the all mechanics the opportunity to use diagnostic IDC5 TRUCK update 45 allow working on a large tools that are always updated and state-of-the- number of vehicles that belong to makes of the art, to operate successfully on the vast majority most popular manufacturers. The work TEXA’s of vehicles on the road. developers carried out on industrial vehicles, The TRUCK update 45 also offers new, very useful light commercial vehicles and buses guarantees Wiring Diagrams and DASHBOARDs. WORLDWIDE MARKET CHEVROLET / ISUZU: • Instrumentation. • The new model D-MAX [02>] 2.5 TD was • The new model Berlingo M59 engine1.6i 16V developed with the following systems: Flex Kat was developed with the • ABS; following systems: • Airbag; • ABS; • Body computer; • Airbag; • Immobiliser; • Anti-theft system; • Diesel injection; • Radio; • Transfer case; • Body computer; • Service warning light. • Door locking; • Multi-function display; CITROËN: • Immobiliser; • The new model Berlingo [14>] (B9e) EV was • Flex Fuel injection; developed with the following systems: • CD multiplayer; • ABS; • Auxiliary heating; • Anti-theft system; • Instrumentation. • Airbag; • Body computer; COBUS: • A/C system; • The new model Series 2000 & 3000 Euro 3 - • Comfort system; EM3 was developed with the following systems: • Emergency call; • Automatic transmission; • Multi-function display; • Diesel injection; • Steering column switch unit; • Network system; • Trailer control unit; • Motor vehicle control; • Hands-free system; • Instrumentation; • CD multiplayer; • Tachograph. -

Study of the Sales-To-Delivery Process for Complete Buses and Coaches

Study of the Sales-to-Delivery Process for Complete Buses and Coaches at Scania CV Anna Elmgren and Anna-Josefina Mattmann Department of Industrial Management and Logistics Division of Production Management Lund Institute of Technology Lund University Foreword With this master thesis we terminate our studies at the Industrial Management and Engineering programme at Lund Institute of Technology. The thesis comprises twenty academic points, and is commissioned by Scania CV AB in Södertälje. It is performed in collaboration with the division of Production Management within the Department of Industrial Management and Logistics at Lund Institute of Technology. We would like to thank our tutor at Scania CV AB, Anders Dewoon, for his support and feedback during our work with this thesis, as well as the rest of the staff at the B department for welcoming and helping us. We would also like to thank the rest of the staff, in Södertälje as well as at the sales companies, that we have come in contact with during our work. We also thank Irizar and Omni for receiving us with kindness and answering our questions. Finally we would like to thank our tutor at Lund Institute of Technology, Bertil I Nilsson, for supporting us with an optimistic attitude throughout our work, and for giving us valuable feedback. Anna Elmgren Anna-Josefina Mattmann Stockholm, the 28th of May 2004 III Abstract Title: Study of the sales-to-delivery process for complete buses and coaches at Scania CV. Authors: Anna Elmgren and Anna-Josefina Mattmann. Tutors: Anders Dewoon, BD department at Scania CV, and Bertil I Nilsson, lecturer at Lund Institute of Technology. -

Rába Éves Jelentés, 2016

ANNUAL REPORT 2016 ÉVES JELENTÉS Breakdown of sales revenue by geographic region (million EUR) Table of contents Tartalomjegyzék Az árbevétel alakulása földrajzi régiók szerint (millió EUR) Financial statements (2012–2016) 4 Pénzügyi adatok (2012–2016) USA EU HUNGARY/BELFÖLD CIS/FÁK CEO’s assessment of the year 6 Vezérigazgatói évértékelő • John Deere • Scania • Volán companies • KAMAZ • Marmon-Herrington • Claas Volán társaságok • GAZ Growth, innovation, efficiency 8 Növekedés, innováció, hatékonyság • Meritor • Hamm AG. • Suzuki • Fehrer • Ministry of Defence Rába Automotive Holding Plc. 10 Rába Járműipari Holding Nyrt. • NAF Honvédelmi Minisztérium • BPW Axle Business Unit 12 Futómű üzletág Automotive Compontents Business Unit 22 Alkatrész üzletág Vehicle Business Unit 30 Jármű üzletág 6 Elements of success – 38 A siker építőkövei – innovation, quality, expertise innováció, szaktudás, minőség 63 52 Rába Development Institute – 40 Rába Fejlesztési Intézet (RFI) – 10 an efficient R+D base A hatékony K+F bázis 6 HR – training and retention of specialists 44 HR – Szakemberképzés és -megtartás Quality assurance – efficiency programs 50 Minőségbiztosítás – Hatékonysági programok Environmental awareness, environmental strategy 54 Környezettudatosság, környezeti stratégia Property management – 58 Ingatlangazdálkodás – investments into energy efficiency energiahatékonysági fejlesztések Financial statement 60 Pénzügyi értékelés ÁZSIA ASIA USA 10 USA EU 63 EU HUNGARY 52 BELFÖLD CIS 6 FÁK ASIA 6 ÁZSIA Győr Total in 2016: EUR 137 million EUR* MÓR SÁRVÁR * Összesen 2016: 137 millió euró Production sites / Telephelyeink: Győr, SÁRVÁR, MÓR „The basis of the data is the summary consolidated statement of comprehensive income, calculated using the HUF/EUR exchange rate as of 31 December 2016.” „Az adat alapja az összesített konszolidált átfogó jövedelemre vonatkozó kimutatás, 2016. -

Katalog Ventila I Senzora Ka Tire BH

KA TIRE BH Sarajevo KATALOGventila i senzora za kamione, autobuse i prikolice www.katirebh.com Pronađite sve što vam je potrebno od ventila i senzora vrhunske izrade namijenjenim kamionskom, autobuskom i prikoličnom programu vodećih svjetskih proizvođača. Konkurentne cijene sa robom na stanju i garancijom od 12 mjeseci. 2 VENTILI KA1710 UNIVERZALNI ISUŠIVAČ ZRAKA KA1711 UNIVERZALNI ISUŠIVAČ ZRAKA 12.5 ± 0.2bar cut-off pressure 8.5 ± 0.2 bar Snap-on exhaust Cross Ref. 4324101130 Cross Ref. 4324100410 4324101110 432410 1020 Application MAN 81521026097 Application MERCEDES A0004318815 DAF 1517967 225,00 KM + PDV 225,00 KM + PDV NA STANJU NA STANJU REGULATOR PRITISKA RL3511AZ-AD ISUŠIVAČ ZRAKA KA2009 M22x1.5. Cut-off pressure 8.1 bar No Heater. Snap-on exhaust With Tyre inflation port Cross Ref. 9753034740 Cross Ref. 4324200020 Application MERCEDES 0024314606 Application MERCEDES 0004313615 DAF VOLVO IVECO NEOPLAN NA STANJU 225,00 KM + PDV 84,00 KM + PDV NA STANJU KA3800 VENTIL REGULACIJE PRITISKA KA3802 VENTIL REGULACIJE PRITISKA 4750103170 Cross Ref. 4750104000 Cross Ref. Application Application DAF 95XF DAF MAN 81521016286 MAN MERCEDES MERCEDES NA STANJU NA STANJU 105,00 KM + PDV arajevo95,00 KM + PDV S RL3512BJ VENTIL REGULACIJE PRITISKA RL3512AB VENTIL REGULACIJE PRITISKA Port 1, 21:M22x1.5 Port 22: M12x1.5 Cross Ref. 9753001100 9753034730 Cross Ref. 9753034470 Application MERCEDES, FAP, 9753034730 KA TIRE BHDAF, MAN, IVECO, Application MERCEDES RVI, VOLVO NA STANJU NA STANJU 105,00 KM + PDV 105,00 KM + PDV 3 VENTILI REGULACIONI VENTIL OPTEREĆENJA RL3512MA03 VENTIL REGULACIJE PRITISKA RL3523AB-C Control stroke 60 M22x1.5Voss Pressure output (10.0 ± 0.3) bar M16x1.5Voss Pressure input 12.5 bar Cross Ref. -

Adressverzeichnis

ADRESSVERZEICHNIS ANHÄNGER & AUFBAUTEN . .Seite 11–13 BUSSE. .Seite 13–16 LKW und TRANSPORTER . .Seite 16–19 SPEZIALFAHRZEUGE . .Seite 19–22 ANHÄNGER & Aebi Schmidt ALF Fahrzeugbau Andreoli Rimorchi S.r.l. Deutschland GmbH GmbH & Co.KG Via dell‘industria 17 AUFBAUTEN Albtalstraße 36 Gewerbehof 12 37060, Buttapietra (Verona) 79837 St. Blasien 59368 Werne ITALIEN Acerbi Veicoli Industriali S.p.A. Tel. +49.7672-412-0 Tel. +49.2389 98 48-0 Tel. +39 045 666 02 44 Strada per Pontecurone, 7 www.aebi-schmidt.com www.alf-fahrzeugbau.de www.andreoli-ribaltabili.it 15053 Castelnuovo Scrivia (AL) ITALIEN Agados spol. s.r.o. ALHU Fahrzeugtechnik GmbH Andres www.acerbi.it Rumyslová 2081 Borstelweg 22 Hermann Andres AG 59401 Velké Mezirici 25436 Tornesch Industriering 42 Achleitner Fahrzeugbau TSCHECHIEN Tel. +49.4122 - 90 67 00 3250 Lyss Innsbrucker Straße 94 Tel. +420 566 653 311 www.alhu.de SCHWEIZ 6300 Wörgl www.agados.cz Tel. +41 32 387 31 61 Asch- ÖSTERREICH AL-KO www.andres-lyss.ch wege & Tönjes Aucar- Tel. +43 5332-7811-0 Agados Anhänger Handels Alois Kober GmbH Zur Schlagge 17 Trailer SL www.achleitner.com GmbH Ichenhauser Str. 14 Annaburger Nutzfahrzeuge 49681 Garrel Pintor Pau Roig 41 2-3 Schwedter Str. 20a 89359 Kötz GmbH Tel. +49.4474-8900-0 08330 Premià de mar, Barcelona Ackermann Aufbauten & 16287 Schöneberg Tel. +49.8221-97-449 Torgauer Straße 2 www.aschwege-toenjes.de SPANIEN Fahrzeugvertrieb GmbH Tel. +49.33335 42811 www.al-ko.de 06925 Annaburg Tel. +34 93 752 42 82 Am Wallersteig 4 www.agados.de Tel. +49.35385-709-0 ASM – Equipamentos www.aucartrailer.com 87700 Memmingen-Steinheim Altinordu Trailer www.annaburger.de de Transporte, S Tel. -

Triplex Windscreen for Buses

LAMITEX CATALOGUE * If you can`t find your bus model - contact us, our company can produce any windscreen on your size Height Width Code Brand and Model (mm) (mm) AJOKKI 873 Ajokki 5000 left 1144 1350 874 Ajokki 5000 right 1144 1350 809 Ajokki 5300 / Delta 200-300 / MAN 333/334 Magirus / MB O307 / WIIMA left 1075 1276 810 Ajokki 5300 / Delta 200-300 / MAN 333/334 Magirus / MB O307 / WIIMA right 1075 1276 1081 Ajokki 6000 left 1220 1410 1082 Ajokki 6000 right 1220 1410 7039 Ajokki 7000 left 1172 1404 7040 Ajokki 7000 right 1172 1404 1171 Ajokki City left / VÖV 1138 1277 1172 Ajokki City right / VÖV 1138 1277 1445 Ajokki Express left 1540 1290 1446 Ajokki Express right 1540 1290 7147 Ajokki Royal 1756 2435 7024 Ajokki Royal left 1755 1210 7025 Ajokki Royal right 1755 1210 1634 Ajokki Victor / Carrus 50 1552 2412 7407 Ajokki Victor / Carrus 50 left 1552 1201 7408 Ajokki Victor / Carrus 50 right 1552 1201 7242 Ajokki Vector 1655 2480 1188 Ajokki Apollo / Delta Star 1429 2518 ARNA 7175 Arna 1005 2535 7245 Arna 1127 2457 AUTOSAN 7392 Autosan 1232 2510 7366 Autosan A0808T Gemini 1716 2435 7418 Autosan A0909L Tramp 1130 2680 7385 Autosan H7-10 Traper 1230 2367 7379 Autosan Lider 1221 2616 7530 Autosan A8V Wetlina 1446 2182 BERKHOF 7026 Berkhof Excellence 2000 lower 1065 2732 7092 Berkhof Excellence 2000 HL upper 1073 2608 7118 Berkhof Excellence 1000 LD 1750 2740 7167 Berkhof Emperor lower 1147 2766 7140 Berkhof Esprite 1598 2630 7246 Berkhof Everest lower 1144 2730 7276 Berkhof 500 1530 2704 7395 Berkhof / Volvo 1640 1994 7444 Berkhoff / DAF -

2011 Parciales Y Wvta.Xlsx

Ministerio de Industria, Comercio y Turismo Homologaciones Parciales y WVTA 2011 Nº Homologación Fabricante Tipo ST Nº Informe ST Marcas E9 66R-018469 CARROCERA CASTROSUA, S.A. CS-40 MAGNUS L-10,750 s/ MAN B.2007.46.003 INSIA 11IA0861 CARSA; CASTROSUA CARSA; CARROCERA CASTROSUA, S.A. 022113 BEULAS, S.A. R107-Man-B.2007.46.002-Glory-2 pisos bast. MAN INSIA 11IA0874 BEULAS e9*97/27*2003/19*2158*05 IRIZAR S. COOP. i62 var. i621335 bast. MERCEDES BENZ 634 01 o HTAE 05 INSIA 11IA0877 IRIZAR e9*2001/85*2001/85*2169*05 IRIZAR S. COOP. i62 var. i621335 bast. MERCEDES BENZ 634 01 o HTAE 05 INSIA 11IA0878 IRIZAR E9 66R-018452 Ext. II IRIZAR S. COOP. i6-13,35 s/ MERCEDES BENZ HTAE 05 o 634 01 INSIA 11IA0906 IRIZAR 002146 CALDERERIA DE PABLOS, S.A. NPR75 chasis ISUZU, NPR75 var. NPR75HSM d.c. ISUZU NPR75-V cisterna HIDROCAR-215 INSIA 11IA0926 DE PABLOS e9*2001/85*2001/85*2177*10 IRIZAR S. COOP. PB3 var. PB31537R d.c. PB 15.37 bast. SCANIA M335, 13B6X2E, 9B6X2E d.c. ..EB.. INSIA 11IA0948 IRIZAR e9*97/27*2003/19*2166*10 IRIZAR S. COOP. PB3 M335 var. PB31537R K6X2 EB d.c. PB 15.37 INSIA 11IA0947 IRIZAR E9 66R-008318 Ext. II IRIZAR S. COOP. Century var. NCentury 12.85 s/ MAN R33 D26, R33 D20, B.2007.46.001 d.c. 18.??0 RATIO/EEV, 18.xxx HOC INSIA 11IA0888 IRIZAR e9*2001/85*2001/85*2154*13 IRIZAR S. COOP. i62 var. -

2015 Homologación Nacional De Tipo.Xlsx

Ministerio de Industria, Comercio y Turismo 2015 Homologación Nacional de Tipo C. Homologación Fabricante Tipo ST Nº Acta ST Marcas e9*NKS*1064*00 TOMELLOSO CISTERNAS, S.L. TO-3 INTA V1105607 TOMCISA MAA-0549*00 BOBCAT COMPANY AEFB INTA 09CTMA0044 BOBCAT MAA-0447*00 BOBCAT COMPANY A2G8 INTA 07CTMA0037 BOBCAT MAA-0566*00 DIECI, S.R.L. TR45190 INTA 10CTMA0037 BOBCAT MAA-0565*00 DIECI, S.R.L. TR35160 INTA 10CTMA0036 BOBCAT MAA-0447*01 BOBCAT COMPANY A2G8 INTA 07CTMA0037-I BOBCAT MAA-0447*02 BOBCAT COMPANY A2G8 INTA 07CTMA0037-II BOBCAT MAA-0447*03 BOBCAT COMPANY A2G8 INTA 07CTMA0037-III BOBCAT MAA-0447*01 Rev. 01 BOBCAT COMPANY A2G8 INTA 07CTMA0037-I BOBCAT e9*NKS*2005*00 CARROCERA CASTROSUA, S.A. CV-MN-A22 INSIA 10IA1960 CASTROSUA CARSA; CARSA; CARROCERA CASTROSUA, S.A. e9*NKS*1096*00 CARROCERA CASTROSUA, S.A. HBCS02 IDIADA CV12100314 CASTROSUA CARSA; CARSA; CARROCERA CASTROSUA, S.A. e9*NKS*1068*00 CARROCERA CASTROSUA, S.A. ST-SK-M324 IDIADA CV12030105 CARSA; CARROCERA CASTROSUA, S.A.; CASTROSUA CARSA e9*NKS*2004*00 CARROCERA CASTROSUA, S.A. CV-V-B9S INSIA 10IA1961 CARSA; CARROCERA CASTROSUA, S.A.; CASTROSUA CARSA e9*NKS*1042*00 CARROCERA CASTROSUA, S.A. CV-V-C40C IDIADA V1110183 CARROCERA CASTROSUA, S.A.; CASTROSUA CARSA; CARSA e9*NKS*0059*00 CARROCERA CASTROSUA, S.A. CV-MNA24 IDIADA V1009426 CARROCERA CASTROSUA, S.A.; CASTROSUA CARSA; CARSA e9*NKS*2004*01 CARROCERA CASTROSUA, S.A. CV-V-B9S INSIA 12IA1732,10IA1961 CARROCERA CASTROSUA, S.A.; CASTROSUA CARSA; CARSA e9*NKS*2005*01 CARROCERA CASTROSUA, S.A. -

Jest Głodny Sukcesu Z Gazem Łatwiej Być „Eko” Solaris

AGILE PUBLISHING www.transporttm.pl & www.vanzabudowcy.pl /2020 1 Elektryczna trójka PSA Lew jest głodny sukcesu Z gazem łatwiej być „eko” Solaris Mobilne przychodnie ładuje akumulatory Wstęp do straconego roku Opatrzność też czasami posługuje się gii, piszemy dalej. Warto jednak zwrócić środkowym palcem, gmatwając ludziom uwagę na istotne różnice w otoczeniu misternie budowane plany. Prezentacja rynkowym obu tych debiutów. najnowszej generacji ciężarówek MAN W 2000 r. Zjednoczona Europa już ze względów technicznych omsknęła się wiedziała, że wkrótce zostanie powięk- z jesieni ub. roku na początek lutego, szona o nowych członków, może gorzej więc jej miejscem musiał być ciepły kraj, zorganizowanych i mniej okrzesanych, ale ot Hiszpania, żeby daleko nie szukać, żądnych sukcesu, także w transporcie. Nie a przede wszystkim nie płynąć! Bo to spodziewała się tylko, że w tej dziedzinie nie był tylko debiut prasowy, lecz kilku- dostanie aż takiego łupnia. MAN był tygodniowe pokazy dla VIP-ów, klientów, już mocno zaangażowany przemysłowo sprzedawców etc., na który zwieziono cały w Polsce, choć raczej nikt nie planował, odbudowująca się po kryzysie. Polska prom złotych MAN-ów TGX z naczepami. że Starachowice zostaną jednym z centrów i kraje bałtyckie, transportowe tygrysy, A zatem Hiszpania i port najlepiej do- autobusowych koncernu, a Niepołomi- musiały przystopować. Dotyczy to także stępny z Morza Północnego? Wybór padł ce jego główną montownią. Ale przede pojazdów dostawczych do 3,5 t, choć tu na Bilbao w Kraju Basków, w czym moż- wszystkim: nawet najczarniejsze scena- możemy zapisać rekordowy wynik: do na upatrywać też polityki gospodarczej, riusze na 2020 r. nie przewidywały, że pełnych 70 tys. zabrakło nam niewiele bo to region szczególny nie tylko ze wzglę- UE zostanie wtedy pomniejszona o duży ponad setki! Po prostu staliśmy się krajem du na niepowtarzalny i niezrozumiały kraj z doskonale rozwiniętą gospodarką z „silnym” rynkiem wewnętrznym.