1997 Annual Report Our Objective

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Safe Snack List

Commonly Available Snacks Free of Peanuts, Tree Nuts and Eggs Content Updated: October 15, 2015 Halloween Edition This copy was downloaded: October 20, 2015 Do not use this copy after: November 2, 2015 After this date, download an updated copy from: snacksafely.com/download Please read and understand this entire page before using this guide. Your use of this guide indicates that you have read and understand the disclaimer below and accept and agree to its limitations. DISCLAIMER: ALL INFORMATION REGARDING INGREDIENTS AND MANUFACTURING PROCESSES WERE COMPILED FROM CLAIMS MADE BY THE PRODUCTS’ RESPECTIVE MANUFACTURERS ON THEIR LABELS OR VIA OTHER MEANS AND MAY ALREADY BE OUT OF DATE. ALTHOUGH EVERY EFFORT HAS BEEN MADE TO BE AS ACCURATE AS POSSIBLE, WE DO NOT ACCEPT ANY LIABILITY FOR ERRORS OR OMISSIONS MADE BY US OR THE PRODUCTS’ RESPECTIVE MANUFACTURERS. THIS LIST IS FOR INFORMATIONAL PURPOSES ONLY AND IS INTENDED TO SERVE AS A GUIDE, NOT AS AN AUTHORITATIVE SOURCE, AND IS NOT INTENDED TO REPLACE THE ADVICE OF ANY MEDICAL PROFESSIONAL. PRIOR TO PURCHASING ANY LISTED FOOD ITEM, IT IS YOUR RESPONSIBILITY TO CHECK THE PRODUCT LABEL TO ENSURE THAT UNDESIRED ALLERGENS ARE NOT LISTED AS INGREDIENTS AND TO VERIFY WITH THE MANUFACTURER THAT TRACE AMOUNTS OF UNDESIRED ALLERGENS WERE NOT INTRODUCED DURING THE MANUFACTURING PROCESS. CURRENT FDA LABELING GUIDELINES DO NOT MANDATE MANUFACTURERS DISCLOSE POTENTIAL ALLERGENS THAT MAY BE INTRODUCED AS PART OF THE MANUFACTURING PROCESS. Meaning of the symbols: For items preceeded by green symbols, the information was provided by the manufacturer on their packaging, promotional literature, website, or directly to us. -

Kraft Foods Inc(Kft)

KRAFT FOODS INC (KFT) 10-K Annual report pursuant to section 13 and 15(d) Filed on 02/28/2011 Filed Period 12/31/2010 UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 (Mark one) FORM 10-K [X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2010 OR [ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 COMMISSION FILE NUMBER 1-16483 Kraft Foods Inc. (Exact name of registrant as specified in its charter) Virginia 52-2284372 (State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.) Three Lakes Drive, Northfield, Illinois 60093-2753 (Address of principal executive offices) (Zip Code) Registrant's telephone number, including area code: 847-646-2000 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Class A Common Stock, no par value New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x Note: Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from their obligations under those Sections. -

Kraf Tunion Network 02102011

Kraft Union Network October 2, 2011 There’s always something going on at Kraft Foods… Kraft to split itself in two We believe scale will be an increasing source of competitive advantage both in confectionary and in the food industry at large. Irene Rosenfeld, January 2010, Taking our performance to the next level requires a bold new approach: creating two great companies that can optimize value by focusing on their unique drivers of success. Irene Rosenfeld, August 2011 The deals never stop at Kraft foods. On the road to moving from “one of the world’s largest food and beverage companies” to a “global snacks powerhouse”, Kraft in 2007 paid USD 7.2 billion, to acquire Danone’s European biscuit operations, borrowing cash it didn’t have. Kraft steadily raised dividends while closing over 35 factories and eliminating over 20,000 jobs, squeezing out cash through closures, spinoffs and outsourcing, Cost-cutting, layoffs and divestitures fueled more dividend increases and paved the way for even more debt to power the USD 19.5 billion cash-and-share acquisition of UK-based Cadbury in 2010. “Scale”, “supply chain leverage” and marketing “synergies” were the rationale for the Cadbury deal, trotted out in innumerable press releases and conference calls with investors. Synergy and scale yielded to “focus” on August 4 this year, when Kraft announced it would split the corporation into 2 independent publicly traded companies, both headquartered in North America: “A high-growth global snacks business with estimated 2 revenue of approximately $32 billion and a high-margin North American grocery business with estimated revenue of approximately $16 billion. -

Enel Green Power's Renewable Energy Is Part of the History of Mondelēz International's Business Unit in Mexico

Media Relations T (55) 6200 3787 [email protected] enelgreenpower.com ENEL GREEN POWER'S RENEWABLE ENERGY IS PART OF THE HISTORY OF MONDELĒZ INTERNATIONAL'S BUSINESS UNIT IN MEXICO • Enel Green Power supplies up to 77 GWh annually to two Mondelēz International factories with wind energy from its 200 MW Amistad I wind farm located in Ciudad Acuña, Coahuila. • Thanks to this relationship, Mondelēz International has avoided the emission of approximately 33,000 tons of CO2 per year. Mexico City, October 7th, 2020 – Enel Green Power México (EGPM), the renewables subsidiary of Enel Group, joins the celebration of the 8th anniversary of Mondelēz International in the country, by commemorating two years of successful collaboration through an electric power supply contract. Derived from this contract, Mondelēz International has received up to 77 GWh per year of renewable energy to its factories located in the State of Mexico and Puebla. Thanks to the renewable energy supplied by EGPM´s Amistad I wind farm; Mondelēz International has avoided the emission of around 33,000 tons of CO2 per year, equivalent to almost 80% of its emission reduction target for Latin America in 2020. Similarly, this energy is capable of producing approximately more than 100,000 tons annually of product from brands such as Halls, Trident, Bubbaloo, Oreo, Tang and Philadelphia and is enough to light approximately 33,000 Mexican homes for an entire year. “It is an honor for Enel Green Power México to contribute to Mondelēz International environmental objectives and efforts to accelerate energy transition in the country. Today more and more companies are convinced that renewable energies are not only sustainable, but also profitable, which is why this type of agreements serve as a relevant growth path for clean sources in Mexico”, stated Paolo Romanacci, Country Manager of Enel Green Power Mexico. -

Kelly Promo's

1921 - 2021 Kelly Promo’s 1921 - 2021 Kelly Promo’s SeptemberSeptember 4th 4th to to October October 1st, 1st, 2021 2021 NEW - HALLOWEEN SEASONAL CANDY NOW ON SALE! Page 23 NEW - FOOD & SNACKS Page 16 Page Page Page Page Page 15 15 33 14 5 NEWWelch’s - FruitBEVERAGES & Yogurt Tubes NEW - CANDY Gondola Topper Rack 3 SKU’s Kit #400904 $15 Semi Annual Rack Payment Total Retail: $94.50 Average Cost: $57.50 Profit Dollars: $37.00 Product Turns: 4 Incremental Dollars: $148.00 Placement Item # Description Pack Size Shelf 1 517020 Welch's Fruit 'n Yogurt-Strawberry 10 1.8 oz Dimensions: 41”W x 8”D x 13”H Shelf 2 517020Page Welch's Fruit 'n Yogurt-Strawberry 10 1.8 oz Page Page Page Page Page Shelf 3 5170037 Welch's Fruit 'n Yogurt-Blueberry 10 1.8 oz 30 31 28 25 24 Shelf 4 517011 Welch's Fruit 'n Yogurt-Mango 10 1.8 oz Shelf 5 517011 Welch's Fruit 'n Yogurt-Mango 10 1.8 oz Rack 414760 Gondola Topper Rack 3 SKU's 1 Empty NEWHalls 9- box CCS Counter RACKS Rack | Kit #516678 NEW - HBA, TOBACCO & AUTO $20 Semi Annual Rack Payment Welch’s Fruit & Yogurt Tubes Gondola Topper Rack 3 SKU’s Total Retail: $311.19 Kit #400904 Average Cost: $192.94 Profit Dollars: $118.25 $15 Semi Annual Rack Payment Product Turns: 3 Incremental Dollars: $354.75 Total Retail: $94.50 Placement Item # Description Pack Size Average Cost: $57.50 1 508586 Halls Mini S/F Menthol-Lyptus 8 24 Profit Dollars: $37.00 Peg 2 508578 Halls Mini S/F Honey Lemon 8 24 Product Turns: 3 508560 Halls Mini S/F Cherry 8 24 4 1 69698 Halls Honey Lemon 20 9 Incremental Dollars: $148.00 1st Shelf -

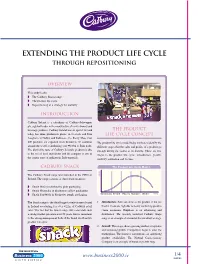

Extending the Product Life Cycle Through Repositioning

CADBURY V-5 9/8/05 1:38 PM Page 1 Extending the Product Life cycle through Repositioning Overview This study looks: ! The Cadbury Snack range ! The product life cycle ! Repositioning as a strategy for maturity introduction Cadbury Ireland is a subsidiary of Cadbury-Schweppes plc, a global leader in the manufacture of confectionery and beverage products. Cadbury Ireland was set up in 1932 and The Product today has three production plants, in Coolock and Dun Life Cycle concept Laoghaire in Dublin and Rathmore, Co. Kerry. More than 200 products are exported from Ireland to 30 countries The product life cycle model helps marketers identify the ! around the world, contributing over 110m to Irish trade. different stages that the sales and profits of a product go The distinctive taste of Cadbury Ireland’s products is due through during the course of its lifetime. There are five to the use of local ingredients and the company is one of stages to the product life cycle: introduction, growth, the largest users of indigenous Irish materials. maturity, saturation and decline. Cadbury Snack The Product Life Cycle Model The Cadbury Snack range was launched in the 1950s in SALES Ireland. The range consists of three main products: ! Snack Wafer in distinctive pink packaging ! Snack Shortcake in distinctive yellow packaging ! Snack Sandwich in distinctive purple packaging Introduction Growth Maturity Saturation Decline TIME The Snack range is the third biggest confectionery brand 1. Introduction: Sales are slow as the product is not yet in Ireland accounting for over !22m of Cadbury retail known. Costs are high due to heavy marketing spend to sales. -

Chocolate Bars in Their Wrappers

Welcome to the 1st Toftwood Brownies - Chocolate Challenge An activity pack for all sections. Here at 1st Toftwood Brownies we absolutely love our chocolate – cooking with it and definitely eating it! That’s why we have decided to make our very own Chocolate Challenge Badge. There are recipes, games and activities that we have tried and tested (some are old Guiding favourites that have been adapted, others we’ve come up with ourselves). The Challenge consists of 5 different sections. We suggest that to gain the badge Rainbows complete 6, Brownies complete 8, Guides complete 10 and Senior Section and Adults complete 10 or more of the challenges, in each case with at least one challenge being completed from each section. The sections are: - Section 1 – a selection of chocolate based games - Section 2 – a selection of puzzles and activities - Section 3 – yum, yum – a selection of chocolate recipes to try - Section 4 – a chocoholic’s dream – tasting activities - Section 5 – crafty chocolate + invention time You could use this badge during your meeting time or perhaps as part of an activity day or sleepover. Once you have finished, send off for your badges (see order form at the back of this booklet). We hope you enjoy yourselves whilst completing this challenge! Take a look at our website for a copy of the pack and pictures of Rainbows, Brownies and Guides taking part in the challenge www.1sttoftwoodbrownies.btck.co.uk SECTION 1: Chocolate Games Chocolate Games Have a go at some of these games with a chocolate theme: The Chocolate Game All you need for this game is a bar of chocolate (Cadburys Dairy Milk or Galaxy work best), a hat, scarf, pair of gloves, 2 dice, a plate and knives and forks. -

1999 Annual Report

CORE Metadata, citation and similar papers at core.ac.uk Provided by Diposit Digital de Documents de la UAB Annual Report and Form 20-F 1999 Contents Page Strategy Statement 1 Corporate Highlights 2 Financial Highlights 3 1 Business Review 1999 5 2 Description of Business 23 3 Operating and Financial Review 33 4 Report of the Directors 57 5 Financial Record 77 6 Financial Statements 83 7 Shareholder Information 131 Glossary 141 Cross reference to Form 20-F 142 Index 144 The images used within this Annual Report and Form 20-F are taken from advertising campaigns and websites which promote our brands worldwide. They demonstrate how we communicate the appeal of our brands in a wide range of markets. “Sunkist” is a registered trademark of Sunkist Growers, Inc. This is the Annual Report and Form 20-F of Cadbury Schweppes public limited company for the year ended 2 January 2000. It contains the annual report and accounts in accordance with UK generally accepted accounting principles and regulations and incorporates the annual report on Form 20-F for the Securities and Exchange Commission in the US. A Summary Financial Statement for the year ended 2 January 2000 has been sent to all shareholders who have not elected to receive this Annual Report and Form 20-F. The Annual General Meeting will be held on Thursday, 4 May 2000. The Notice of Meeting, details of the business to be transacted and arrangements for the Meeting are contained in the separate Annual General Meeting booklet sent to all shareholders. The Company undertook a two for one share split in May 1999. -

Case with Questions J Cadbury 1

j Case with questions Cadbury 1 Cadbury is a very well known British confectionery company. Originally a family fi rm started by John Cadbury and grounded in Quaker values and ideals, it started life in 1824 as a shop selling chocolate as a virtuous alternative to alcohol. It went on to become a large-scale manufacturer of chocolate based at the now legendary Bournville factory, built in 1879, and its picturesque workers’ village with its red-brick terraces, cottages, duck ponds and wide open parks. Over the next 100 years Cadbury developed the products that have become so familiar: Dairy Milk in 1905, Milk Tray in 1915, Flake in 1920, Creme Egg in 1923, Roses in 1938 and more. From 1969 it traded as Cadbury Schweppes plc until, in 2008, it separated its global con- fectionery business (which retained the name ‘Cadbury’) from its US beverages business, which was renamed Dr Pepper Snapple Group Inc. Cadbury Schweppes had already sold off most of its beverages businesses in other countries around the world, a process started in 1999 and concluded in 2009 with the sale of its Australian beverages business. The reason for the exit from the beverages business was to enable Cadbury to focus more clearly on what it saw as its core strengths in confectionery, and better enhance shareholder value. Beverages had become the ‘poor sister’ in the relationship, with a separate management structure but delivering growth below the targets for the company. In 2008 the newly de-merged Cadbury set as its goal maintaining its market leadership position, and leveraging its scale and advantaged positions so as to maximise growth and returns. -

Kosher Nosh Guide Summer 2020

k Kosher Nosh Guide Summer 2020 For the latest information check www.isitkosher.uk CONTENTS 5 USING THE PRODUCT LISTINGS 5 EXPLANATION OF KASHRUT SYMBOLS 5 PROBLEMATIC E NUMBERS 6 BISCUITS 6 BREAD 7 CHOCOLATE & SWEET SPREADS 7 CONFECTIONERY 18 CRACKERS, RICE & CORN CAKES 18 CRISPS & SNACKS 20 DESSERTS 21 ENERGY & PROTEIN SNACKS 22 ENERGY DRINKS 23 FRUIT SNACKS 24 HOT CHOCOLATE & MALTED DRINKS 24 ICE CREAM CONES & WAFERS 25 ICE CREAMS, LOLLIES & SORBET 29 MILK SHAKES & MIXES 30 NUTS & SEEDS 31 PEANUT BUTTER & MARMITE 31 POPCORN 31 SNACK BARS 34 SOFT DRINKS 42 SUGAR FREE CONFECTIONERY 43 SYRUPS & TOPPINGS 43 YOGHURT DRINKS 44 YOGHURTS & DAIRY DESSERTS The information in this guide is only applicable to products made for the UK market. All details are correct at the time of going to press but are subject to change. For the latest information check www.isitkosher.uk. Sign up for email alerts and updates on www.kosher.org.uk or join Facebook KLBD Kosher Direct. No assumptions should be made about the kosher status of products not listed, even if others in the range are approved or certified. It is preferable, whenever possible, to buy products made under Rabbinical supervision. WARNING: The designation ‘Parev’ does not guarantee that a product is suitable for those with dairy or lactose intolerance. WARNING: The ‘Nut Free’ symbol is displayed next to a product based on information from manufacturers. The KLBD takes no responsibility for this designation. You are advised to check the allergen information on each product. k GUESS WHAT'S IN YOUR FOOD k USING THE PRODUCT LISTINGS Hi Noshers! PRODUCTS WHICH ARE KLBD CERTIFIED Even in these difficult times, and perhaps now more than ever, Like many kashrut authorities around the world, the KLBD uses the American we need our Nosh! kosher logo system. -

Gum * Bubble/Kids/Novelty Types- (0200) Gum * Mini Packs

PAGE : 1 SOLD TO CUST NO. DATE : _______________ GUM * BUBBLE/KIDS/NOVELTY TYPES- (0200) 360959 TRIDENT GUM S/F ISLAND BERRY 12/BX 530324 AIRHEAD GUM BL RASPBERRY 14PC 12/BX 360906 TRIDENT GUM S/F MINT BLISS 12/BX 530320 AIRHEAD GUM CHERRY 14 PC 12/BOX 360913 TRIDENT GUM S/F MINT SW TWST 12/BOX 530322 AIRHEAD GUM WATERMELON 14 PC 12/BOX 360951 TRIDENT GUM S/F ORIGINAL 12/BOX 350250 BIG LEAGUE CHEW GRAPE 12/BOX 361003 TRIDENT GUM S/F PASSION FRT 12/BOX 350202 BIG LEAGUE CHEW GIRL 12/BOX 360919 TRIDENT GUM S/F PEPPERMINT 12/BOX 350200 BIG LEAGUE CHEW ORIGINAL 12/BOX 360901 TRIDENT GUM S/F SPEARMINT 12/BOX 350170 BIG LEAGUE CHEW SOUR APPLE 12/BOX 360911 TRIDENT GUM S/F TROPIC TWIST 12/BX 350160 BIG LEAGUE CHEW WATERMELON 12/BOX 360957 TRIDENT GUM S/F WINTERGREEN 12/BOX 350174 BIG LEAGUE CHEW 5-BALL GRAPE 18/BOX 360962 TRIDENT GUM S/F WTR/MLN TWIST 12/BX 350176 BIG LEAGUE CHEW 5-BALL ORIG 18/BX 361031 TRIDENT LAYERS CHERRY + LIME 12/BX 750300 BUBBLE TAPE BUBBLE GUM 24/BOX 361026 TRIDENT LAYERS GRAPE+LEMONADE 12/BX 350400 BUBBLE YUM REGULAR 18/BOX 361020 TRIDENT LAYERS SBERRY/CITRUS 12/BX 350778 BUBBLICIOUS BUBBLE GUM 18/BOX 361035 TRIDENT LAYERS W-MELON/TROPIC 12/BX 350710 BUBBLICIOUS GONZO GRAPE 18/BOX 326001 WRIG "5" ASCENT PTP 10/BX 350900 BUBBLICIOUS S/BERRY SPLASH 18/BOX 326010 WRIG "5" COBALT PTP 10/BX 350950 BUBBLICIOUS WATERMELON 18/BOX 327040 WRIG "5" PRISM WATERMELON PTP 10/BX 351030 HUBBA BUBBA MAX SB/WM 18/BOX 326020 WRIG "5" RAIN PTP 10/BX 351015 HUBBA BUBBA ORIGINAL 18/BOX 328005 WRIG "5" REACT MINT PTP 10/BX 351452 RAINBLO -

The Cadbury Foundation Donates €56000 to Support

23rd October 2017: The Cadbury Foundation donates €56,000 to support Aware’s ‘Beat the Blues’ initiative The Cadbury Foundation, which has been in operation for over 80 years, has donated €56,000 to Irish mental health organisation and Cadbury Ireland charity partner, Aware, to support their ‘Beat the Blues’ initiative for secondary schools. A positive mental health programme, Beat the Blues is aimed at senior cycle students throughout Ireland. Delivered over two class periods, the programme is designed to teach students about mental health and equip them with the tools to deal with life’s challenges. Speaking about The Cadbury Foundation donation to Aware, Eoin Kellett, Managing Director at Mondelez Ireland said: “The whole team at Cadbury Ireland is very proud of our association with Aware and all of the positive work they do around mental health in Ireland. The ‘Beat the Blues’ programme is one of many great initiatives that Aware implements every year. It is so important to educate younger generations about the early signs of mental health issues and to equip them with the knowledge they need to care for their mental health. All too often, we hear of tragic circumstances arising from young people suffering with mental health issues. This programme opens the door for young people to talk about mental health and we are honoured to support such an important initiative.” To mark the donation, Eoin Kellett, Gerry O’Brien, Head of Fundraising at Aware, and Dublin football legend and Aware ambassador, Bernard Brogan, paid a visit to Larkin Community College, Cathal Brugha Street, Dublin 1, to join Bernard’s fellow Dublin teammate and Aware mental health trainer, Kevin McManamon, where he was delivering a ‘Beat The Blues’ talk to the school’s students.