Acfe Insurance Fraud Handbook

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Excesss Karaoke Master by Artist

XS Master by ARTIST Artist Song Title Artist Song Title (hed) Planet Earth Bartender TOOTIMETOOTIMETOOTIM ? & The Mysterians 96 Tears E 10 Years Beautiful UGH! Wasteland 1999 Man United Squad Lift It High (All About 10,000 Maniacs Candy Everybody Wants Belief) More Than This 2 Chainz Bigger Than You (feat. Drake & Quavo) [clean] Trouble Me I'm Different 100 Proof Aged In Soul Somebody's Been Sleeping I'm Different (explicit) 10cc Donna 2 Chainz & Chris Brown Countdown Dreadlock Holiday 2 Chainz & Kendrick Fuckin' Problems I'm Mandy Fly Me Lamar I'm Not In Love 2 Chainz & Pharrell Feds Watching (explicit) Rubber Bullets 2 Chainz feat Drake No Lie (explicit) Things We Do For Love, 2 Chainz feat Kanye West Birthday Song (explicit) The 2 Evisa Oh La La La Wall Street Shuffle 2 Live Crew Do Wah Diddy Diddy 112 Dance With Me Me So Horny It's Over Now We Want Some Pussy Peaches & Cream 2 Pac California Love U Already Know Changes 112 feat Mase Puff Daddy Only You & Notorious B.I.G. Dear Mama 12 Gauge Dunkie Butt I Get Around 12 Stones We Are One Thugz Mansion 1910 Fruitgum Co. Simon Says Until The End Of Time 1975, The Chocolate 2 Pistols & Ray J You Know Me City, The 2 Pistols & T-Pain & Tay She Got It Dizm Girls (clean) 2 Unlimited No Limits If You're Too Shy (Let Me Know) 20 Fingers Short Dick Man If You're Too Shy (Let Me 21 Savage & Offset &Metro Ghostface Killers Know) Boomin & Travis Scott It's Not Living (If It's Not 21st Century Girls 21st Century Girls With You 2am Club Too Fucked Up To Call It's Not Living (If It's Not 2AM Club Not -

Long-Term Care Insurance Policy

NEW YORK LIFE INSURANCE COMPANY 51 Madison Avenue, New York, NY 10010 New York Life, Long-Term Care Insurance (800) 224-4582 www.newyorklife.com Long-Term Care Insurance Policy FEDERAL TAX-QUALIFIED COVERAGE: THIS CONTRACT FOR LONG-TERM CARE INSURANCE IS INTENDED TO BE A FEDERALLY QUALIFIED LONG-TERM CARE INSURANCE CONTRACT AND MAY QUALIFY YOU FOR FEDERAL AND STATE TAX BENEFITS. THIS POLICY IS AN APPROVED LONG-TERM CARE INSURANCE POLICY UNDER CALIFORNIA LAW AND REGULATIONS. HOWEVER, THE BENEFITS PAYABLE BY THIS POLICY WILL NOT QUALIFY FOR MEDI-CAL ASSET PROTECTION UNDER THE CALIFORNIA PARTNERSHIP FOR LONG-TERM CARE. FOR INFORMATION ABOUT POLICIES AND CERTIFICATES QUALIFYING UNDER THE CALIFORNIA PARTNERSHIP FOR LONG-TERM CARE, CALL THE [HEALTH INSURANCE COUNSELING AND ADVOCACY PROGRAM AT THE TOLL-FREE NUMBER 1 (800) 434-0222. This Policy is a legal contract between You and New York Life Insurance Company (herein called We, Us, and Our). Please read this Policy carefully and in its entirety. It is issued in exchange for Your Application, and payment of required premiums. This is a long-term care insurance policy that covers Nursing Facility Care, Residential Care Facility, and Home and Community Based Care. 30 Day Free Look Period. Please examine Your Policy promptly. Within 30 days after delivery, You can return the Policy by first class United States mail to New York Life Insurance Company. Upon our receipt of Your Policy a full premium refund will be made to You within 30 days of the Policy’s return and coverage will be void from start. PARTICIPATING. -

Illinois Mandatory Insurance Brochure

The Illinois Department of Insurance regulates insur- IF YOU ARE INVOLVED ance companies, agencies and agents. It maintains a IN AN ACCIDENT Consumer Services Division that can answer your questions about auto insurance. If you have questions An accident report form must be filed with the Illinois or wish to file a complaint, please contact: Department of Transportation (IDOT) if damages exceed Mandatory Vehicle $500 or if injuries resulted from the accident. At-fault, Illinois Department of Insurance uninsured motorists are required to pay for damages 320 W. Washington St. they cause or face license plate registration and driver's Springfield, IL 62767-0001 INSURANCE license suspensions. www.state.il.us/ins/ The Secretary of State's office does not maintain insur- ance information for all registered motor vehicles. FOR MORE INFORMATION Insurance information is available only from the motorist involved in the accident or from the report filed with For more information about Illinois’ Mandatory Insur- IDOT. ance Law, please contact: For more information on reporting an accident, please Office of the Secretary of State contact: Mandatory Insurance Division 501 S. Second St. Illinois Department of Transportation 429 Howlett Bldg. Office of Planning and Programming Springfield, IL 62756-7000 Bureau of Data Collections 217-524-4946 2300 S. Dirksen Pkwy. Springfield, IL 62764 217-782-4518 PURCHASING INSURANCE Contact an insurance agent to buy liability insurance for your vehicle. Some companies do not sell insurance to vehicle owners who have been driving uninsured. If you have problems buying insurance, ask your insur- ance agent about the Illinois Automobile Insurance Plan. -

Directors Guild of America, Inc. National Commercial Agreement of 2017

DIRECTORS GUILD OF AMERICA, INC. NATIONAL COMMERCIAL AGREEMENT OF 2017 TABLE OF CONTENTS Page WITNESSETH: 1 ARTICLE 1 RECOGNITION AND GUILD SHOP 1-100 RECOGNITION AND GUILD SHOP 1-101 RECOGNITION 2 1-102 GUILD SHOP 2 1-200 DEFINITIONS 1-201 COMMERCIAL OR TELEVISION COMMERCIAL 4 1-202 GEOGRAPHIC SCOPE OF AGREEMENT 5 1-300 DEFINITIONS OF EMPLOYEES RECOGNIZED 1-301 DIRECTOR 5 1-302 UNIT PRODUCTION MANAGERS 8 1-303 FIRST ASSISTANT DIRECTORS 9 1-304 SECOND ASSISTANT DIRECTORS 10 1-305 EXCLUSIVE JURISDICTION 10 ARTICLE 2 DISPUTES 2-101 DISPUTES 10 2-102 LIQUIDATED DAMAGES 11 2-103 NON-PAYMENT 11 2-104 ACCESS AND EXAMINATION OF BOOKS 11 AND RECORDS ARTICLE 3 PENSION AND HEALTH PLANS 3-101 EMPLOYER PENSION CONTRIBUTIONS 12 3-102 EMPLOYER HEALTH CONTRIBUTIONS 12 i 3-103 LOAN-OUTS 12 3-104 DEFINITION OF SALARY FOR PENSION 13 AND HEALTH CONTRIBUTIONS 3-105 REPORTING CONTRIBUTIONS 14 3-106 TRUST AGREEMENTS 15 3-107 NON-PAYMENT OF PENSION AND HEALTH 15 CONTRIBUTIONS 3-108 ACCESS AND EXAMINATION OF BOOKS 16 RECORDS 3-109 COMMERCIAL INDUSTRY ADMINISTRATIVE FUND 17 ARTICLE 4 MINIMUM SALARIES AND WORKING CONDITIONS OF DIRECTORS 4-101 MINIMUM SALARIES 18 4-102 PREPARATION TIME - DIRECTOR 18 4-103 SIXTH AND SEVENTH DAY, HOLIDAY AND 19 LAYOVER TIME 4-104 HOLIDAYS 19 4-105 SEVERANCE PAY FOR DIRECTORS 20 4-106 DIRECTOR’S PREPARATION, COMPLETION 20 AND TRAVEL TIME 4-107 STARTING DATE 21 4-108 DIRECTOR-CAMERAPERSON 21 4-109 COPY OF SPOT 21 4-110 WORK IN EXCESS OF 18 HOURS 22 4-111 PRODUCTION CENTERS 22 ARTICLE 5 STAFFING, MINIMUM SALARIES AND WORKING CONDITIONS -

The ACLU of Florida Opposes This Bill Because It Is Designed to Further

Alicia Devine/Tallahassee Democrat The ACLU of Florida opposes this bill because it The murders of George Floyd, protesters and the injustices of our is designed to Breonna Taylor, and so many criminal legal system. others at the hands of police further silence, Floridians wishing to exercise their reinvigorated Floridians’ calls for punish, and constitutional rights would have to police reform and accountability. weigh their ability to spend a night criminalize those Millions took to the streets to in jail if the protest is deemed an advocating for exercise their First Amendment “unlawful assembly.” Peaceful racial justice and rights and demand justice. protesters could be arrested and an end to law Under existing law, these peaceful charged with a third-degree felony enforcement’s protests were met with tear gas, for “committing a riot” even if they excessive use of rubber bullets, and mass arrests. didn’t engage in any disorderly and force against Black Under existing law, armed officers violent conduct. in full riot gear repeatedly used and brown people. Floridians need justice – real excessive force against peaceful police accountability and criminal unarmed protesters. justice reform. Florida’s law Florida’s militaristic response enforcement and criminal legal against Black protesters and their system have no shortage of tools to allies demanding racial justice keep the peace and punish violent stands in stark contrast to the actors, and they’ve proven their lackluster, and at times complicit, tendency time and time again to police response we saw to the misapply these tools to punish failed coup by white supremacist Black and brown peaceful terrorists in D.C. -

And I Heard 'Em Say: Listening to the Black Prophetic Cameron J

Claremont Colleges Scholarship @ Claremont Pomona Senior Theses Pomona Student Scholarship 2015 And I Heard 'Em Say: Listening to the Black Prophetic Cameron J. Cook Pomona College Recommended Citation Cook, Cameron J., "And I Heard 'Em Say: Listening to the Black Prophetic" (2015). Pomona Senior Theses. Paper 138. http://scholarship.claremont.edu/pomona_theses/138 This Open Access Senior Thesis is brought to you for free and open access by the Pomona Student Scholarship at Scholarship @ Claremont. It has been accepted for inclusion in Pomona Senior Theses by an authorized administrator of Scholarship @ Claremont. For more information, please contact [email protected]. 1 And I Heard ‘Em Say: Listening to the Black Prophetic Cameron Cook Senior Thesis Class of 2015 Bachelor of Arts A thesis submitted in partial fulfillment of the Bachelor of Arts degree in Religious Studies Pomona College Spring 2015 2 Table of Contents Acknowledgements Chapter One: Introduction, Can You Hear It? Chapter Two: Nina Simone and the Prophetic Blues Chapter Three: Post-Racial Prophet: Kanye West and the Signs of Liberation Chapter Four: Conclusion, Are You Listening? Bibliography 3 Acknowledgments “In those days it was either live with music or die with noise, and we chose rather desperately to live.” Ralph Ellison, Shadow and Act There are too many people I’d like to thank and acknowledge in this section. I suppose I’ll jump right in. Thank you, Professor Darryl Smith, for being my Religious Studies guide and mentor during my time at Pomona. Your influence in my life is failed by words. Thank you, Professor John Seery, for never rebuking my theories, weird as they may be. -

Making the Best of Felony Murder

University at Buffalo School of Law Digital Commons @ University at Buffalo School of Law Journal Articles Faculty Scholarship 2011 Making the Best of Felony Murder Guyora Binder University at Buffalo School of Law Follow this and additional works at: https://digitalcommons.law.buffalo.edu/journal_articles Part of the Criminal Law Commons Recommended Citation Guyora Binder, Making the Best of Felony Murder, 91 B.U. L. Rev. 403 (2011). Available at: https://digitalcommons.law.buffalo.edu/journal_articles/287 This Article is brought to you for free and open access by the Faculty Scholarship at Digital Commons @ University at Buffalo School of Law. It has been accepted for inclusion in Journal Articles by an authorized administrator of Digital Commons @ University at Buffalo School of Law. For more information, please contact [email protected]. ARTICLES MAKING THE BEST OF FELONY MURDER GuYoRA BINDER* INTRODUCTION: THE WORST OF FELONY MURDER ........................................ 404 I. THE PRINCIPLES OF FELONY MURDER LIABILITY ............................... 411 A. The Constructive Interpretationof Legal Principle .................... 411 B. The Development of Felony Murder Liability ............................. 413 C. Objections to Felony Murder ...................................................... 421 1. Theoretical O bjections ........................................................... 422 2. Constitutional Objections ...................................................... 428 D. Felony Murder as a Crime of Dual Culpability ......................... -

Flowers for Algernon.Pdf

SHORT STORY FFlowerslowers fforor AAlgernonlgernon by Daniel Keyes When is knowledge power? When is ignorance bliss? QuickWrite Why might a person hesitate to tell a friend something upsetting? Write down your thoughts. 52 Unit 1 • Collection 1 SKILLS FOCUS Literary Skills Understand subplots and Reader/Writer parallel episodes. Reading Skills Track story events. Notebook Use your RWN to complete the activities for this selection. Vocabulary Subplots and Parallel Episodes A long short story, like the misled (mihs LEHD) v.: fooled; led to believe one that follows, sometimes has a complex plot, a plot that con- something wrong. Joe and Frank misled sists of intertwined stories. A complex plot may include Charlie into believing they were his friends. • subplots—less important plots that are part of the larger story regression (rih GREHSH uhn) n.: return to an earlier or less advanced condition. • parallel episodes—deliberately repeated plot events After its regression, the mouse could no As you read “Flowers for Algernon,” watch for new settings, charac- longer fi nd its way through a maze. ters, or confl icts that are introduced into the story. These may sig- obscure (uhb SKYOOR) v.: hide. He wanted nal that a subplot is beginning. To identify parallel episodes, take to obscure the fact that he was losing his note of similar situations or events that occur in the story. intelligence. Literary Perspectives Apply the literary perspective described deterioration (dih tihr ee uh RAY shuhn) on page 55 as you read this story. n. used as an adj: worsening; declining. Charlie could predict mental deterioration syndromes by using his formula. -

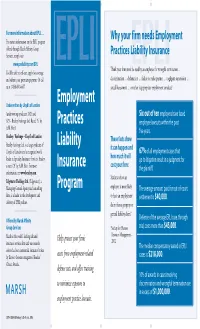

Employment Practices Liability Insurance Program EPLI

B5848_EPLI 2/14/06 2:49 PM Page 1 For more information about EPLI … Why your firm needs Employment For instant information on the EPLI program offered through Marsh Affinity Group Services, simply visit Practices Liability Insurance www.proliablity.com/EPLI Think your firm won’t be sued by an employee for wrongful termination … You’ll be able to self-rate, apply for coverage EPLI EPLI and submit your premium payment. Or call discrimination … defamation … failure to make partner … negligent supervision … us at 1-888-601-6667. sexual harassment … or other inappropriate employment conduct? Underwritten by Lloyd’s of London Employment (underwriting syndicates 2623 and Six out of ten employers have faced 623 – Beazley Furlonge Ltd. Rated “A” by Practices employee lawsuits within the past A.M. Best) five years. Beazley / Furlonge – Lloyd’s of London These facts show Beazley Furlonge Ltd. is a large syndicate of Liability it can happen and Lloyd’s of London and a recognized world 67% of all employment cases that leader in Specialty Insurance Services. Beazley how much it will go to litigation result in a judgment for is rated “A” by A.M. Best. For more Insurance cost your firm: the plaintiff. information, see www.beazley.com. Statistics show an Edgewater Holdings Ltd. (Edgewater), a Managing General Agency and consulting Program employer is more likely The average amount paid for out-of-court firm, is a leader in the development and to have an employment settlement is $40,000. delivery of EPLI policies. claim than a property or general liability claim.* Offered by Marsh Affinity Defense of the average EPLI case, through Group Services *Society for Human trial, costs more than $45,000. -

Motor Vehicle Insurance Fraud and Related Crimes

2017 Statewide Plan of Operation Detection, Prevention, Deterrence, and Reduction of Motor Vehicle Insurance Fraud and Related Crimes COPYRIGHT NOTICE Copyright 2017 by the New York State Division of Criminal Justice Services (DCJS) This publication may be reproduced without the express written permission of DCJS provided that this copyright notice appears on all copies or segments of the publication. The 2017 edition is published on behalf of the New York State Motor Vehicle Theft and Insurance Fraud Prevention by the: New York State Division of Criminal Justice Services Office of Program Development and Funding Alfred E. Smith Office Building 80 South Swan Street Albany, New York 12210 Table of Contents The Statewide Plan of Operation for Motor Vehicle Insurance Fraud Introduction ........................................................................................................... 1 Eligible Programs ................................................................................................. 1 Outline of Statewide Plan ..................................................................................... 1 Part I: Problem Identification of Motor Vehicle Insurance Fraud National Overview ................................................................................................ 3 Statewide Overview .............................................................................................. 3 Part II: Analysis of Motor Vehicle Insurance Fraud in New York State Statewide ............................................................................................................. -

The Go-Giver Ch1.Pdf

The Go-Giver A Little Story About A Powerful Business Idea By Bob Burg and John David Mann Excerpted from The Go-Giver. Published by Portfolio / Penguin. Copyright Bob Burg and John David Mann, 2007-2013. 1: The Go-Getter If there was anyone at the Clason-Hill Trust Corporation who was a go-getter, it was Joe. He worked hard, worked fast, and was headed for the top. At least, that was his plan. Joe was an ambitious young man, aiming for the stars. 4 Still, sometimes it felt as if the harder and faster he worked, the further away his goals appeared. For such a 6 dedicated go-getter, it seemed like he was doing a lot of going but not a lot of getting. 8 Work being as busy as it was, though, Joe didn’t have 9 much time to think about that. Especially on a day like today—a Friday, with only a week left in the quarter and a critical deadline to meet. A deadline he couldn’t afford not to meet. Today, in the waning hours of the afternoon, Joe decided it was time to call in a favor, so he placed a phone call— but the conversation wasn’t going well. “Carl, tell me you’re not telling me this . .” Joe took a breath to keep the desperation out of his voice. “Neil Hansen?! Who the heck is Neil Hansen? . Well I don’t 1 21066_01_1-134_r4mw.indd 1 h 9/25/07 1:12:57 PM THE GO-GIVER care what he’s offering, we can meet those specs . -

Consumers Guide to Auto Insurance

CONSUMERS GUIDE TO AUTO INSURANCE PRESENTED TO YOU BY THE DEPARTMENT OF BUSINESS REGULATION INSURANCE DIVISION 1511 PONTIAC AVENUE, BLDG 69-2 CRANSTON, RI 02920 TELEPHONE 401-462-9520 www.dbr.ri.gov Elizabeth Kelleher Dwyer Superintendent of Insurance TABLE OF CONTENTS Introduction………………………………………………………………1 Underwriting and Rating………………………………………………...1 What is meant by underwriting and how is it accomplished…………..1 How are rates and premium charges determined in Rhode Island……1 What factors are considered in ratemaking……………………………. 2 What discounts are used in determining final premium cost…………..3 Rhode Island Automobile Insurance Plan…………………..…………..4 Regulation of Rates……………………………………………………….4 The Tort System…………………………………………………………..4 Liability Coverages………………………………………………………..5 Coverages Other Than Liability…………………………………………5 Physical Damage to the Automobile……………………………………..6 Other Optional Coverages………………………………………………..6 The No-Fault System……………….……………………………………..7 Smart Shopping……………………………………………………………7 Shop for True Comparison………………………………………………..8 Consumer Protection Available...…………………………………………8 What to Do if You are in an Automobile Accident………………………9 Your State Insurance Department………………………………….........9 Auto Insurance Buyer’s Worksheet…………………………………….10 Introduction Auto insurance is an expensive purchase for most Americans, and is especially expensive for Rhode Islanders. Yet consumers rarely comparison-shop for auto insurance as they might for other products and services. Auto insurance companies vary substantially both in price and service to policyholders, so it pays to shop around and compare different insurance companies. This guide to buying auto insurance was developed to help you become a more knowledgeable policyholder and to get the combination of price and service best suited to your needs. It provides information on how to shop for coverage and how insurance premiums are determined. You will also find an Auto Insurance Buyer’s Worksheet in the guide to help you compare premium prices among insurers.