Impact Assessment

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Town Centre and Retail Study

Leicester City Council and Blaby District Council Town Centre and Retail Study Final Report September 2015 Address: Quay West at MediaCityUK, Trafford Wharf Road, Trafford Park, Manchester, M17 1HH Tel: 0161 872 3223 E-Mail: [email protected] Web: www.wyg.com Document Control Project: Town Centre and Retail Study Client: Leicester City Council and Blaby District Council Job Number: A088154 T:\Job Files - Manchester\A088154 - Leicester Retail Study\Reports\Final\Leicester and Blaby Retail File Origin: Study_Final Report.doc WYG Planning and Environment creative minds safe hands Contents Page 1.0 Introduction ................................................................................................................................... 1 2.0 Current and Emerging Retail Trends ................................................................................................ 3 3.0 Planning Policy Context .................................................................................................................. 16 4.0 Original Market Research ................................................................................................................ 28 5.0 Health Check Assessments.............................................................................................................. 67 6.0 Population and Expenditure ............................................................................................................ 149 7.0 Retail Capacity in Leicester and Blaby Authority Areas ..................................................................... -

Main Report Leicester and Blaby Town Centre Retail Study 2015

Leicester City Council and Blaby District Council Town Centre and Retail Study Final Report September 2015 Address: Quay West at MediaCityUK, Trafford Wharf Road, Trafford Park, Manchester, M17 1HH Tel: 0161 872 3223 E-Mail: [email protected] Web: www.wyg.com Document Control Project: Town Centre and Retail Study Client: Leicester City Council and Blaby District Council Job Number: A088154 T:\Job Files - Manchester\A088154 - Leicester Retail Study\Reports\Final\Leicester and Blaby Retail File Origin: Study_Final Report.doc WYG Planning and Environment creative minds safe hands Contents Page 1.0 Introduction ................................................................................................................................... 1 2.0 Current and Emerging Retail Trends ................................................................................................ 3 3.0 Planning Policy Context .................................................................................................................. 16 4.0 Original Market Research ................................................................................................................ 28 5.0 Health Check Assessments.............................................................................................................. 67 6.0 Population and Expenditure ............................................................................................................ 149 7.0 Retail Capacity in Leicester and Blaby Authority Areas ..................................................................... -

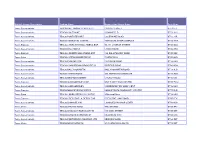

Multiple Group Description Trading Name Number and Street Name

Multiple Group Description Trading Name Number And Street Name Post Code Tesco Supermarkets TESCO BALLYMONEY CASTLE ST CASTLE STREET BT53 6JT Tesco Supermarkets TESCO COLERAINE 2 BANNFIELD BT52 1HU Tesco Supermarkets TESCO PORTSTEWART COLERAINE ROAD BT55 7JR Tesco Supermarkets TESCO YORKGATE CENTRE YORKGATE SHOP COMPLEX BT15 1WA Tesco Express TESCO CHURCH ST BALLYMENA EXP 99-111 CHURCH STREET BT43 8DG Tesco Supermarkets TESCO BALLYMENA LARNE ROAD BT42 3HB Tesco Express TESCO CARNINY BALLYMENA EXP 144 BALLYMONEY ROAD BT43 5BZ Tesco Extra TESCO ANTRIM MASSEREENE CASTLEWAY BT41 4AB Tesco Supermarkets TESCO ENNISKILLEN 11 DUBLIN ROAD BT74 6HN Tesco Supermarkets TESCO COOKSTOWN BROADFIELD ORRITOR ROAD BT80 8BH Tesco Supermarkets TESCO BALLYGOMARTIN BALLYGOMARTIN ROAD BT13 3LD Tesco Supermarkets TESCO ANTRIM ROAD 405 ANTRIM RD STORE439 BT15 3BG Tesco Supermarkets TESCO NEWTOWNABBEY CHURCH ROAD BT36 6YJ Tesco Express TESCO GLENGORMLEY EXP UNIT 5 MAYFIELD CENTRE BT36 7WU Tesco Supermarkets TESCO GLENGORMLEY CARNMONEY RD SHOP CENT BT36 6HD Tesco Express TESCO MONKSTOWN EXPRES MONKSTOWN COMMUNITY CENTRE BT37 0LG Tesco Extra TESCO CARRICKFERGUS CASTLE 8 Minorca Place BT38 8AU Tesco Express TESCO CRESCENT LK DERRY EXP CRESCENT LINK ROAD BT47 5FX Tesco Supermarkets TESCO LISNAGELVIN LISNAGELVIN SHOP CENTR BT47 6DA Tesco Metro TESCO STRAND ROAD THE STRAND BT48 7PY Tesco Supermarkets TESCO LIMAVADY ROEVALLEY NI 119 MAIN STREET BT49 0ET Tesco Supermarkets TESCO LURGAN CARNEGIE ST MILLENIUM WAY BT66 6AS Tesco Supermarkets TESCO PORTADOWN MEADOW CTR MEADOW -

Celebrate the Life of Your Loved One with a Limited-Edition LOROS Forget Me Not Inside This Issue

LOROS For friends Summer 2018 and supporters Issue 8 matters of LOROS Hospice Celebrate the life of your loved one with a limited-edition LOROS Forget Me Not Inside this issue LOROS transforms as Phase Two takes shape 4 Welcome Join us to shape LOROS’ future 8 New appointment strengthens community services 9 This issue of LOROS and sailing with Matthew, Matters introduces our giving me a lifetime of Hospice Open Day – save the date! 10 brand new Forget Me Not happy memories to recall campaign, a wonderful and enjoy in a quiet Our fundraising promise 11 opportunity for people moment. Trish and Rob’s perfect day 12-13 to remember loved ones Exciting new Patrons The LOROS Forget Me in a very special way. It strikes me that LOROS bring star appeal 5 Not Flower Appeal 6-7 Leave LOROS a gift in your Will 16 “I will never It’s a major fundraising plays an important role in Join our volunteering team 17 forget my friend campaign for the Hospice helping families to gather and we hope that you will happy memories with their © 2018 LOROS All in a day’s work – the LOROS housekeepers 20-21 Matthew and support us by buying a loved ones at life’s end. LOROS, Groby Road, Community heroes 22-23 the lifetime flower to remember your The care that we strive to Leicester LE3 9QE special someone. provide includes time to Shantelle’s story 24-25 of wonderful talk, reflect and remember (0116) 231 3771 Choose charity, shop LOROS 26-27 I will be buying a Forget – a reservoir of memories [email protected] memories I have Me Not in memory of my that can provide comfort for Research at LOROS 28 of us out riding close friend Matthew, families long into the future. -

Blaby Retail Study Update 2012

Blaby District Council Blaby Retail Study Update 2012 THIS DOCUMENT IS FORMATTED FOR DOUBLE-SIDED PRINTING Date: July 2012 Amended by: SJR Principal changes: SJR/JW Final sign off: JW/MJ Contents 1 Introduction ............................................................................... 1 2 The Requirements of National and Regional Policy .............. 3 National Planning Policy Framework (2012) ............................................................. 3 3 Performance Analysis of Centres ........................................... 5 4 Current Patterns of Retail Spending ....................................... 7 Overall Catchment Area ........................................................................................... 7 Comparison and Convenience Goods Expenditure Patterns ..................................... 8 5 Quantitative Need in the Retail Sector .................................... 9 Methodology ............................................................................................................ 9 Catchment Population Forecasts .............................................................................. 9 Convenience Goods .............................................................................................. 10 Comparison Goods ................................................................................................ 13 Higher Population Growth Scenario........................................................................ 16 Expenditure Capacity – Convenience Goods ......................................................... -

Auction: Thursday 22Nd July 2021

Auction: Thursday 22nd July 2021 Welcome to our July 2021 online auction sale. This auction will be conducted behind closed doors. Buyers will be able to view the auction in real time and have the option to bid online, by telephone or by proxy. For those of who work closely with us will know that this sale will be our 5th Auction of 2021. Online Auctions have proved to be a great platform for both buyers and sellers and have meant that we have been able to offer an uninterrupted platform to continue during the pandemic. Which has been fantastic as with traditional room Auctions we have been selling properties by auction for over 29 years. The energies of the team at Kal Sangra,Shonki Brothers have remained high whilst we have adapted to remote auctions and socially distanced viewings amongst other measures we have had to put in place. Our online auctions over the past year I am delighted to say have averaged at a success rate of over 90%. The property market has shown great resilience during the challenges over the last year. Around 1.3 million buyers have benefitted from the stamp duty holidays since they were announced in July last year, according to Rightmove. I expect that house prices will continue in the right direction. The winding down of the stamp duty holiday will mean there will not be the rush to complete, I am sure conveyancers up and down the country will be giving out a huge sigh of relief as a sense to some kind of normality returns to their workload. -

City of Leicester Local Plan 1996-2016 Saved Policies Version

City of Leicester Local Plan (Incorporating the City of Leicester Minerals Local Plan) 1996 - 2016 ADOPTED JANUARY 2006 The Ordnance Survey mapping included within this publication is provided by Leicester City Council under licence from the Ordnance Survey in order to fulfi l its function to act as a Planning Authority. Persons viewing this mapping should contact Ordnance Survey Copyright for advice where they wish to licence Ordnance Survey mapping for their own use. Contents The list of contents includes all chapter headings, other headings and the titles of policies. Policy titles begin with the policy reference, e.g. PS01. How to use the Plan xi 1. Introduction 1 A Sustainable Direction for the City 2 The International Context 2 The National and Regional Context 3 The Local Context 4 Leicester’s People 5 Work 5 Social Exclusion 6 The Purpose and Nature of the Plan 6 Working in Partnership 6 2. Plan Strategy 9 Core Statement of General Policies 10 The Community Plan 10 A Rationale for the Plan Strategy 11 PS01. THE PLAN STRATEGY 12 Regeneration 13 PS02. REGENERATION AND COMPREHENSIVE DEVELOPMENT 16 The Principle of Comprehensive Development 16 Land Assembly 16 Integrating Planning and Transport 18 PS03. INTEGRATED PLANNING AND TRANSPORT STRATEGY 18 A Strategy for the City Centre 19 The Central Shopping Core 20 PS04. STRONG CITY CENTRE CORE 21 The New Business Quarter 21 PS05. CENTRAL OFFICE CORE (NEW BUSINESS QUARTER) 21 St. George’s Residential and Working Community 22 PS06. ST. GEORGE’S RESIDENTIAL AND WORKING COMMUNITY 23 Waterside 24 PS07. WATERSIDE 25 Science and Technology Based Business Park and Environs - Abbey Meadows 25 PS08. -

Charnwood Borough Council Retail and Town Centres Study

Charnwood Borough Council Retail and Town Centres Study December 2018 Final Report Prepared on behalf of WYG Environment Planning Transport Limited. Quay West at MediaCityUK, Trafford Wharf Road, Trafford Park, Manchester, M17 1HH Tel: +44 (0)161 872 3223 Fax: +44 (0)161 872 3193 Email: [email protected] Website: www.wyg.com WYG Environment Planning Transport Limited. Registered in England & Wales Number: 03050297 Registered Office: Arndale Court, Otley Road, Headingley, Leeds, LS6 2UJ Charnwood Retail and Town Centres Study Contents 1.0 Introduction .......................................................................................................... 4 1.1 Instruction ................................................................................................................. 4 1.2 Structure of Report ..................................................................................................... 5 2.0 Current and Emerging Retail and Leisure Trends ...................................................... 6 2.1 Introduction ............................................................................................................... 6 2.2 Polarisation and the Decline of Secondary Centres ........................................................ 6 2.3 The End of the ‘Big Four Space Race’ and the Rise of the Discounter ............................. 8 2.4 Special Forms of Trading ...........................................................................................11 2.5 Leisure and the Appetite for Additional Food and Drink ................................................13 -

0906 294 1113

Official Visitor Guide to Leicester & Leicestershire 2007 FREE To book your short break and get all the best deals, including family rooms from just £60 per night, visit www.goleicestershire.com or call 0906 294 1113 Calls cost 25p per minute Produced by In partnership with © Leicester Shire Promotions 2006 7-9 Every Street, Town Hall Square, Leicester LE1 6AG www.goleicestershire.com Great ideas for short breaks • Things to do • Accommodation • Great days out www.goleicestershire.com www.goleicestershire.com brought to you by Leicester Shire Promotions Market Harborough CONTENTS Great Ideas for 3-16 Go Beyond Your Getting Away Living Life to the 3 Full in Leicester Expectations The Fun has Just Begun 5 A Journey to Foodie Heaven 7 Town Hall Square Over a Thousand Years 9 of Adventure Belgrave Mela Get Fresh in the Great Outdoors 11 Leicester & Leicestershire’s Market Place 15 Leicestershire 17-45 Places to go If you haven’t already discovered Leicester and Leicestershire, Family Days Out 19 you’re in for a wonderful surprise! At the heart of England, Gardens, Parks & Nature 26 this county combines the finest English rural traditions with the cosmopolitan buzz of city life. Perfectly located, Leicestershire Museums & Galleries 30 is easy to find, but almost impossible to leave without savouring History & Heritage 34 at least some of its many delights. Waterways 38 Leicester’s continuing renaissance has created one of the UK’s Places to Shop & Eat 40 most cultural, creative and progressive cities. Visitors can witness Entertainment 44 this first-hand at cutting-edge visitor attractions like the National Space Centre and at a wide range of world-renowned events including the Leicester Comedy Festival, Summer Sundae 46-49 Events 2007 Weekender and the UK’s most spectacular Diwali celebrations. -

Retail and Town Centre Study 2008

Charnwood Borough Council RETAIL AND TOWN CENTRE STUDY FINAL REPORT September 2008 ROGER TYM & PARTNERS 3 Museum Square Leicester LE1 6UF t 0116 249 3970 f 0116 249 3971 e [email protected] w www.tymconsult.com This document is formatted for double-sided printing. CONTENTS 1 INSTRUCTIONS AND OUTLINE OF REPORT ................................................................... 1 Instructions ....................................................................................................................... .. 1 Structure of Remainder of Report ..................................................................................... .. 1 2 THE REQUIREMENTS OF NATIONAL PLANNING POLICIES ....................................... .. 3 Planning Policy Statement 6: Planning for Town Centres - March 2005 .......................... .. 3 Planning Policy Statement 12: Local Spatial Planning – June 2008 .................................. 11 Potential Changes to National Policy................................................................................ 12 Conclusion in Relation to Potential Changes to National Policy ....................................... 13 Proposed Changes to Planning Policy Statement 6: Planning for Town Centres Consultation July 2008 ..................................................................................................... 13 3 REGIONAL AND LOCAL POLICY CONTEXT.................................................................. 15 Regional Planning Policy ................................................................................................. -

Appendix 7 – Shopping Patterns and Quantitative Retail Capacity Tables

Appendix 7 – Shopping Patterns and Quantitative Retail Capacity Tables WYG PLANNING CHARNWOOD BOROUGH RETAIL STUDY TABLE 1A: POPULATION ZONE Population 2018 2023 2028 2033 2036 1 36,179 37,222 38,410 39,394 39,871 2 30,038 31,081 32,269 33,253 33,730 3 17,359 18,416 19,621 20,619 21,103 4 28,888 29,515 30,230 30,823 31,109 5 33,924 37,475 41,522 44,875 46,499 6 37,230 38,486 39,916 41,102 41,676 7 29,665 30,733 31,637 32,442 32,844 8 31,158 32,061 32,933 33,638 34,002 Study Area 244,441 254,989 266,539 276,147 280,835 TABLE 1B: CONVENIENCE EXPENDITURE PER CAPITA ZONE PER CAPITA EXPENDITURE CONVENIENCE (£) 2016 2016 2018 2023 2028 2033 2036 with SfT 1 1,869 1,815 1,795 1,783 1,781 1,782 1,786 2 2,038 1,979 1,957 1,945 1,942 1,944 1,947 3 2,024 1,965 1,943 1,931 1,929 1,930 1,934 4 2,000 1,942 1,920 1,908 1,906 1,907 1,911 5 2,044 1,985 1,963 1,950 1,948 1,949 1,953 6 2,097 2,036 2,014 2,001 1,998 2,000 2,004 7 2,306 2,239 2,214 2,200 2,197 2,199 2,203 8 2,265 2,199 2,175 2,161 2,158 2,160 2,164 Study Area Notes: a.