Town Centre and Retail Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Summary Facts and Figures About Blaby District

Appendix B Summary Facts and figures about Blaby district The District is home to nearly 96, 000 people (Mid 2014 estimates) living in 40,345 households. Leics East Blaby England County Midlands Age 2014 2014 2014 2014 0-19 23.35% 23.00% 23.40% 23.76% 20 to 64 56.96% 57.53% 58.05% 58.68% 65 to 89 18.82% 18.56% 17.66% 16.69% 90 and over 0.87% 0.91% 0.86% 0.87% Male Female Source: Office for National Statistics website: http://www.ons.gov.uk/ons/guide- method/census/2011/index.html Crown copyright material is reproduced with the permission of the Controller of HMSO 0.4% 6.1% 0.9% 1.6% Ethnicity 2.5% 11.5% of residents White British % are from minority All Other White % ethnic backgrounds (2011 All Mixed % census), this is All Asian % mainly in the All black % Asian/Asian British All Other % group (6.1%). 88.5% (Source: ONS http://www.ons.gov.uk/ons/guide-method/census/2011/index.html Crown copyright material is reproduced with the permission of the Controller of HMSO) % of people aged 16- 64 with long-term limiting disability or health problem (2011 Census) Leicestershire East Measure Blaby (Exc Leic City) Midlands England Total % 15.8 16.2 18.6 17.6 Source: ONS: http://www.ons.gov.uk/ons/guide-method/census/2011/index.html Appendix B Life Expectancy 86 84 82 80 78 76 74 (Exc Leic City) Blaby Leicestershire East Midlands England Male 80.7 79.7 77.8 79.4 Female 84.6 83.4 81.8 83.1 Source: www.healthprofiles.info local profiles 2011-2013 Carers 11% of local people provide 1 hour or more a week of unpaid care for others. -

LEICESTERSHIRE. Newaold-DE

DIUOTOBY.J LEICESTERSHIRE. NEwaOLD-DE .. VERDt1:f. 767 N ARBOROUGHis & township, parish and large village, Parish Clerk, George Heighton. pleasantly sitnated .on the west bank of the river Soar, with POST, M. O. & T. 0., S. B. & Annuity & Insurance Office. a station on the Leicester and Nuneaton branch of tile Arthur Dawkins, postmaster. Letters arrive from Leices London and North Western rail way, 5 miles south-west from ter at 6.35 a.m. & r p.m. ; & are dispatched at XI a.m. Leicester, 9 north from Lutterworth and 100 from London, 6.10 &8 p.m in the Southern division of the c::lUnty, Sparkenhoe hundred, Blaby union, Leicester petty sessional division and county National & Sunday Schools, re-erected in 1872, for 200 court district, rural deanery of Guthlaxton first portion, children & 50 infants; average attendance, 136 children archdeaconry of Leicester and diocese of Peterborough. The & 38 infants; Richard Meats, master; Mrs. A, Meats, church of All Saints is a building of stone in the Early sewing mistress English and Perpendicular styles, consisting of chancel, re CARRIERS TO Ll!:ICESTER.-James Southam, IJl{)n. wed. & built in 1881, south porch and a massive embattled western sat. ; Charles Haines, mono wed. fri. & sat tower containing 6 bells, dated 1672: there are memorial Railway Station, WiIliam Hatcheldor, stat,ion master windows to the wife of a former rector, to George Hunt, to Ueorge and Elizabeth Wills, to Henry Kirk and to Dr. and Huncote is a township, in the parish of Nal'borough. li Mrs. Orton: the church affords 500 sittings. -

Leicester & Leicestershire Authorities

Leicester & Leicestershire Authorities - Statement of Common Ground relating to Housing and Employment Land Needs (March 2021) 1.0 The Leicester and Leicestershire HMA and FEMA 1.1 The Leicester and Leicestershire Housing Market Area (HMA) and Functional Economic Area (FEMA) covers the administrative areas of eight local planning authorities and two transport authorities. The eight local planning authorities responsible for plan making are: • Blaby District Council • Charnwood Borough Council • Harborough District Council • Hinckley & Bosworth Borough Council • Leicester City Council (Unitary) • Melton Borough Council • North West Leicestershire District Council • Oadby & Wigston Borough Council 1.2 The two upper tier authorities in Leicester and Leicestershire (L&L), with statutory responsibilities for transportation, education, social care, flooding, minerals & waste planning and public health are: • Leicester City Council (Unitary) • Leicestershire County Council 1.3 This Statement has been prepared jointly by the eight plan making authorities and Leicestershire County Council as an additional signatory given their statutory responsibilities, hereafter referred to as “the authorities”. The Map in Appendix C shows the location and administrative areas covered by this statement. The Housing & Economic Development Needs Assessment 2017 (HEDNA) identifies this area as the Leicester & Leicestershire HMA and FEMA. 1.4 Local planning authorities across L&L are currently progressing plans at different stages. Appendix D sets out the latest position. 2.0 Purpose 2.1 This statement has been prepared by the authorities to support the Charnwood Local Plan. The key strategic matters covered in this statement under the Duty to Cooperate are; L&L Housing and Employment Needs to 2036; Unmet Need to 2036; and the process of apportioning unmet need to 2036. -

![Mineral and Waste Safeguarding [Blaby District] Document S1/2014](https://docslib.b-cdn.net/cover/7028/mineral-and-waste-safeguarding-blaby-district-document-s1-2014-347028.webp)

Mineral and Waste Safeguarding [Blaby District] Document S1/2014

Mineral and Waste Safeguarding [Blaby District] Document S1/2014 October 2014 Contents Contents Mineral Safeguarding 1 Figure B1: Areas of borough/district for mineral safeguarding, categorised by mineral type 1 Waste Safeguarding 2 Table B1: Waste sites in borough/district for safeguarding 2 Figure B2: Location in borough/district of waste sites for safeguarding 3 Detailed location plans for each waste site for safeguarding in borough/district 4 Aston Flamville SPS 4 Barrows Lane, Glenfield & Glenfield STW 5 Cosby Spinneys, Cosby 6 Countesthorpe STW 7 Coventry Road, Narborough 8 Enderby Road Whetstone, Vicarage Lane SPS Whetstone, Whetstone RHWS and Transfer, & Whetstone STW 9 Granite Close Enderby, Quartz Close Enderby, & Warren Parks Way Enderby 10 Greens Lodge Farm Huncote & Huncote Quarry 11 Leicester Forest West SPS 12 Manor Farm, Aston Flamville 13 Soars Lodge Farm, Foston 14 Station Yard, Elmesthorpe 15 Stoney Stanton STW 16 i Mineral Safeguarding Figure B1: Areas of borough/district for mineral safeguarding, categorised by mineral type Legend Clay Coal Gypsum Igneous Rock Limestone Sand & gravel 1 Waste Safeguarding Table B1: Waste sites in borough/district for safeguarding District or Site District or Site Site Name Address Operator Site Name Address Operator Borough Reference Borough Reference Manor Farm, Sharnford Soars Lodge Farm, Foston Soars Lodge Farm, Aston Flamville Road, Aston Flamville, Severn Trent Lane, Foston, Leicester, D Clark Blaby B16 Blaby B1 Foston SPS Hinckley, Leicestershire, Water Leicestershire, LE8 5WP -

Main Report Leicester and Blaby Town Centre Retail Study 2015

Leicester City Council and Blaby District Council Town Centre and Retail Study Final Report September 2015 Address: Quay West at MediaCityUK, Trafford Wharf Road, Trafford Park, Manchester, M17 1HH Tel: 0161 872 3223 E-Mail: [email protected] Web: www.wyg.com Document Control Project: Town Centre and Retail Study Client: Leicester City Council and Blaby District Council Job Number: A088154 T:\Job Files - Manchester\A088154 - Leicester Retail Study\Reports\Final\Leicester and Blaby Retail File Origin: Study_Final Report.doc WYG Planning and Environment creative minds safe hands Contents Page 1.0 Introduction ................................................................................................................................... 1 2.0 Current and Emerging Retail Trends ................................................................................................ 3 3.0 Planning Policy Context .................................................................................................................. 16 4.0 Original Market Research ................................................................................................................ 28 5.0 Health Check Assessments.............................................................................................................. 67 6.0 Population and Expenditure ............................................................................................................ 149 7.0 Retail Capacity in Leicester and Blaby Authority Areas ..................................................................... -

Supplier Payments Over £500 - May 2019

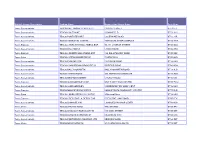

Supplier payments over £500 - May 2019 Invoice Corporate Subjective Payment Vendor Name Description Amount Payment Date 2M HEATH & HOMECARE SERVICES LTD&&ISHC3873 Home Care / Domiciliary 855.91 17/05/2019 2M HEATH & HOMECARE SERVICES LTD&&ISHC3873 Home Care / Domiciliary 3736.74 17/05/2019 2M HEATH & HOMECARE SERVICES LTD&&ISHC3873 Home Care / Domiciliary 11137.86 17/05/2019 365 CARE HOMES LTD T/A CLITHEROE CARE HOME &&SSARO8528Residential 508 03/05/2019 365 CARE HOMES LTD T/A CLITHEROE CARE HOME &&SSARO8528Residential 2032 03/05/2019 AARON HOUSE CARE LTD&&SSARO5337 Residential 1668 03/05/2019 ABBERDALE LIMITED&&SSAROE40419 Residential -1520.4 03/05/2019 ABBERDALE LIMITED&&SSAROE40419 Residential 1144 03/05/2019 ABBERDALE LIMITED&&SSAROE40419 Residential 2288 03/05/2019 ABBEYFIELDS EXTRA CARE&&SSAROE52835 Residential 15639.16 03/05/2019 ABBEY HEALTHCARE (AARON COURT) LTD&&SSARO2996 Nursing -7528.5 03/05/2019 ABBEY HEALTHCARE (AARON COURT) LTD&&SSARO2996 Nursing 10506 03/05/2019 ABBEY HEALTHCARE (AARON COURT) LTD&&SSARO2996 Nursing 22624.31 03/05/2019 ABBEY HEALTHCARE (AARON COURT) LTD&&SSARO2996 Private Contractors -7528.5 03/05/2019 ABBEY HEALTHCARE (AARON COURT) LTD&&SSARO2996 Private Contractors 835 03/05/2019 ABBEY HEALTHCARE (AARON COURT) LTD&&SSARO2996 Private Contractors 3340 03/05/2019 ABBEY HEALTHCARE (AARON COURT) LTD&&SSARO2996 Private Contractors 10506 03/05/2019 ABBEY HEALTHCARE (AARON COURT) LTD&&SSARO2996 Private Contractors 22624.31 03/05/2019 ABBEY HEALTHCARE (AARON COURT) LTD&&SSARO2996 Residential -7528.5 03/05/2019 -

Ratby VDS Adopted

Adopted February 2011 Local Development Framework Ratby Village Design Statement Supplementary Planning Document CONTENTS page 1.0 Introduction 3 2.0 THE VILLAGE CONTEXT 5 3.0 SETTLEMENT PATTERN 11 3.1 Zone A: The Conservation Area 13 3.2 Zone B: Station Road, Park Road, Desford Lane, Mill Drive, Taverner Drive, Brook Drive 20 3.3 Zone C: Markfield Road, Charnwood & Stamford Street 28 3.4 Zone D: Church Farm Development 39 4.0 LANDSCAPE SETTING & WILDLIFE 47 5.0 GREEN SPACES HEDGES, WALLS & FENCES 54 6.0 HIGHWAYS, TRAFFIC AND FOOTPATHS 56 Ratby Village Design Statement 1.0 INTRODUCTION The Ratby Village Design Statement (VDS) sets Who the Statement is for? out the principles, design features and quality The Ratby Design Statement has been developed standards that should be adopted by those for: wishing to build, modify or extend property in the settlement of Ratby. • The Parish and Borough Councils’ Planning Committees as a Supplementary Planning Residents of Ratby and the Parish Council have Document to the Hinckley and Bosworth developed the Village Design Statement with Local Plan. support from officers of Hinckley and Bosworth Borough Council and the Leicestershire and • Developers, their architects and designers, to Rutland Rural Community Council. The Village explain what the community of Ratby expect Design Statement forms part of the planning to see in new and modified buildings. policy framework used by the Borough Council in • Local residents, to help them keep alterations making decisions on planning applications. and extensions in sympathy with the The aim of the VDS is to support various local character of Ratby. -

The Leicestershire County Council

THE LEICESTERSHIRE COUNTY COUNCIL (VARIOUS ROADS, ASTON FLAMVILLE, ENDERBY, NARBOROUGH, SAPCOTE AND STONEY STANTON (AREA 1), DISTRICT OF BLABY) AMENDMENT ORDER NO.1 2008 The Leicestershire County Council ("the Council") in exercise of its powers under Section 1(1) and (2) 2(1) to (3) 4(2) and Part IV to Schedule 9 of the Road Traffic Regulation Act 1984 ("the Act"), the Road Traffic Act 1991 (“the 1991 Act”) and of all other enabling powers, hereby makes the following Order:- 1. This Order shall come into force on the Twenty-Fourth day of November 2008 and may be cited as "The Leicestershire County Council (Various Roads, Aston Flamville, Enderby, Narborough, Sapcote and Stoney Stanton (Area 1), District of Blaby) Amendment Order No. 1 2008". 2. The exemptions contained in this Order as set out in column 1 of Schedule 1 shall hereafter be referred to by reference to the code letters given in column 2 of Schedule 1. 3. (1) In this Order – "authorised cab rank" means any area of carriageway which is comprised within and indicated by a road marking complying with diagram 1028.2 in Schedule 6 of The Traffic Signs Regulations and General Directions 2002; "authorised parking place" means any parking place on a road authorised or designated by an Order made or having effect as if made under the Act; "bus" means any Public Service Vehicle or bus operating a local stage carriage service as defined in the Transport Act 1985; "bus stop area" means any area of carriageway on the sides of roads specified in this Order which is comprised within and -

SCRUTINY NETWORK Friday 1 February 2019, 10:00 – 12:30

SCRUTINY NETWORK Friday 1 February 2019, 10:00 – 12:30 Rutland County Council Attendees Blaby District Council Linda McBean Bolsover District Council Joanne Wilson Bolsover District Council Cllr Karl Reid Charnwood Borough Council Michael Hopkins Chesterfield Borough Council Amanda Clayton Chesterfield Borough Council Rachel Appleyard Chesterfield Borough Council Cllr Kate Sarvent East Midlands Councils Kirsty Lowe Erewash Borough Council Angelika Kaufhold Gedling Borough Council Cllr Marje Paling Lincolnshire County Council Nigel West Northampton Borough Council Cathrine Russell Northampton Borough Council Tracy Tiff Rutland County Council Natasha Taylor Rutland County Council Jo Morley University of Birmingham John Cade Apologies Bassetlaw District Council Richard Gadsby Bassetlaw District Council Cllr John Shepherd Blaby District Council Suraj Savant Chesterfield Borough Council Cllr Peter Innes Gedling Borough Council Helen Lee Hinckley and Bosworth Borough Council Rebecca Owen Kettering Borough Council Cllr Mick Scrimshaw Northampton Borough Council Cllr Graham Walker South Northamptonshire and Cherwell Emma Faulkner South Northamptonshire and Cherwell Lesley Farrell South Northamptonshire and Cherwell Natasha Clark Notes Welcome from Cllr Karl Reid, Chair of the East Midlands Scrutiny Network Cllr Karl Reid welcomed network members to Oakham and thanked Rutland County Council for hosting the network meeting. Minutes from the last meeting The minutes of the last meeting were agreed. CfPS Scrutiny Guidance Workshop John Cade from the Institute of Local Government Studies at the University of Birmingham provided an overview of the recent Centre for Public Scrutiny workshop on the Government guidance that is due to be published in the coming weeks. John provided an update on the guidance and the journey so far, from the initial Select Committee review into Local Government Overview and Scrutiny. -

Multiple Group Description Trading Name Number and Street Name

Multiple Group Description Trading Name Number And Street Name Post Code Tesco Supermarkets TESCO BALLYMONEY CASTLE ST CASTLE STREET BT53 6JT Tesco Supermarkets TESCO COLERAINE 2 BANNFIELD BT52 1HU Tesco Supermarkets TESCO PORTSTEWART COLERAINE ROAD BT55 7JR Tesco Supermarkets TESCO YORKGATE CENTRE YORKGATE SHOP COMPLEX BT15 1WA Tesco Express TESCO CHURCH ST BALLYMENA EXP 99-111 CHURCH STREET BT43 8DG Tesco Supermarkets TESCO BALLYMENA LARNE ROAD BT42 3HB Tesco Express TESCO CARNINY BALLYMENA EXP 144 BALLYMONEY ROAD BT43 5BZ Tesco Extra TESCO ANTRIM MASSEREENE CASTLEWAY BT41 4AB Tesco Supermarkets TESCO ENNISKILLEN 11 DUBLIN ROAD BT74 6HN Tesco Supermarkets TESCO COOKSTOWN BROADFIELD ORRITOR ROAD BT80 8BH Tesco Supermarkets TESCO BALLYGOMARTIN BALLYGOMARTIN ROAD BT13 3LD Tesco Supermarkets TESCO ANTRIM ROAD 405 ANTRIM RD STORE439 BT15 3BG Tesco Supermarkets TESCO NEWTOWNABBEY CHURCH ROAD BT36 6YJ Tesco Express TESCO GLENGORMLEY EXP UNIT 5 MAYFIELD CENTRE BT36 7WU Tesco Supermarkets TESCO GLENGORMLEY CARNMONEY RD SHOP CENT BT36 6HD Tesco Express TESCO MONKSTOWN EXPRES MONKSTOWN COMMUNITY CENTRE BT37 0LG Tesco Extra TESCO CARRICKFERGUS CASTLE 8 Minorca Place BT38 8AU Tesco Express TESCO CRESCENT LK DERRY EXP CRESCENT LINK ROAD BT47 5FX Tesco Supermarkets TESCO LISNAGELVIN LISNAGELVIN SHOP CENTR BT47 6DA Tesco Metro TESCO STRAND ROAD THE STRAND BT48 7PY Tesco Supermarkets TESCO LIMAVADY ROEVALLEY NI 119 MAIN STREET BT49 0ET Tesco Supermarkets TESCO LURGAN CARNEGIE ST MILLENIUM WAY BT66 6AS Tesco Supermarkets TESCO PORTADOWN MEADOW CTR MEADOW -

British Family Names

cs 25o/ £22, Cornrll IBniwwitg |fta*g BOUGHT WITH THE INCOME FROM THE SAGE ENDOWMENT FUND THE GIFT OF Hcnrti W~ Sage 1891 A.+.xas.Q7- B^llll^_ DATE DUE ,•-? AUG 1 5 1944 !Hak 1 3 1^46 Dec? '47T Jan 5' 48 ft e Univeral, CS2501 .B23 " v Llb«"y Brit mii!Sm?nS,£& ori8'" and m 3 1924 olin 029 805 771 The original of this book is in the Cornell University Library. There are no known copyright restrictions in the United States on the use of the text. http://www.archive.org/details/cu31924029805771 BRITISH FAMILY NAMES. : BRITISH FAMILY NAMES ftbetr ©riain ano fIDeaning, Lists of Scandinavian, Frisian, Anglo-Saxon, and Norman Names. HENRY BARBER, M.D. (Clerk), "*• AUTHOR OF : ' FURNESS AND CARTMEL NOTES,' THE CISTERCIAN ABBEY OF MAULBRONN,' ( SOME QUEER NAMES,' ' THE SHRINE OF ST. BONIFACE AT FULDA,' 'POPULAR AMUSEMENTS IN GERMANY,' ETC. ' "What's in a name ? —Romeo and yuliet. ' I believe now, there is some secret power and virtue in a name.' Burton's Anatomy ofMelancholy. LONDON ELLIOT STOCK, 62, PATERNOSTER ROW, E.C. 1894. 4136 CONTENTS. Preface - vii Books Consulted - ix Introduction i British Surnames - 3 nicknames 7 clan or tribal names 8 place-names - ii official names 12 trade names 12 christian names 1 foreign names 1 foundling names 1 Lists of Ancient Patronymics : old norse personal names 1 frisian personal and family names 3 names of persons entered in domesday book as HOLDING LANDS temp. KING ED. CONFR. 37 names of tenants in chief in domesday book 5 names of under-tenants of lands at the time of the domesday survey 56 Norman Names 66 Alphabetical List of British Surnames 78 Appendix 233 PREFACE. -

Great Easton Neighbourhood Plan 2017 – 2031

GREAT EASTON NEIGHBOURHOOD PLAN 2017 – 2031 REFERENDUM VERSION Great Easton Neighbourhood Plan 2017-2031 Contents Introduction from Chairmen 3 1.Why Neighbourhood Plans are important 5 2.Why we need a Neighbourhood Plan in Great Easton 6 3.How the Neighbourhood Plan was prepared 6 4.Our neighbourhood 10 5.What we want the Neighbourhood Plan to achieve 12 6.Meeting the requirement for sustainable development 15 Neighbourhood Plan Policies 7.A Sustainable Great Easton 17 8.Housing 20 9.Design and the Built Environment 29 10.Natural and Historical Environment 34 11.Employment 50 12.Community Facilities and Amenities 57 13.Transport and Access 64 14.Delivery 68 15. Monitoring and Review 70 16. List of Appendices 71 Page 2 of 71 Great Easton Neighbourhood Plan 2017-2031 Introduction from the Chairmen of the Great Easton Neighbourhood Plan Advisory Committee and Great Easton Parish Council In late 2014, the Parish Council of Great Easton decided to prepare a Neighbourhood Plan. Although situated just outside the Parish boundary, Bringhurst Primary School was included in the designated area of the Neighbourhood Plan. This reflected the importance to the community of the local School and was endorsed by Bringhurst, Drayton & Nevill Holt Parish Meeting. The Great Easton Neighbourhood Plan Advisory Committee was established to prepare a Plan that would deliver the long term goals of a balanced and vibrant neighbourhood. Since becoming established, we have held many public meetings, both general open events and specific discussions with groups of, for example, school children and older people; prepared a village questionnaire to seek the views of local residents and other stakeholders (including landowners), groups and businesses who share an interest in Great Easton.