ANNUAL REPORT 2017 His Majesty King Abdullah II

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Time Needed to Assess Environmental Impact of Water Shortage. Case Study: Jerash Governorate / Jordan

IOSR Journal of Environmental Science, Toxicology and Food Technology (IOSR-JESTFT) e-ISSN: 2319-2402,p- ISSN: 2319-2399.Volume 10, Issue 7 Ver. III (July 2016), PP 58-63 www.iosrjournals.org Time needed to assess environmental impact of water shortage. case study: Jerash governorate / Jordan . Eham S. Al-Ajlouni Public Health Department, Health Sciences College, Saudi Electronic University, Jeddah, Saudi Arabia. Abstract:Time needed to measure environmental impact varies according to the field (economic, financial, health, education, social, ..) and to the subject (project, policy, disease, program, ..) . The aim of this work was determining time duration needed to assess environmental impact of water shortage. Water share in Jerash governorate is only 71 litres per day per person, which is very low. So, cluster survey was applied, official records during 2000 – 2011 were reviewed and drinking water samples were analyzed. Water analysis data showed slight or no impact on ammonia, fluoride, and lead levels in water; and on pH and salinity of water; but there was high level of nitrate in water. Furthermore, national reports showed increased level of salinity of soil, however data of Total Dissolved Solids and pH of soil were officially not available. It was concluded that to show the negative impacts of water shortage on water quality and soil, time duration should be beyond 20 years. Moreover, salinity of soil could be indirectly affected by water shortage through over pumping and pollution, but mainly affected by agricultural practices and climate. Keywords:Environmental impact assessment; Falkenmark indicator; Jerash governorate; Time duration ;Water shortage. I. Introduction Duration of time frame to show positive or negative effects of a treatment, a project, a program, or a policy, is varied. -

Disaster Risk Reduction Assessment Understanding Livelihood Resilience in Jordan

Jordan Cover photo: Arabah, Jordan Rift Valley © Michael Privorotsky, 2009 DISASTER RISK REDUCTION ASSESSMENT UNDERSTANDING LIVELIHOOD RESILIENCE IN JORDAN ASSESSMENT REPORT NOVEMBER 2016 Contents Executive Summary 3 List Of Acronyms 7 Geographical Classifications 8 Introduction: Context And Objectives 9 Methodology 12 Findings 17 Socio-Economic Challenges And Risks 19 Environmental Challenges And Risks 26 Livelihood Resilience: Trends Over Time 32 Challenges Faced In Risk Mitigation And Preparedness 32 Summary 34 Conclusion And Recommendations 36 Annex 1: Focus Group Discussion Question Route 40 Annex 2: Elevation, Landcover, Sloping Maps Used For Zoning Exercise 45 Annex 3: Livelihood Zones In Jordan (Participatory Mapping Exercise) 48 Annex 4: Risk Perceptions Across Jordan 49 2 Executive Summary Context According to the INFORM 2016 risk index,1 which assesses global risk levels based on hazard exposure, fragility of socio- economic systems and insufficient institutional coping capacities, Jordan has a medium risk profile, with increasing socio-economic vulnerability being a particular area of concern.2 Since 1990, Jordan has also experienced human and economic losses due to flash floods, snowstorms, cold waves, and rain which is indicative of the country’s vulnerability to physical hazards.3 Such risk factors are exacerbated by the fact that Jordan is highly resource-constrained; not only is it semi-arid with only 2.6% of arable land,4 but it has also been ranked as the third most water insecure country in the world.5 Resource scarcity aggravates vulnerabilities within the agriculture sector which could have severe implications given that agriculture provides an important means of livelihood for 15% of the country’s population, primarily in rural areas.6 Resilience of agriculture is also closely linked to food and nutrition security. -

Subnational Governance in Jordan

THE INSTITUTE FOR MIDDLE EAST STUDIES IMES CAPSTONE PAPER SERIES CENTRALIZED DECENTRALIZATION: SUBNATIONAL GOVERNANCE IN JORDAN GRACE ELLIOTT MATT CIESIELSKI REBECCA BIRKHOLZ MAY 2018 THE INSTITUTE FOR MIDDLE EAST STUDIES THE ELLIOTT SCHOOL OF INTERNATIONAL AFFAIRS THE GEORGE WASHINGTON UNIVERSITY © OF GRACE ELLIOTT, MATT CIESIELSKI, REBECCA BIRKHOLZ, 2018 Table of Contents Introduction 1 Literature Review: Decentralization and 3 Authoritarian Upgrading Methodology 7 Local Governance in Jordan 9 Political Economy and Reform 12 Decentralization in Jordan 15 Decentralization as a Development Initiative 20 Political Rhetoric 28 Opportunities and Challenges 31 Conclusion 35 Works Cited 37 Appendix 41 1 Introduction Jordan is one of the last bastions of stability in an otherwise volatile region. However, its stability is threatened by a continuing economic crisis. In a survey conducted across all twelve governorates in 2017, only 22% of citizens view Jordan’s overall economic condition as “good” or “very good” compared to 49% two years ago.1 Against this backdrop of economic frustration, Jordan is embarking on a decentralization process at the local level in an attempt to bring decision-making closer to the citizen. In 2015, Jordan passed its first Decentralization Law, which continued calls from King Abdullah II dating back to 2005 to “enhance our democratic march and to continue the process of political, economic, social and administrative reform” by encouraging local participation in the provision of services and investment priorities.2 This is the latest in a series of small steps taken by the central government intended to improve governance at the local level and secure long-term stability in the Kingdom. -

Jordan Contents Executive Summary

FEBRUARY 24, 2020 LAND USE MEASURES TO SUSTAIN TRADITIONAL USES OF THE PRODUCTIVE LANDSCAPE IN DIBEEN KBA SITUATION ANALYSIS AND MEASURES IDENTIFICATION AMJAD AND MAJDI SALAMEH COMPANY ENVIROMATICS Amman, Jordan Contents Executive summary ................................................................................................................ 3 Chapter 1 Present Situation and Trends ................................................................................. 5 Land cover and ecological character of the study area ............................................................... 5 Closed old-growth forests ....................................................................................................... 5 Open old-growth forests ......................................................................................................... 5 Non-forest Mediterranean habitats (also referred to as marginal undeveloped land) .......... 6 Planted (Man-made) forests ................................................................................................... 6 Wadi systems ........................................................................................................................... 6 Zarqa River and King Talal Dam ............................................................................................... 6 Mix-use rural agricultural areas (Orchids) and Farmlands (crop plantations) ........................ 7 Urban areas ............................................................................................................................ -

Women's Political Participation in Jordan

MENA - OECD Governance Programme WOMEN’S Political Participation in JORDAN © OECD 2018 | Women’s Political Participation in Jordan | Page 2 WOMEN’S POLITICAL PARTICIPATION IN JORDAN: BARRIERS, OPPORTUNITIES AND GENDER SENSITIVITY OF SELECT POLITICAL INSTITUTIONS MENA - OECD Governance Programme © OECD 2018 | Women’s Political Participation in Jordan | Page 3 OECD The mission of the Organisation for Economic Co-operation and Development (OECD) is to promote policies that will improve the economic and social well-being of people around the world. It is an international organization made up of 37 member countries, headquartered in Paris. The OECD provides a forum in which governments can work together to share experiences and seek solutions to common problems within regular policy dialogue and through 250+ specialized committees, working groups and expert forums. The OECD collaborates with governments to understand what drives economic, social and environmental change and sets international standards on a wide range of things, from corruption to environment to gender equality. Drawing on facts and real-life experience, the OECD recommend policies designed to improve the quality of people’s. MENA - OECD MENA-OCED Governance Programme The MENA-OECD Governance Programme is a strategic partnership between MENA and OECD countries to share knowledge and expertise, with a view of disseminating standards and principles of good governance that support the ongoing process of reform in the MENA region. The Programme strengthens collaboration with the most relevant multilateral initiatives currently underway in the region. In particular, the Programme supports the implementation of the G7 Deauville Partnership and assists governments in meeting the eligibility criteria to become a member of the Open Government Partnership. -

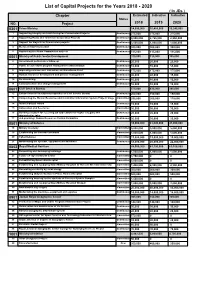

List of Capital Projects for the Years 2018 - 2020 ( in Jds ) Chapter Estimated Indicative Indicative Status NO

List of Capital Projects for the Years 2018 - 2020 ( In JDs ) Chapter Estimated Indicative Indicative Status NO. Project 2018 2019 2020 0301 Prime Ministry 14,090,000 10,455,000 10,240,000 1 Supporting Integrity and Anti-Corruption Commission Projects Continuous 275,000 275,000 275,000 2 Supporting Radio and Television Corporation Projects Continuous 9,900,000 8,765,000 8,550,000 3 Support the Royal Film Commission projects Continuous 3,500,000 1,000,000 1,000,000 4 Media and Communication Continuous 300,000 300,000 300,000 5 Supporting the Media Commission projects Continuous 115,000 115,000 115,000 0501 Ministry of Public Sector Development 310,000 310,000 305,000 6 Government performance follow up Continuous 20,000 20,000 20,000 7 Public sector reform program management administration Continuous 55,000 55,000 55,000 8 Improving services and Innovation and Excellence Fund Continuous 175,000 175,000 175,000 9 Human resources development and policies management Continuous 40,000 40,000 35,000 10 Re-structuring Continuous 10,000 10,000 10,000 11 Communication and change management Continuous 10,000 10,000 10,000 0601 Civil Service Bureau 575,000 435,000 345,000 12 Enhancement of institutional capacities of Civil Service Bureau Continuous 200,000 150,000 150,000 13 Completing the Human Resources Administration Information System Project/ Stage Committed 290,000 200,000 110,000 2 14 Ideal Employee Award Continuous 15,000 15,000 15,000 15 Automation and E-services Committed 30,000 30,000 30,000 16 Building a system for receiving job applications for higher category and Continuous 20,000 20,000 20,000 administrative jobs. -

Development Report 2015

Empowered lives. Resilient nations. JORDAN HUMAN DEVELOPMENT REPORT 2015 REGIONAL DISPARITIES JORDAN HUMAN DEVELOPMENT REPORT 2015 Regional Disparities Jordan Human Development Report 2015: Regional Disparities Project Board Members Mukhallad Omari, Ministry of Planning and International Cooperation Zena Ali Ahmad, UNDP-Jordan Mohammad Nabulsi, Economic and Social Council National Reviewers Mukhallad Omari, Ministry of Planning and International Cooperation Basem Kanan, Ministry of Planning and International Cooperation Diya Elfadel, UNDP-Jordan Zein Soufan, Ministry of Planning and International Cooperation Orouba Al-Sabbagh, Ministry of Planning and International Cooperation Raedah Frehat, Jordanian National Commission for Women Junnara Murad, Development and Employment Fund Ahmad Al-Qubelat, Department of Statistics Maisoon Amarneh, Jordan Economic and Social Council Osama Al-Salaheen, Ministry of Social Development Reem Al-Zaben, Jordanian Hashemite Fund for Human Development Ali Al-Metleq, The Higher Population Council Laith Al-Qasem Abdelbaset Al-Thamnah, Department of Statistics JORDAN HUMAN DEVELOPMENT REPORT 2015 1 Jordan Human Development Report 2015: Regional Disparities International reviewers Selim Jahan, Director, Human Development Report Ofce Jon Hall, Policy Specialist, National Human Development Reports, UNDP Consultants Core Team of Writers Khalid W. Al-Wazani- Chief Researcher and Team Leader (Issnaad Consulting) Ahmad AL-Shoqran, Report Coordinator (Issnaad Consulting) Ibrahim Aljazy Alaa Bashaireh Other Participating Experts Fawaz Al-Momani Abdallah Ababneh Abdelbaset Al-Thamnah Fairouz Aldahmour Mohammad Bani Salameh Naser Abu Zayton Hani Kurdi Mohammad Nassrat Salma Nims Survey Team Naser Abu Zayton Taqwah Saleh Ebtisam Abdullah Issnaad Consulting Management advisory services Ahmad Hindawi Lara Khozouz Lana Mattar Taqwah Saleh 2 JORDAN HUMAN DEVELOPMENT REPORT 2015 Jordan Human Development Report 2015: Regional Disparities Jordan Human Development Report 2015: Regional Disparities No. -

![Support to the Municipalities Affected by the Influx of Syrian Refugees in Jordan [PHASE 2]](https://docslib.b-cdn.net/cover/5220/support-to-the-municipalities-affected-by-the-influx-of-syrian-refugees-in-jordan-phase-2-4455220.webp)

Support to the Municipalities Affected by the Influx of Syrian Refugees in Jordan [PHASE 2]

SUPPORT TO THE MUNICIpaLITIes AFFECTED BY THE INFLUX OF SYRIAN REFugees IN JORDAN [PHASE 2] • Increased social cohesion and environment protection, AICS Amman works jointly with Jordanian Institutions on: GOVERNANCE through the provision of equipment, rehabilitation of infrastructure and quality improvement of urban life • Support to local municipalities on service delivery • Support to social cohesion in the municipal territory; • Rehabilitation of infrastructures PROGRAMME SUMMARY The “Support to the municipalities affected by the influx of Syrian refugees in Jordan” programme aims to improve Sector | Governance living conditions of the population in the municipalities of Status | Ongoing Syria’s neighbouring Governorates, which are particularly affected by the concentration of refugees seeking shelter Funded in | 2017 across the border. Budget | € 1,500,000.00 The intervention aims to ensure: • Restored health care services through the provision Implementing Partners| Ministry of Municipal of medical equipment supply and/or medicines in Affairs (MoMA) hospitals and health centres; Beneficiaries | Municipalities of Jerash • Improved education services for refugees and the most vulnerable Jordanian population in Jordan’s (Jerash Governorate); Junaid (Ajloun public schools, through the acquisition of goods and Governorate); Al- Halabat, Dhlail (Zarqa restoration of school facilities; Governorate). • Increased social cohesion and environment protection, through the provision of equipment, rehabilitation of infrastructure and quality 8 interventions 4 municipalities improvement of urban life in the municipal territory; • Enhanced access to health and hygiene services for school rehabilitation/maintenance Syrian refugees and the most vulnerable Jordanian youth centre construction population, through improved planning process of library/public spaces restoration health services, as well as rehabilitation of medical medical equipment supply infrastructure and waste management system. -

Jordan Poverty Reduction Strategy 2013

January 1, 2013 JORDAN POVERTY REDUCTION STRATEGY 28 JANUARY 2013 Jordan Poverty Reduction Strategy Final Report 2013 1 UNDP January 1, 2013 JORDAN POVERTY REDUCTION STRATEGY CONTENTS His Majesty King Abdullah II ibn Al Hussein ......................................................................................................... 4 (ii) Foreword ..................................................................................................................................................................... 5 EXECUTIVE SUMMARY ................................................................................................................................................... 6 1. APPROACHING POVERTY REDUCTION IN JORDAN ................................................... 13 1.1 The Aim and Scope of PRS .................................................................................................................................. 13 1.2 Measuring Poverty ................................................................................................................................................ 23 1.3 Jordan Integrated Outreach Worker Program ........................................................................................... 29 2. THE CONTEXT ............................................................................................................................ 31 2.1 Jordan’s Changing Social and Economic Environment ............................................................................ 31 2.2 Poverty, Inequality and -

Governorates Budgets According to the Determined Ceiling

Total of Capital Expenditures Distributed According to the Determined Ceilings for the Fiscal Year 2018 ( In JDs ) Expenditures of GOVERNORATE Sustaining the Capital Total Work of the Expenditures Governorates Councils Irbid Governorate 372,000 22,981,000 23,353,000 Mafraq Governorate 325,000 18,952,000 19,277,000 Jerash Governorate 176,000 14,974,000 15,150,000 Ajloun Governorate 189,000 15,818,000 16,007,000 The Capital Governorate 474,000 34,464,000 34,938,000 Balqa' Governorate 216,000 16,400,000 16,616,000 Zarqa Governorate 284,000 20,322,000 20,606,000 Ma'daba Governorate 162,000 13,691,000 13,853,000 Karak Governorate 230,000 14,361,000 14,591,000 Ma'an Governorate 162,000 19,121,000 19,283,000 Tafileh Governorate 155,000 13,785,000 13,940,000 Aqaba Governorate 155,000 15,131,000 15,286,000 Total 2,900,000 220,000,000 222,900,000 Budget Summary of Irbid Governorate for the Years 2018 - 2020 ( In JDs) Description Estimated Indicative Indicative 2018 2019 2020 Expenditures of Sustaining the Work of the Governorate Council 372,000 385,000 385,000 Capital Expendituers 22,981,000 23,967,000 25,733,000 Total 23,353,000 24,352,000 26,118,000 Appropriations of Sustaining the Council Work of Irbid Governorate for the Years 2018 - 2020 ( In JDs) Description Estimated Indicative Indicative 2018 2019 2020 001 Council of Irbid Governorate 372,000 385,000 385,000 001 Bonuses 312,000 312,000 312,000 004 Hospitality 3,900 3,900 3,900 999 Others 56,100 69,100 69,100 Total 372,000 385,000 385,000 Capital Budget for Irbid Governorate for the years -

Emerging Trends in the Jordanian Host Community

Journal of Sociology and Social Work December 2019, Vol. 7, No. 2, pp. 115-125 ISSN: 2333-5807 (Print), 2333-5815 (Online) Copyright © The Author(s). All Rights Reserved. Published by American Research Institute for Policy Development DOI: 10.15640/jssw.v7n2a12 URL: https://doi.org/10.15640/jssw.v7n2a12 Emerging trends in the Jordanian Host Community: Service Delivery Gaps, Ethnographic Shifts and Social Tension: a Field Study in the Governorates of Jerash and Ajloun Dr. Basem Al Atom1 Abstract This field research study examines the underlying causes of social tension between Syrian refugees and the Jordanian host community in Northern Jordan. It does so, moreover, within the framework of the current shift being undertaken by international and local non-governmental organizations from an emergency response to Syrian refugees to a development response. Specifically, such a shift brings with it an increased focus on livelihoods as a means of sustainable economic empowerment. With a focus on livelihoods, however, comes an increase in the potential for tension between employers and employees. Furthermore, this tension complements an already-existing tension that exists between landlords and tenants. Understanding the sources of these types of conflict will help mitigate against future tensions and better facilitate social cohesion amongst Syrian refugees and the Jordanian host community. Keywords: Syrian refugees, host communities, social cohesion, social tension, dispute resolution 1. Introduction This research study provides an overview and analysis of research undertaken between February 2018 and April 2018. The purpose of this report is to examine the underlying causes of social tension between Syrian refugees and the Jordanian host community in Northern Jordan, and to help mitigate against future tensions and better facilitate social cohesion between these two communities. -

The Effect of Water Shortage on Water Quality of Different Resources in Jerash Governorate/Jordan, Based on New Water Quality Index

Eham Al-Ajlouni et al. Int. Journal of Engineering Research and Application www.ijera.com ISSN : 2248-9622, Vol. 6, Issue 6, ( Part -4) June 2016, pp.36-48 RESEARCH ARTICLE OPEN ACCESS The Effect of Water Shortage on Water Quality of Different Resources in Jerash Governorate/Jordan, Based On New Water Quality Index Eham Al-Ajlouni1*, Samia Abdel Hamid2, Linda Saad2, Mohammad Subbarini3, Ashraf Wahdan4. 1Public Health Department, Health Sciences College, Saudi Electronic University, Jeddah. Saudi Arabia. 2Department of Environmental Health, High Institute of Public Health, University Of Alexandria, Egypt. 3President of Irbid National University (Inu), Irbid, Jordan. 4Department of Biostatistics, High Institute of Public Health, University Of Alexandria, Egypt. ABSTRACT The individual average of water share In Jerash governorate is only 71 litres per day and that is the lowest allotment in Jordan. The aim of the study is to assess water quality of different resources in Jerash governorate, based on demographic, chemical and biological changes within a period of 11 years. Cluster survey method was applied and samples of drinking water were taken from different resources. Water of municipality and bottled groundwater resources were of acceptable quality; groundwater of tanker trucks and wells were also acceptable except that of high level of nitrate; spring water and harvested rainwater were potentially not safe and susceptible for biological contamination. At level of sub-districts, based on a new developed water quality index, it was chemically found that water in Mastaba sub-district was more complying with standards than Jerash and Burma sub-districts, but in biological respect both Jerash and Burma sub-districts were more compliance with the standards than Mastaba sub-district.