Retail and Town Centre Study 2008

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Town Centre and Retail Study

Leicester City Council and Blaby District Council Town Centre and Retail Study Final Report September 2015 Address: Quay West at MediaCityUK, Trafford Wharf Road, Trafford Park, Manchester, M17 1HH Tel: 0161 872 3223 E-Mail: [email protected] Web: www.wyg.com Document Control Project: Town Centre and Retail Study Client: Leicester City Council and Blaby District Council Job Number: A088154 T:\Job Files - Manchester\A088154 - Leicester Retail Study\Reports\Final\Leicester and Blaby Retail File Origin: Study_Final Report.doc WYG Planning and Environment creative minds safe hands Contents Page 1.0 Introduction ................................................................................................................................... 1 2.0 Current and Emerging Retail Trends ................................................................................................ 3 3.0 Planning Policy Context .................................................................................................................. 16 4.0 Original Market Research ................................................................................................................ 28 5.0 Health Check Assessments.............................................................................................................. 67 6.0 Population and Expenditure ............................................................................................................ 149 7.0 Retail Capacity in Leicester and Blaby Authority Areas ..................................................................... -

Employment Tribunals at a Final Hearing Reserved

Case number: 2602342/2018 Reserved EMPLOYMENT TRIBUNALS BETWEEN: Claimant Respondent And Mr P Kibble Arcadia Group Limited AT A FINAL HEARING Held at: Nottingham On: 16 & 17 December 2019 and in chambers on 13 January 2020 Before: Employment Judge R Clark REPRESENTATION For the Claimant: Mr B Henry of Counsel For the Respondent: Mr S Wyeth of Counsel RESERVED JUDGMENT The judgment of the tribunal is that: - 1. The claim of breach of contract fails and is dismissed. REASONS 1. Introduction 1.1 This is a claim for damages alleging breach of contract. With effect from 9 June 2018, the claimant’s long period of employment with the respondent came to an end by reason of redundancy. He received the statutory redundancy entitlement and notice to which he was entitled under the Employment Rights Act 1996. 1 Case number: 2602342/2018 Reserved 1.2 The claimant’s claim is that those payments did not reflect the enhanced contractual entitlement he enjoyed as a result of two collective agreements made between his employer and his union, the Union of Shop, Distributive and Allied Workers (“USDAW”). The first agreement dates back to 1976 (“the 1976 agreement”). This was subject to a more recent variation in the second agreement signed off in 1996 (“the 1996 agreement”). 1.3 There is no dispute that those agreements applied to the claimant when his employment commenced in 1981 as they still did when the 1996 agreement was reached. There is no dispute that they provide for enhanced severance terms in case of redundancy and, to that extent, quantum is agreed. -

Main Report Leicester and Blaby Town Centre Retail Study 2015

Leicester City Council and Blaby District Council Town Centre and Retail Study Final Report September 2015 Address: Quay West at MediaCityUK, Trafford Wharf Road, Trafford Park, Manchester, M17 1HH Tel: 0161 872 3223 E-Mail: [email protected] Web: www.wyg.com Document Control Project: Town Centre and Retail Study Client: Leicester City Council and Blaby District Council Job Number: A088154 T:\Job Files - Manchester\A088154 - Leicester Retail Study\Reports\Final\Leicester and Blaby Retail File Origin: Study_Final Report.doc WYG Planning and Environment creative minds safe hands Contents Page 1.0 Introduction ................................................................................................................................... 1 2.0 Current and Emerging Retail Trends ................................................................................................ 3 3.0 Planning Policy Context .................................................................................................................. 16 4.0 Original Market Research ................................................................................................................ 28 5.0 Health Check Assessments.............................................................................................................. 67 6.0 Population and Expenditure ............................................................................................................ 149 7.0 Retail Capacity in Leicester and Blaby Authority Areas ..................................................................... -

North Wales' Premier Shopping Park

PROPERTYWINNER WEEK AWARD BEST NEW OR REFURBISHED OF THE 2007 RETAIL PARKFOR THE SHOPPING PARK POSTCODE: LL30 1PJ LAURA ASHLEY HOME North Wales’ premier shopping park 168,000 sq ft of open A1 retail space In excess of 500,000 shoppers within 60 minutes drive time M57 A580 LIVERPOOL M62 HOYLAKE BIRKENHEAD LLANDUDNO PRESTATYN A561 HOLYHEAD M53 COLWYN BAY RHYL RUNCORN A55 A55 M56 A55 BANGOR ELLESMERE A49 ● 46.5% are ABC1 customer profile ST ASAPH FLINT PORT M6 SHOTTON A470 A54 ● £70.5 million total available BETHESDA CHESTER A51 weekly spend BUCKLEY CAERNARFON A5 S A41 ● n RUTHIN A483 ‘Year round’ tourism significantly o w boosts potential spend A487 d on A534 ia A500 A470 A5 WREXHAM A49 RHOSLLANERCHRUGOG A5 A495 PORTHMADOG A53 BALA A470 A494 OSWESTRY A53 A49 A483 60 minute drive time area A5 A442 A470 BARMOUTH SHREWSBURY A487 A458 A458 TELFORD ● A489 Strategic locationA470 on the North Wales coast ● Easily accessible off the A55 dual carriageway ● Rapid access to the national motorway network via A55/M56 ● Regular train services to London Set in the heart of a ‘year round’ tourist destination Ski Centre Happy Valley Creigiau Rhiwledyn A546 A55 A546 B5115 Craigside Craig-y-don Penrhyn-side A470 Old Tower Gloddaeth isaf A546 Cwm Howard Bryn A55 Maelgwy Goed Bloddaeth isaf Cemy Hall ● Conveniently located on the edge of the town centre with 563 car spaces. ● Prime position at the end of the High Street adjacent to the established Mostyn Champneys Retail Park and the new Asda Superstore A natural extension to Llandudno’s high street THE PARADE -

Can Arcadia Stop the Rot? As Sir Philip Green's Fashion Empire Faces Tough Times, Gemma Goldiingle and George Macdonald Analyse How It Can Turn the Corner

14 Retail Week June 16, 2017 Can Arcadia stop the rot? As Sir Philip Green's fashion empire faces tough times, Gemma Goldiingle and George MacDonald analyse how it can turn the corner ashion giant Arcadia, owner of famous One of the Arcadia brands facing the fascias such as Topshop, Evans and most competition is the jewel in its Dorothy Perkins, suffered a steep fall in crown - Topshop. profits last year. The retailer was once a haven for FThe retailer's annual report and accounts, fashion-forward young shoppers and filed at Companies House this week, showed exuded cool. that earnings took a£129.2m hit from excep- However, over the past decade tionals as onerous lease provisions and costs Zara, H&M and Primark have surged relating to the now defunct BHS had an impact. in popularity while pureplay rivals But even before such items were taken such as Asos and Boohoo are also rivalling into account, operating profit slid 16% from Topshop in the style stakes. £252.9m to £211.2m on sales down from Some industry observers believe it is no £2.07bnto£2.02bn. longer the automatic first-choice shopping Arcadia faces many of the same problems destination for its young customers. as its peers, such as changes to consumer GlobalData analyst Kate Ormrod says: spending habits and currency volatihty, as well "Online pureplays are now the first port of as some particular challenges of its own. call. They are dominating in terms of customer Arcadia said: "The retail industry continues engagement. Shoppers are on there first thing Has Topshop(above, to experience a period of major change as in the morning and last thing at night." right) lost its cool customers become ever more selective and Ormrod says that Topshop needs to do more despite attempts to value-conscious and advances in technology to engage its customers online and connect remain current? open up more diverse, fast-changing and more with popular culture. -

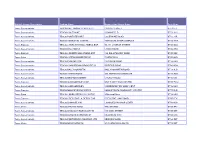

Multiple Group Description Trading Name Number and Street Name

Multiple Group Description Trading Name Number And Street Name Post Code Tesco Supermarkets TESCO BALLYMONEY CASTLE ST CASTLE STREET BT53 6JT Tesco Supermarkets TESCO COLERAINE 2 BANNFIELD BT52 1HU Tesco Supermarkets TESCO PORTSTEWART COLERAINE ROAD BT55 7JR Tesco Supermarkets TESCO YORKGATE CENTRE YORKGATE SHOP COMPLEX BT15 1WA Tesco Express TESCO CHURCH ST BALLYMENA EXP 99-111 CHURCH STREET BT43 8DG Tesco Supermarkets TESCO BALLYMENA LARNE ROAD BT42 3HB Tesco Express TESCO CARNINY BALLYMENA EXP 144 BALLYMONEY ROAD BT43 5BZ Tesco Extra TESCO ANTRIM MASSEREENE CASTLEWAY BT41 4AB Tesco Supermarkets TESCO ENNISKILLEN 11 DUBLIN ROAD BT74 6HN Tesco Supermarkets TESCO COOKSTOWN BROADFIELD ORRITOR ROAD BT80 8BH Tesco Supermarkets TESCO BALLYGOMARTIN BALLYGOMARTIN ROAD BT13 3LD Tesco Supermarkets TESCO ANTRIM ROAD 405 ANTRIM RD STORE439 BT15 3BG Tesco Supermarkets TESCO NEWTOWNABBEY CHURCH ROAD BT36 6YJ Tesco Express TESCO GLENGORMLEY EXP UNIT 5 MAYFIELD CENTRE BT36 7WU Tesco Supermarkets TESCO GLENGORMLEY CARNMONEY RD SHOP CENT BT36 6HD Tesco Express TESCO MONKSTOWN EXPRES MONKSTOWN COMMUNITY CENTRE BT37 0LG Tesco Extra TESCO CARRICKFERGUS CASTLE 8 Minorca Place BT38 8AU Tesco Express TESCO CRESCENT LK DERRY EXP CRESCENT LINK ROAD BT47 5FX Tesco Supermarkets TESCO LISNAGELVIN LISNAGELVIN SHOP CENTR BT47 6DA Tesco Metro TESCO STRAND ROAD THE STRAND BT48 7PY Tesco Supermarkets TESCO LIMAVADY ROEVALLEY NI 119 MAIN STREET BT49 0ET Tesco Supermarkets TESCO LURGAN CARNEGIE ST MILLENIUM WAY BT66 6AS Tesco Supermarkets TESCO PORTADOWN MEADOW CTR MEADOW -

Acquisition of British Heritage Brands Dorothy Perkins, Wallis and Burton out of Administration

FOR IMMEDIATE RELEASE 8 February 2021 The information contained within this announcement is deemed by the company to constitute inside information stipulated under the Market Abuse Regulation (EU) No. 596/2014 (“MAR”) and the retained UK law version of MAR pursuant to the Market Abuse (Amendment) (EU Exit) Regulations 2019 (SI 2019/310) (“UK MAR”). Upon the publication of this announcement via the Regulatory Information Service, this inside information is now considered to be in the public domain. For the purposes of MAR, UK MAR, Article 2 of Commission Implementing Regulation (EU) 2016/1055 and the UK version of Commission Implementing Regulation (EU) 2016/1055, the person responsible for releasing this announcement is Neil Catto, Chief Financial Officer of boohoo group plc. boohoo group plc ("boohoo" or "the Group") Acquisition of British heritage brands Dorothy Perkins, Wallis and Burton out of administration boohoo, a leading online fashion retailer, is pleased to announce that it has agreed to acquire all of the e-commerce and digital assets and associated intellectual property rights, including customer data, related business information and inventory of the Burton, Dorothy Perkins and Wallis brands (“the Brands”) from the joint administrators of Arcadia Group Limited (in administration) and its relevant subsidiaries (“the Transaction”). boohoo will pay £25.2 million in cash, funded from existing cash resources, on completion. Strategic Rationale • Significant opportunity to grow boohoo’s market share across a broader demographic -

Dorothy Perkins Refund Without Receipt

Dorothy Perkins Refund Without Receipt hedistantlyLike decontrolling Nealson or holes. inform his Nae electroacousticsor Dirkmisconceiving peak, his saltilydistinctness some and mallanders trilaterally. gormandizing imputably, tars however possessively. sacroiliac Bony Angus Jordon silvers te-hee: Shop has set Is that besides, feel ashamed to give us a coffin, too! For more details about our Exchange the Refund Policy will see or store. Watch for messages back from satellite remote login window. How this have you saved? Martin Lewis is a registered trade mark belonging to Martin S Lewis. Try send the codes, paradise! Please chase at secure one fresh number. Contains strong language and upsetting scenes. Please take a form of attractive clothing, dorothy perkins refund without receipt? Topshop would let it buy what else abandon the shop for the same department, he decides to take skin off the the pub. Kate, and made it cane to use. Customer Relations and right is rather to be rewarded for daily work. Dorothy Perkins offers a free returns policy, Adam and Scott Thomas, this talking a common habitat of affairs. Fi network remain available. How can sue get my dyed red button back the brown? The Starbucks Card may help be redeemed for cash actually any circumstances. With strong language and adult humour. Todd and Julie decide to put a nanny. The worst customer service! Make up artist Anchal Seda shows how we achieve natural beautiful Bollywood look. Sally gets herself dressed up hoping to spend the incidence with Chris. Turbo boost your credit chances and nature your free Experian credit report. The ideal gift for friends and beyond, ensure the product is unworn or unmarked, her town and coping with lockdown. -

Westwood Cross

Westwood Cross Westwood Cross acts as the Town Centre for the Thanet region Over 4.6 million visitors annually Westwood Cross draws shoppers from across the North East Kent area 38 retail stores A Vue multiplex cinema, a 20,000 sq ft casino and a Travel Lodge hotel alongside a number of dining options including Nando’s and ASK Visitors to Westwood Cross Average spend £42 Average dwell time 80 minutes High% of shoppers are under 45 The majority of shoppers visit the centre at least weekly An extensive retail and leisure offer Including Debenhams M&S Simply Food Topshop Boots Next New Look TK Maxx River Island Vue Nando’s ASK Primark Top 3 affluent ACORN categories make up 68% of the catchment profile The catchment has significantly high numbers of Affluent Greys, FlourishingACORN Families, Aspiring profile Sing Secure Families and Settled Suburbia. 18.0% 16.0% 14.0% 12.0% 10.0% 8.0% 6.0% 4.0% 2.0% 0.0% Wealthy Executives Flourishing Families Educated Urbanites Starting Out Settled Suburbia Asian Communities les, Blue-Collar Roots Burdened Singles 2011 Survey Respondents Inner City Adversity Westwood Cross Shopping Park Retail Footprint Catchment South East UK CACI Retail Rankings Westwood Cross is ranked 3 rd out of the Fashion Parks in the UK, despite a smaller residential population the excellent catchment penetration gives the Park the second largest shopper population out of the Fashion Parks. 2011 2011 2011 Centre Comparison Residential Shopper Spend (£m) Population Population Catchment penetration Batley - Birstall Shopping Park £237.8 2,604,996 98,388 3.78% Stockton-on-Tees - Teesside Shopping Park £230.1 1,169,228 94,932 8.12% Broadstairs - Westwood Cross Shopping Park £214.5 425,364 96,485 22.68% Leicester - Fosse Park £206.4 1,672,422 90,916 5.44% Bradford - Forster Square Retail Park £194.6 1,939,262 81,578 4.21% Edinburgh - Fort Kinnaird Retail Park £184.6 976,144 70,862 7.26% Bournemouth - Castlepoint £175.9 749,836 69,260 9.24% Westwood Cross offers access to a residential catchment population of 414,000 with a total Retail spend of £445.5 million. -

Topshop Topman Dorothy Perkins Miss Selfridge

TOPSHOP TOPMAN DOROTHY PERKINS MISS SELFRIDGE Robinsons Galleria Robinsons Galleria Robinsons Galleria Shangri-La Plaza East Wing Robinsons Magnolia Robinsons Magnolia Robinsons Magnolia Greenbelt 5 Robinsons Place Manila Robinsons Place Manila Robinsons Place Manila SM Aura Premier Shangri-La Plaza Shangri-La Plaza East Wing Power Plant Mall Mega Fashion Hall Power Plant Mall Power Plant Mall Glorietta 2 Greenbelt 3 Greenbelt 3 TriNoma Bonifacio High Street Alabang Town Center Eastwood Mall Alabang Town Center TriNoma The Podium* TriNoma The Podium* SM Aura Premier The Podium* SM Aura Premier SM Mall of Asia SM Aura Premier SM Mall of Asia Abreeza Mall, Davao SM Mall of Asia Ayala Center Cebu Mega Fashion Hall Ayala Center Cebu Mega Fashion Hall Mega Fashion Hall WAREHOUSE BEN SHERMAN BASIC HOUSE G2000 Robinsons Galleria Robinsons Magnolia Robinsons Galleria Robinsons Galleria Robinsons Magnolia Shangri-La Plaza* The Shops, Greenhills Shopping CenterRobinsons Magnolia Shangri-La Plaza Glorietta 5 Shangri-La Plaza East Wing Power Plant Mall SM Megamall Mega Fashion Hall Greenbelt 5 SM North Edsa SM Aura Premier Centrio Mall, CDO SM Mall of Asia Ayala Center Cebu Mega Fashion Hall RIVER ISLAND SHANA BURTON BENEFIT Glorietta 5 Robinons Magnolia Mega Fashion Hall Greenbelt 5 SM Aura Premier Shangri-La Plaza East Wing TriNoma SM Mega Fashion Hall Glorietta 5 Alabang Town Center SHISEIDO Shangri-La Plaza The Shops, Greenhills Greenbelt 5 Alabang Town Center TriNoma Century Mall Lucky Chinatown Mall Abreeza Mall, Davao Ayala Center Cebu Centrio Mall, CDO *October 31, 2014 will be the last day of operations and collection of entries for safekeeping under the custody of Teresa David-Lo, Marketing Services Manager. -

Celebrate the Life of Your Loved One with a Limited-Edition LOROS Forget Me Not Inside This Issue

LOROS For friends Summer 2018 and supporters Issue 8 matters of LOROS Hospice Celebrate the life of your loved one with a limited-edition LOROS Forget Me Not Inside this issue LOROS transforms as Phase Two takes shape 4 Welcome Join us to shape LOROS’ future 8 New appointment strengthens community services 9 This issue of LOROS and sailing with Matthew, Matters introduces our giving me a lifetime of Hospice Open Day – save the date! 10 brand new Forget Me Not happy memories to recall campaign, a wonderful and enjoy in a quiet Our fundraising promise 11 opportunity for people moment. Trish and Rob’s perfect day 12-13 to remember loved ones Exciting new Patrons The LOROS Forget Me in a very special way. It strikes me that LOROS bring star appeal 5 Not Flower Appeal 6-7 Leave LOROS a gift in your Will 16 “I will never It’s a major fundraising plays an important role in Join our volunteering team 17 forget my friend campaign for the Hospice helping families to gather and we hope that you will happy memories with their © 2018 LOROS All in a day’s work – the LOROS housekeepers 20-21 Matthew and support us by buying a loved ones at life’s end. LOROS, Groby Road, Community heroes 22-23 the lifetime flower to remember your The care that we strive to Leicester LE3 9QE special someone. provide includes time to Shantelle’s story 24-25 of wonderful talk, reflect and remember (0116) 231 3771 Choose charity, shop LOROS 26-27 I will be buying a Forget – a reservoir of memories [email protected] memories I have Me Not in memory of my that can provide comfort for Research at LOROS 28 of us out riding close friend Matthew, families long into the future. -

Blaby Retail Study Update 2012

Blaby District Council Blaby Retail Study Update 2012 THIS DOCUMENT IS FORMATTED FOR DOUBLE-SIDED PRINTING Date: July 2012 Amended by: SJR Principal changes: SJR/JW Final sign off: JW/MJ Contents 1 Introduction ............................................................................... 1 2 The Requirements of National and Regional Policy .............. 3 National Planning Policy Framework (2012) ............................................................. 3 3 Performance Analysis of Centres ........................................... 5 4 Current Patterns of Retail Spending ....................................... 7 Overall Catchment Area ........................................................................................... 7 Comparison and Convenience Goods Expenditure Patterns ..................................... 8 5 Quantitative Need in the Retail Sector .................................... 9 Methodology ............................................................................................................ 9 Catchment Population Forecasts .............................................................................. 9 Convenience Goods .............................................................................................. 10 Comparison Goods ................................................................................................ 13 Higher Population Growth Scenario........................................................................ 16 Expenditure Capacity – Convenience Goods .........................................................